Harsh Batra

Harsh Batra

Hello,

Here’s what’s new in Indian M&A this week.

UK-headquartered legal firm CMS has formalised its India ambitions by partnering with domestic deal lawyers, IndusLaw. The move may mean expectation for greater deal flow, innovative commercial structures, and growing post-globalisation regulatory complexity. Indian policymakers take note: the ease of doing business may become a global differentiator.

In new asset classes and regulatory shifts: HK-based TPG NewQuest says continuation vehicles, once a workaround, are now critical to capital raising; markets regulator SEBI tweaked what qualified as Category II AIFs, impacting credit and hybrid vehicles.

But Finance Minister Nirmala Sitharaman pushed for faster clearances while former FM Chidambaram, flagged an alarming rise in cancelled domestic investments i.e. a rise in approved investments that are later shelved or abandoned before execution.

And a quiet goodbye to Shanti Ekambaram, one of the last high-profile women leaders in Indian banking retiring from Kotak.

Hope you enjoy this week’s roundup. Do connect with me on LinkedIn to find out how I may help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in India.

Market Trends

What funding crunch?

The foreign investment flip is real, but so is India’s local resilience

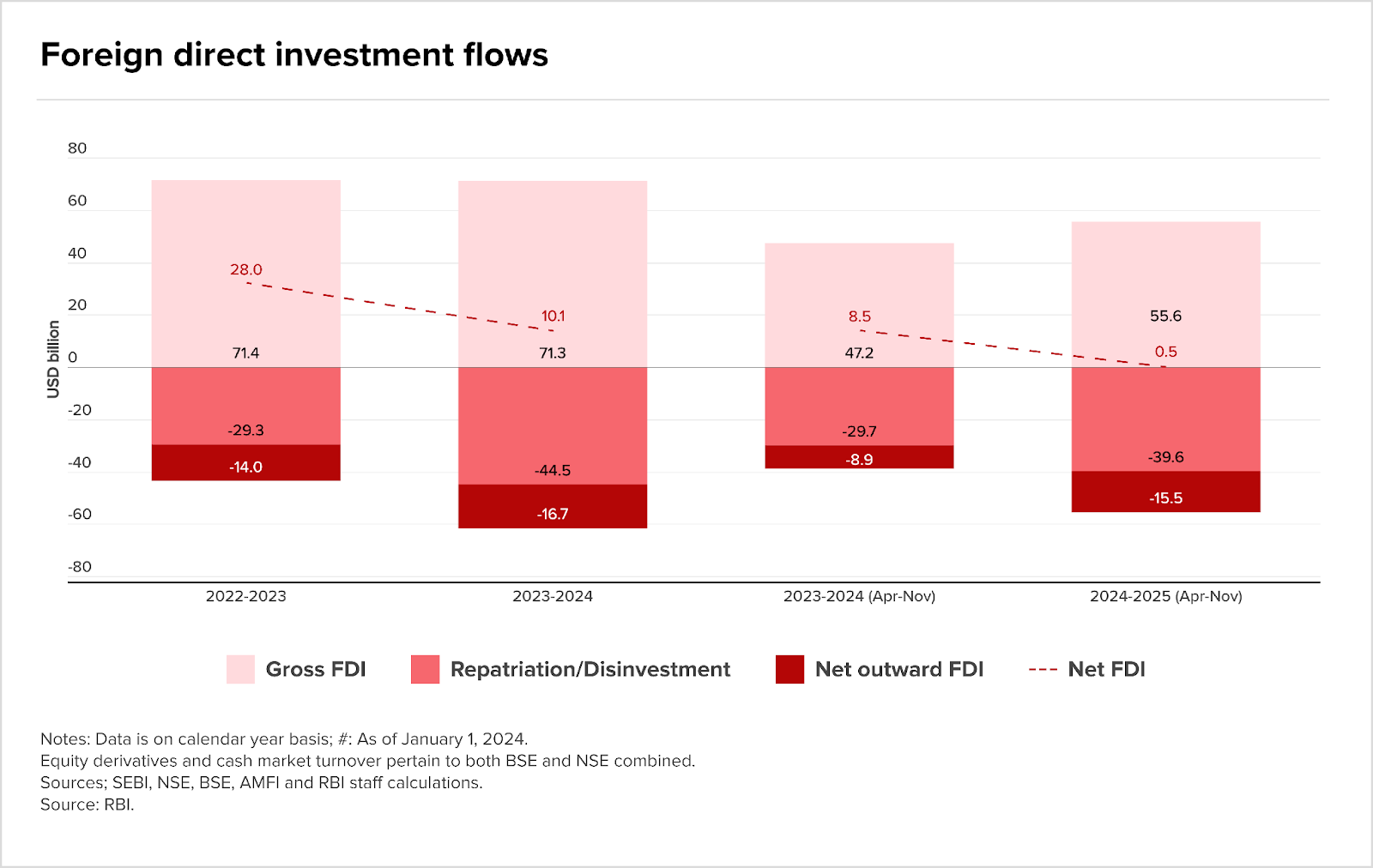

At first glance, India’s foreign investment data paints a picture of drought. RBI numbers show net FDI inflows collapsed by 96.5% in CY25 ($0.49 billion), a headline-grabbing stat that dominated press coverage last week. The collapse, driven by record repatriation and outbound investments, sparked talk of investor exodus but events told a nuanced story.

^^^Net FDI into India turned negative in early 2025 as repatriation and outward investments overtook gross inflows for the first time in a decade.^^^

Source: RBI

The dealmaking hasn’t stopped. Strategic capital is bending over backwards for India-facing assets, while Indian firms make bold outbound bets.

India’s largest auto parts maker Motherson Group is reportedly bidding for Pirelli, the troubled Italian-Japanese supplier to Nissan and Franco-Italian-American automaker Stellantis. If successful, the deal would mark an audacious reverse acquisition that might position the buyer in the top tier of global component makers. While Motherson has faced margin pressure, management appears to be banking on a familiar turnaround logic: two underperformers may outperform when brought together, not unlike domestic conglomerate JSW’s acquisition of Ispat back in 2012.

Also, Mumbai-based digital business services provider Altimetrik is nearing a $614 million acquisition of SLK Software, an AI solutions business.

Meanwhile, JSW Paints, a unit of local conglomerate OP Jindal Group, is scooping up AkzoNobel India’s stake for $1.1 billion: inbound play wrapped in compliance with new Minimum Public Shareholding (MPS) norms which require at least 25% public float in listed firms. This will lead to many family-owned businesses toward greater institutional discipline.

Rakesh Gangwal’s family trust offloaded a 5.72% stake in low-cost airline IndiGo, unlocking ₹11,564 crore ($1.39 billion) , correcting earlier reports that cited a sale of 3.4% and ₹11,988 crore ($1.44 billion). Gangwal, an Indian-born US citizen, has hinted at more strategic divestments in the pipeline.

Other telling signs of maturity: The National Stock Exchange just paid a record $118 million to settle with SEBI, paving the way for a long-delayed IPO; and a British American Tobacco $1.36 billion-block deal in Indian consumer goods firm ITC is imminent. They claim there are plans for further stake reduction.

In private credit and structured debt fundraising, India continues to outperform: Multiples PE closed a $430 million continuation fund, bucking the broader pullback.

Also Quadria Capital, a healthcare-focussed PE firm with a strong India-Asia footprint, secured $1.07 billion for its third vehicle; and debutant Enko Capital, is receiving LP commitments for its first private credit fund.

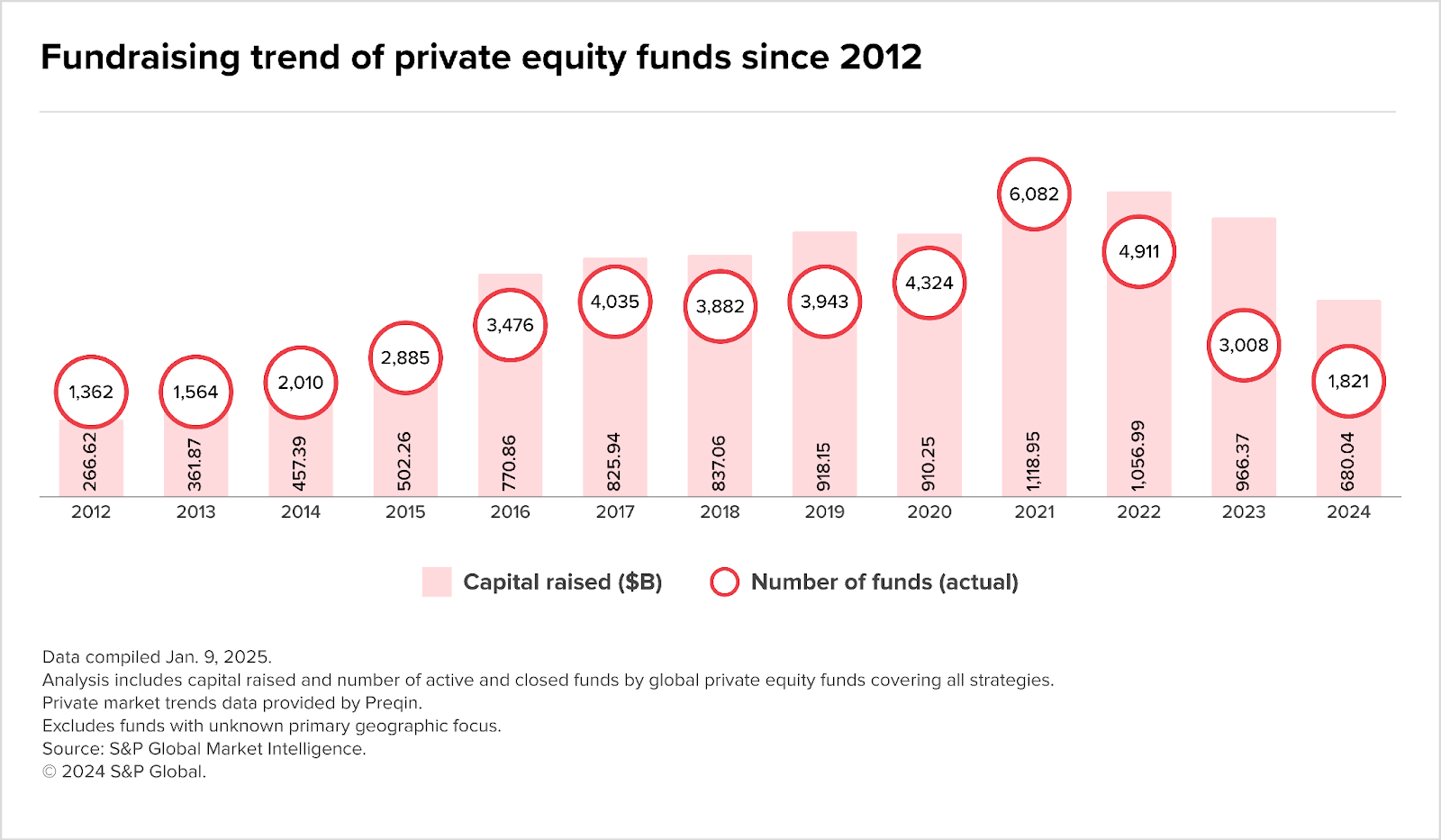

Globally, the contrast is stark. According to Bloomberg and S&P, 2024–25 marks the sharpest drop in deals in a decade (see chart below), with fewer funds returning capital to LPs and exits becoming rarer, too.

^^After peaking in 2021, PE fundraising volumes and the number of funds globally are both on a downward trend, with a sharp fall in 2024.^^^

Source: S&P Global

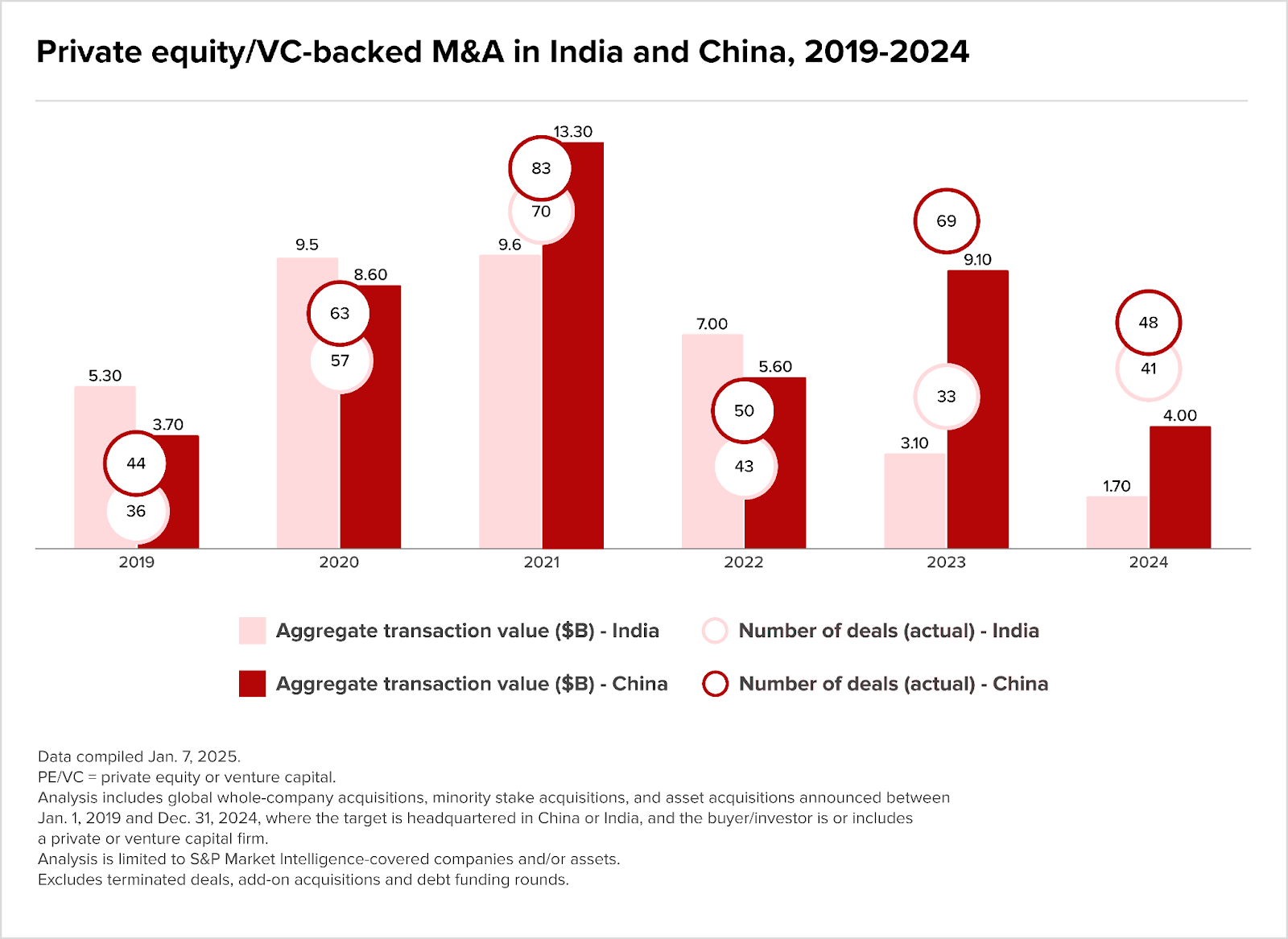

While global funds pull back, India is pivoting from control-focused PE to credit and hybrid structures– a response to liquidity mismatches and glacial resolutions under India’s 2016 Insolvency and Bankruptcy Code (IBC).

The country diverges again compared to its next-door rival China, still buoyed by state-led capital and cloistered access while India’s pitch rests on private initiative, domestic consumption, and openness to global LPs.

Source: S&P Global Market Intelligence (excludes terminated deals, add-on acquisitions and debt funding rounds; only funds HQ’d in China or India).

Policymakers, including central bank RBI, have framed the declining inflows as an inevitable sign of a maturing market, a correction, rather than a cause for alarm.

Deals lawyer, Zia Mody, founding partner at Indian legal firm AZB & Partners, too, remarked that it’s creative deal structures that are keeping Indian M&A upbeat.

That said, some of this churn could be disguised round tripping, where capital leaves only to re-enter via more favourable channels. Mauritius, Singapore, and the Netherlands have consistently ranked among the top sources of FDI inflows thanks to tax treaties and secrecy laws. As the IMF once described it, some of this may be ‘phantom FDI.’

But from NSE’s regulatory clearance, to regulators greenlighting Myntra and Groww, Investcorp’s 4x return from selling fashion retailer Citykart to A91 and NewQuest, and a $65 million Series B that valued the shop at $169 million; there’s little reason to fear the capital crunch is near. Or at least, not the kind that dims animal spirits.

The rumour mill

- Adani Energy nod for Rs 4.3k crore share sale

- India’s Motherson eyes top 10 in auto parts with Marelli bid

- India approves HCL, Foxconn JV for 6th semiconductor unit

- Embassy Developments proposes Rs 3,700 cr commercial project divestment to Embassy REIT in Bengaluru

- IndiGo co-founder Rakesh Gangwal to sell part of stake in deal worth $800 million: Report

- IndiGo shares slip 3% as co-founder Rakesh Gangwal likely offloads Rs 11,988 crore stake via block deal

- Why are private sector banks rapidly gaining market share over public banks?

- Yes Bank shares jump 6% on fundraising buzz; board meet set for June 3

- Altimetrik nears Rs5100 crore acquisition of SLK Software

- BDO India in talks with private equity companies to raise growth capital

- Rate cut expected, RBI’s views in focus with economy near a sizzle

- House of cards: Roll-up ecommerce model stumbles as founders reclaim brands amid funding struggles

- Niva Bupa Shares Tank 10% As Promoters Plan 7.2% Stake Sale Via Block Deals On Monday

- ConnectM Finalizes Acquisition of Cambridge Energy Resources, Expands in India After Nasdaq Delisting

- EC clears stake sale of Siemens Gamesa’s Indian wind biz

- RBI may go for jumbo rate cut of 50 bps on Friday: SBI research

- Adani Energy nod for Rs4.3k crore share sale

- Bajaj Group get CCI’s clearance to acquire Allianz’s stakes in insurance joint ventures for Rs 24180 crore

- JSW Paints to acquire AkzoNobel India stake for $1.1-billion

- Paint stock crashes after venture capital firm offloads its entire 3.18% stake in the company

- Adani Energy board approves $502 million fundraise via share sale

- ITC’s top investor BAT considering further stake sale in Indian FMCG major

- In the works: Motherson Group’s offer to acquire Marelli Holdings

- Toyota Industries likely to accept $42 billion takeover bid by group firms

- OFS today: Sagility India promoter to sell 15.02% stake; all eyes on non-retail bids

- Golden Growth Fund, Grovy India invest in three projects worth Rs 180 crore in South Delhi

- Behind Accor’s plans to expand its hotel business in India through partnerships

- Dhan in talks to raise $200m from Chryscapital Alpha Wave

- India’s Jubilant Bhartia taps debt route to buy stake in Hindustan Coca-Cola Holdings

- KKR commits $600m to Manipal Group in its largest India credit deal

- India’s Tenet eyes stake sale to fund growth plans diagnostics Veda fundraise

- Vodafone Idea share price target after Q4 results 2025 and fundraise plans

- IFB Agro to acquire Cargill India’s aquafeed business

- BYJU’S 3.0 is back: Can the edtech company reclaim the trust Byju Raveendran has lost?

- Indian-origin man creates fake founder persona, tricks 27 investors: ‘This game is rigged’

- Flipkart Plans ₹582 Crore Exit from Aditya Birla Fashion Stake

- SeQuent–Viyash merger receives stock exchange approvals; NCLT filing underway

- Legal reforms in India’s oil & gas sector to unlock strategic investment potential

- Adani Energy to raise $502 million through stake sale

- IndiGo shares to be in focus as Rakesh Gangwal is likely to sell stake worth ₹6,831 crore via block deal

- Private Credit Funds Target Billions in Retail Demand From Asia

- It isn’t just PE, sovereign wealth funds want a piece of the wealth management business

- Emirates NBD likely top contender for IDBI Bank stake, DIPAM said to have explored valuations with potential bidders

- Whirlpool puts up a decent show amid parent’s stake sale overhang

- ACQUISITION? THIS British company is attracting interest from Mukesh Ambani’s Reliance Industries

- Unacademy Cofounders To Take A Backseat, Eye Spinoff For Duolingo Competitor

- ITC stake sale: BAT evaluates disposal of ‘small part’ via on-market trade, says this

- Bharti Airtel and TATA Group End Merger Talks

- Positive start likely for markets ahead of RBI interest rate decision

- CCI approves proposed acquisition of The Interpublic Group of Companies, Inc. by Omnicom Group Inc.

- Indian Railways to Merge with Konkan Railway under Maharashtra’s Approval

- Private credit’s deal desperation lands in India

- Technology Company Discovers Massive Digital Gold Opportunity in India

- Indian carrier IndiGo will do its first U.S. codesharing

- French energy giant TotalEnergies reaffirms support for Adani Green’s expansion in India

- India’s Next Big Investment: Natural Capital

- Indian authority approves merger of Tata Group’s seven companies

M&A news

- Renault Group seeks CCI nod to buy out remaining 51% stake in Indian joint venture

- ETMarkets Smart Talk: From 1,200 to 10,000 | Abhishek Banerjee charts the next decade of SME listings in India

- Promoters selling stakes bigger threat in the market: Sandip Sabharwal

- 87% Indian firms shift focus to domestic market amid global trade turmoil, HSBC survey finds

- Adani bull GQG raises stake in ITC to 5.47% following BAT’s partial exit

- Ericsson sells Vodafone Idea stake worth Rs 428 crore via bulk deal

- Gravita India promoter pares 3.4% stake for Rs 498 crore

- ITC shares tumbles 4% on BAT’s 2.5% stake sale worth Rs 12,900 crore

- Market surge leads to Rs 50,000 crore worth stake sales by promoters and shareholders

- Ola Electric shares shed 8% after 3.2% stake changes hands in block deal

- Outdated risk, renewed opportunities: A case for acquisition financing

- Who controls India Inc.? The answer is starting to change: NSE report

- Singapore remains biggest FDI source for India for 7th straight year

- RBI expected to deliver 3rd consecutive rate cut of 25 bps on Friday, say experts

- RBI likely to go for deeper interest rate cuts amid slower growth, low inflation: Morgan Stanley

- Adani Energy approves $502 million stake sale amid renewed investor confidence

- Titan Capital launches investment vertical to back defence-tech founders

- Jet Airways puts BKC office for sale; reserve price fixed at Rs 335 crore

- Is India’s distressed asset market still a bet worth taking for foreign investor

- Delay in regulatory clearances can hurt investor confidence, says Nirmala Sitharaman

- Hines-kanakia-mitsubishi-and-sumitomo-partner-on-mumbai-office-project

- From $10.1B to $353M: The Great Net FDI Collapse

- Himadri Makes Strategic Investment in IBC to Accelerate Global Growth in Li-ion Battery Materials and Clean Energy

- U.S. News & World Report Deepens India Engagement with Strategic Investment in White Bridge Education

- India’s net FDI plunges 96 percent in 2024–25, RBI calls it ‘sign of mature market’

- India’s Net Foreign Direct Investment Plummets by 96.5% to Reach Record Low

- Hyundai motor exits Ola electric with Rs552 crore stake sale, Kia also offloads shares

- Rakesh Gangwal family trust likely to offload 3-4% stake in IndiGo for Rs 6,831 crore amid ongoing divestment

- DRT Delhi directs status quo in ₹992 Cr proceedings by IREDA and PFC against Gensol

- Manipur’s Startup Pipeline Faces Funding Cliff; MTI-HUB Pushes for Capital Access, Market Linkages Amidst Political Unrest

- ITC stake strategic investment, not financial: BAT chief executive Marroco

- Kanakia, US-based Hines, Japanese firms partner for $1 bn project in Mumbai

- India’s private sector PMI grows to 61.2 in May

- Net FDI into India falls to $0.4 bn in FY25 amid repatriation surge

- India’s FDI puzzle: Why India Inc is investing more abroad than at home

- Judicial Delays Undermine Gains From IBC Reforms: Ind-Ra

- Nishant Pitti Starts Strategic Investment Initiative To Back Scalable Indian Startups

- Co-founder of India’s IndiGo continues share divestment

- Singapore retains top spot as India’s largest FDI source for seventh straight fiscal

- Rakesh Gangwal and Family has amassed ₹40,000 crore in three years of IndiGo stake sales

- Indian two wheeler maker Ola electrics losses double in Q4

- Beyond the buyout: Reallocations amid market challenges

- Continuation vehicles are now key to raising capital, not just exits: TPG NewQuest

- Vivriti Asset Management is tapping into the $342b MSME credit gap: Interview

- Haryana’s Vision 2047: A Blueprint for a Trillion-Dollar Economy

- India Emerges as a Global Economic Powerhouse: Fourth-Largest Economy

- Nazara Gets Regulatory Green Light for Strategic Stake Sale to Axana Estates and Partners

- IBC outlook FY25: Better recoveries, fewer liquidations, but slower resolutions – ICRA seeks reforms

- Chidambaram flags alarming trend of investment cancellations by Indian companies; calls out Finance Ministry

- Underlying weakness may be behind surge in outbound FDI

- RBI Repo Rate Cut: How Another Rate Cut By Sanjay Malhotra-Led MPC Impact Your FD Rates?

- What makes venture capitalists bet big money on Indian start-ups?

- CMS Formalizes India Ambitions, Enters Into Agreement With Local Firm Indus Law

- THE BRIEFS: JSW Resolution Rejection Gives Reality Check to India’s Bankruptcy Code

- BAT offloads $1.5 billion stake in ITC via block deal

- CPPIB’s India portfolio touches $22 billion in FY25

- Supreme Court to hear JSW Steel’s plea on Bhushan Power liquidation on Monday

- India’s manufacturing PMI eased to three-month low in May

- New funds surge in GIFT City but old money stays offshore

- RBIs interest rate decision, macroeco data, global trends to drive stock mkts this week: Analysts

- Supreme Court’s Decision In National Spot Exchange Limited v. Union Of India: Priority Of Secured Creditors In Flux?

- IDBI Divestment in 2025, PSU General Insurer Merger Off the Table for Now; New IRDAI Chief Soon

- FinMin Urges Faster M&A Approvals for Low-Risk Deals; Will This Hurt Competition?

- From Maharashtra to Mizoram: What AMFI Data Reveals About India’s Investment Divide

- Shares of Vopak’s 2.7 billion euro Indian JV rise on Mumbai debut

- India lures foreign investors back with big ticket block trades

- Paramount snaps ties with WPP Media after a 20-year partnership

- Delays in regulatory approvals can disrupt business timelines: Nirmala Sitharaman

- India Fuels Marriott’s Mid-Market Hotel Expansion with Strategic Investment in Concept Hospitality to Launch New Budget-Friendly Brand

- Carlyle makes another India exit move but did it meet the benchmark

- Hines Mitsubishi Sumitomo Form JV with Indian Developer for office asset

- Truenorth churns out high returns from financial services bet

- Funding India’s next AI-native builders; Nykaa nearly triples its profit

Job moves

- Paytm Appoints Ramana Kumar as CEO for Middle East Business

- Kotak Bank names Paritosh Kashyap as ED; Dy MD Ekambaram to retire

- SEBI grants approval to Jio BlackRock Mutual Fund, Sid Swaminathan appointed as first CEO

- ‘We made right investments – not just in assets, but people’ too: Suresh Narayanan bids farewell to Nestle India

- Kotak Mahindra Bank’s deputy MD Shanti Ekambaram to retire; appoints Paritosh Kashyap as executive director

- IndiGo shares edge higher on appointment of Vikram Singh Mehta as Chairman of the Board

- SMBC Group Appoints New Global Advisor

- Ratnakar Patnaik joins LIC of India as Managing Director

Fundraising

- 360 ONE Asset Launches Rs. 500 Crore Early-Stage VC Fund to Back India’s Next-Gen Startups

- PE firm L Catterton to raise $600 million for its first India-dedicated fund

- 360 ONE Asset launches $60 Mn sector-agnostic VC fund

- Snitch raises $40 Mn in Series B round; to enter quick commerce

- From Battery Smart To Chalo — Indian Startups Raised $93 Mn This Week

- Value fashion retailer Citykart raises Rs 538 crore in a Series B funding round

- Ola Electric board approves Rs 1,700 crore debt fundraise, first since IPO

- ASK Curated Luxury Assets Fund raises ₹500 crore to invest in luxury housing projects

- Slikk raises $10 million in Series A led by Nexus Venture Partners

- Beauty brand Simply Nam raises funding from Bhaane Group

- GydeXP Raises Pre-Seed Round Led by Rukam Sitara for Technology Startups

- 360 One Asset launches early-stage VC fund to back startups

- India business: Indian bond market strengthens as inflation eases and anticipated RBI rate cuts Jefferies

- JSW Steel Q4 net profit rises 13.54 to Rs1501 crore, board approves multiple fundraising plans

- Snitch raises $40 mn to expand men’s fashion brand in India, overseas

- L Catterton, a private equity firm, plans to raise $600 million for its inaugural India-focused fund

- Quadria Capital Closes Oversubscribed US$1 Billion Fund III to Advance Healthcare Transformation Across Asia

- L Catterton Plans $600 Mn India-dedicated Fund Backed By LVMH

- JSW Steel board approves fundraise of up to ₹19,000 crore via QIP, debt issuance

- ASK, ISIR Raise Rs 5 Billion for Luxury Housing Fund

- India’s Meenakshi Group launches $82m real estate fund

- Battery Smart bags $29m funding and other India deals

- StableMoney, OpenFX raise funds

- India’s Stable Money raises $20m in Series B funding round

- B2B SaaS Firm Data Sutram Raises USD 9 Mn Series A from B Capital and Lightspeed

- Vedanta to Raise INR 5,000 Crore via Debentures

- Series X Capital Raises Funds to Support Alphabet’s X Lab Spin-Offs

- ASK Property Fund, ISIR-backed real estate AIF raises ₹500 crore for Investment in luxury housing projects

- Incred’s Vivek Bansal ex-Kotak executive Sunil Daga raises Rs475 crore SeriesA for new NBFC venture

- CureBay raises USD 21 million to expand national footprint

- India’s Motilal Oswal Alternates eyes $600m first close for fifth flagship

- Info Edge Gears Up to Back Startups with Rs 1,000 Crore Venture Fund Approval

- Indian B2B SaaS startup Data Sutram nets $9m series A

- Indian EV battery-swapping firm Battery Smart nets $29m series B

- Lightspeed joins $20m series B for Indian wealthtech firm

- LVMH-backed L Catterton raising $600 India fund with former Hul Sanjiv Mehta

- GROWiT raises $3 million in Series A round

- Shuru App Raises Series A to Accelerate AI-Driven Hyperlocal Innovation

- Meenakshi Group’s alternatives arm rolls out debut real estate fund

- PE firm Trident Growth Partners lays out timeline for closing inaugural fund

- Agritech startup GROWiT India gets $3 million funding in Series A round led by GVFL

- Social media startup Shuru raises Series A funding from Krafton, Omidyar and Eximius

IPOs

Compliance/regulatory update

- Jio BlackRock Asset Management Receives SEBI Approval to Launch Mutual Fund Operations in India

- PNC Infratech completes stake sale in 10 road assets

- Resolution professional can now invite interim finance providers to CoC meetings

- IBBI chairperson sheds light on IBC’s benefits

- Govt prioritizes investor confidence, eyes bankruptcy law reform and industrial revival

- Ekambaram among last women leaders in banking to retire

- India grants Saudi FPI more flexibility in equity markets

- India’s Shapoorji closes $3.4 billion record private credit deal

- IVCA asks VCFs to act on Sebi circular, migrate to AIF regime by July 19

- Sebi eases norms for Category II AIFs on debt securities investments

- S&R Associates represented Bertelsmann India Investments

- Parliamentary panel to recommend fresh set of changes to insolvency code (IBC)

- RBI may go for ‘jumbo rate cut’ of 50 bps on Friday: SBI research

- Venture capital for SaaS has dried up most of it is going towards AI”: Zoho’s Sridhar Vembu

- India considers easing bank ownership rules as foreign interest grows

- India rupee, bonds expected to move higher in run-up to RBI policy decision

- Sebi redefines AIF category

- IBBI Simplifies Corporate Insolvency Resolution with Consolidated Five-Form Framework …

- BlackRock Gets Regulatory Nod to Start Mutual Fund Business in India

- Essar’s Mesabi Metallics Strategic Investment for a Sustainable Future