Guten Tag,

Der Deal der Woche markiert einen tiefgreifenden Wandel im europäischen Elektronikhandel, denn JD.com steigt mit 59,8 Prozent bei Ceconomy ein und kontrolliert nun gemeinsam mit Convergenta über 85 Prozent des Unternehmens.

Derweil berichten Medien, dass der FC Bayern München Sondierungsgespräche mit dem Investor EQT über eine mögliche Minderheitsbeteiligung geführt haben soll.

Darüber hinaus gab es weitere relevante Entwicklungen:

- SEFE trennt sich von seinem Mobility-Geschäft und verkauft 100 Prozent der Anteile an die in Münster ansässige Biogeen.

- Bastei Lübbe baut sein Portfolio im rasant wachsenden Webtoon- und Manhwa-Segment aus und übernimmt den Spezialverlag Papertoons vollständig.

- Ein zentrales Risiko in Deutschland ist die anhaltende Investitionsschwäche, die das Wachstum bremst.

Wenn Sie Interesse an einer Zusammenarbeit bei Ihrem nächsten M&A-Deal haben, freue ich mich über eine Kontaktaufnahme über LinkedIn.

Vielen Dank fürs Lesen.

Deal tracker

Deal der Woche

JD.com wird zum Hauptaktionär von Ceconomy

Der chinesische Technologiekonzern JD.com steigt mit 59,8 Prozent bei Ceconomy ein und hält gemeinsam mit Convergenta nun insgesamt 85,2 Prozent des Mutterkonzerns von Media Markt und Saturn. Mit der geplanten Dekotierung von der Börse sowie dem direkten Zugang zu über 1.000 europäischen Filialen markiert die Transaktion einen tiefgreifenden strategischen Umbau in der europäischen Handelslandschaft.

Für Ceconomy bedeutet der neue Mehrheitseigentümer nicht nur frisches Kapital, sondern auch die Chance auf beschleunigtes Wachstum, digitale Transformation und operative Skaleneffekte. Dabei wird das Unternehmen von einem der größten E-Commerce-Player der Welt unterstützt. Zugleich unterstreicht der Deal den Trend, dass chinesische Tech-Konzerne ihre Präsenz auf dem europäischen Markt deutlich ausbauen.

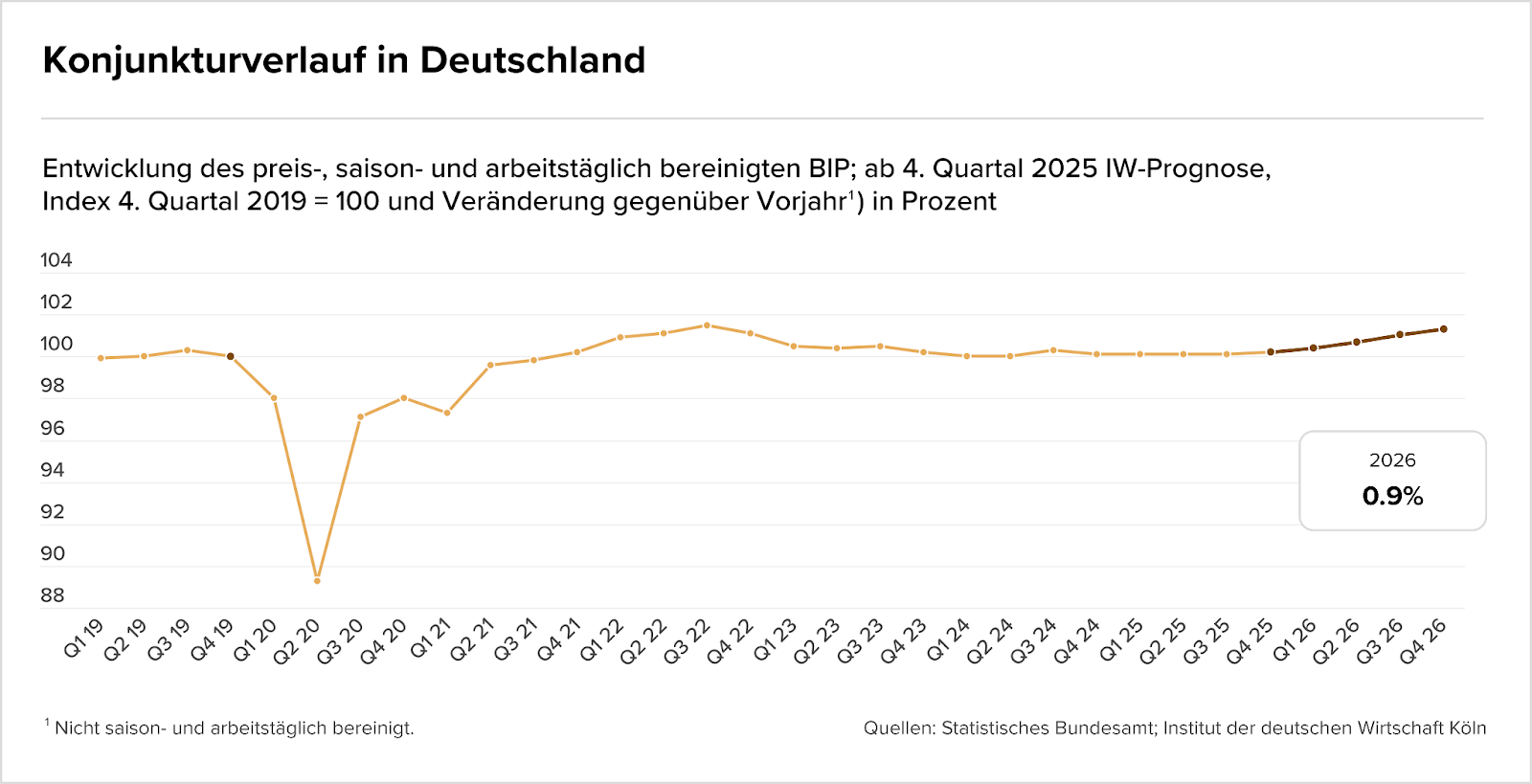

Verhaltener Aufschwung trotz schwacher Dynamik

Nach Jahren wirtschaftlicher Schwäche zeichnet sich in Deutschland nur ein moderater Konjunkturaufschwung ab. Die IW-Winterprognose 2025 beschreibt ein Umfeld, das zwar stabiler wirkt, aber weiterhin von strukturellen Belastungsfaktoren wie hohen Kosten und schwacher Investitionsneigung geprägt ist. Der erwartete Zuwachs für 2026 fällt entsprechend verhalten aus.

Die Grafik unten aus einer aktuellen IW-Studie zeigt, wie das preis-, saison- und arbeitstäglich bereinigte BIP nach dem pandemischen Einbruch nur schrittweise zum Vorkrisenniveau zurückkehrt. Ab dem 4. Quartal 2025 deutet sich eine leichte, aber fragile Erholung an. Für 2026 rechnet das IW mit lediglich +0,9 % Wachstum, was den anhaltenden Gegenwind unterstreicht.

Die Kurve bestätigt, dass die deutsche Wirtschaft zwar Boden gutmacht, von einem kraftvollen Aufschwung jedoch noch weit entfernt ist. Die langsame Steigung verdeutlicht eine sich stabilisierende, aber nicht beschleunigende Konjunktur. Unternehmen können zwar mit mehr Planungssicherheit rechnen, Wachstumsimpulse bleiben jedoch rar.

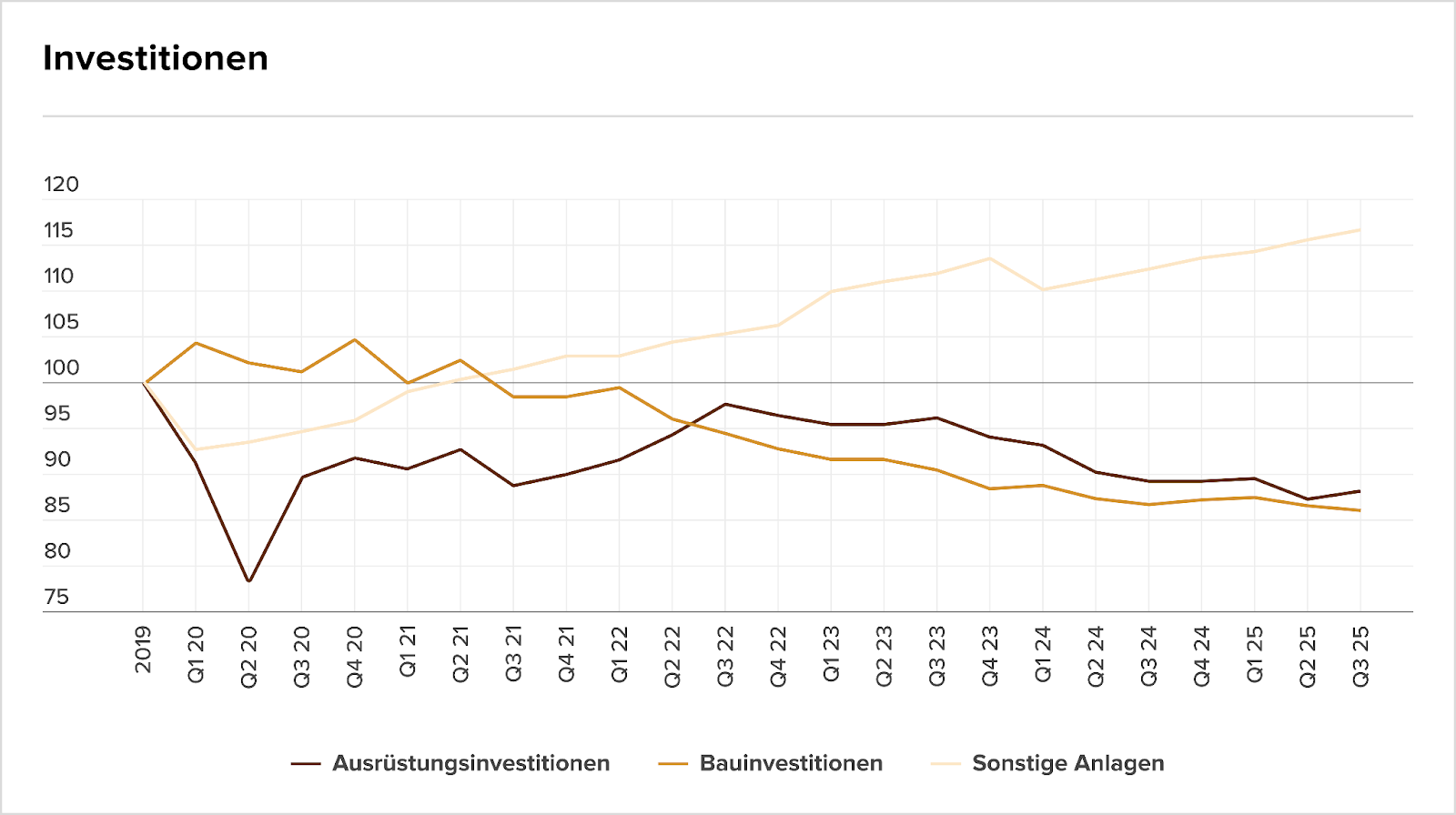

Investitionsschwäche wird zum Bremsklotz

Parallel zur schwachen Konjunktur zeigt sich eine anhaltende Investitionszurückhaltung, die zunehmend zum strukturellen Problem wird. Besonders energieintensive Industrien und das Baugewerbe leiden unter hohen Kosten, Lieferengpässen und regulatorischer Unsicherheit. Diese Faktoren drücken auf die Fähigkeit der Wirtschaft, neue Wachstumsquellen zu erschließen.

Die Grafik unten aus der IW-Konjunkturprognose Winter 2025 macht deutlich, wie die Bau- und Ausrüstungsinvestitionen seit 2022 kontinuierlich zurückgehen. Während sonstige Anlagen immerhin leicht zulegen, liegen die beiden zentralen Kategorien inzwischen klar unter dem Niveau von 2019. Der Rückgang bei Ausrüstungsinvestitionen ist besonders kritisch, da er unmittelbar die Innovations- und Wettbewerbsfähigkeit betrifft.

Die Entwicklung zeigt: Deutschland investiert zu wenig in seine wirtschaftliche Zukunft. Ohne Impulse in den Bereichen Maschinen, Anlagen und Bauprojekte verstärken sich die bereits erkennbaren Strukturprobleme. Die Investitionsschwäche bleibt somit ein zentraler Hemmschuh und birgt Risiken für die Erholung ab 2026.

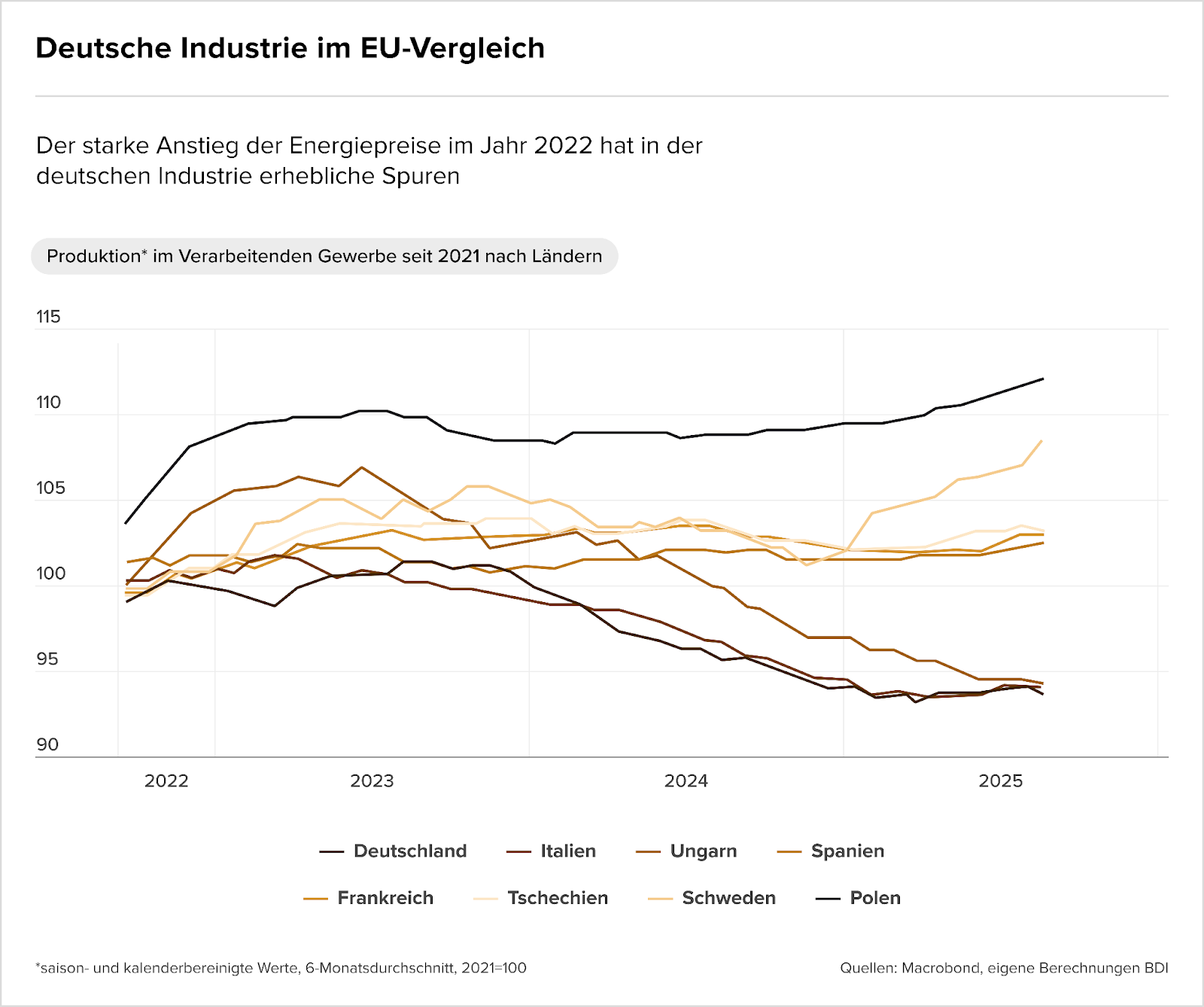

Deutschlands Industrie verliert im EU-Vergleich an Boden

Die deutsche Industrie bleibt 2025 deutlich hinter der Entwicklung vieler europäischer Länder zurück. Hohe Energiepreise, strukturelle Standortprobleme und eine schwache Investitionsdynamik haben die Wettbewerbsfähigkeit sichtbar unter Druck gesetzt. Während andere Volkswirtschaften wieder im Aufschwung sind, verharrt Deutschland auf einem niedrigeren Produktionsniveau.

Besonders auffällig ist, dass zentrale Industrien wie Maschinenbau, Chemie und Automobilfertigung nur langsam auf die Energiepreisschocks von 2022 reagiert haben und im europäischen Vergleich weniger resilient wirkten. Länder mit flexibleren Energie- und Regulierungsstrukturen konnten dagegen schneller Kapazitäten ausbauen und Marktanteile zurückgewinnen.

Das unten gezeigte BDI-Diagramm aus dem Industriebericht Dezember 2025 verdeutlicht diese Divergenz: Während Polen und Schweden ihre Industrieproduktion seit 2021 deutlich steigern, rutscht Deutschland kontinuierlich ab und bildet im EU-Feld inzwischen das Schlusslicht. Die Grafik illustriert somit, wie weit die Schere zwischen Deutschland und seinen Wettbewerbern inzwischen auseinandergeht und wie dringend strukturelle Reformen erforderlich sind.

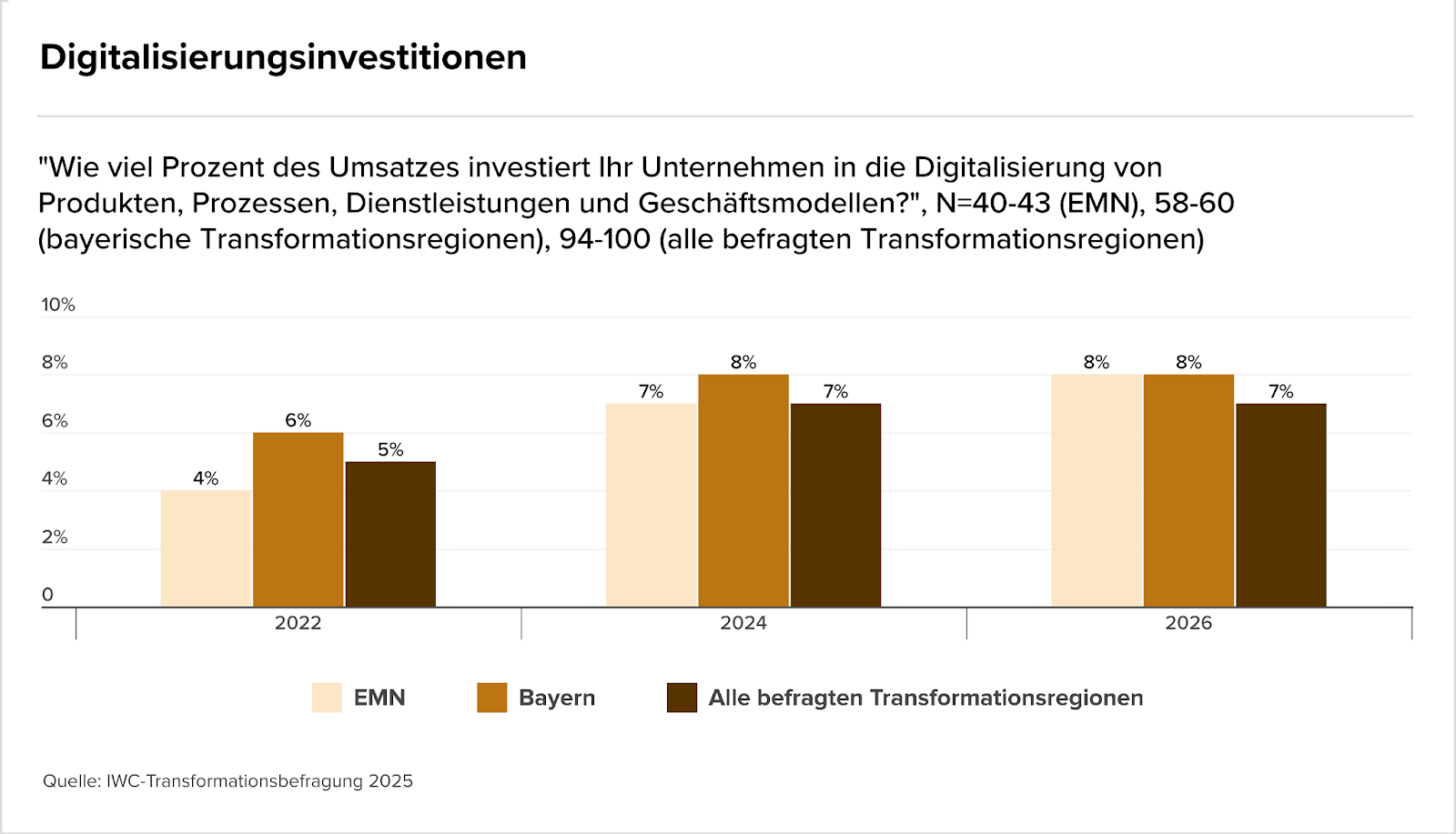

Unternehmen erhöhen konsequent ihre Digitalisierungsinvestitionen

In vielen Industrie- und Technologieregionen bleibt Digitalisierung ein zentraler Hebel, um Wettbewerbsfähigkeit und Resilienz zu sichern. Trotz struktureller Herausforderungen wie Lieferkettenrisiken und Kostendruck zeigen die jüngsten Erhebungen, dass Unternehmen ihre Transformationsbemühungen deutlich verstärken. Besonders im automotive-nahen Mittelstand rückt die Frage „Wie viel Digitalisierung braucht mein Geschäftsmodell?“ stark in den Fokus.

Die aktuelle IWC-Transformationsbefragung 2025 bestätigt diesen Trend: Unternehmen planen, ihre Ausgaben für digitale Produkte, Prozesse und Dienstleistungen weiter zu erhöhen. Bis 2026 werden die Budgets in allen Transformationsregionen stabil oder steigend erwartet – ein Signal für langfristige Strategien jenseits kurzfristiger Konjunkturzyklen. Damit gehört die Digitalisierung zu den wenigen Investitionskategorien, die trotz unsicherer Märkte nicht zurückgefahren werden.

Die unten stehende Grafik aus dem Bericht verdeutlicht diese Entwicklung: In den EMN-Regionen steigen die Investitionen von 4 %(2022) auf 8 % im (2026). Bayern und andere Transformationsregionen liegen mit 7-8 % stabil im Mittelfeld. Die Werte belegen, dass die digitale Transformation ein fester Bestandteil der Ressourcenplanung ist. Für Unternehmen ist sie deshalb ein entscheidender Faktor, denn wer jetzt investiert, sichert sich die Innovationsbasis für die nächste Dekade.

Marktgerüchte

- SpaceX verhandelt laut Medienberichten über einen Verkauf von Mitarbeiteraktien zu einer Bewertung von rund 800 Milliarden Dollar. Zudem mehren sich Hinweise, dass ein möglicher Börsengang des Unternehmens näher rückt.

- Worthington Steel befindet sich in Gesprächen über ein mögliches freiwilliges Übernahmeangebot für Klöckner & Co. Die Due-Diligence läuft, doch ob es tatsächlich zu einer Transaktion kommt, ist laut beiden Unternehmen noch offen.

- Anta Sports sondiert eine Puma-Übernahme und kooperiert dazu mit Investoren, auch Li Ning und Asics sind interessiert. Der Pinault-Familie, die Anta Sports Großaktionärin ist, wird mit Verkauf gedroht.

- Laut Financial Times soll der FC Bayern München Gespräche mit dem Investor EQT über eine mögliche Minderheitsbeteiligung geführt haben. Ein Einstieg von Private Equity bei deutschen Fußballvereinen wäre ein bemerkenswerter Schritt.

- Der südkoreanische Baumaschinenhersteller Doosan Bobcat verhandelt über den Erwerb von 63 Prozent von Wacker Neuson. Ob es zu einer Übernahme kommt, ist unklar.

- IBM befindet sich laut Medienberichten in fortgeschrittenen Gesprächen über die Übernahme des Dateninfrastruktur-Anbieters Confluent für rund elf Milliarden Dollar. Mit dem Deal würde IBM sein Cloudgeschäft deutlich ausbauen – eine Bekanntgabe könnte bereits am Montag erfolgen.

M&A-Nachrichten

- Netflix’ geplante Übernahme von Warner Bros. Discovery im Wert von 83 Milliarden Dollar wird zum Bieterwettstreit: Paramount legt ein feindliches Angebot über rund 108 Milliarden Dollar vor, was den Deal erheblich gefährdet und politische Einflussfaktoren ins Spiel bringt.

- TKMS meldet ein Rekordjahr mit einem Auftragsbestand von über 18 Milliarden € und erwartet weitere Konsolidierungsschritte in der deutschen Verteidigungsindustrie. Das Unternehmen prüft zudem derzeit einen möglichen Zukauf.

- Eine Handelsblatt-Analyse zeigt eine deutliche Verschiebung im deutschen Einhorn-Ökosystem: Während KI-, Verteidigungs- und Software-Start-ups 2025 stark wachsen, verlieren andere Sektoren an Boden, wodurch die Zahl der Einhörner von 33 auf 28 sinkt. Einige der neuen Milliarden-Start-ups könnten zudem Kandidaten für einen Börsengang sein.

- Thyssenkrupp kehrt zwar in die Gewinnzone zurück, erwartet jedoch für 2025/26 wieder Verluste und einen negativen Free Cashflow aufgrund hoher Restrukturierungskosten. Der belastende Ausblick drückt bereits auf den Aktienkurs.

- Swisspod hat in den USA 102 km/h geschafft und arbeitet nun an einem erweiterten “Closed-Loop”-System für höhere Geschwindigkeiten. Der Investor sieht den Fortschritt als wichtigen Meilenstein für die Skalierung der Technologie.

- Die Deutsche Börse verhandelt exklusiv über die Übernahme der Fonds-Handelsplattform Allfunds für insgesamt 8,80 € pro Aktie. Ob der Milliarden-Deal zustande kommt, ist noch offen; die Märkte reagierten gemischt.

- Die Raiffeisen-Holding Niederösterreich-Wien erklärt ihre langfristige Investmentstrategie in Start-ups und VC-Fonds: strategische Beteiligungen ohne Exit-Druck, enge Zusammenarbeit mit Portfolio-Unternehmen und gezielte Unterstützung bei Skalierung und Produktentwicklung.

- Doosan Bobcat verhandelt über die Übernahme von Wacker Neuson. Der südkoreanische Konzern erwägt den Erwerb von rund 63 Prozent der Anteile und bereitet ein öffentliches Barangebot vor.

- AustrianStartups, Speedinvest und invest.austria begrüßen das Deregulierungspaket und fordern weitergehende Reformen. Die Organisationen legen fünf Vorschläge vor, die Startups und Investor:innen entlasten sollen.

- Die Crowdfunding-Plattform Conda kooperiert mit dem Wiener KI-Startup StartMatch, um Emissionstexte mit KI zu automatisieren und Kapitalmarktprozesse deutlich zu beschleunigen.

- Die Deutsche Börse plant ab 2026 jährliche Aktienrückkäufe als festen Bestandteil ihrer neuen Strategie. Zusätzlich will der Konzern seine Nettoerlöse und den Betriebsgewinn bis 2028 deutlich steigern.

- Die Plattform X blockiert künftig Werbeschaltungen der EU-Kommission, nachdem diese wegen eines Beitrags zur Millionenstrafe gegen X angeblich gegen Plattformregeln verstoßen haben soll. Hintergrund ist der eskalierende Konflikt zwischen Elon Musk und der EU über Desinformation und Regulierung.

- Japanische Investoren haben beim ICSID Schiedsklage gegen die Schweiz eingereicht, nachdem AT1-Anleihen der Credit Suisse im Zuge der UBS-Übernahme abgeschrieben wurden. Sie fordern über 300 Mio. Dollar Schadenersatz – die Schweiz weist die Vorwürfe entschieden zurück.

- Die Mailänder Staatsanwaltschaft ermittelt gegen den MPS-Chef Luigi Lovaglio und zwei Großaktionäre wegen mutmaßlicher geheimer Absprachen beim Kauf von Mediobanca. Die Ermittlungen betreffen Marktmanipulation und mögliche Behinderung der Aufsicht.

- Deutsche Börse und Kraken schließen eine strategische Partnerschaft, um ihre Plattformen und Produkte gegenseitig zugänglich zu machen und damit das Angebot für institutionelle Kunden im Kryptobereich auszubauen.

- Die Bundesregierung bereitet den Ausstieg aus Uniper vor und sieht einen Börsengang als zentrale Option für die Reprivatisierung. Parallel werden auch außerbörsliche Verkaufswege geprüft, während weiter eine mögliche Fusion mit Sefe im Raum steht.

Personalien

- SellerX baut seine Belegschaft erneut stark ab und reduziert auch sein Markenportfolio um die Hälfte. Der Amazon-Aggregator reagiert damit auf die anhaltende Marktflaute und zunehmenden Wettbewerbsdruck im E-Commerce.

- Der frühere Credit-Suisse-Manager André Helfenstein steht laut Medienberichten kurz vor der Ernennung zum neuen Präsidenten der Schweizer Börsenbetreiberin SIX. Er würde Thomas Wellauer ablösen, der sein Amt im Mai 2026 abgeben will.

- UBS plant laut Medienberichten bis 2027 den Abbau von rund 10.000 Stellen, vor allem durch natürliche Fluktuation und Frühpensionierungen. Besonders betroffen ist die Schweiz im Zuge der andauernden Integration der Credit Suisse.

- Vonovia ernennt Katja Wünschel, derzeit Chefin von RWE Renewables Europa/Australien, zur neuen Vorständin für den Neubau ab Juni 2026. Sie folgt auf Daniel Riedl und soll vor allem den wieder aufgenommenen Neubau vorantreiben sowie Baukosten weiter senken.

- Binance führt eine neue Doppelspitze ein: Mitgründerin Yi He wird Co-CEO an der Seite von Richard Teng. Die beiden wollen die Nutzerbasis weiter ausbauen und steuern langfristig die Marke von einer Milliarde Nutzer an.

- Die Neue Bank in Vaduz richtet per Januar 2026 einen neuen COO-Bereich ein und beruft Manuel Ribar in die Geschäftsleitung. Der Schritt dient der Modernisierung des operativen Fundaments und der Umsetzung der Strategie 2030.

- Valiant hat Matthias Hiestand zum Leiter Unternehmenskunden ab Juni 2026 ernannt. Der langjährige Manager folgt auf Daniel Horat und soll das strategisch wichtige KMU-Geschäft weiter ausbauen.

- Die Bank Avera stellt ein neues Team für die Betreuung kleinerer Firmen- und Gewerbekunden auf, geleitet von der erfahrenen Managerin Sarah Parker. Damit soll die persönliche Beratung dieser Kundengruppe weiter gestärkt werden.

- Allianz Global Investors stärkt seinen Standort Zürich mit zwei Neuzugängen: Marc-André Hug übernimmt als Head of Wholesale Switzerland den Vertrieb, während Jan Berg ab Januar 2026 das European Small & Mid Cap Equity-Team leitet.

- Der frühere Credit-Suisse-Schweiz-Chef André Helfenstein gilt Berichten zufolge als Favorit für die Nachfolge von Thomas Wellauer als Verwaltungsratspräsident der SIX Group. Die Entscheidung soll in den kommenden Tagen fallen.

- Die Partners Group erweitert ihre Geschäftsleitung und beruft Ana Campos sowie Anette Waygood in Führungsfunktionen. Gleichzeitig kommt es zu weiteren internen Umbesetzungen, darunter einer neuen Leitung für den Bereich Business Development.

Kapitalrunden

- Das Zoll-KI-Startup Digicust hat seine Pre-Series-A-Runde abgeschlossen und insgesamt 2,3 Mio € aus Investments und Förderungen eingesammelt. Das Kapital soll Expansion und Skalierung der KI-basierten Zollautomatisierung beschleunigen.

- Das Lichttherapie-Start-up Syntropic hat eine zusätzliche Finanzspritze erhalten. Das Angel-Netzwerk Better Ventures unterstützt Syntropic dabei, das Medikament in den USA auf den Markt zu bringen.

- Das Wiener KI-Startup DotSimple hat eine Finanzierungsrunde im mittleren sechsstelligen Bereich abgeschlossen. Mit dem Kapital sollen Plattform, KI-Funktionen und der Marktausbau im DACH-Raum weiter vorangetrieben werden.

Börsengänge

- Magnum Ice Cream Company wagt nach der Abspaltung von Unilever den Börsengang in Amsterdam, startet jedoch mit einem Kurs unter dem erwarteten Referenzpreis. Unilever hält weiterhin knapp 20 Prozent, während der Konzernumbau voranschreitet.

- Anthropic bereitet laut Financial Times einen Börsengang vor und hat dafür bereits Wilson Sonsini mandatiert. Parallel verhandelt das KI-Unternehmen über eine neue Finanzierungsrunde, die seine Bewertung auf mehr als 300 Milliarden Dollar steigern könnte.

O Ibovespa voa acima de 164 mil pontos, o real se valoriza entre as principais moedas globais e a curva de juros finalmente sinaliza alívio. Na superfície, tudo indica um mercado aquecido, maduro e pronto para receber novos players. Mas tem um detalhe incômodo: a B3 completa quatro anos sem um único IPO.

Quatro anos. Nenhuma estreia. Enquanto isso, 95 empresas deixaram a Bolsa pela porta dos fundos — via OPAs de fechamento de capital. O paradoxo é gritante: recordes no índice, deserto nas estreias.

Nesta edição, navegamos por esse cenário contraditório e destrinchamos o que está travando a retomada dos IPOs no Brasil. Spoiler: não é só culpa dos juros.

Principais insights desta edição:

- Ibovespa em alta histórica, mas com 95 empresas a menos na B3 desde 2021

- Curva de juros precifica Selic a 12% em 2026 — mas ainda insuficiente para IPOs

- PIB fraco (0,2% t/t no 3T25) alivia inflação, mas expõe crescimento morno

- Fiscal no vermelho: déficit de R$ 75 bi projetado para 2025, com arrecadação abaixo do esperado

- Custo de capital proibitivo: juro real perto de 10% torna dívida mais barata que equity

- Expectativa para 2026? Zero. Janela pode entreabrir só em 2027 — se vier com responsabilidade fiscal real

Quer mais insights do backstage do M&A brasileiro? Se conecte comigo no LinkedIn e vamos conversar.

Boa leitura.

Deals breakdown

Curadoria entre 24 de novembro e 11 de dezembro.

Deals identificados: 32

IPOs no Brasil: recordes na bolsa, mas sem novas estreias

O Ibovespa bateu recordes históricos na última semana, fechando acima dos 164 mil pontos com alta generalizada em quase todas as 82 ações da carteira. O otimismo veio embalado por um PIB do terceiro trimestre abaixo do esperado — o que, paradoxalmente, animou o mercado ao reforçar apostas de corte na Selic — e pela expectativa de afrouxamento monetário tanto aqui quanto nos Estados Unidos. “Há um apetite por risco renovado”, resumiu uma analista. A euforia é tanta que há quem aposte em Ibovespa a 171 mil pontos até o fim do ano.

Mas tem um detalhe: enquanto o índice voa, a B3 completa quatro anos sem um único IPO.

Quatro anos. Para quem viveu o êxtase de 2020 e 2021, quando empresas abriam capital como quem inaugura padaria de bairro, o contraste é brutal. Naquela época, havia 463 empresas listadas. Hoje? 368. A diferença não evaporou: saiu pela porta dos fundos, via OPAs de fechamento de capital — a Neoenergia é só o exemplo mais recente.

O diagnóstico é claro, mas incômodo: aquele boom foi artificial. Com a Selic a 2%, o mercado se embriagou de liquidez e levou à Bolsa empresas que, convenhamos, não tinham lá muito preparo para o protagonismo. Quando a taxa básica voltou para a realidade — beirando dois dígitos — o custo médio ponderado de capital disparou. Emitir dívida privada virou mais barato que emitir ações. E se o investidor local migrou para a renda fixa e o gringo prefere commodities e bancos tradicionais, quem sobra para comprar papel de estreante? Ninguém.

A regulação não é vilã — o mercado brasileiro é maduro nisso. Mas os custos de ser companhia aberta pesam quando a Bolsa não remunera de verdade. E os controladores sabem fazer contas: se minha empresa está subavaliada, por que não comprar de volta?

Para 2026? Expectativa zero. A janela pode entreabrir em 2027, mas só se vier acompanhada de responsabilidade fiscal, queda estrutural dos juros e reconstrução de credibilidade. Até lá, seguimos nesse paradoxo: recordes no índice, deserto nas estreias.

Juros em Queda, real forte, IPOs no Brasil em Espera: o paradoxo do otimismo incompleto

O mercado brasileiro vive um momento curioso: otimismo na superfície, cautela nas entrelinhas. O Ibovespa bate recordes, o real se valoriza e a curva de juros futuros indica alívio à frente — mas a fila de IPOs segue vazia há quatro anos.

Os sinais macro recentes animam. O IPCA-15 de novembro veio com alta de 0,20% m/m, acima do consenso, mas com surpresas concentradas em itens voláteis. A média dos núcleos recuou para o menor nível desde meados de 2024, evidenciando uma dinâmica benigna da inflação. O mercado de trabalho de outubro trouxe resultados mistos: o CAGED gerou 85 mil empregos formais, abaixo do esperado, enquanto a taxa de desemprego caiu para 5,4%. É um mercado ainda apertado, mas sem sinais de superaquecimento.

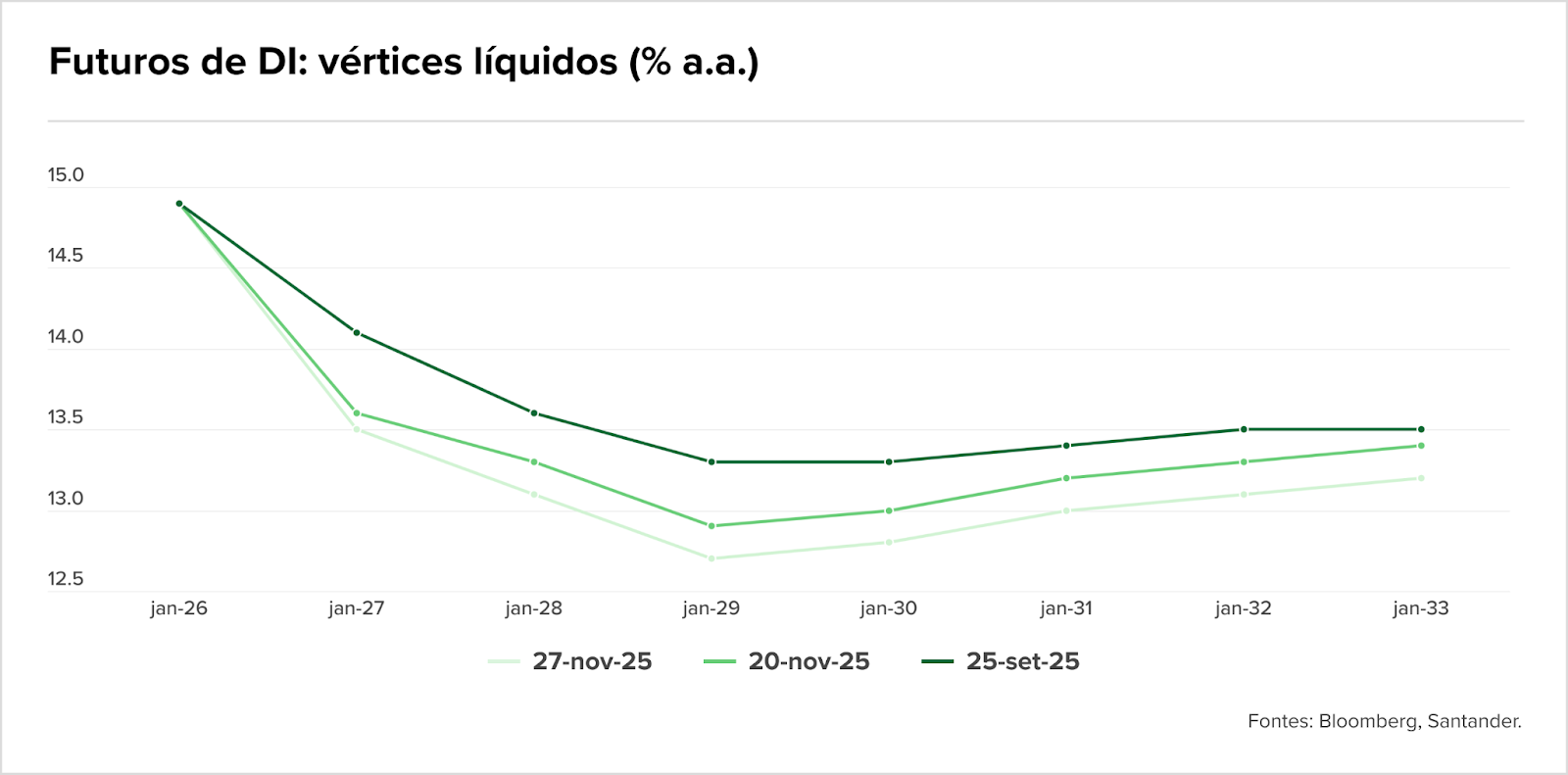

A curva de juros captou o recado. Os futuros de DI tiveram deslocamento para baixo ao longo de toda a estrutura, com a precificação indicando Selic ao redor de 12% no final de 2026 — ante 12,25% na semana anterior. A probabilidade de corte já em janeiro? 64%, segundo as últimas leituras. O mercado projeta início do ciclo de afrouxamento em breve, com Selic terminal de 2026 em 12,50%.

Então por que as empresas não voltam à Bolsa?

Porque o alívio na curva de juros não é suficiente — ainda. Com juro real próximo de 10%, o custo médio ponderado de capital segue proibitivo para IPOs. E há o lado fiscal: a revisão bimestral do Orçamento de 2025 veio levemente mais desfavorável, com o aperto líquido reduzido em menos de BRL 1 bi. A sanção da lei que amplia a faixa de isenção do IR até BRLk 5 e a aprovação da aposentadoria especial para agentes comunitários de saúde (impacto estimado em BRL 5-6 bi por ano, segundo estudo do Santander) mantêm o radar fiscal piscando em amarelo.

A conta é simples: sem âncora fiscal, a política monetária trabalha em dobro. E sem credibilidade estrutural, mesmo com cortes de juros à vista, o apetite por IPOs segue congelado. Para 2026, expectativa zero. A janela pode entreabrir em 2027 — mas só se vier acompanhada de responsabilidade fiscal real, não apenas de sinalizações pontuais.

PIB fraco, contas públicas no vermelho: a receita perfeita para adiar IPOs no Brasil

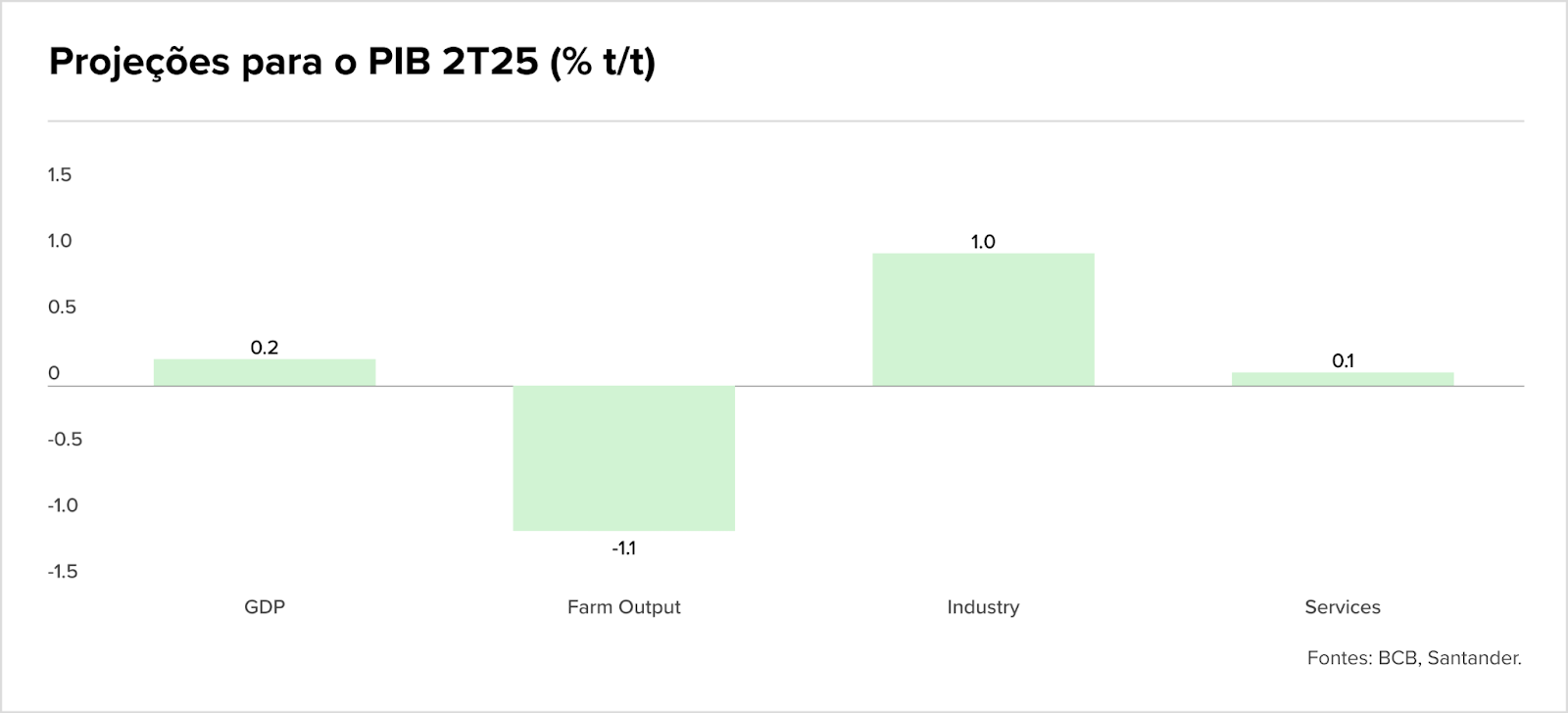

A prévia do PIB trouxe um dado que o mercado adorou — mas pelo motivo errado. Após desacelerar no 2T25, a projeção para o 3T25 é de alta marginal de apenas 0,2% t/t, reforçando um cenário de pouco suave para a economia no segundo semestre. A produção agrícola deve seguir como fator negativo, enquanto serviços e indústria devem manter contribuição positiva, apesar da fraqueza nos segmentos mais sensíveis ao ciclo. Para 2025, projeta-se crescimento de 2% — longe de robusto.

O mercado comemorou porque crescimento fraco significa menos pressão inflacionária e, teoricamente, espaço para corte de juros. Mas tem um problema: essa lógica só funciona se o lado fiscal estiver arrumado. E não está.

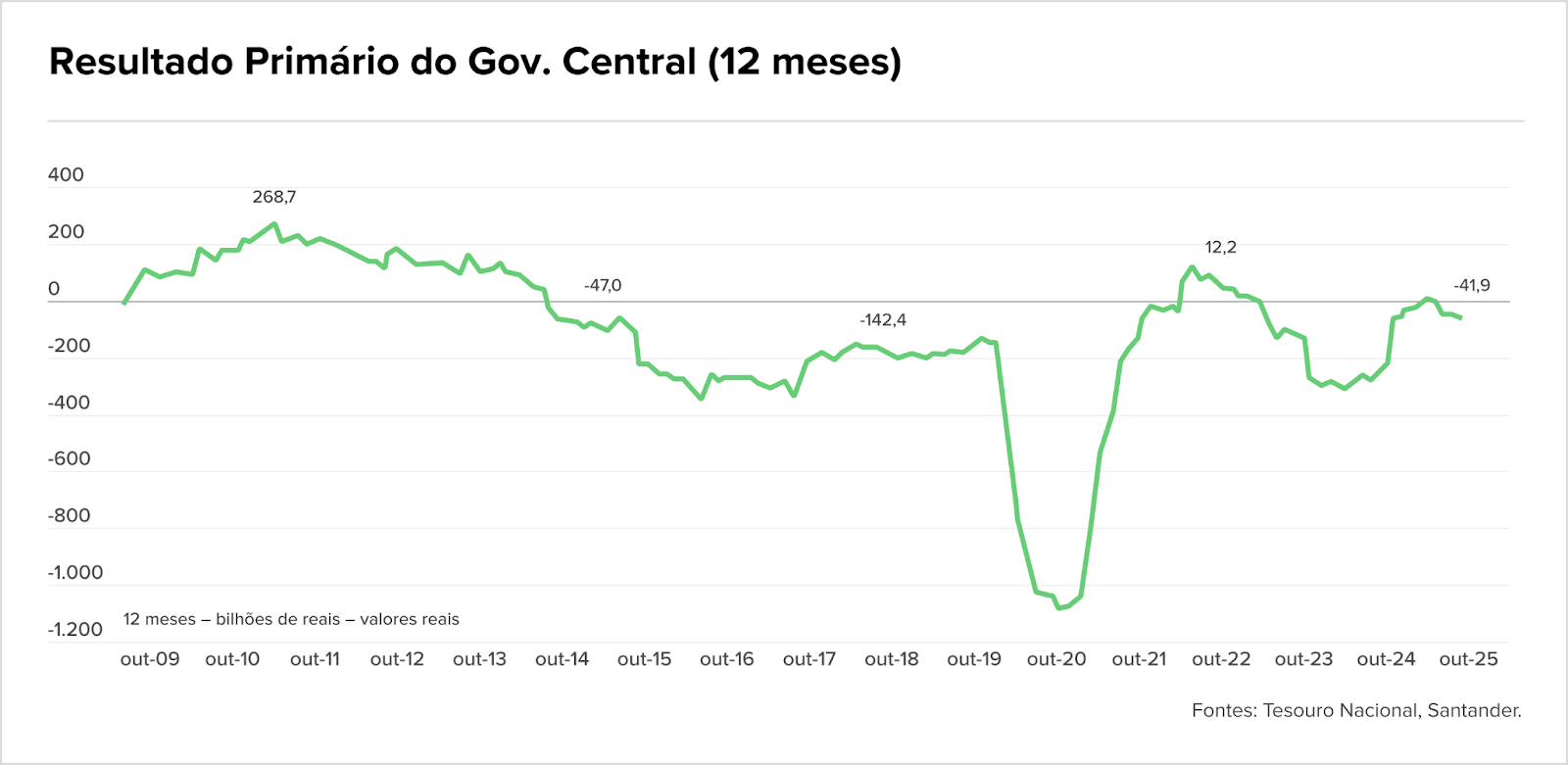

A arrecadação federal até outubro totalizou BRL 261,9 bi, alta real de 0,9% a/a, abaixo das expectativas, refletindo a desaceleração dos componentes cíclicos diante de menor atividade e inflação mais baixa. O IOF e o mercado de trabalho seguem sustentando parte da receita, mas o governo central registrou superávit de BRL 36,5 bi em outubro, impulsionado por BRL 2,8 bi em dividendos de estatais — um alívio pontual, não estrutural. A receita líquida avançou 4,5% a/a, mas as despesas subiram 9,2%, puxadas por benefícios sociais e maior execução orçamentária.

Em 12 meses, o déficit do governo central permanece em BRL 41,9 bi (0,35% do PIB). A projeção para 2025 é de déficit de BRL 75 bi (0,6% do PIB), com cumprimento da meta dependente de receitas extraordinárias e de riscos crescentes de menor arrecadação em 2025.

Traduzindo: o fiscal está apertado, o crescimento está morno e a política monetária vai precisar segurar a onda sozinha. Nesse contexto, mesmo com Selic caindo, o custo de capital segue alto e a percepção de risco segue elevada. Para empresas que pensam em IPO, a conta não fecha. Crescimento fraco significa múltiplos comprimidos. Fiscal frágil significa prêmio de risco alto. Juros em queda, mas ainda em dois dígitos, significam que emitir dívida segue mais barato que emitir ações.

Resultado? A fila de IPOs segue vazia. E deve seguir assim até que o Brasil entregue não apenas sinalizações, mas resultados fiscais críveis e crescimento sustentável. Enquanto isso, a B3 continuará batendo recordes — com cada vez menos empresas no índice.

Brasil

Tendências de Mercado

- Interesse por M&A na América Latina cresce e Brasil se destaca por avaliações atrativas, aponta KPMG

- Governança de IA redefine due diligence e muda o jogo das operações de M&A

- 65,2% das startups brasileiras nunca receberam aportes, diz Abstartups

- Brasil atrai investimentos em data centers para IA

- Startups e PMEs impulsionam ciclo virtuoso entre tecnologia e M&As

- CVCs avançam: o que explica a preferência dos top founders por capital corporativo

Mundo

Agronegócio

Controvérsias

Fundraising

Intenções e Estratégias

- Com recuperação extrajudicial autorizada, Lavoro planeja vender a Crop Care e anuncia nova liderança no Brasil

- Grupo BLB cria unidade de M&A e mira BRLm 360 em transações até 2026

- De olho no agro, BTG pode ficar com 49,9% da Ceres Investimentos

M&A

- Wallerius Seguros adquire 100% da Ativa Agro e reforça presença no setor de irrigação. a transação não teve o valor divulgado

- JBS e Grupo VIVA se unem para criar líder global no segmento de couro

- Be8 investe BRLm 70 na aquisição de usina de biodiesel em MT

- Empresas do Brasil e da China criam joint venture para produzir pequenas máquinas agrícolas

- Raça Agro adquire a Agroline por BRLm 80 e amplia presença no mercado de insumos pecuários

Consumo

Controvérsias

Fundraising

- Crescera amplia portfólio e investe na VIX Brasil com compra de participação

- Atlantikos capta BRLm 1 em rodada Seed com participação da Invisto, BossaNova, GVAngels e outros grupos de investidores

Intenções e Estratégias

M&A

- Multi conclui venda de unidade de tapetes higiênicos para pets por BRLm 15 para Grupo Bun

- Após Semenzato, Carlos Wizard entra no setor ótico e se torna sócio da Óticas Duty, que planeja saltar de 5 para 1.000 lojas

- Fundos do Grupo Muffato compram BRLm 63,65 de ações do Assaí e alcançam participação de ~10% na atacadista

- Grupo Impettus compra Sirène por BRLm 14 e incorpora rede de fish & chips ao portfólio

Energia

Intenções e Estratégias

- Iberdrola Energia entra com pedido de oferta pública para fechar capital da Neoenergia

- Após sair de Emae e Eletronuclear, Axia Energia ainda tem cerca de BRL 25 bi em ativos para liquidar

- Iberdrola fará oferta de BRL 6,5 bi para comprar ações da Neoenergia

- Raízen prepara venda de ativos superiores a USD 1 bi e acelera desinvestimento na Argentina

- CPFL aprova projeto para alterar controle acionário de controlada CPFL Transmissão

- Controlada da Cemig conclui reorganização societária de 11 usinas fotovoltaicas

- Family office dos Moreira Salles vende mais de BRLm 600 em ações da Eneva, dizem fontes

M&A

FIG

Fundos

Fundraising

- AB Card recebe investimento de BRLm 1 da DOMO.VC em série seed e lança plataforma que revoluciona benefícios corporativos para empresas de médio porte

- Clara capta USDm 70 para crescer no México e na Colômbia – os recursos vêm das instituições BBVA Spark, Covalto e International Finance Corporation (IFC)

- Indicator Capital investe BRLm 3 na Doji em rodada pré-Série A

- Omni levanta BRLm 500 em emissão de debêntures para acelerar operações financeiras

- Mercado de Recebíveis conclui captação de BRLm 150 em FIDC próprio

- Creditas conclui rodada Série F de USDm 108, liderada pela Advent International e acompanhada por Redpoint eventures e SoftBank

Intenções e Estratégias

- Após vender divisão Empírica por BRLm 75, Arandu anuncia novo pacote de dois ativos à venda

- Agibank mira IPO nos EUA em janeiro e acelera preparação para abertura de capital

M&A

- Patria entra com força em FIDCs ao adquirir 51% da Solis e garantir opção pelos 49% restantes; a transação não teve valor divulgado

- SRM conclui compra da Empírica, em operação que marca desinvestimento da Arandu (ex-Reag)

- Nubank faz acquihire e absorve time da DEX Labs em movimento para reforçar IA

- Arandu, antiga Reag Investimentos, vende gestora de fortunas para CVPar

Industria

Intenções e Estratégias

- Fechamento de capital: Monteiro Aranha lança OPA de BRL 1,34 bi marcada para 18 de dezembro

- IPO da Vale Base Metals pode acontecer — só não está no objetivo estratégico do momento

- De Pouso Alegre para Madri: fabricante mineira de fornos busca expansão na bolsa espanhola

- Irmãos Batista contratam Citi para vender fatia da mineradora LHG e atrair sócio estrangeiro

M&A

Infraestrutura

Fundraising

Intenções e Estratégias

- CSN negocia venda de participação na MRS ao CSN Mineração — operação avaliada em até BRL 3,26 bi

- GRU Airport leva 12 aeroportos regionais no AmpliAR; Fraport assume Jericoacoara e operação prevê mais de BRLm 700 em investimentos

- Consórcio formado por Petrobras e Shell arremata jazida de Mero por BRL 7,79 bi

- Bradesco BBI venderá fatia da Motiva, ex-CCR

- A Rodobens passou a deter 93,3% da RNI na OPA, equivalente a 31,9% do capital social; o preço realizado foi de R$ 2,13, prêmio de 4% sobre o fechamento de quinta-feira

- Sócios de adquiridas da Ambipar acusam empresa de raspar o caixa

- Em vez de crescimento de base, provedores buscam M&A, caixa e receita

M&A

- A Zaaz anunciou a aquisição da operadora regional Proxxima, com atuação concentrada em Pernambuco, Paraíba, Bahia, Rio Grande do Norte e Ceará em transação sem valor divulgado

- Engemon dá salto internacional: compra construtora no Paraguai e inaugura a Engemon Internacional; a transação não teve valor divulgado

- TIM aprova compra da V8.Tech por BRLm 140 e reforça aposta no B2B

Real Estate

Fundraising

M&A

- Gafisa avança em desalavancagem e aprova venda de participação na SPE para a Soter; a transação não teve valor divulgado

- TRXF11 compra agências da Caixa e do Santander por BRLm 140

- TRXF11 entra em shoppings e compra 100% do ViaBrasil Pampulha e 50% do Paragem por BRLm 257,7 — pagamento integral em cotas

- FII RZAT11 vende ativos por BRLm 14 e avança em estratégia de reciclagem de portfólio

Tendências de Mercado

Saúde

Fundraising

Intenções e Estratégias

M&A

Serviços

Fundraising

- Diva capta BRLm 2,5 com Grupo Ginga, e anuncia novo momento de negócio

- The LED recebe aporte de BRLm 150 em rodada Growth liderada pela Kinea

- Lastlink faz rodada de BRLm 28 com Astella e BTG para brigar com a Hotmart

Intenções e Estratégias

- Correios aprovam plano de reestruturação, com BRL 1,5 bi por venda de imóveis e possíveis fusões

- Após aporte de BRLm 50 da Monashees, 180 Seguros acelera expansão e novos produtos

M&A

- DOT Digital Group anuncia aquisição da Edusense, em transação sem valor divulgado, e avança na estratégia de educação corporativa digital

- Navemazônia assume WPL e cria novo gigante de transporte fluvial de combustíveis na Amazônia com aval do Cade

- Colégios Albert Sabin e Vital Brazil são vendidos ao fundo britânico Stirling Square por cerca de BRLm 500

- Eletromidia assina acordo para comprar 100% da Context

- Fundo de Lemann vende Edify para Arco Educação em transação sem valor divulgado

TMT

Fundraising

- A Sororitê Ventures fez aporte de BRLm 5 na plataforma de serviços para idosos Sanii

- ColmeIA capta BRLm 18 em rodada follow-on com Crescera Capital – aproximando a ColmeIA de um valuation de BRLm 500

- Multiagents, plataforma de agentes de IA voltada para automação de tarefas em empresas, captou aproximadamente BRLm 1,5 em uma rodada com participação do fundo norte-americano Conscience

M&A

Dicembre si apre con un ulteriore colpo di Bending Spoons, che mette a segno un’acquisizione per mezzo miliardo USD di Eventbrite, continuando una serie di acquisizioni ed ottimizzazioni nel mondo tech. Brookfield fa shopping in Italia, comprando Fosber per quasi $1B. Infine, il neonato NewPrinces Group coglie la palla al balzo dalla chiusura di Carrefour per rilevarne gli asset.

Ecco i dettagli sulle informazioni più rilevanti:

- L’unicorno milanese cala un altro asso e rileva il gigante del ticketing Eventbrite, per 500 milioni di dollari. Bending Spoons conferma la sua natura di “macchina da ottimizzazione” globale: acquisire brand digitali iconici ma stanchi per rigenerarli. Dopo Evernote e WeTransfer, l’ingegneria italiana sfida la Silicon Valley sul suo stesso terreno.

- Il private equity nordamericano scommette pesante sulla meccanica lucchese. Brookfield stacca un assegno monstre da 900 milioni di dollari per Fosber, leader nel cartone ondulato. Un deal che certifica l’eccellenza del manifatturiero italiano: i grandi capitali globali vedono nelle nostre fabbriche asset reali capaci di generare cassa anche in un mondo volatile.

- Terremoto nella distribuzione: NewPrinces Group chiude il cerchio e finalizza l’acquisizione degli asset di Carrefour Italia. Il passaggio di mano ridefinisce gli equilibri del retail, con il gruppo italiano che scommette sul rilancio della rete attraverso un’integrazione mirata a recuperare margini e aggressività commerciale sul territorio.

Troverete questo e molto altro in questa edizione di M&A Teaser Italia.

Deal Tracker

Trasferimenti

- LB Capital alza il tiro sul private capital arruolando Pierluigi Borle Gioppi. A lui le chiavi delle operazioni in Club Deal: una mossa che segnala la volontà di strutturare veicoli d’investimento sempre più sofisticati per aggregare capitali privati a caccia di rendimenti decorrelati dai mercati tradizionali.

- Cambio al vertice per la compagnia del movimento cooperativo. Assimoco affida la direzione generale a Mirella Maffei, scegliendo la continuità strategica per navigare un mercato assicurativo sempre più complesso. La sfida è blindare il legame tra etica e profitto, innovando l’offerta senza tradire il DNA mutualistico.

- Scalable Capital affida l’Italia a Michele Raisoni. È la scommessa sulla maturità del risparmiatore italiano, sempre più attratto da piattaforme digitali e costi contenuti. Una sfida diretta all’industria tradizionale del risparmio gestito, costretta a guardarsi le spalle dall’avanzata inesorabile della democratizzazione finanziaria.

- Il colosso dell’immobiliare logistico serra i ranghi in Italia. Con la nomina di Sobotkova e Casalenuovi a Co-Managing Director, Panattoni scommette su una governance bicipite. L’obiettivo è chiaro: presidiare un mercato cruciale per le supply chain europee, dove la fame di spazi moderni continua a sfidare i cicli economici.

- La guerra dei talenti nel private banking non conosce tregua. Ersel blinda la squadra con tre innesti senior, confermando che nella gestione dei grandi patrimoni il fattore umano resta l’asset più prezioso. Una mossa tattica per alzare l’asticella della consulenza in un mercato dove la fiducia è la vera valuta.

- Azimut alza il tiro e affida a Rodolfo Errore la regia dell’area EMEA per la divisione Capital Solutions. Non è un semplice cambio di poltrona, è una dichiarazione d’intenti: il gruppo vuole aggredire i mercati internazionali con la finanza strutturata per le imprese. Serve esperienza manageriale pesante per coordinare la crescita oltre i confini domestici.

Global trends

-

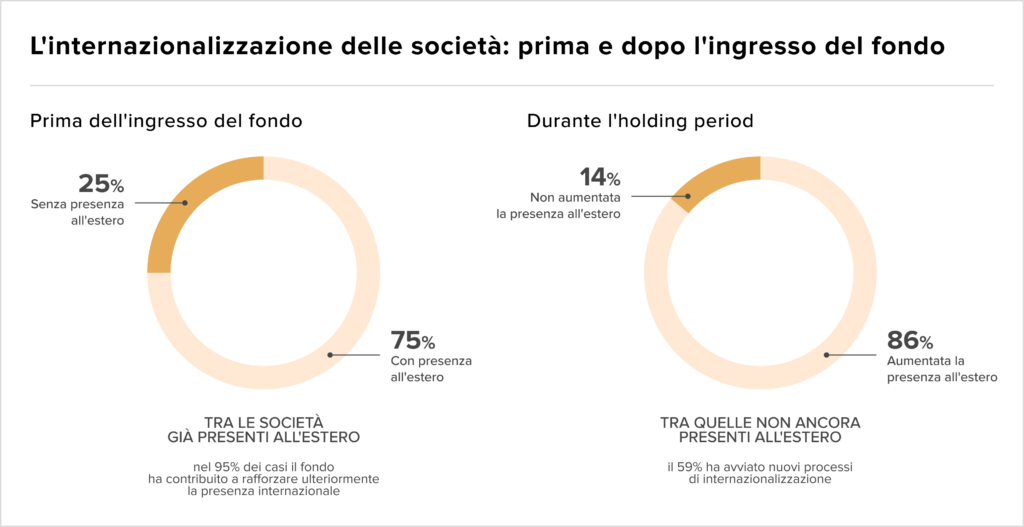

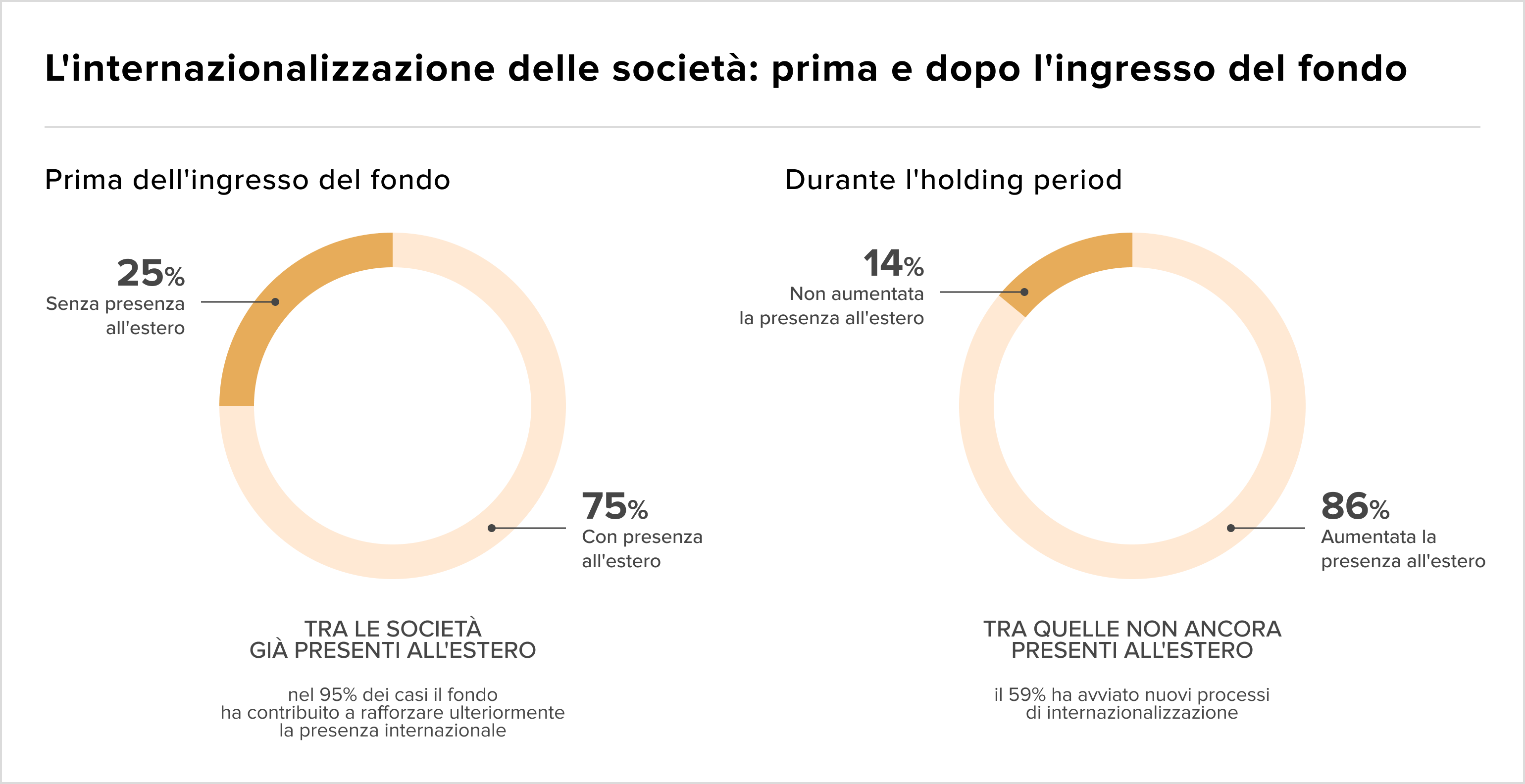

La ricerca AIFI-GPL rivela che il Private Equity agisce da moltiplicatore globale. I fondi privilegiano target già internazionalizzati, ma è nell’holding period che avviene l’accelerazione: il 95% delle partecipate rafforza l’export, mentre il 59% delle domestiche varca i confini per la prima volta. Complessivamente, l’impatto espansivo tocca l’86% dei casi.

-

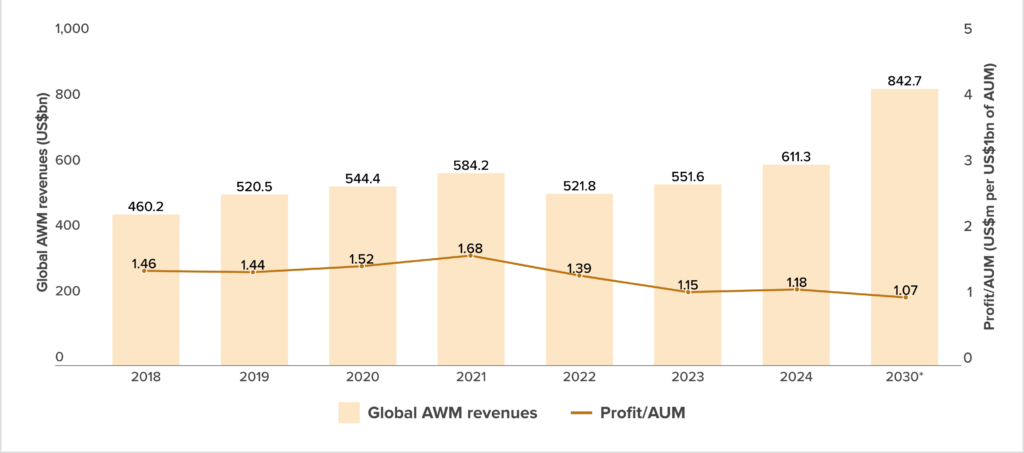

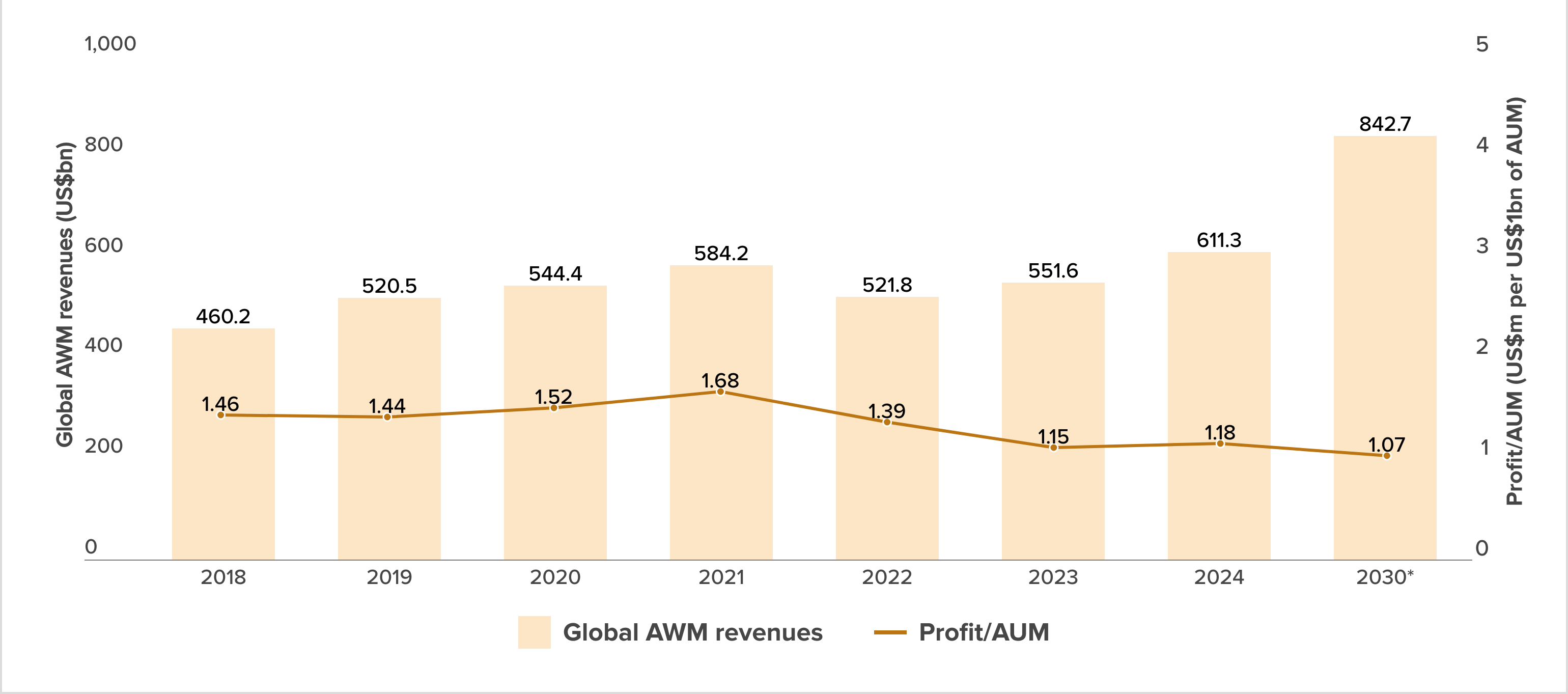

PwC traccia la fine della vecchia finanza: la gestione attiva tradizionale cede il passo. Il futuro dei ricavi globali si gioca sulla polarizzazione: o strumenti passivi a basso costo o private assets ad alto rendimento. Chi resta nel mezzo è destinato all’irrilevanza in un mercato che non fa più sconti alle rendite di posizione.

- C’è un ingranaggio rotto nel motore italiano. I dati svelano un disallineamento inquietante: la disponibilità finanziaria è ai massimi, eppure la crescita ristagna. Non è crisi di risorse, ma di allocazione. Il capitale resta parcheggiato o circola in rendite sterili, fallendo la missione cruciale: trasformare la liquidità in produttività reale.

- Mentre si chiude un 2025 complesso, i segnali dai listini sono inequivocabili: la vecchia mappa non serve più. Tra rotazione settoriale e incognite geopolitiche, la strategia passiva cede il passo alla gestione attiva. Chi non ricalibra ora l’asset allocation rischia di affrontare le turbolenze del nuovo anno senza protezioni adeguate.

Bancario/Assicurativo

Landscape

- La bufera giudiziaria sulla scalata senese a Mediobanca non deve diventare un’arma politica. Tajani difende a spada tratta l’operato del Tesoro: “Giorgetti inattaccabile, mi auguro non sia giustizia a orologeria”. Mentre la Procura indaga su presunte irregolarità, la politica alza un muro di protezione attorno a Via XX Settembre per evitare che l’inchiesta deragli i piani industriali del nuovo corso bancario.

- Luigi Lovaglio ha compiuto il miracolo contabile salvando il Monte, ma la traversata nel deserto non è finita. Ora serve la visione industriale: trasformare una banca risanata in una macchina da profitti sostenibili. Il mercato non farà sconti: senza più l’alibi della crisi, Siena deve dimostrare di poter correre (o sposarsi) alle proprie condizioni.

- Andrea Orcel squarcia il velo di ipocrisia sul collocamento governativo. A verbale resta la frustrazione di Unicredit: pronti a comprare, ma bloccati da un “tutto esaurito” che sa di mossa difensiva. Non è solo un mancato deal, è la fotografia di un sistema che alza barricate quando il predatore si fa troppo vicino.

- Mentre i colossi bancari desertificano gli sportelli, il Credito Cooperativo si prende la sua rivincita storica. Raccolta e impieghi volano: è la vittoria del modello di prossimità contro la standardizzazione degli algoritmi. Le Bcc occupano gli spazi lasciati vuoti dalle big, dimostrando che conoscere il cliente vale più di un bilancio ripulito.

- Fumata bianca a Mediobanca: si chiude l’era Nagel-Vinci con un accordo tombale da 5 milioni di euro. Non è solo una questione di buonuscite, è la fine di un ciclo di potere nel “salotto buono” della finanza milanese. La governance si normalizza, le vecchie tensioni si sciolgono: il prezzo della pace armata è stato pagato.

- Il compromesso è servito. Niente tassa sugli extraprofitti, ma un anticipo di cassa sulle imposte differite. Il sistema bancario accetta di puntellare i conti pubblici garantendo liquidità immediata al governo: un do ut des pragmatico che disinnesca lo scontro istituzionale e salva i dividendi agli azionisti.

- Luci e ombre nel report Covip. Le Casse professionali toccano il record storico di 125,1 miliardi di patrimonio, confermandosi investitori istituzionali di primo livello. Ma c’è una zavorra: i fondi immobiliari soffrono pesantemente. Si apre il dibattito sull’asset allocation: serve diversificare oltre il “mattone di carta” che non garantisce più i rendimenti di un tempo.

- Il colosso dei servizi agli investitori, spalleggiato da Astorg, mette la bandierina su Milano acquisendo Zenith Global. Non è una semplice market entry, è una dichiarazione d’intenti: il mercato italiano della finanza strutturata e dell’asset servicing diventa cruciale per le strategie di consolidamento paneuropeo dei grandi player internazionali, pronti a integrare le eccellenze locali.

- Vento freddo dalla City sul credito tricolore. Barclays taglia il giudizio su Mediobanca e Credem in ottica 2026. Il messaggio è netto: la festa dei tassi è finita, il margine di interesse (NII) ha toccato il picco e ora si scende. Gli investitori devono ricalibrare le aspettative: la rendita di posizione svanisce, torna a contare la pura efficienza operativa.

M&A

- Il rullo compressore di Wide Group (Pollen Street Capital) non conosce soste: quarto add-on del 2025 con l’acquisizione di Ariostea Broker dalla famiglia Giovannini. La strategia è cristallina: aggregare un mercato frammentato tramite un buy-and-build aggressivo. Tecnologia e capitali londinesi per creare un gigante italiano dell’intermediazione assicurativa.

- Piccolo M&A, grande strategia nel mondo dei servizi. Brandy Studio ingloba il ramo marketing di BeMyCompany: un deal che segnala la necessità di massa critica anche nelle boutique creative. In un mercato frammentato, integrare competenze verticali è l’unica via per offrire servizi “end-to-end” e non restare marginali.

Consumo

Landscape

-

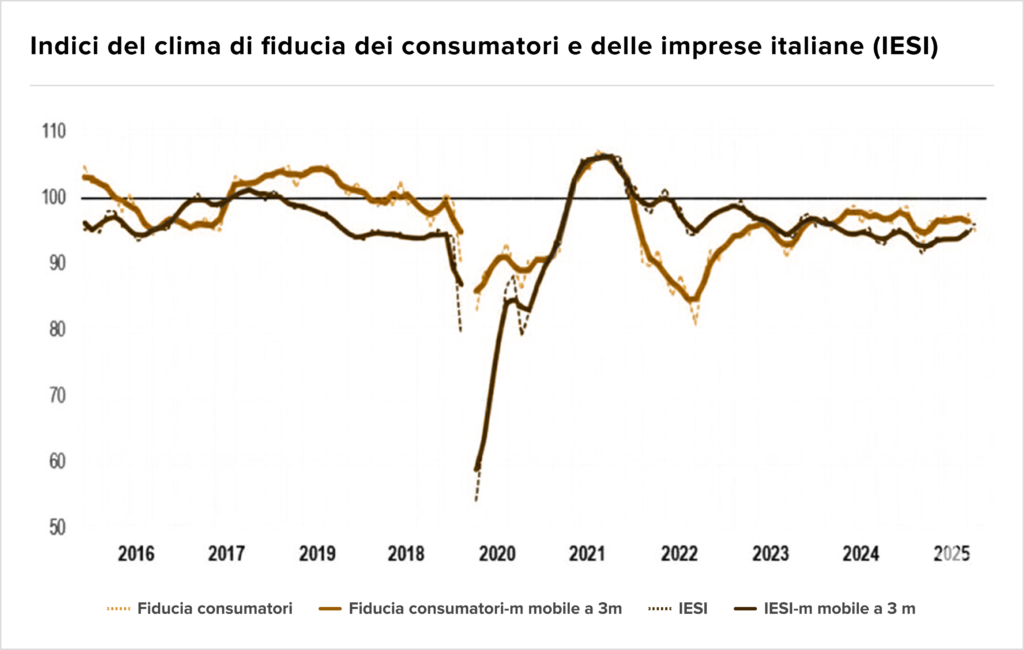

L’indice Istat svela il paradosso di novembre: la fiducia sale, trainata dall’ottimismo dei servizi, mentre le aspettative future crollano. È il sintomo di un’economia che regge l’urto presente ma non vede una rotta chiara all’orizzonte, con la manifattura che gela gli investimenti per il 2026 temendo una frenata strutturale.

- Bertelli e Guerra tracciano la linea del Piave: stop alle acquisizioni fino al 2028. Dopo il colpo grosso su Versace, la priorità assoluta è l’integrazione operativa e l’estrazione di sinergie. Un messaggio chiaro al mercato: la fase di caccia è chiusa, ora conta solo l’esecuzione industriale per non disperdere valore nel risiko del lusso.

- L’ambizione cinese non ha confini: dopo aver digerito Fila, Anta prepara l’assalto a Puma. È la geopolitica applicata allo sportswear: Pechino usa la leva finanziaria per comprare heritage e tecnologia occidentale. Se il deal va in porto, si ridisegnano gli equilibri globali contro i giganti americani Nike e Adidas.

- L’Europa svela un paradosso economico: mentre i consumi fuori casa flettono (-0,6%), il dolce diventa un asset rifugio. Con una crescita continentale del 6% e 3,2 miliardi di porzioni, l’Osservatorio Sigep certifica che la gratificazione non è un semplice lusso, ma una variabile macroeconomica resiliente alla stagnazione.

- Dimenticate il fast fashion: il Dragone scala la catena del valore e sfida l’Europa sul terreno sacro del lusso. Forbes traccia la nuova rotta di Pechino, che punta su heritage e qualità per erodere quote ai marchi occidentali. Non vogliono più essere la fabbrica del mondo, vogliono esserne l’atelier.

M&A

- EssilorLuxottica si prepara a rilevare tra il 5 e il 10% di Armani. Si disegna l’assetto difensivo definitivo: blindare l’indipendenza del marchio iconico attraverso un incrocio azionario industriale che tiene alla larga gli appetiti dei conglomerati francesi.

- Colpo di mercato per il gruppo torinese che si aggiudica l’iconico marchio del surfwear Sundek. Non è solo shopping, è strategia industriale: BasicNet amplia il perimetro replicando il modello di business che ha già fatto volare K-Way. Un’operazione chirurgica, supportata da un fitto pool di advisor legali e finanziari, per diversificare l’offerta lifestyle.

- FVS SGR e Clessidra Capital Credit non si fermano: la loro platform company Candy Factory acquisisce Italgum Caramelle. È il consolidamento del “Made in Italy” dolce: unire le forze per scalare i mercati. Le famiglie fondatrici restano a bordo, scommettendo su un piano industriale che mira a 60 milioni di ricavi già nel 2025.

- Fine di un’era per la dinastia della frutta secca. Illimity SGR assume il controllo di Noberasco, iniettando le risorse necessarie per il turnaround. È il paradigma del capitalismo italiano contemporaneo: i brand storici, soffocati dalla leva finanziaria, devono cedere il passo ai fondi specializzati per garantire la continuità industriale e salvare il Made in Italy.

- Operazione completata: Prada strappa il 100% di Versace a Capri Holdings per 1,25 miliardi. Dopo sette anni di “esilio” americano, un’icona nazionale torna sotto bandiera italiana. Closing firmato il 2 dicembre, compleanno del fondatore Gianni: simbolismo potente per un reshoring di lusso che sfida i giganti francesi.

- Un pezzo di storia alimentare italiana cambia pelle. Newport & Co, società benefit, rileva Prodotti Baumann: non è una semplice acquisizione, ma un’operazione di salvataggio culturale. L’obiettivo è rivitalizzare il mitico “dado” e le gelatine, coniugando l’heritage del Made in Italy con i nuovi paradigmi della sostenibilità d’impresa.

- Terremoto nella distribuzione: NewPrinces Group chiude il cerchio e finalizza l’acquisizione degli asset di Carrefour Italia. Il passaggio di mano ridefinisce gli equilibri del retail, con il gruppo italiano che scommette sul rilancio della rete attraverso un’integrazione mirata a recuperare margini e aggressività commerciale sul territorio.

- La holding di Novara rimescola le carte e rileva il 42% di Legami. Non è solo diversificazione, è l’intuizione che nell’era digitale l’oggetto fisico, ironico e tangibile, conserva un valore premium. De Agostini inietta capitali per trasformare una boutique creativa in un brand globale, sfidando la smaterializzazione dei consumi.

- La platform company Inovara (Ambienta) continua la campagna acquisti e annette IBL, specialista nei preparati a base frutta. È l’ennesimo add-on strategico che rafforza il polo degli ingredienti alimentari. Logica industriale impeccabile: integrazione verticale e sinergie immediate in un mercato affamato di soluzioni clean label.

Energia

Landscape

- Navigare al buio nella transizione ecologica è un lusso che non possiamo permetterci. Atena lancia “Atlante”, la bussola dati per decifrare il cambiamento energetico. Non è un esercizio accademico, ma uno strumento tattico per imprese e decisori: capire oggi dove va l’energia significa anticipare i flussi di investimento (e i profitti) di domani.

-

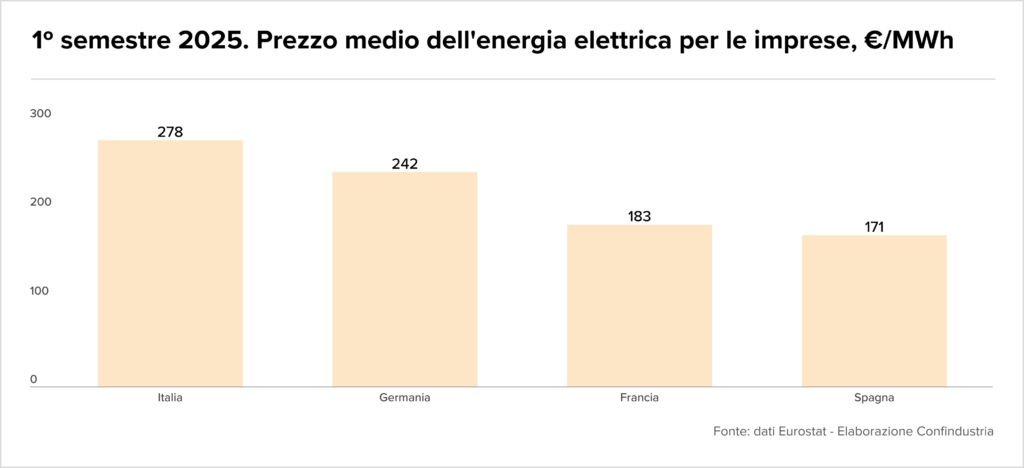

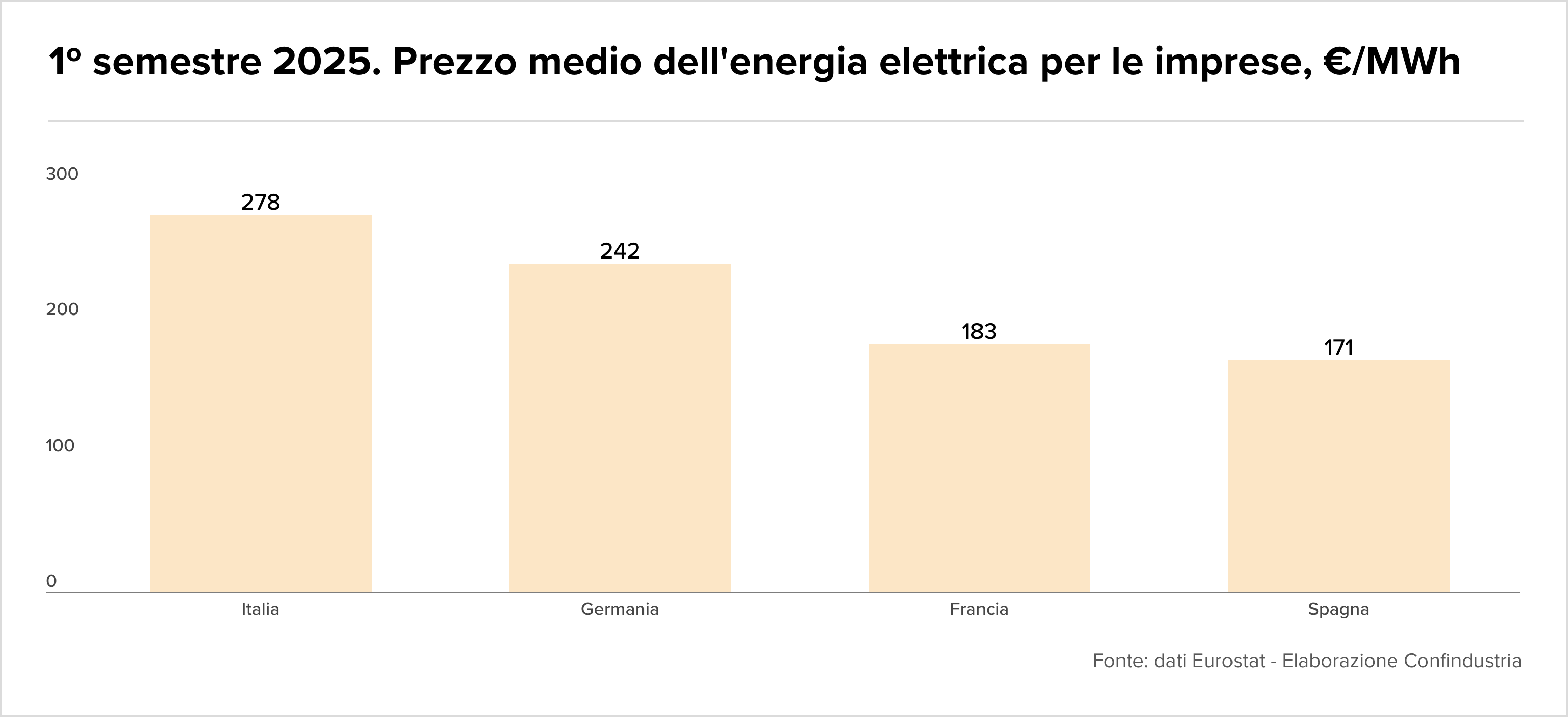

L’allarme di Confindustria è una sentenza inappellabile sulla competitività: le nostre bollette, le più care del continente, non sono solo un costo, ma un gap strutturale che ci spinge fuori mercato. Mentre i competitor europei corrono, l’industria italiana paga dazio su ogni kilowattora, erodendo margini vitali per l’export.

-

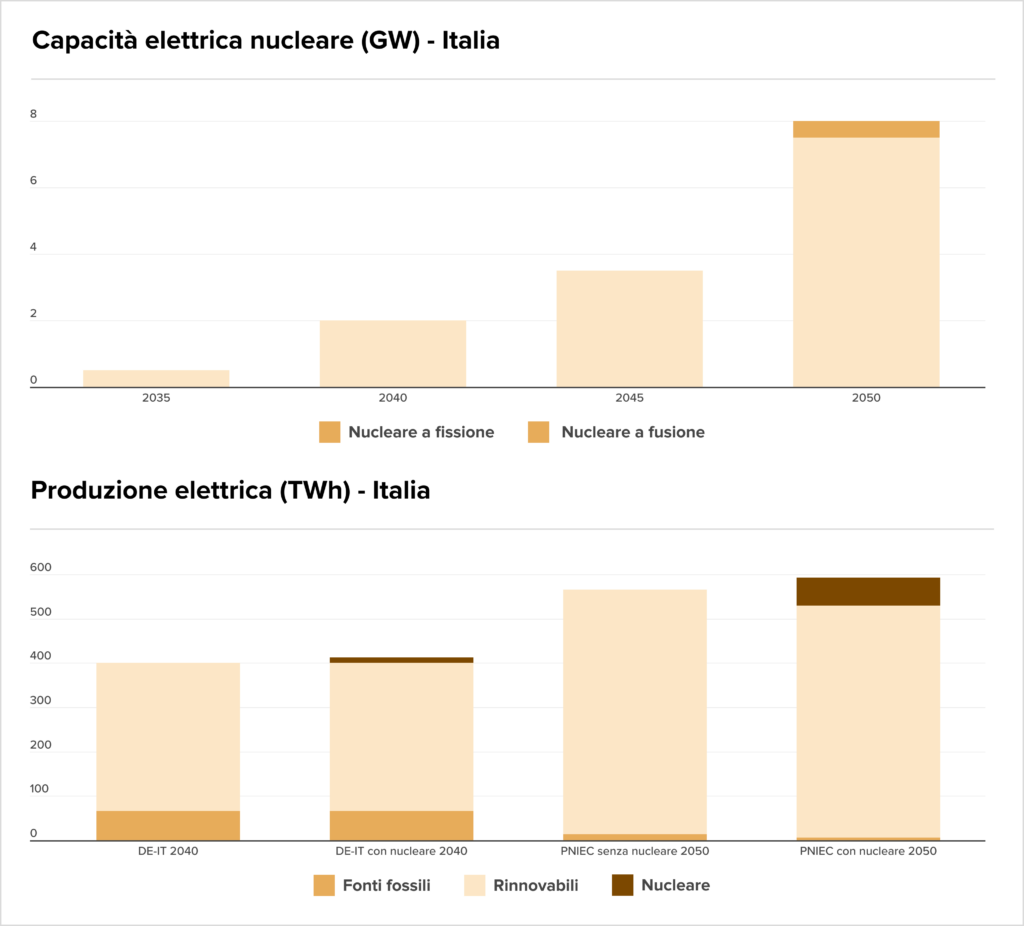

I dati del Polimi impongono un brusco bagno di realtà ai sogni energetici del governo. Il ritorno al nucleare entro il 2050 non è una marcia trionfale ma un percorso a ostacoli tecnici ed economici. Senza un’accelerazione industriale drastica e immediata, l’atomo resterà una variabile marginale, incapace di garantire la decarbonizzazione nei tempi previsti. In foto: Fonte: Pniec; Terna-Snam. Gli scenari DE-IT (Distributed Energy Italia) sono proiezioni Terna-Snam che rappresentano le variazioni dello scenario Pniec in linea con i Paesi europei fino al 2040 e prevedono una quota maggiore di rinnovabili distribuite e prosumer.

- Green Arrow Capital lavora di fino sulla struttura del capitale, rifinanziando il portafoglio eolico da 39 MW in Basilicata. Con asset maturi e funzionanti, la creazione di valore passa dall’ingegneria finanziaria: abbattere il costo del debito e allungare le scadenze è la mossa tattica per massimizzare l’IRR in un contesto di tassi volatili.

- Mentre l’Italia cerca disperatamente il mix perfetto, la geotermia resta un “club” esclusivo della Toscana. Una risorsa baseload formidabile e pulita che rimane confinata a livello regionale. La burocrazia e la mancanza di visione nazionale tengono ingessato un potenziale che potrebbe alleggerire la dipendenza estera, lasciando vapore e megawatt nel sottosuolo.

- L’agrivoltaico esce dalla nicchia e diventa industria pesante: 115 GW di progetti nei primi nove mesi del 2025 sono un segnale fragoroso. I dati Althesys confermano che la simbiosi tra pannelli e colture non è solo fattibile, è un moltiplicatore economico. È la fine della guerra ideologica sull’uso del suolo: l’energia diventa il secondo raccolto dell’agricoltore.

- Plenitude pianta la bandiera in Calabria: parte il cantiere del parco eolico di Tarsia. Eni conferma che la transizione energetica non si fa con gli slogan ma con l’acciaio e le turbine. Un investimento infrastrutturale che valorizza il Mezzogiorno come hub energetico verde, accelerando la corsa verso la decarbonizzazione nazionale.

- Eni non molla la presa sugli idrocarburi e conquista il blocco offshore nelle acque argentine insieme a YPF. È la realpolitik energetica: diversificare le fonti di approvvigionamento globali e presidiare bacini strategici restano priorità assolute per garantire la sicurezza energetica e i flussi di cassa, mentre altrove si costruisce il futuro green.

M&A

- La transizione non si fa solo con i cavi, ma con i dati. ACP SGR, tramite il fondo SSF, entra in Bia Power puntando sul software per la ricarica elettrica. Una mossa che anticipa il futuro: il valore non sarà più nella semplice infrastruttura fisica, ma nell’algoritmo capace di ottimizzare i flussi energetici della rete.

- Eni Plenitude non bada a spese e mette sul piatto fino a 587 milioni di euro per il 100% di Acea Energia e il 50% di Umbria Energy. Un’operazione titanica, orchestrata da Rothschild e Jefferies, che ridisegna le gerarchie del retail elettrico nazionale blindando la leadership di Eni.

- Operazione di finanza strutturata nel cuore della meccanica specializzata. Siwis, supportata dal private debt di Bravo Capital, acquisisce Drilling Solutions. Un buyout che inietta liquidità per internazionalizzare una nicchia tecnica. Gli advisor hanno disegnato un’architettura finanziaria su misura per garantire la continuità operativa e spingere la crescita oltre confine.

- Scambio di figurine strategico nelle rinnovabili. Alerion Clean Power monetizza e cede la quota in Eolica PM; dall’altra parte del tavolo, Estra (Gruppo Plures) ha fame di asset green e compra. È la rotazione del capitale tipica della transizione energetica: chi sviluppa vende, le multiutility consolidano per decarbonizzare il proprio mix di generazione.

- Il consolidamento delle utility del Nord-Est procede a marce forzate. AGSM AIM completa l’acquisizione di Global Power, rafforzando la presa sul mercato retail veronese. In un settore dove i margini si fanno sui volumi e sulla densità territoriale, inglobare portafogli clienti è l’unica via per restare rilevanti nella competizione con i giganti nazionali.

- Ravano Power diversifica il mix e rileva il 100% di Aemmegi. L’energia programmabile da biomassa è il tassello mancante per stabilizzare la volatilità di solare ed eolico. Un’acquisizione mirata che integra produzione agricola e generazione elettrica, creando un modello di business ibrido capace di difendersi meglio dalle oscillazioni dei prezzi zonali.

- Il gruppo Elevion mette le mani su Maserati Energia e sul suo impianto di valorizzazione rifiuti. È la scommessa sulla circolarità reale: trasformare lo scarto organico in energia non è più solo etica, è margine operativo. Un deal che posiziona Elevion al centro della filiera del waste-to-energy, dove la materia prima è (purtroppo) inesauribile.

- Ascopiave prosegue la campagna di densificazione territoriale acquisendo Società Impianti Metano. In un mercato che guarda all’elettrico, l’infrastruttura gas resta un asset strategico difensivo fondamentale (RAB). Consolidare la distribuzione locale significa garantirsi flussi di cassa regolati e stabili, linfa vitale per finanziare la transizione del gruppo.

Healthcare

Landscape

- L’Europa prova a non perdere il treno dell’innovazione sanitaria. La BEI scende in campo a fianco di Angelini Ventures per co-finanziare le startup Life Science. È la risposta del Vecchio Continente allo strapotere americano: unire la potenza di fuoco pubblica al know-how industriale privato per far nascere i futuri unicorni della salute.

- Siamo il Paese della grande bellezza, anche artificiale. L’Italia svetta in Europa per procedure di medicina estetica: un primato che spiega perfettamente l’assalto dei fondi al settore. Una società che invecchia ma rifiuta il declino fisico è il motore immobile di un’industria miliardaria, resiliente a qualsiasi scossone macroeconomico.

M&A

- Anche il benessere entra nei radar dei grandi investitori istituzionali. L’ELTIF Infrastrutture di Ali SGR tratta l’ingresso in Terme e Spa Italia. È un cambio di paradigma: le terme non sono più solo svago, ma asset reali capaci di generare flussi di cassa stabili, parificabili a un’autostrada o una rete energetica.

- Il risiko delle cliniche dentali continua a macinare deal. Dental Feel Group ingloba Dott. Luis Novestar, proseguendo la strategia di aggregazione che sta trasformando l’odontoiatria da artigianato a industria. L’obiettivo è chiaro: economie di scala e brand unico per dominare un mercato ancora polverizzato.

- Equita Smart Capital ELTIF continua la campagna nella diagnostica. La partecipata Clonit rileva Dia.Pro, saldando un asse strategico nell’in-vitro. Non è semplice somma algebrica, ma integrazione di know-how per scalare i mercati internazionali, dove la massa critica è l’unica difesa contro i giganti del pharma.

- La fame del colosso britannico Ardonagh non si placa. Tramite la controllata Mediass, mette le mani su Assimedici, blindando la leadership nella nicchia ad alto valore della responsabilità sanitaria. È la conferma che il brokeraggio italiano è ormai terra di conquista per i grandi consolidatori globali a caccia di specializzazione.

- Il consolidamento dei laboratori è una marcia forzata. PureLabs ingloba Ricerca Diagnostica, confermando che nella sanità privata la frammentazione è un lusso del passato. Servono volumi per ammortizzare le tecnologie: i piccoli centri vengono assorbiti dai grandi network in una corsa all’efficienza che ridisegna la geografia della salute sul territorio.

- Il Private Equity flirta con la dermo-cosmesi. Ethica Global Investments entra in maggioranza in Seventy BG, puntando sull’eccellenza “made in Italy” nella cura della pelle. L’obiettivo è chiaro: prendere un gioiello di nicchia e trasformarlo in un brand internazionale, cavalcando l’onda lunga di un settore che non conosce crisi di domanda.

- Koinos Capital non si limita a comprare, costruisce. Con un triplice colpo (Dynamicom, Formedica, Meeting Planner) lancia Meduspace. È la risposta industriale alla frammentazione dei servizi per il Life Science: un unico hub capace di dialogare con Big Pharma offrendo formazione e comunicazione integrata. La scala dimensionale diventa l’unico passaporto per competere.

- Il fondo paneuropeo Carbyne Equity Partners entra nel capitale di Chemia, storico marchio della nutrizione vegetale. La famiglia Giberti cede il controllo ma reinveste restando alla guida operativa. Capitali freschi per spingere l’internazionalizzazione e l’R&D in un settore difensivo ma cruciale come l’agrochimica.

- La sanità privata tricolore resta preda ambita. Il gruppo francese Simago cala in Italia e acquisisce il Centro Radiologico Polispecialistico di Ternate. È la conferma di un trend inarrestabile: il consolidamento europeo della diagnostica per immagini. I giganti esteri rastrellano le eccellenze locali per costruire piattaforme sanitarie scalabili e integrate.

Immobiliare

Landscape

M&A

- I capitali francesi tornano a muoversi sulla “provincia ricca”. Praemia REIM acquisisce un asset strategico a Bologna, confermando la vitalità delle città universitarie come magneti per gli investitori istituzionali. Non c’è solo Milano: la ricerca di fondamentali solidi e rendimenti stabili spinge il real estate oltre i soliti confini.

- Da Berlusconi agli studenti: il simbolo di Milano 2 cambia pelle. Il San Raffaele stacca un assegno da 30 milioni a Kryalos per espandere il campus nel Palazzo dei Cigni. È il segno dei tempi: il mattone che ospitò la rivoluzione televisiva ora diventa tempio della formazione medica, asset class sempre più pregiata.

- Colliers Global Investors non bada a spese: assegno da 170 milioni per fare incetta di asset logistici in Italia. Il “mattone” industriale si conferma bene rifugio e snodo cruciale per le supply chain continentali. I grandi investitori globali votano la fiducia al sistema-Italia come piattaforma distributiva strategica per il Mediterraneo.

- Dismettere per rinascere. ATM cede l’area ex Socimi a 2C Sviluppo Immobiliare. È la parabola della rigenerazione urbana: un vuoto industriale alle porte di Milano si trasforma in opportunità di sviluppo. Un’operazione di chirurgia immobiliare che valorizza gli asset pubblici dormienti restituendoli al mercato, probabilmente in chiave logistica.

- L’Olanda scende in campo: CTP, colosso dello sviluppo industriale, entra in Italia acquisendo VLD. Un ingresso deciso su Bergamo che certifica l’attrattività del nostro comparto produttivo. I grandi player continentali non possono più ignorare la logistica tricolore: esserci significa presidiare uno snodo cruciale del traffico merci europeo.

- Il consolidamento degli affitti brevi non fa prigionieri. CleanBnB prosegue la marcia annettendo il 100% di Case Ospitali: un’operazione di pura densità che rafforza la leadership del player quotato e conferma che, nel property management, la taglia dimensionale è l’unica difesa contro la frammentazione.

- Il lusso siciliano torna a brillare grazie ai capitali internazionali. Sagitta SGR, con la potenza di fuoco di Arrow Global, rileva il Donnafugata Golf Resort. Un’operazione di rilancio che trasforma un asset distressed in una destinazione d’élite, confermando che il turismo di alta gamma nel Sud Italia resta una calamita per gli investitori sofisticati.

- Mentre si celebra il funerale dei centri commerciali, gli specialisti comprano. Il Gruppo Filcasa cede il Cinisello Shopping Center a Itay Properties. Una rotazione di asset che dimostra come il “mattone commerciale”, se ben posizionato nell’hinterland milanese, resti una macchina da reddito capace di attrarre investitori pronti a scommettere sulla tenuta dei consumi fisici.

- La logistica non dorme mai e Kryalos lo sa. Rilevando 13 hub “last mile” da Logiman, il fondo blinda la cintura strategica della distribuzione. Non stiamo parlando di semplici capannoni, ma di nodi vitali per l’e-commerce: la guerra dei tempi di consegna si vince possedendo fisicamente l’ultimo chilometro.

Industriale

Landscape

- La banca francese scommette sulla transizione marittima finanziando l’acquisto della “Eco Mediterranea” per Grimaldi Euromed. Un’operazione che salda l’asse industriale italo-francese: finanza strutturata al servizio della logistica pesante, con l’armatore napoletano che rinnova la flotta per restare competitivo nelle autostrade del mare, ormai governate dalla rigida bussola dei criteri ESG.

- I numeri di Federchimica raccontano una tenuta eroica. Con 65 miliardi di valore, il settore resiste ai costi energetici e alla concorrenza asiatica. Ma è una resistenza al limite: senza una politica industriale europea sui prezzi dell’energia, questa resilienza rischia di trasformarsi in una lenta, silenziosa deindustrializzazione della nostra base produttiva.

- I dati di metà anno tracciano un quadro di stabilità armata per l’industria lombarda. Non c’è il boom, ma arrivano i primi segnali di disgelo: la manifattura più potente d’Italia tiene le posizioni in attesa della ripresa globale. È la resilienza delle filiere d’eccellenza che, pur senza brillare, evitano la recessione tecnica.

M&A

- Cieli più sereni per l’eccellenza laziale degli interni cabina. Il colosso giapponese Jamco, con la potenza di fuoco di Bain Capital, rileva Iacobucci HF Aerospace. Un’operazione che unisce muscoli finanziari USA e pragmatismo industriale nipponico per riportare il design italiano al centro della supply chain aeronautica globale.

- Nasce un gigante globale nel “Test & Quality Engineering”. Andera Partners orchestra la fusione tra la francese Spherea e la canadese Averna, creando un player da oltre 260 milioni di ricavi. Non una semplice somma di parti, ma un salto di scala decisivo per dominare il testing tecnologico su entrambe le sponde dell’Atlantico.

- Xenon Private Equity non perde tempo e chiude un double deal strategico: acquisite Zanetti Arturo & C. e Saste Servizi Ecologici. L’obiettivo è chiaro: aggregare player frammentati per forgiare un campione industriale nella gestione dei rifiuti sanitari.

- Doppio colpo per Xenon Private Equity. Il fondo acquisisce Betoncablo e Arcsystem, orchestrando un polo integrato nelle infrastrutture e nei prefabbricati tecnologici. È il manuale del buy-and-build: unire competenze complementari per creare un player capace di cavalcare l’onda degli investimenti nelle reti e nella transizione energetica.

- La svedese Dacke Industri (galassia Nordstjernan) mette a segno il colpo e rileva il 70% di Hydronit, eccellenza nelle microcentraline idrauliche. Il fondatore Andrea Gambusera non lascia, anzi: reinveste per il 30% e mantiene il timone come CEO. Un’operazione chirurgica per consolidare il polo idraulico scandinavo con tecnologia italiana.

- Il private equity nordamericano scommette pesante sulla meccanica lucchese. Brookfield stacca un assegno da 900 milioni per Fosber, leader nel cartone ondulato. Un deal che certifica l’eccellenza del manifatturiero italiano: i grandi capitali globali vedono nelle nostre fabbriche asset reali capaci di generare cassa anche in un mondo volatile.

- In Group, spalleggiata da Bravo Capital, annette Sondedile e crea un polo di riferimento nei controlli e monitoraggi strutturali.

- Alto Capital V, in tandem con Idea Cinquanta, mette le mani sulla tecnologia antisismica di Fip Mec. È la scommessa sulla resilienza delle infrastrutture: capitali freschi per spingere un campione di nicchia del Made in Italy verso una dimensione autenticamente globale, sfruttando l’onda lunga degli investimenti pubblici.

- Il “club deal” continua a fare pulizia nella frammentazione italiana. Smart Capital, tramite il veicolo Smart4Mechanics, rileva Officina C.I. Esse. L’obiettivo è chiaro: trasformare l’eccellenza artigianale della meccanica di precisione in un sistema industriale strutturato. Piccolo è bello, ma per sopravvivere oggi serve massa critica e spalle larghe.

- La manifattura italiana va all’attacco nel Nord Europa. Industrie Polieco-MPB, sotto l’egida di RedFish LongTerm Capital, compra The Compound Company. Non è solo chimica, è geopolitica industriale: acquisire un competitor olandese significa scalare la catena del valore e imporsi come player continentale nei materiali compositi, senza timori reverenziali.

Servizi

Landscape

M&A

- Mentre l’auto annaspa, la logistica si blinda. La famiglia Conti (XCA), in orbita Arcese, rileva il ramo d’azienda di Autotrade Logistics. È il realismo industriale che vince: consolidare la filiera della movimentazione veicoli per ottimizzare i margini in un mercato che non perdona inefficienze. Un’operazione di pura densità operativa che ridisegna la supply chain del settore.

- Il consolidamento dell’istruzione d’élite accelera. Ingenium Education ingloba la St. Francis International School, confermando che l’education è diventata un’asset class pregiata. In un mondo globale, le scuole internazionali sono le nuove miniere d’oro: fabbriche di capitale umano che attirano investitori a caccia di flussi di cassa anticiclici e resilienti

- Alessandro Benetton (21 Invest) prende il volante di ParkinGO. Non è solo parcheggio, è mobilità integrata. L’obiettivo è trasformare un campione nazionale in una piattaforma europea da esportazione. I fondatori restano a bordo, ma ora c’è la potenza di fuoco per aggregare, digitalizzare e conquistare nuovi scali internazionali.

Sport

Landscape

- Il calcio italiano continua a ballare sul Titanic. Le plusvalenze coprono fino a un quarto dei bilanci: una dipendenza tossica dalla compravendita di calciatori che maschera l’incapacità cronica di generare ricavi commerciali strutturali. È un modello di business fragile, dove basta un rallentamento del mercato trasferimenti per mandare in default il sistema.

- Il patron del Napoli alza i toni: o vendita dell’impianto o addio. La battaglia per lo stadio di proprietà non è capriccio, ma necessità industriale. Per competere in Europa servono asset che generino ricavi 365 giorni l’anno, liberando il club dalla zavorra dell’immobilismo burocratico municipale.

M&A

TMT

Landscape

- L’euforia dell’Intelligenza Artificiale incontra i fantasmi del passato. Wall Street inizia a tremare: le valutazioni stratosferiche reggeranno alla prova dei profitti reali? Il dubbio serpeggia tra i trader, evocando il ricordo delle dot-com. Siamo sul crinale sottile tra la più grande rivoluzione tecnologica del secolo e l’ennesima esuberanza irrazionale.

- Non è solo hype, è un cambio di paradigma tettonico. L’Intelligenza Artificiale guiderà flussi per 600 miliardi di dollari nel Private Equity e VC entro il 2028. Siamo all’alba di una rivoluzione nell’allocazione del capitale globale: i portafogli si ridisegnano, i vecchi modelli saltano. Chi ignora l’algoritmo rischia l’irrilevanza strategica.

- Il nuovo ordine mondiale del tech ha i suoi imperatori indiscussi. Mentre l’antitrust affila le armi, il dominio di Nvidia sui chip e di Google sui dati ridisegna la mappa del potere economico globale. Non è solo business, è una questione di sovranità digitale che spaventa i regolatori e seduce gli investitori.

M&A

- L’unicorno milanese cala un altro asso e rileva il gigante del ticketing Eventbrite, per 500 milioni. Bending Spoons conferma la sua natura di “macchina da ottimizzazione” globale: acquisire brand digitali iconici ma stanchi per rigenerarli. Dopo Evernote e WeTransfer, l’ingegneria italiana sfida la Silicon Valley sul suo stesso terreno.

- Un terremoto scuote l’America: Netflix inghiotte la Warner Bros per 82 miliardi. È il trionfo definitivo della Silicon Valley sulla vecchia Hollywood. Mentre la “tv classica” di Discovery si stacca, nasce un impero dell’immaginario senza rivali. Non è solo business, è la nuova egemonia culturale che ridisegna l’Occidente.

- Il Club Deal si dimostra leva potente per il tech. Orienta Partners organizza la cordata per rilevare InUnUp, regalando l’exit a Smart Capital. Un passaggio di testimone classico che inietta nuove risorse nel marketing tecnologico, mentre gli investitori della prima ora monetizzano il valore creato.

- Zucchetti prosegue la sua inarrestabile annessione del software italiano. L’ingresso in Sinergest blinda il segmento della compliance e della sicurezza sul lavoro. Non è semplice shopping, è la costruzione metodica di un’autarchia digitale capace di coprire ogni singola esigenza operativa delle PMI, chiudendo gli spazi ai competitor.

- La fame di TeamSystem non si placa. Con l’acquisizione di Arca24, il gruppo (spalleggiato da Hellman & Friedman) mette un altro tassello strategico, questa volta nell’HR Tech. Digitalizzare il recruiting è la nuova frontiera: l’azienda diventa un ecosistema unico dove il software gestisce non solo i conti, ma anche le persone.

- I dati sono il nuovo petrolio, e Stirling Square vuole la raffineria. Il fondo prende il controllo di Iconsulting, eccellenza nel Big Data e AI. Un’operazione che certifica la maturità del tech italiano: capitali internazionali a caccia di competenze specifiche per governare la complessità analitica delle imprese in un mercato data-driven.

- Il Private Equity muove le pedine del tech tricolore. H.I.G. incassa e passa la mano, EMK Capital mette sul piatto circa 260 milioni per il controllo di Project Informatica. La scommessa è chiara: consolidare un polo IT capace di scalare i 450 milioni di fatturato, sfruttando il “passaggio del testimone” finanziario come motore di crescita.

- La consulenza tradizionale ha bisogno di sangue nuovo. Excellence Group non aspetta e ingloba KVA, venture studio nativo AI. È la corsa all’oro algoritmico: integrare l’intelligenza artificiale nei processi di business non è più un optional, ma l’unico modo per restare rilevanti nella catena del valore e difendere i margini.

- Quadrivio Group aggrega Pipeline, One4 e MDM, costruendo un hub nazionale dell’intelligenza artificiale. È la strategia del “fare massa”: unire le eccellenze frammentate per competere in un mercato dove la taglia dimensionale è l’unica garanzia di sopravvivenza.

- Il private equity tedesco Auctus Capital Partners fa shopping ad alta tecnologia in Lombardia e rileva la maggioranza di Delo Instruments. Un gioiello del testing elettronico che attira capitali d’Oltralpe per scalare il mercato. I fondatori non escono di scena, anzi: reinvestono e restano al comando. Manifattura italiana e finanza tedesca: un asse che si rafforza.

- La tela europea degli eredi Berlusconi si espande a Lisbona: MFE rastrella il 3,29% di Impresa. Un chip tattico che replica il copione tedesco: entrare in punta di piedi per costruire, pezzo dopo pezzo, quel polo televisivo continentale necessario per sopravvivere alla guerra dello streaming contro i giganti USA. La strategia è aggregare o sparire.

Fundraising

- Un nuovo attore entra nell’arena del Private Equity. Theorikon Industrial Fund punta dritto al cuore manifatturiero italiano con ticket tra i 5 e i 50 milioni. Il target è quel tessuto di aziende industriali solide che necessitano di capitale paziente per il salto dimensionale, colmando il gap tra piccola impresa e multinazionale.

- Future Energy Ventures fa il pieno raccogliendo 235 milioni di euro per i suoi nuovi veicoli. Non si finanziano solo pale e pannelli, ma il software che li governa: la scommessa è che la decarbonizzazione passi inevitabilmente dalla digitalizzazione spinta delle infrastrutture.

- Il modello del Search Fund continua a sedurre. Vitis Capital chiude la raccolta iniziale a 680mila euro con un obiettivo chirurgico: individuare, acquisire e gestire un’unica PMI italiana. È la micro-finanza che si fa imprenditoria attiva, offrendo una soluzione concreta al problema del ricambio generazionale nelle nostre aziende familiari.

We’ve reached December, but dealmakers aren’t taking time off just yet. We’ve seen notable deals in solar and wind, as well as a collapsed merger.

Top stories include:

- Prime Capital acquires Project Jupiter from WBS Power, paving the path for 500 MW hyperscale data-centre integration.

- Low Carbon secures £1.1 bn capital package led by CVC DIF.

- HICL and TRIG abandon proposed £5.3 bn merger after investor pushback.

If you’d like to keep following these stories as they evolve, feel free to connect with me on LinkedIn.

Deals breakdown

Battery storage

- Poland | Investor acquires 52 MW standalone BESS project from PV Construction, marking continued scale-up of the country’s storage market amid rising IPP demand; JLL advised the seller on the transaction

- United Kingdom | HICL and TRIG abandon proposed £5.3 bn merger after investor pushback, halting plan to form UK’s largest listed infrastructure fund despite scale synergies across 2.3 GW renewables portfolio

Multiple

- Germany | Natural Power acquires renerco plan consult from BayWa r.e., expanding European consultancy footprint and deepening presence across key renewable markets following recent Italy entry

- United Kingdom | Low Carbon secures £1.1 bn capital package led by CVC DIF, granting investor majority control and accelerating buildout of multi-GW pan-European renewables pipeline toward next-generation IPP growth

Solar

- United Kingdom | Capital Dynamics acquires 121 MW Clump and Yanel solar portfolio from BayWa, expanding consented pipeline as seller posts 235 MW of 2025 approvals and advances large-scale storage strategy

- United Kingdom | Downing acquires two RTB solar projects totaling 35 MWp in Devon and Shropshire, strengthening CfD-backed buildout as firm advances scaled solar portfolio strategy for 2027 delivery

Solar + BESS

- Germany | Prime Capital acquires 500 MW / 2 GWh Project Jupiter from WBS Power, backing nation’s largest planned co-located PV-plus-storage scheme and paving path for 500 MW hyperscale data-centre integration

- United Kingdom | Ethical Power sells 49.9 MW co-located Burcot Energy Park to Chint Solar, marking England’s first grey-belt-designated solar project and advancing 2027 delivery of PV-plus-BESS development

Wind

- Finland | Enefit Green sells 72 MW Tolpanvaara wind farm for €83 m to TD Greystone and Rabbalshede Kraft, exiting non-core market as parent Eesti Energia refocuses growth on Baltics and Poland

- Finland | Fortum acquires ABO Energy’s 4.4 GW onshore wind development portfolio for up to €65 m, bolstering Nordic pipeline to ~8 GW as utility positions for future industrial-driven power demand growth

- France | Encavis acquires 41 MW Vallée de Joie wind farm under construction from Enertrag, expanding French portfolio to 250 MW and reinforcing long-standing partnership ahead of 2026 grid connection

- Germany | European Energy sells majority stake in 21 MW onshore wind portfolio to Alterric, extending long-standing partnership while recycling capital into new renewables and hybrid projects across Europe

- Ireland | Ørsted–ESB JV wins rights to develop 900 MW Tonn Nua offshore wind farm in ORESS 2, securing 20-year CfD and advancing early-stage pathway toward 2031 FID and mid-2030s delivery

- Romania | OX2 acquires three onshore wind projects totaling 235 MW from Future Power, lifting national portfolio beyond 1.1 GW and reinforcing expansion strategy in one of Europe’s fastest-growing renewable markets

- Spain | ACCIONA Energía in talks to sell 550 MW Galicia wind portfolio for ~€700 m to Recursos de Galicia, advancing multibillion-euro asset-rotation strategy and further deleveraging trajectory

- Spain | Opdenergy buys 440 MW portfolio of 13 wind farms from ACCIONA Energía for €530 m, advancing asset-rotation strategy and unlocking hybrid PV development linked to 351 MWp pipeline

Hello,

We’ve reached December, it’s all downhill from here. And yet there’s still deals being done, such as CVC’s £2bn acquisition of Smiths’ airport scanner unit.

There’s also plenty in the rumour mill, such as:

- Blackstone is making plans to sell a Canary Wharf office block

- BHP offered £40bn in its attempt to buy Anglo American

- Airport handler Menzies is considering an IPO

Thanks for reading, and connect with me on LinkedIn if you want to discuss how Ideals VDR can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Blackstone weighs second attempt to sell BP Canary Wharf office

- UK energy tech firm Kraken seeks $500m in funding round

- Airport Handler Menzies weighs IPO, acquisitions amid expansion

- ICG Real Estate is acquiring a portfolio of 24 new stores from Lidl, worth a total of €203.5m

- Perwyn to exit Interact Software to funds managed by Castik Capital

- Epiris to acquire Winterflood Business Services

- Qatar to sell $360m Sainsbury’s stake after share rally

- Saba blocks Baillie Gifford plan to combine two listed funds

- German Doner Kebab targets £1.3bn global sales as it prepares India launch

- Vodacom takes control of Safaricom in $2.4bn deal

- BHP is said to have offered £40bn in aborted Anglo Bid

- Smiths sells airport scanner unit to CVC at £2bn value

- Deutsche Börse launches €5.3bn bid for private equity-backed Allfunds

- UK’s Schroders examines options for Benchmark business, sources say

- Oil majors unite to oppose Subsea7-Saipem merger in Brazil antitrust case

- Exclusive: Amber Energy plans to hold on to Citgo refineries after takeover

- NatWest in exclusive talks to sell Cushon to Willis Towers Watson, sources said

- Domestic and General acquired by US-based insurance firm

- Asurion agrees to buy CVC-Backed UK warranty provider D&G

- Getty warns over UK operations if Shutterstock deal is blocked

- Where will DMGT find £500mn to pay for the Telegraph?

- Delta Group Plc to acquire UpScale IT

- HICL, TRIG scrap plan for £5.3bn tie-up after investor pushback

- PE firm CVC to take control of Low Carbon via £1.1bn fundraising

- Bridgepoint to buy defense communications and power company Comrod

- Fundsmith heads towards record year of outflows as investors pull more than £5bn

Industry news

- BoE lowers capital requirements for UK banks as they pass stress tests

- KKR, Apollo opt in for first BoE private markets stress test

- London Stock Exchange Group partners with OpenAI for ChatGPT data push

Salaries and bonuses

Job moves

- HSBC names former KPMG partner Brendan Nelson as chair

- JPMorgan shakes up ECM with Europe promotions

- HSBC opts for compromise candidate after shambolic search for new chair

- RBC Capital Markets hires ex-Citigroup dealmaker Weissenberger

- Consultant relations head becomes latest senior exit from Newton

- Hargreaves Lansdown taps Vanguard’s Doug Abbott for chief product officer role

- Former Newton IM chief Euan Munro joins Brooks Macdonald board

- Stifel cuts more European markets jobs after advisory shift

- Rothschild hires Barclays’ European sponsors head

- Hedge fund Rokos Capital loses London-based partner

Market trends

Megadeals dominate the market

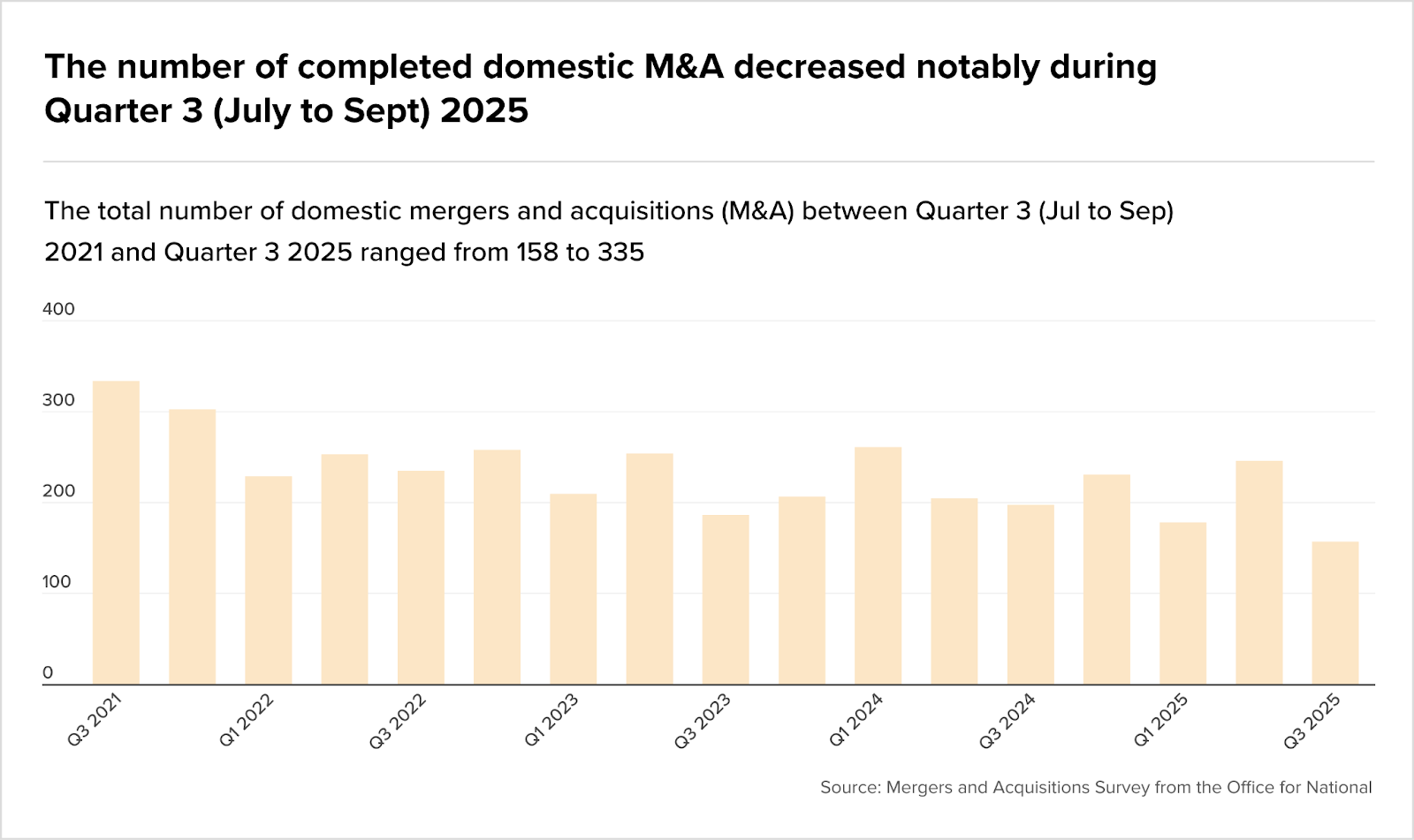

The Office for National Statistics reveals a notable contrast in Q3 2025: while UK M&A values held remarkably steady, the number of domestic deals plummeted to just 158 transactions, the lowest level since 2017.

This disparity, with domestic M&A values actually rising to £5.3bn (up £1.9bn from Q2) despite 89 fewer deals, signals a market increasingly concentrated in mega-transactions rather than broad-based activity.

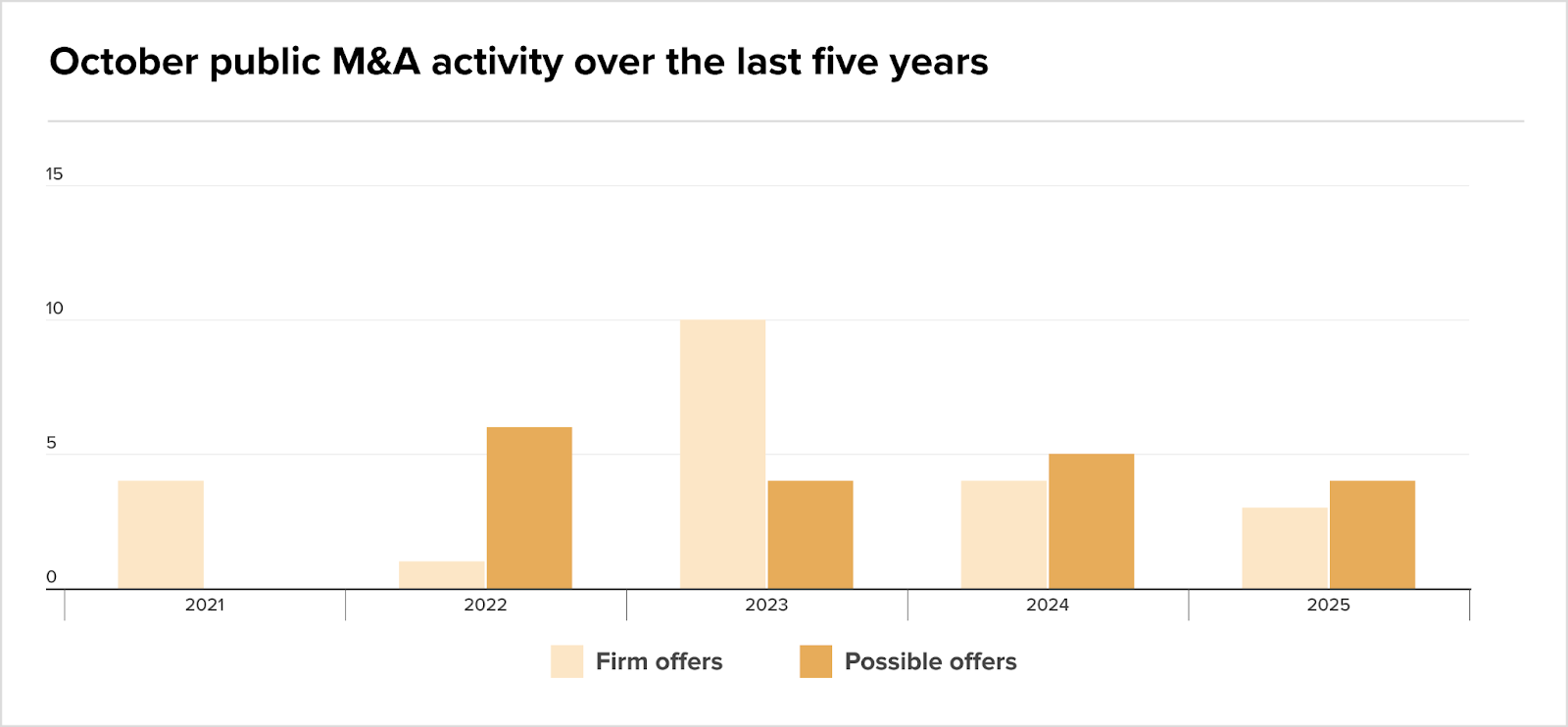

Public offers tick along in October

Turning the page to Q4, October’s public M&A landscape maintained a stable rhythm with three firm offers announced, marking activity levels broadly consistent with the same period in 2024.

What stands out is the continued dominance of strategic buyers, which drove two of the three firm offers during the month, extending a trend that has defined the second half of 2025 and represents a marked shift from the sponsor-heavy environment of October 2024.

Noteworthy transactions included Cicor Technologies’ £287m approach for TT Electronics and Long Path’s £339.5m public-to-private take of Idox, while the computer and electronic equipment sector emerged as the month’s hotspot with three separate approaches.

BDO tops Q3 advisory charts