Daniel Black

Daniel Black

Hello,

Be thankful for what you’ve got. That’s the message apparently coming from PE firms reacting to problems in the global economy.

The FT reported this week that funds are pausing dealmaking and going “risk off”. Instead they’re giving more attention to their existing portfolio companies as they wait for things to settle and the market to pick up again.

In other news:

- KKR is nearing a deal to buy OSTTRA for about $3 billion

- Barclays has struck a deal to offload its payments business

- Morgan Stanley hiked bonuses by 67% for top UK bankers

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- UK economy beats expectations in February with 0.5% growth

- UK inflation falls more than expected to 2.6% in March

- UK consumers plan to ‘buy British’ as Trump’s trade war bites, survey shows

- Stocks rise again on talk of auto sector tariff support

- Which UK stocks are most at risk from Trump tariffs?

- Private equity goes ‘risk off’ as it pauses dealmaking

- Gerry Cardinale’s RedBird evaluates takeover of UK’s Telegraph newspaper

- Belgian insurer Ageas agrees £1.3bn deal for Esure

- KKR nears deal to buy OSTTRA for about $3 billion

- Lotus Technology is to acquire majority stake in Lotus UK from Geely

- Two funds managed by UK’s Foresight Group LLP are set to buy Harmony Energy in £210m deal

- Abu Dhabi’s Mubadala to buy £528.3m stake in UK school operator Nord Anglia

- Abu Dhabi’s Taqa agrees to buy Transmission Investment

- UAE’s Sidara bids £242m for Wood Group after offering £1.5bn last year

- De La Rue accepts £263m bid by Atlas

- MP Evans inks deal for takeover of two Indonesian plantation companies

- Reckitt homecare suitors temper valuations amid tariff worries

- Flutter receives regulatory approval for Snai acquisition

- Barclays and Brookfield agree to offload bank’s payment unit

- Playtech plans special dividend as Snaitech sale completes

- UK’s Haleon takes full control of Chinese consumer healthcare venture

- Tullow Oil sells Kenya interests for £90.7m to Gulf Energy

- Bakkavor gives Greencore more time to make firm takeover offer

- Niox shares fall as Keensight Capital backs away from takeover deal

- Urban Logistics confirms offer terms of LondonMetric takeover approach

- Helical seals £333m London sale

- LondonMetric boosts bid for UK’s Urban Logistics REIT to £670.2m

- Takeover of BBGI Global Infrastructure awaits UK approval

- Science in Sport receives takeover bid from bd-capital

- Velocity Capital to acquire ownership stake in Unique Sports Group

Salaries and bonuses

- Newton Investment Management lags UK peers on gender pay gap

- Morgan Stanley hikes bonuses for top UK investment bankers by 67%

Job moves

Market trends

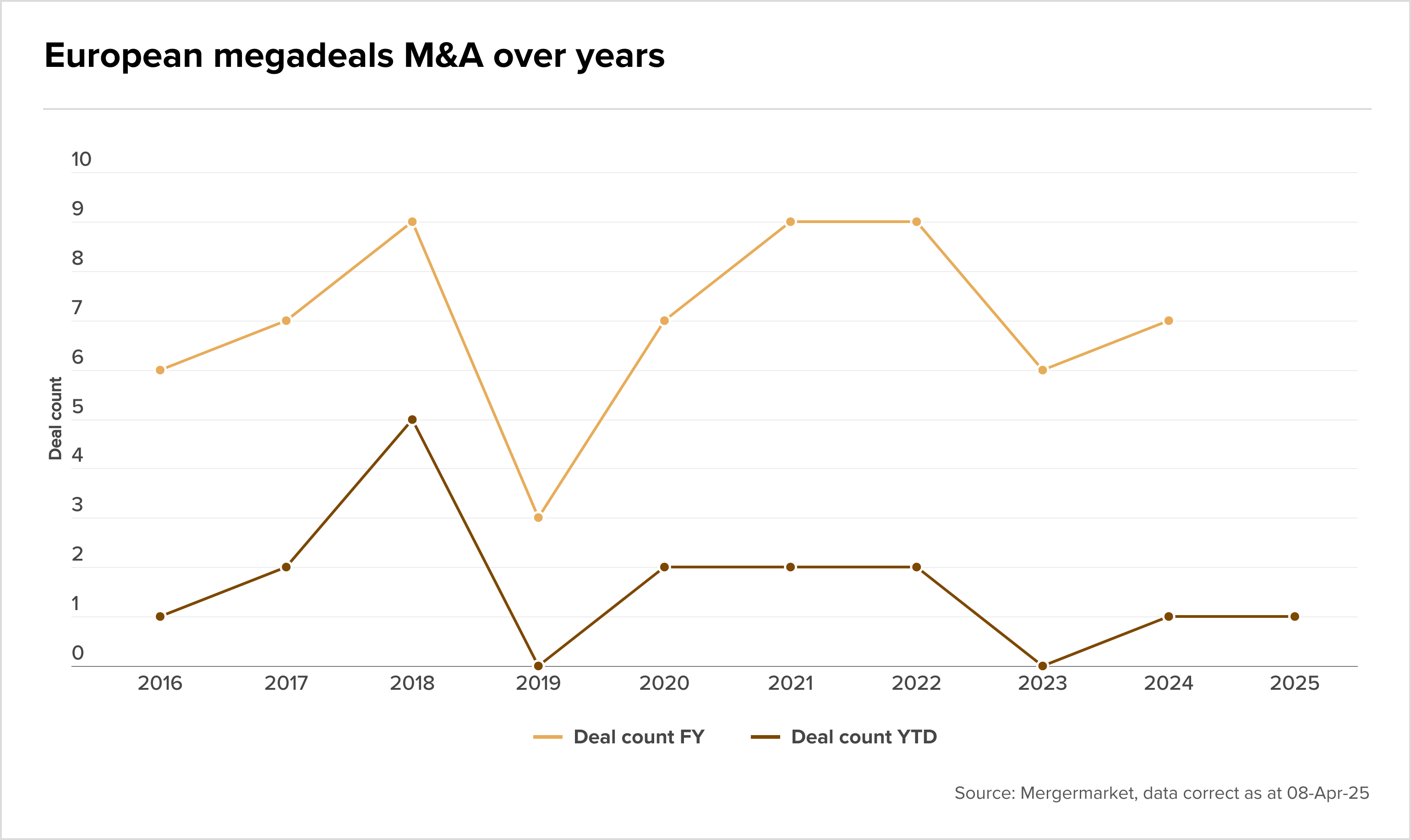

JVs step up as Europe’s megadeals face headwinds

In today’s uncertain macroeconomic landscape, volatility and trade tensions have put traditional megadeals on ice. Of the 68 €10bn+ megadeals in Europe over the past decade, most have been strategic moves, yet few recent transactions match the scale of historic giants like AB InBev’s $119bn SABMiller acquisition.

European joint ventures are quietly emerging as a viable alternative, according to Mergermarket. These large-scale collaborations allow companies to share both valuation risk and strategic upside – an appealing formula in the environment where full takeovers seem too bold.

In sectors like automotives and defence, such a model is increasingly attractive, due to uncertain timings and capital-intensive transformations. For example, Rheinmetall’s growing JV strategy in defence signals how industries under geopolitical pressure are pivoting.

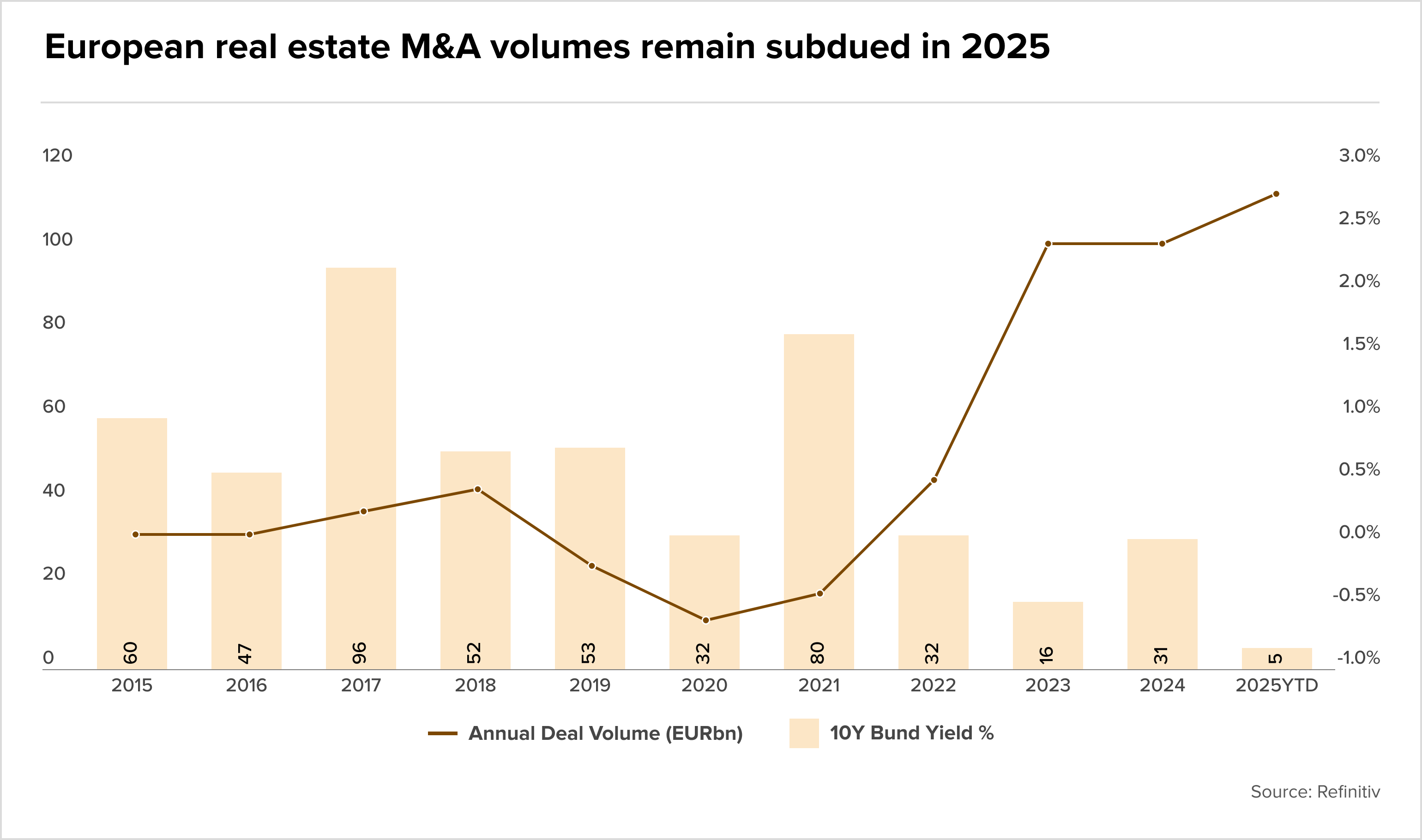

Tariffs dampen European real estate M&A

Analysis from ING shows that the hoped-for revival in European real estate M&A is yet to materialise. While deals doubled in 2024, hitting €31bn, momentum has faltered in early 2025. The tariff turbulence did not bypass this sectors’ deal volumes either, which remain well below the €50bn 10-year average.

Looking ahead, easing interest rates and a shift in global capital flows – notably the “Sell America” trend – could support a pickup in activity later in the year. With nearly €400bn in global real estate dry powder, the foundations for a pick-up are there.

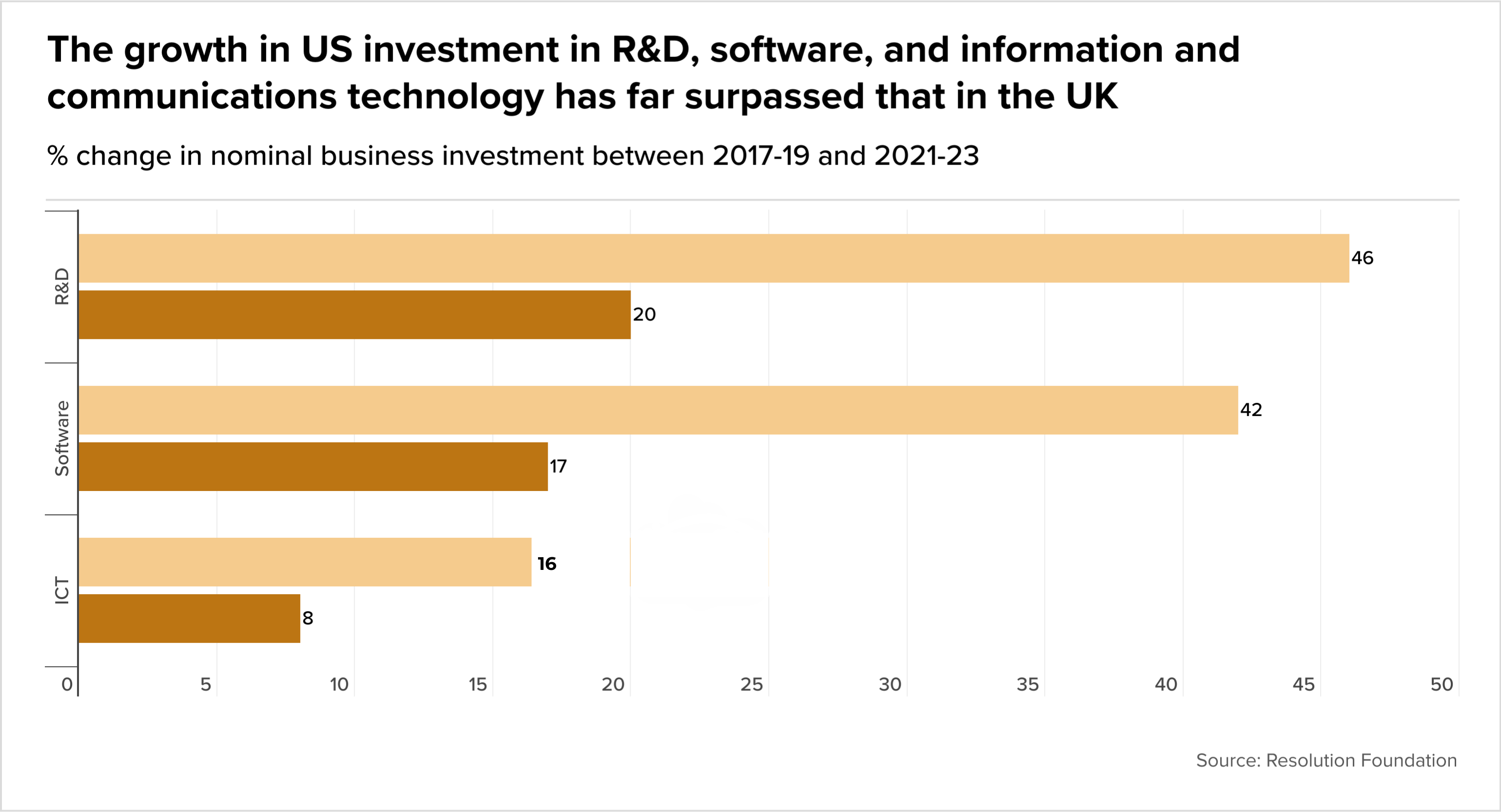

Lacking in the productivity stakes

Britain’s productivity malaise is nothing new – but global headwinds are making the current picture even bleaker. New data reported in the FT shows that UK labour productivity has grown by just 5.9% since 2007. Real wages – only by 2.2%. By comparison, in the 17 years prior, both figures were closer to 40%.

Furthermore, productivity has actually declined since 2019 in sectors that account for almost two-thirds of UK output. The US meanwhile, has pulled ahead – not just thanks to its tech giants, but because technology adoption across industries has accelerated, backed by the serious investment in R&D and software.

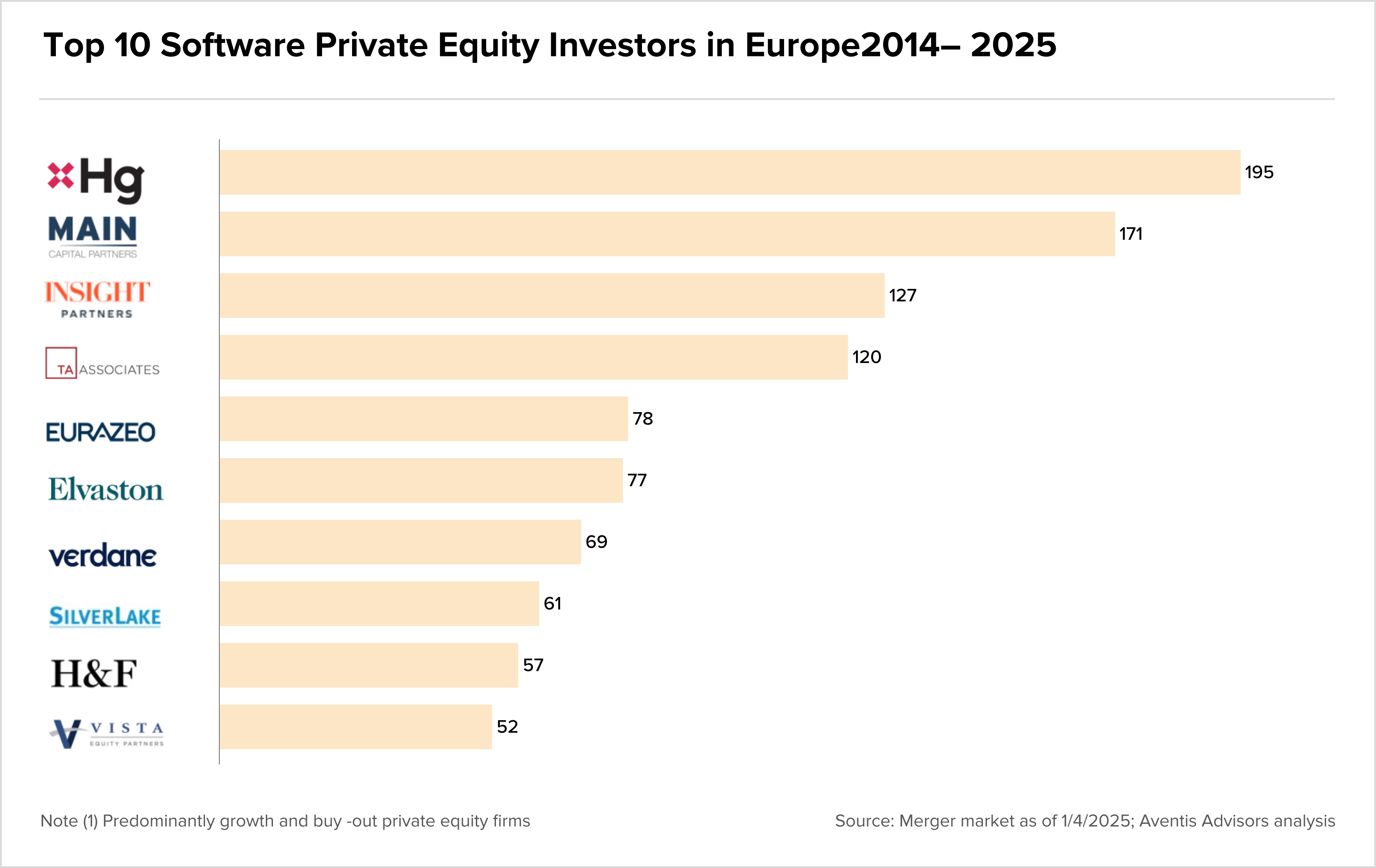

Hg tops the list of most active PE firms in software

Aventis Advisors has published an interesting analysis of the most active PE firms in the software space. It shows that PE appetite for European software remains strong, with the top five most active firms responsible for over 5% of all software deals in the region since 2014. Hg leads the list, followed by Main Capital, Insight Partners, and TA Associates.

Despite ongoing macroeconomic uncertainty, deal volume has held steady. With most firms focused on mid to large-cap targets, there’s a growing interest in sectors like enterprise SaaS, cybersecurity, and infrastructure software.

Separately, you can read our recent interview with Filip Drazdou, an M&A advisor at Aventis Advisors, which focuses on European tech M&A trends.

IPOs