Harsh Batra

Harsh Batra

Hello,

What’s new this week in Indian M&A?

The financial services landscape continues to hum thanks to a major bank-led M&A play. Japan’s Sumitomo Mitsui deepened its India bet with a $1.6 billion stake in Yes Bank, boosting investor confidence and bank stock momentum.

SEBI gave AIF managers a breather by extending the certification deadline for PE managers, as fund formation activity remains high.

Meanwhile, capital deployment also remains strong: A91 Partners closed its third fund at $665 million, as Everstone neared a $400 million first close.

Finally, India’s drone game got a lift as Garuda Aerospace raised $11.98 million in Series B, with eyes on global expansion and a beefed-up tech stack.

It appears a new wave of specialised capital is remaking the rules, whether it’s backing drones, banks, or debt plays, just as the regulator fine-tunes the fund framework for the next cycle.

I hope you enjoy this week’s roundup, and please do connect with me on LinkedIn to find out how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in India.

Market Trends

What does court ruling mean for private credit markets and the IBC?

India’s Supreme Court did something unusual in April—it sent a deal back, not forward. It reversed JSW Steel’s $2.4 billion resolution plan for Bhushan Power & Steel (BPSL), a transaction long thought closed with protection under India’s insolvency code.

JSW had taken over the company in 2019, but the court found fatal flaws. It noted the buyer failed to disclose ongoing criminal investigations involving the former owners of the target company, missed a legal deadline, and that creditors approved the deal without fully vetting these issues. The judges ruled in favour of the dissatisfied creditors, ordering a liquidation of BPSL, and asked the banks to return the recovered funds.

The ruling sparked anxiety among investors and debtors, some called it a shock ruling. But that’s an overreaction. This wasn’t a surprise so much as a signal that shortcuts under the IBC process will not fly.

In contrast, Tata Steel’s $4.2 billion acquisition of Bhushan Steel in 2018 still stands as the IBC’s gold standard. It followed deadlines, cleared disclosures, and helped lenders recover with a minimal haircut (37% compared to JSW’s 58%). The result: a clean resolution, a functioning asset, and a new benchmark for distressed M&A.

For India Inc., where family ownership is common and corporate governance can vary widely, it’s clear that bending compliance timelines or dodging disclosures, however well-intentioned or pragmatic, can undermine trust. The ruling is a reminder that due process is not optional, and that workarounds cost time and money.

Over 1,800 cases are active under the IBC today and India’s private capital machine is still running, driven in part by these assets. By 2024-end more than 1,000 businesses had been rescued, restored or taken over, leading to payouts of $42 billion to creditors, Reuters reported.

The court oversight is considerable but so are the stakes. The authorities know that global investors price in more than just asset value and will ensure the robust IBC-facilitated M&A model holds up.

Indian businesses must factor in legal discipline, and with regulators chipping away to perfect the process since 2016, demand that resolution candidates now pass the next stress test—the rule of law.

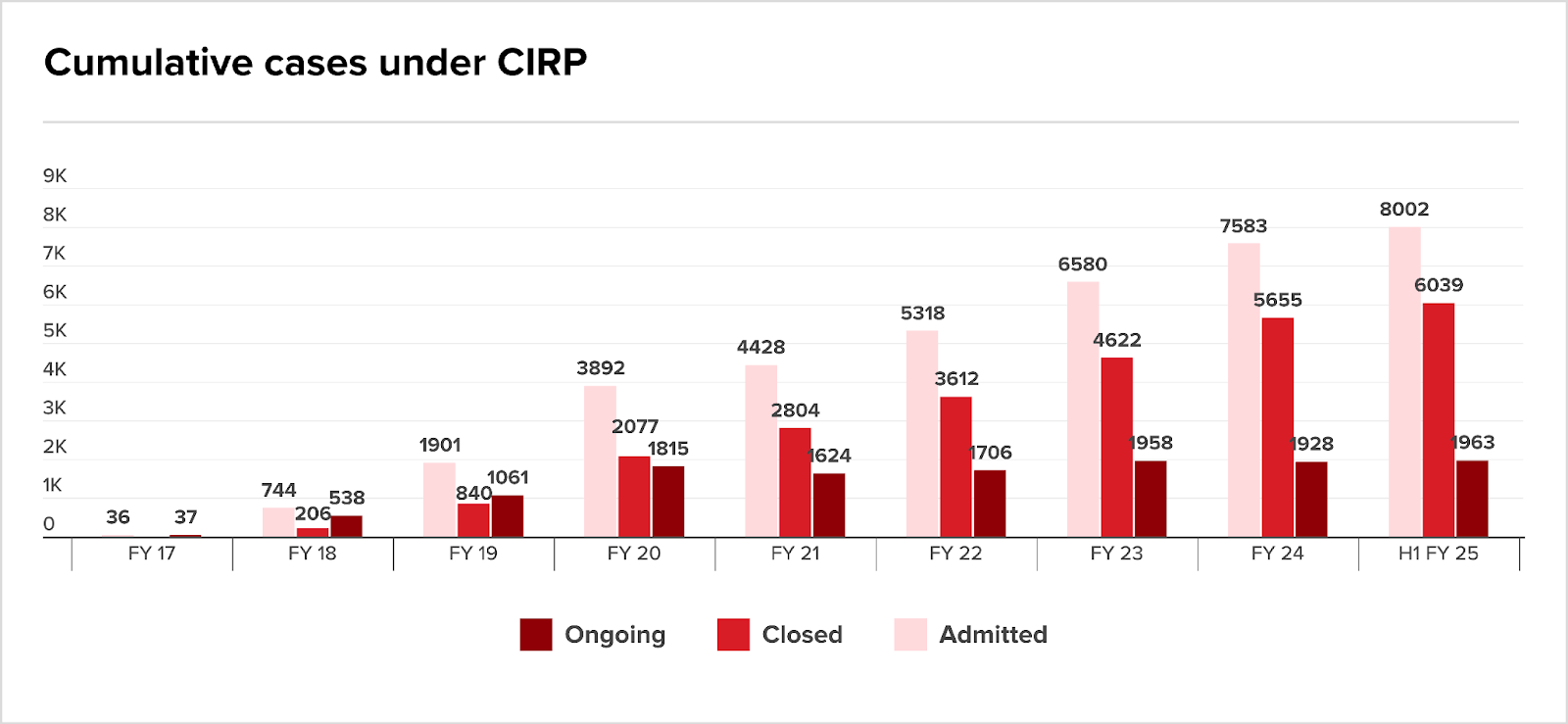

The story so far in numbers

Since the IBC’s inception in 2016, India’s insolvency ecosystem has matured significantly. More than 8,000 insolvency cases have been admitted, a sixfold increase since FY19 alone.

Source: EY

While closures have picked up pace (now over 6,000), the number of ongoing cases has plateaued around 1,900 while the gap between admissions and resolutions has widened.

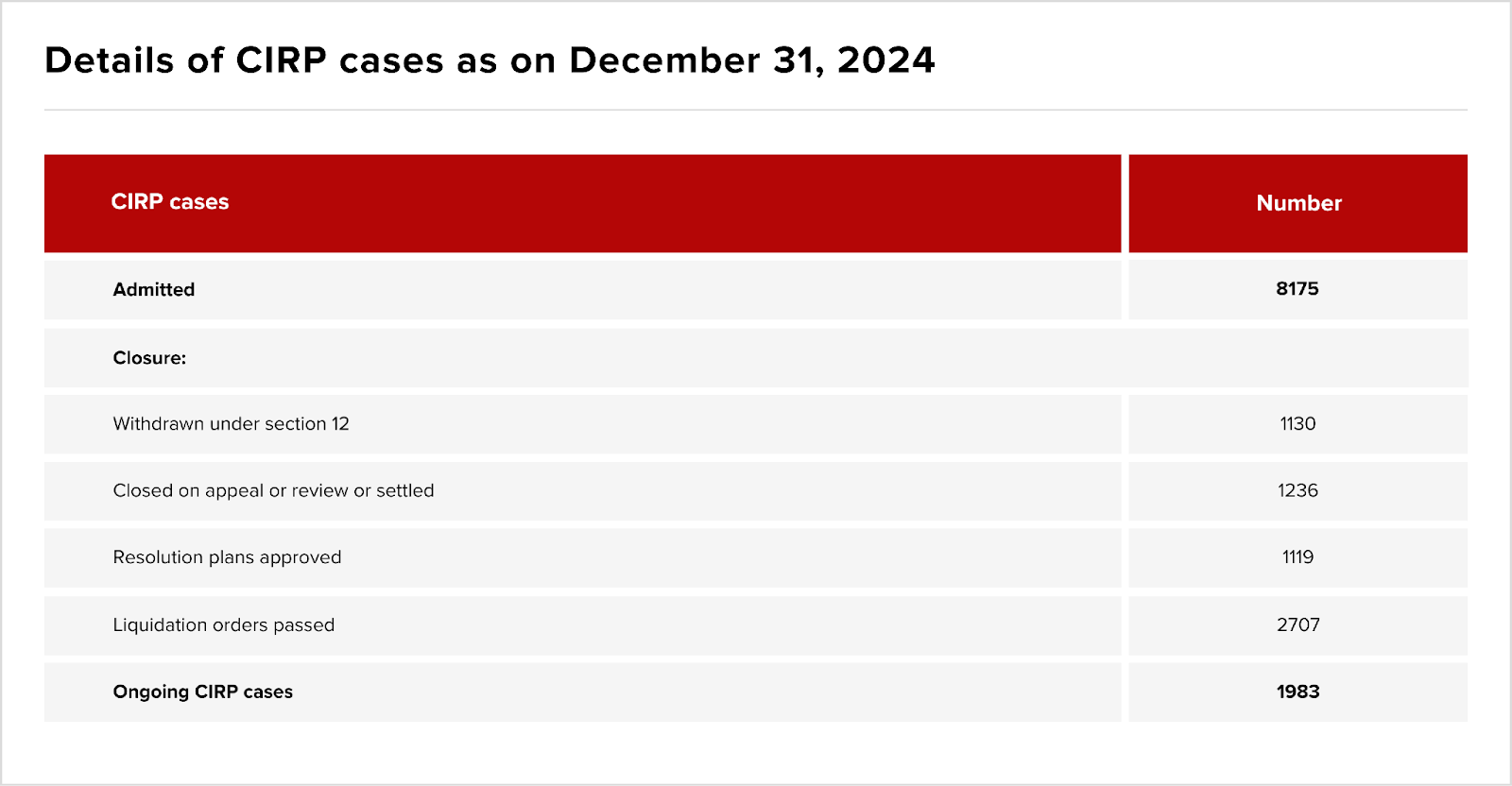

How cases are closing

Liquidation and resolution or settlements are split almost equally. This may reflect lingering issues with asset quality and investor appetite, especially for MSMEs and real estate entities (the sector with the most insolvency filings).

Source: Insolvency and Bankruptcy Board of India (IBBI)

According to an EY report, the ratio of resolution to liquidation orders under IBC in FY18 was just 0.21, meaning that for every five companies liquidated, only one company was successfully resolved through a formal plan. By FY24, the ratio had climbed to 0.61, or six resolutions for every 10 liquidations, reflecting improvement in recovery outcomes: more companies are being revived than written off.

This shift points to growing maturity in India’s insolvency ecosystem. More resolution applicants are stepping in, creditors are increasingly choosing resolution over liquidation, and legal processes are working, if slowly.

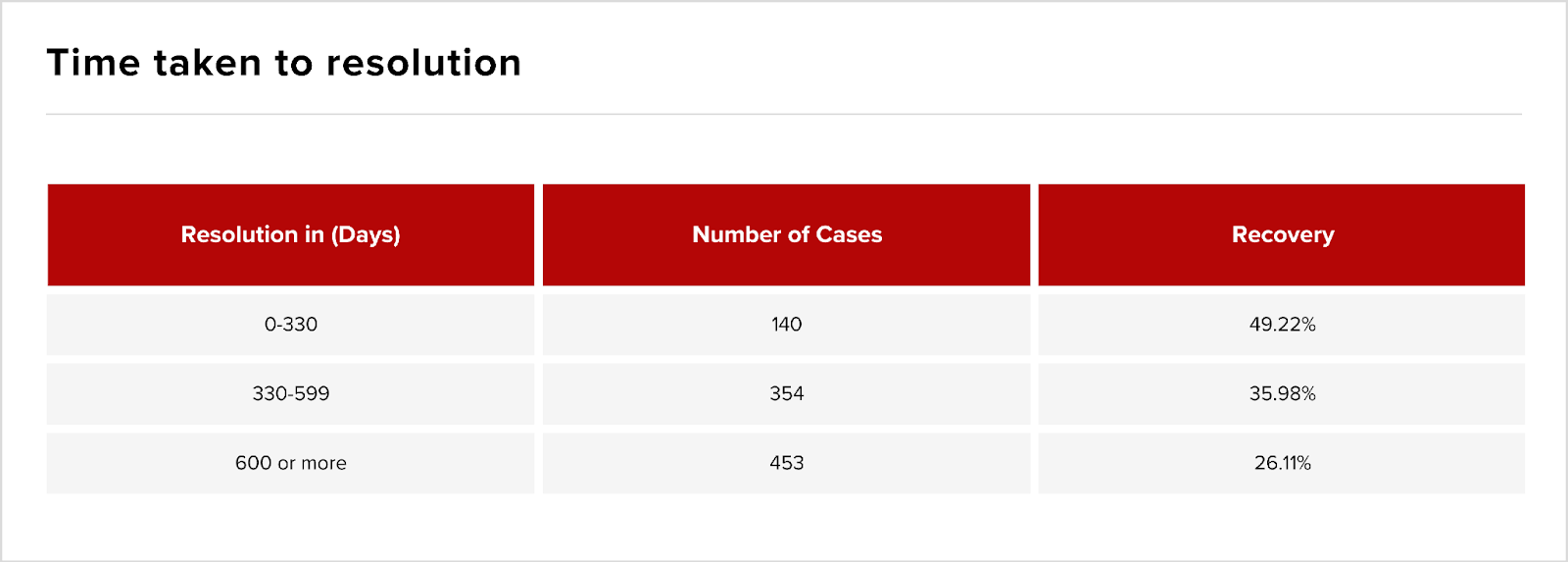

The time to resolution remains stubbornly high. Over 60% of resolved cases exceed the statutory 330-day limit, though things are improving:

Source: IBBI

Market trends suggest that distressed M&A is no longer just a last resort, but an active investment strategy.

The rumour mill

- Mining & Infrastructure Company Board Approves Rs 107 Crore Stake Sale In IDL Explosives Subsidiary to Apollo Defence Industries

- GOCL Corporation to sell entire stake in subsidiary IDL Explosives for ₹107 crore

- Aramco eyes 20% stake in ONGC, BPCL mega oil projects

- Sojitz, IOC-GPS JV eyes $400M for 30 biomethane facilities

- Bharti Airtel and TATA Group End Merger Talks

- Macrotech Developers to launch Rs 19k crore housing projects this fiscal

- Nirala World-backed AIF to invest Rs 2,000 crore in distressed real estate projects

- JSW MG Motors sets in motion up to $350 million fund raise from PE investors

- State Bank of India to raise funds via share sale this fiscal year

- Order in respect of Cinema Capital Venture Fund

- KFin Technologies shares in focus as General Atlantic plans 6% stake sale via block deals

- Block deal: KFin Tech shares in focus as promoter eyes 6% stake sale today

- Deutsche Bank’s DWS and Japan’s Nippon Life in talks on India venture

- India and Japan drive revenue growth among top 20 APAC banks as Chinese giants slow down, reveals GlobalData

- Quest Global in 2023, is considering an initial public offering of Quest Global Services in India

- SMBC nears YES Bank stake deal; India may see biggest private bank M&A

- Biggest ever banking M&A deal? Japanese banking giant Sumitomo Mitsui closer to taking control of Yes Bank, in talks with SBI to buy stake.

- Yes Bank says stake sale talks are still in preliminary stag ..

- India has already agreed to drop its high tariffs to nothing: Donald Trump

- SAT denies interim relief to Gensol in Sebi fraud case, reply due in 2 wks

- Nuvini Group advances with AI and M&A strategy

- India’s capital is coming home & and it’s not stopping at the Sensex

- SCHOTT Pharma and Serum Institute of India welcome new partner to Joint Venture in India; TPG makes strategic investment in SCHOTT Poonawalla

- Indian Aletrnative Investment Fund managers hit a pause on public equities in Q1

- Manipal, Max Healthcare, and KKR Line Up to Bid for Sahyadri Hospitals

- Adani group stocks surge up to 14% on reports of Gautam Adani’s representatives meeting trump officials

- No change imminent to foeign nvestment strategy in Space InSpace’s Pawan Goenka

- Actis: India’s energy transition gains momentum

- TPG to buy Schott Poonawalla from Serum Institute

- SMBC said to be in talks to buy significant stake in India’s Yes Bank

- AU Small Finance Bank Block Deal: Private Equity Firms To Sell Shares Up To Rs 600 Crore

- Vedanta mulls Zambian copper biz listing in US among fundraising options

- India offers zero-for-zero tariffs on auto parts, steel from US

- IDBI Bank Stake Sale to Be Completed in 2025: Who Are the Bidders in the Race

- IDBI Sale On Track, LIC Stake Dilution By FY27, Says DIPAM Secretary — NDTV Profit Exclusive

- Fintech-focused VC firm QED Investors eyes India in $300 mn Asia push

- Paras Defence to build India’s first optics park in Maharashtra with ₹12,000 crore investment

- Oil India in talks with global majors for joint E&P bids, says CMD Ranjit Rath

- Indian regulator accuses Adani nephew in insider trading case, he seeks to settle

- India, Angola decide to expand energy partnership

M&A news

- BII invests $100m in ReNew photovoltaics, its first solar bet in India

- Jubilant Beverages get CCI nod to acquire 40 pc stake in Hindustan Coca-Cola

- India’s liberal FDI policy offers huge investment opportunities for global investors: Deloitte

- Resolution to ruin: Supreme Court’s Bhushan Power ruling jolts IBC playbook

- Penny stock below Re 1: NBFC stock in focus after ₹50 crore fundraise via issuance of NCDs

- EY: India secures 22% of global IPO share in Q1 2025 with 62 listings raising $2.8 billion

- Private capital expenditure in India remains sluggish in Q4FY25, despite overall rise in new projects: Report

- Investors find their way back to retail and consumer checkout aisle

- Indian startups raised over $102 million from April 28 to May 03, 2025; Kult tops the list

- Dixon Technologies and Inventec Form Joint Venture to Manufacture PCs and Servers in India

- Singhania acts for Value Angels on Urbanaut investment

- Private capex: Corporate caution risks stalling India’s investment engine

- PE and the growth story

- Supreme Court Reverses JSW Steel’s Acquisition Of Bhushan Power, Orders Liquidation

- Aurum Proptech Trims Losses in Full Year Results

- NB Housing shares jump 7% as Carlyle likely sells 10.44% stake via block deal

- Bulk & Block deals: Quality Investment Holdings exits PNB Housing Finance with 10.43% stake sale

- Artha Global Opportunities Fund nets 6X return from investments in distressed assets

- india-market-buzz-banks-seize-bullish-mood-for-fundraising-push

- India’s $14 Billion Medical Tourism Boom: A Strategic Push Towards a Global Healthcare Hub

- 1 share becomes 10: Bajaj Finance unleashes bonus bonanza and stock split surprise

- Indus Towers Sees Marginal Q4 Profit Decline Amid Airtel Tower Deal, Finance Expenses

- Adani Enterprises Q4 profit jumps 7.5x on Wilmar stake sale, strong growth in solar mfg

- Schibsted shares jump 10% after Q1 profit rise, divestment plans

- Biohaven directors re-elected, EY appointed as auditors

- Union Bank probing lapses in procurement of Subramanian’s book worth Rs 7.25 crore

- TVS to Launch Norton Bikes in India

- Disney projects $300m equity loss in FY25 from India JV with Reliance

- Merger state-run general insurers back on the table

- Grant Thonrton’s Technology Dealtracker Q1 2025

- Sluggish distribution to push investors towards GP-led continuations amid tariff uncertainty

- India’s Services sector PMI surges to 58.7 in April

- Info Edge pegs Zomato, PB Fintech holdings at $3.7 billion

- Earnings call transcript: TPG Q1 2025 results miss EPS forecast, stock dips

- Algorhythm Holdings Buying SemiCab India To Expand AI Transportation Footprint

- Fed rate freeze sparks anxiety amid tariff turmoil

- Agilent inaugurates India Solution Center to accelerate innovation and expand frontiers of science

- RackBank Announces India’s First AI Data Center Park

- Warburg Pincus lifts stake in India financial services portfolio firm

- Moody’s cuts India’s 2025 GDP growth forecast to 6.3% amidst Trump’s trade tariff uncertainty

- India, Russia Ink Pact on Six Strategic Investment Projects

- RIL, ONGC shares in focus as JV completes India’s first offshore decommissioning

- Actis ropes in key LP for Indian smart metering platform with EDF

- Shell, Reliance & ONGC JV completes India’s first offshore facilities decommissioning project

- India’s Paytm narrows losses marginally in Q4 despite $58m hit from ESOP costs

- India’s posha, Bharatpe, The Good Bug raise funds

- Decarbonising SE Asia presents $50bn in investment opportunity

- India’s defence stocks rally on FY25 order surge, FY26 bullish outlook

- Rehau expands presence with land acquisition in Sri City

- Bulk Deal: Penny stocks jump up to 15% after share worth ₹3 Cr changed hands

- Apollo Micro Systems shares gain over 7% acquiring entire stake in IDL Explosives

- Plum’s Shankar Prasad: The chemical engineer who cultivated a Rs 350cr beauty brand

- Blusmart employees seek legal recourse over unpaid salaries

- Galaxy and e& Capital co-lead $12.2m funding in Fuze and other India deals

- QED shapes Asia playbook with bigger cheques, expanded footprint

Job moves

IPOs

Fundraising

- SG Real Estate Fund raises ₹450 crore, disburses ₹125 crore to revive two stalled real estate projects in Noida

- Anveshan Raises Rs 48 Cr In Series A Round Led By Wipro Ventures

- ASG & Partners, Trilegal and India Juris act on KULT $20 million Series A fundraise

- SGRE Fund raises Rs 450 crore, invested Rs 125 crore across two real estate projects

- Arnya RealEstate Launches Debt-Focused Real Estate AIF, Eyes Rs 1,000 Crore Corpus

- Power Sustainable Lands $330 Million for Private Equity Fund

- 91Trucks Secures $5M Series A Funding Led by Arkam Ventures

- Porter raises $200m led by Kedaara, Wellington; Peak XV, Kae exit

- Avendus raises Rs 1,000 Cr in first close of third private credit fund

- Ex-ArcelorMittal senior exec surges towards $1bn target for latest Synergy Capital fundraise

- Ex-KKR partner’s debut fund said to have bagged over $100m commitments

- Dubai-based Synergy Capital to raise $1bn for third Asia fund, with India focus

- Celebal Tech kicks off Series B round with 2X valuation jump

- HUDCO board approves ₹2,190 crore fundraise via NCDs on private placement basis

- Abraaj Spin-off RMBV gets LP commitment for first independent fund

- Metafin Raises $10M Series A From Vertex Ventures SEAI Leading Finance Platform

- Celcius Logistics raises Rs 250 Cr in Series B funding to expand cold chain network

- Ex-Temasek India executives target $400m for fund debut

- JSW cement backer Synergy Capital hits first close of $1bn private credit fund

- Indian startups raise $102.93 million in funding over the week

- InvAscent mark final close of fourth PE fund at $304m final close

Compliance/regulatory update

- Reversal for the reforms process

- SEBI directs winding up of Cinema Capital Venture Fund over “gross mismanagement”

- India’s 4.4% fiscal deficit target hinges on solid revenue. Global conditions pose a challenge

- Adani pauses talks with Israel’s Tower for $10 billion India chip foray, sources say

- Indian startups’ funding falls to $745 Mn in April: Entrackr report

- India completes merger of 26 Regional Rural Banks across 11 states today

- SEBI Amends Framework For REITs And InvITs To Ease Preferential Issues And Follow-On Offers

- Set Off Under The IBC Regime: Analysing The Judgment In Bharti Airtel vs Vijaykumar v. Iyer

- NSE seeks govt intervention in IPO standoff with Sebi

- Indian court’s reversal of $2.3 billion deal casts shadow on bankruptcy law

- Centre puts merger plans on hold after three weak general insurers post profits

- India urged to investigate “quick commerce” concerns

- India – UK finalise Free Trade Agreement and Double Contribution Convention

- Govt Moving Ahead With IDBI Bank Disinvestment Plan In Current Fiscal

- India-EU trade talks edge towards truce as WTO appeals stall

- RBI eases FPI rules on corporate bonds to boost foreign inflows

- Elon Musk’s Starlink secures crucial approval for India ops

- Govt may begin offloading minor stakes in five PSU banks via OFS in FY27; strategic sale deferred for now

- HDFC Capital Advisors pays Rs 36 lakh to Sebi, settles AIF rule violation case

- RBI may go for jumbo rate cuts this fiscal: SBI

- SEBI bars Synoptics Technologies, promoters for siphoning off IPO funds

- Corporate exit regime: India’s bankruptcy reforms need one final push

- SBI research predicts aggressive rate cuts by RBI in FY26 amid benign inflation

- QED Investors to deploy $300 million in India and Asia Pacific over next five years: Asia head Sandeep Patil

- How a recent RBI move gives foreign firms greater flexibility in M&A deal structuring

- India’s Supreme Court cancels JSW Steel’s acquisition of Bhushan Power

- Finalising response to SC’s decision on JSW Steel-Bhushan deal: Govt officials