Guten Tag,

die Transaktion der Woche markiert einen wichtigen Schritt im europäischen Private Banking: ABN Amro übernimmt die deutsche Privatbank Hauck Aufhäuser Lampe und integriert sie in ihre Frankfurter Tochter Bethmann Bank. Mit einem verwalteten Vermögen von € 70 Milliarden steigt ABN Amro zur drittgrößten Privatbank in Deutschland auf.

Im Industriesektor der DACH-Region steigen im 2. Quartal 2025 die Zahl und das Volumen industrieller Deals trotz geopolitischer Unsicherheiten. Laut Sabine Schilg, VP Customer Success bei Ideals, wollen Unternehmen unabhängiger vom US-Markt werden, indem sie sich geografisch breiter aufstellen, besonders durch Carve-Outs und strategische Beteiligungen.

Darüber hinaus gab es weitere wichtige Entwicklungen:

- Der Darmstädter Konzern Merck übernimmt Springworks Therapeutics für rund € 3 Milliarden und tätigt damit die größte Pharma-Transaktion des Unternehmens seit zwei Jahrzehnten.

- Die EU-Kommission genehmigte die Übernahme von About You durch Zalando. Somit entsteht ein starker europäischer Online-Modekonzern, der dem Druck chinesischer Plattformen wie Temu und Shein gezielt begegnen will.

- Die Horst Brandstätter Holding, Mutter von Playmobil, plant laut Medienberichten einen Teilverkauf. Grund ist ein Umsatzrückgang von 15,6 % im Jahr 2023 und ein Verlust von € 120 Millionen.

Vielen Dank fürs Lesen. Wenn Sie Interesse an einer Zusammenarbeit bei Ihrem nächsten M&A-Deal haben, freue ich mich über eine Kontaktaufnahme über LinkedIn.

Deal tracker

Deal der Woche

ABN Amro übernimmt Hauck Aufhäuser Lampe

Die niederländische Großbank ABN Amro hat die Übernahme der deutschen Privatbank Hauck Aufhäuser Lampe (HAL) erfolgreich abgeschlossen. Nach der Unterzeichnung und Ankündigung erfolgte die Umsetzung am 30. Juni 2025. HAL wird in die Frankfurter Tochter Bethmann Bank integriert und künftig unter dem Markennamen Bethmann HAL geführt.

Mit einem verwalteten Vermögen von rund € 70 Milliarden steigt ABN Amro zur drittgrößten Privatbank in Deutschland auf – hinter Deutsche Bank und Commerzbank. Für ABN Amro ist Deutschland nun der zweitgrößte Markt. Das Institut verfolgt ambitionierte Wachstumspläne: Bis 2030 soll das verwaltete Vermögen auf € 100 Milliarden anwachsen.

Der Deal unterstreicht die zunehmende Konsolidierung im Private-Banking-Markt, die durch den Wettbewerb um wohlhabende Kunden und das Streben nach stabilen Gebührenerträgen vorangetrieben wird.

White & Case beriet ABN Amro rechtlich bei der Transaktion, zeb unterstützte als Strategieberater mit Fokus auf das Asset-Servicing-Geschäft. Der Verkäufer Fosun ließ sich von Linklaters begleiten. Gleiss Lutz beriet das Management von Hauck Aufhäuser Lampe, insbesondere beim Carve-out des Asset Servicing.

Markttrends

Rückgang bei Startup-Investments verschärft Standortschwäche

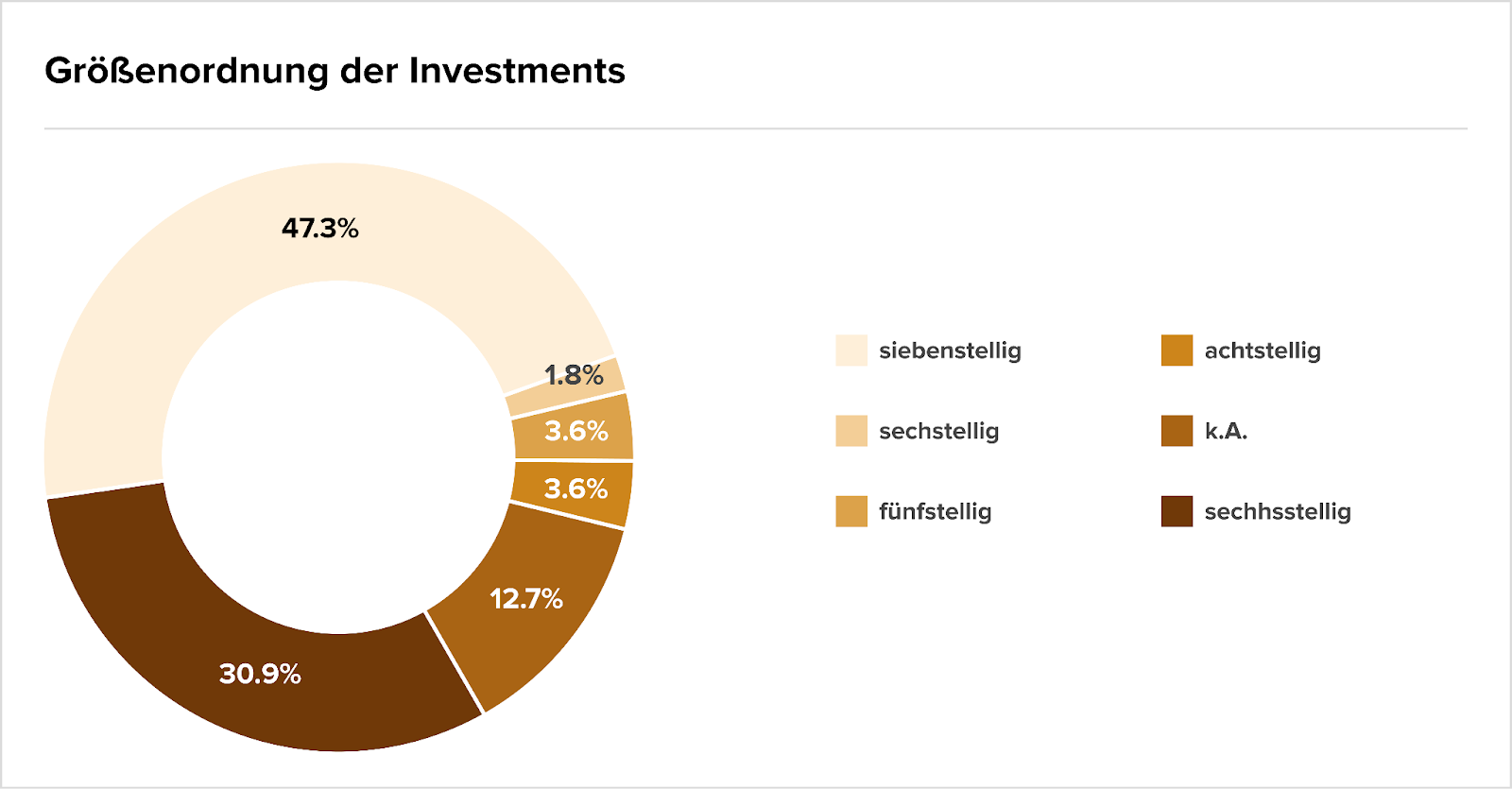

Ein genauer Blick auf das erste Halbjahr 2025 zeigt eine dramatische Entwicklung im Finanzierungsumfeld von Start-ups: Das Gesamtvolumen von Kapitalrunden in Österreich ist laut dem EY-Start-up-Barometer um 64 % auf nur noch € 110 Millionen eingebrochen. Während die Anzahl der Deals mit rund 70 nahezu stabil blieb, hat sich die durchschnittliche Höhe der Investitionen deutlich verringert.

Die beigefügte Grafik unterstreicht diesen Trend: Knapp die Hälfte aller Deals (47,3 %) lag im siebenstelligen Bereich, während Finanzierungsrunden im achtstelligen Bereich die Ausnahme blieben. Frühphasen-Start-ups, die sonst eine Stärke des österreichischen Ökosystems sind, wurden besonders hart getroffen.

Diese Entwicklung ist nicht nur ein Alarmsignal für den Innovationsstandort Österreich, sondern auch für die M&A-Pipeline im DACH-Raum. Kleine Investments, sinkende Bewertungen und zurückhaltende internationale Fonds lassen weniger Spielraum für skalierbare Geschäftsmodelle und verringern die Zahl potenzieller Targets für strategische Käufer.

Laut EY liegt das Problem nicht nur an der global fragilen Investitionsstimmung, sondern zunehmend auch an österreichspezifischen Faktoren wie regulatorischer Unsicherheit und mangelnden staatlichen Förderimpulsen. Eine Ausnahme bildet der KI-Sektor: 38 % des gesamten Kapitals flossen in KI-Start-ups – doch selbst dort sind die Finanzierungsrunden kleiner geworden.

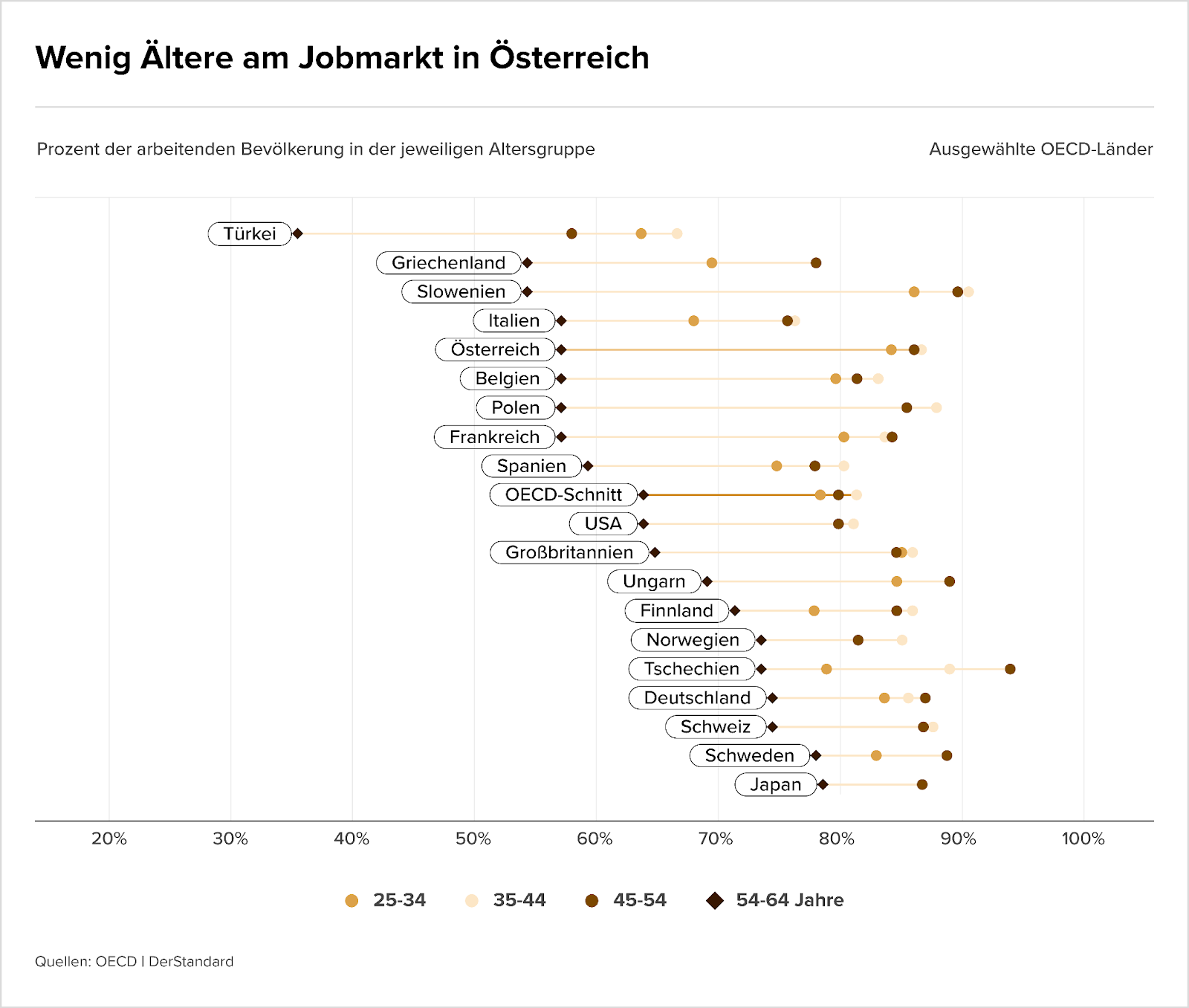

Ältere Menschen am Arbeitsmarkt bieten ein Potenzial mit Wachstumskraft

Die Erwerbsquote der 55- bis 64-Jährigen unterscheidet sich innerhalb der DACH-Region deutlich. Während Deutschland und insbesondere die Schweiz über dem OECD-Schnitt liegen, bildet Österreich eines der Schlusslichter. Eine Visualisierung der Tageszeitung Der Standard macht deutlich, dass in einer alternden Gesellschaft ungenutztes Beschäftigungspotenzial schlummert und dies vor allem vor dem Hintergrund des zunehmenden Fachkräftemangels von Bedeutung ist.

Für Investoren und M&A-Akteure ist diese Dynamik relevant. Unternehmen mit einer alternden Belegschaft sehen sich mit Fragen der Nachfolge, Produktivität und Know-how-Sicherung konfrontiert. Gleichzeitig können gezielte HR-Strategien und Maßnahmen zur Bindung erfahrener Mitarbeiter ein Wettbewerbsvorteil sein. Dies ist ein Aspekt, der bei Buy-and-Build-Strategien oder Commercial Due Diligence zunehmend Beachtung findet.

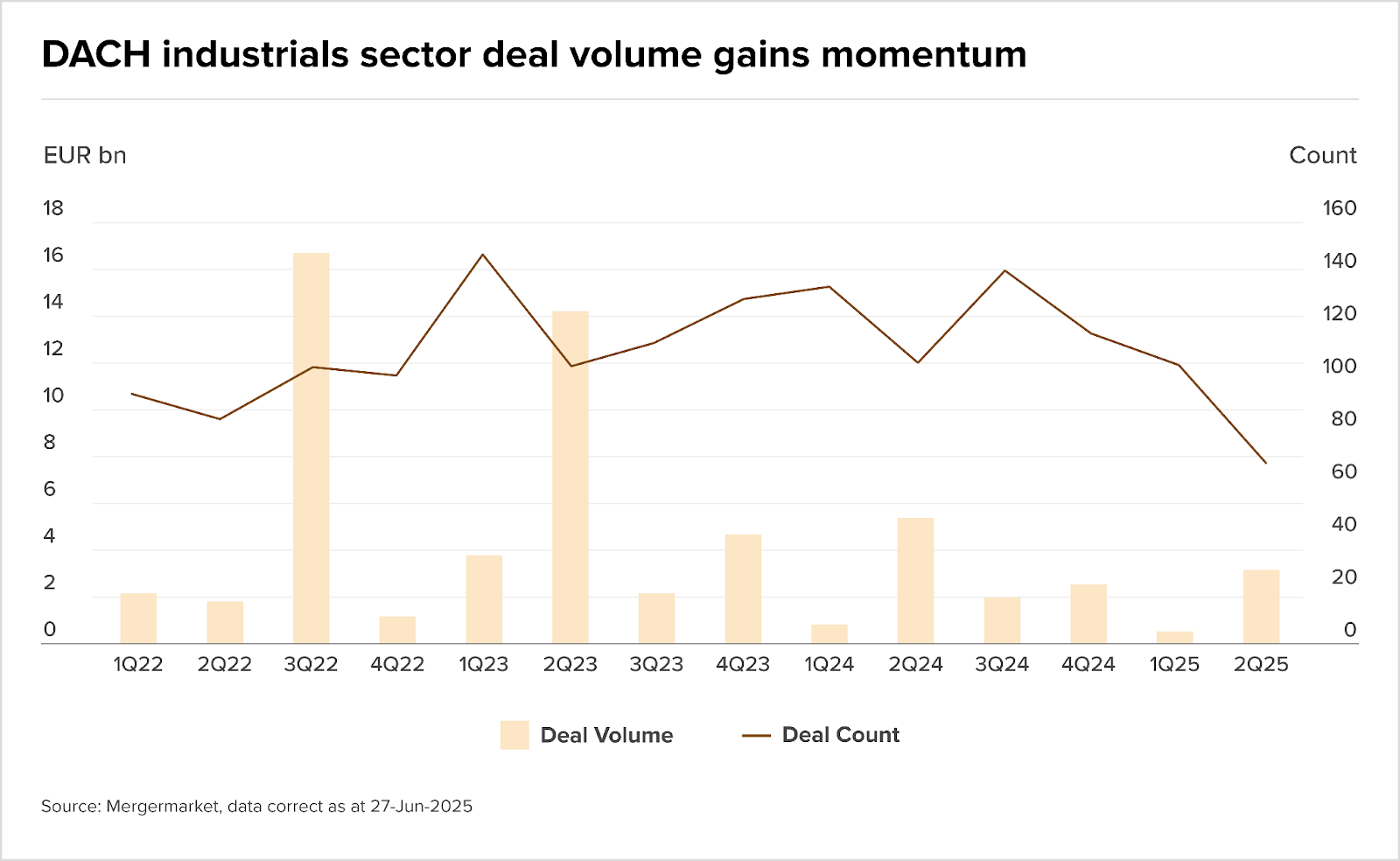

Industrials gewinnen an Attraktivität: Investoren setzen auf Sicherheit und strategische Standorte

Aufgrund geopolitischer Spannungen und wachsender Unsicherheiten auf den Weltmärkten stehen industrielle Assets in Deutschland, Österreich und der Schweiz zunehmend im Fokus von Investoren. Besonders gefragt sind Public-to-Private-Transaktionen und Carve-outs, um Lieferketten strategisch neu aufzustellen.

Der Chart aus einem aktuellen Artikel von Mergermarket zeigt: Mit 69 Deals im Wert von € 3,29 Milliarden wurde im zweiten Quartal 2025 das beste Ergebnis seit dem zweiten Quartal 2024 erzielt. Dies ist ein klares Zeichen für das neue Momentum im DACH-Industriesektor.

Sabine Schilg, VP Customer Success bei Ideals, beobachtet ebenfalls einen Strategiewechsel: Unternehmen hinterfragen zunehmend, wo sie künftig präsent sein müssen, um geopolitische Risiken abzufedern und sich weniger abhängig vom US-Markt zu machen. Neben klassischen Zukäufen gewinnen alternative Dealstrukturen wie Minderheitsbeteiligungen oder Joint Ventures an Bedeutung, vor allem für europäische Unternehmen, die auf dem US-Markt Fuß fassen wollen.

Der Anstieg an Auktionen und Exit-Aktivitäten, etwa durch Triton oder PINOVA, belegt zudem, dass der DACH-Markt ein attraktives Jagdrevier für PE-Investoren mit Fokus auf industrielle Resilienz bleibt.

Standards als unterschätzter Wachstumsmotor in Österreich

Eine neue Studie des Wirtschaftsforschungsinstituts GAW im Auftrag von Austrian Standards zeigt: Technische Normen sind nicht nur die Grundlage für Qualität und Kompatibilität, sondern auch ein messbarer Treiber des Wirtschaftswachstums.

Zwischen 2013 und 2023 trugen Standards jährlich rund € 1 Milliarde zum realen BIP-Wachstum bei, was einem Anteil von 20 % entspricht. Gleichzeitig führten standardisierte Prozesse zu einem Produktivitätszuwachs von 30 % und schufen 1.500 neue Vollzeitäquivalente.

Insbesondere kleine und mittlere Unternehmen profitieren davon. Durch die Anwendung internationaler Normen können sie schneller und kosteneffizienter auf Exportmärkten expandieren. Für strategische Investoren sind standardkonforme Unternehmen aufgrund ihrer Skalierbarkeit besonders attraktive Targets, da sie reibungslosere Integrationen, niedrigere Transaktionsrisiken und einen schnelleren Marktzugang ermöglichen.

Ein internationaler Vergleich zeigt zudem, dass der volkswirtschaftliche Effekt in Österreich ebenso stark ausfällt wie in Deutschland, Frankreich oder den nordischen Ländern und somit auch länderübergreifende Buy-and-Build-Strategien begünstigt.

Marktgerüchte

- Unicredit wirbt mit sechs konkreten Versprechen um die Übernahme der Commerzbank, darunter Investitionen und Standortgarantien. Die Bundesregierung lehnt jedoch jegliche Gespräche ab, solange kein detailliertes Konzept vorliegt.

- Verdi lehnt die Übernahme der Commerzbank durch Unicredit weiterhin ab – trotz umfassender Zusagen zum Erhalt von Filialen und Arbeitsplätzen. Gewerkschaftschef Frank Werneke äußert Zweifel an den Versprechen und warnt vor Risiken im aktuellen Marktumfeld.

- Die britische Frasers Group hat ihren Anteil an Hugo Boss auf 25 % erhöht und sich Optionen auf eine Mehrheitsübernahme gesichert. Der Großinvestor drängt auf umfassende Reformen und sitzt bereits im Aufsichtsrat.

- Revolut plant den Einstieg ins Private Banking in der Schweiz und sucht bereits nach entsprechenden Fachkräften. Noch handelt es sich um frühe Überlegungen – offiziell bestätigt ist nur die Prüfung der Machbarkeit.

- Ein Bericht enthüllt, dass das deutsche Gesundheitsministerium 2020 Masken im Wert von € 749 Millionen vom Startup Emix bezog – bei durchschnittlich 5,58 € pro Maske. Wegen Wuchers laufen in Zürich Ermittlungen.

- Mehrere geschädigte UBS-Kund:innen haben Strafanzeige wegen fragwürdiger Dollar-Derivate erstattet. Der Vorwurf: mangelnde Risikoaufklärung und intransparente Range-Produkte. Die Bank hat eine interne Taskforce gebildet, die Fälle intern prüft.

- Der Filmfinanzier und Banker Hans Syz wollte das Zurich Film Festival übernehmen, doch das Medienhaus NZZ verkaufte es überraschend an Festivaldirektor Christian Jungen und dessen Investorenkreis. Syz fühlt sich übergangen.

- Während ZEAM-Gründerin Yaël Meier auf LinkedIn Rekordwachstum feiert, melden Insider prekäre Arbeitsbedingungen: unbezahlte Workation-Flüge, 100 Fr. Laptop-Zuschuss, Praktika mit CHF 1.500-2.000 netto. ZEAM widerspricht teils – das Echo bleibt kritisch.

- Nach dem geplatzten Verkauf von Techem an TPG und GIC arbeitet Partners Group an einer neuen Deal-Struktur, eine Einigung erfolgt womöglich bald.

- Die Mutter von Playmobil, die Horst Brandstätter Holding, plant laut Manager Magazin einen Teilverkauf. 2023 sank der Umsatz um 15,6 % auf € 449 Millionen, der Verlust stieg auf € 120 Millionen. Eine Umstrukturierung der Stiftung soll Verkäufe erleichtern; auch Standortschließungen sind im Gespräch.

M&A-Nachrichten

- Die DFL und die Schwarz-Gruppe (Lidl, Kaufland) steigen beim Sport-Streamingdienst Dyn ein. Besonders Schwarz verfolgt mit dem Engagement strategische Ziele und will den Dienst in seine digitalen Angebote integrieren.

- Der Maschinenbauer Dürr verkauft seine Division „Clean Technology Systems” für rund € 385 Millionen an Stellex Capital Management. Dürr behält eine 25-prozentige Rückbeteiligung und will den Nettoerlös von ca. € 250 Millionen zur Schuldenreduzierung nutzen.

- Die EU-Kommission hat der Übernahme von About You durch Zalando zugestimmt. Damit entsteht ein dominanter Player im europäischen Online-Modehandel, der dem wachsenden Druck durch Temu und Shein trotzen will.

- Das Bundeskartellamt hat die Beteiligung der Lufthansa an Air Baltic trotz Bedenken genehmigt. Die Wettbewerbshüter warnen vor steigenden Preisen auf Verbindungen zwischen Deutschland und dem Baltikum.

- Die thailändische Central Group übernimmt das Carsch-Haus in Düsseldorf von der insolventen Signa-Gruppe. Damit zeichnet sich ein Ende des jahrelangen Baustopps und eine mögliche Rückkehr des Luxushandels in der Innenstadt ab.

- UM PanMedia gewinnt den Media-Etat des WienTourismus und übernimmt ab Juli die weltweite Mediaplanung für Wiens Vermarktung als Reisedestination. Die Wiener Agentur setzte sich in einer EU-weiten Ausschreibung durch.

- Change of Scandinavia übernimmt die insolvente Palmers Textil AG und sichert deren Fortbestand. Die Gläubiger erhalten gestaffelt 20 % ihrer Forderungen, der Sanierungsplan wurde umgesetzt.

- BNP Paribas übernimmt das Verwahrstellengeschäft von HSBC in Deutschland. Die französische Bank stärkt ihre Marktposition und wird mit einem Volumen von über 1 Billion Euro zur größten Verwahrstelle Deutschlands.

- Die Ypsilon Group hat sich mit der Hamburger Kanzlei GHP zusammengeschlossen und baut so ihre Präsenz im Norden sowie ihre Beratungskompetenz in der Transaktionsberatung und Wirtschaftsprüfung aus. Das Team wächst auf über 210 Mitarbeitende.

- Ein weiterer PE-Investor steigt in den deutschen Wirtschaftsprüfermarkt ein. Der Deal ist klein, zeigt aber den anhaltenden Strukturwandel in der Branche – getrieben von Digitalisierung, Nachfolgeproblemen und wachsender Nachfrage nach Advisory-Services.

Gehälter & Boni

- Eine neue Saläranalyse zeigt: Spartenleiter verdienen in der Schweiz aktuell am meisten – mit bis zu CHF 317.000 Jahresgehalt. Die Studie basiert auf über 20.000 Positionen und gibt Orientierung für Führungskräfte auf allen Ebenen.

- Einstiegslöhne in der Schweiz variieren stark: Während Big-Tech-Talente bis zu CHF 180.000 verdienen, liegt der Medianlohn deutlich darunter bei 84.500 Franken. Besonders Informatik-Absolventen profitieren vom Tech-Boom.

Personalien

- Die BLKB schreibt über 100 Millionen Franken auf ihre Neobank-Tochter Radicant ab. Infolge des Debakels treten CEO John Häfelfinger und Bankratspräsident Thomas Schneider zurück – eine in der Schweizer Finanzwelt seltene Doppeldemission.

- UBS startet ein neues Aktienrückkaufprogramm über bis zu US$ 2 Milliarden. Trotz regulatorischer Debatten hält die Großbank an ihrer Strategie zur Kapitalrückführung fest und plant weiterhin eine Dividendensteigerung.

- Schiefer Rechtsanwälte holt mit Christian Richter-Schöller einen führenden ESG- und Transformationsexperten ins Führungsteam und etabliert ein neues Kompetenzzentrum für resiliente Lieferketten und nachhaltige Finanzierung.

- IP Österreich firmiert ab sofort unter RTL AdAlliance und vollzieht damit die vollständige Integration in die internationale Vermarktungsstruktur der RTL Group. Elisabeth Frank übernimmt ab 2026 die Geschäftsführung von Walter Zinggl.

- Sarah Huber übernimmt ab Sommer die Geschäftsführung von Nestlé Österreich von Cédric Boehm, der künftig als Generaldirektor Nestlé Schweiz führen wird.

- Nach weniger als zwei Jahren verlässt Carina Kozole die Digitalbank N26. Ihr Nachfolger als Chief Risk Officer wird Jochen Klöpper, zuvor CRO bei der Santander Consumer Bank.

- Thomas Althaus wird neuer Chief Risk Officer und GL-Mitglied der Migros Bank. Dort soll er die Risikokultur stärken, trotz seiner Erfahrung im gescheiterten CS-Risikosystem.

- Die BayernLB besetzt die Nachfolge des ehemaligen CFO und COO Markus Wiegelmann mit einem IT-Manager von Unicredit. Die Finanzverantwortung verbleibt vorerst beim CEO.

Kapitalrunden

- Trotz Krise und Stellenabbau sammelt das Zürcher ETH-Spin-off Climeworks US$ 162 Millionen ein. Die CO₂-Entnahmetechnologie bleibt teuer und wenig effizient, doch Investoren halten an der Klimavision fest.

- Das auf Quantenkryptografie spezialisierte Wiener Startup Zerothird hat eine Seed-Finanzierung über US$ 10 Millionen erhalten. Zu den Investoren zählen Sparring Capital Partners, Findus Ventures und KGAL.

- Die B&C-Gruppe plant, über ihre Tochter BCII in den nächsten fünf Jahren € 300 Millionen in österreichische Industrie- und Tech-Scale-ups zu investieren. Der Fokus liegt dabei auf den Bereichen Cleantech, Automatisierung und industrielle Software.

- Das in London ansässige Windel-Start-up Peachies, dessen Co-Founderin Rima Suppan aus Niederösterreich stammt, hat eine Finanzierungsrunde über € 2,5 Millionen abgeschlossen. Die Lead-Investoren sind ArmaVir Partners (New York) und Triple B (Amsterdam).

- Das Linzer Deeptech-Start-up Tributech sichert sich € 1 Million in einer Bridge-Finanzierung. Neben bestehenden Investoren beteiligen sich neue Geldgeber wie Angels United, Werner Lanthaler und Christoph La Garde.

- Das Münchner EdTech-Start-up Edurino hat in einer Series-B-Finanzierungsrunde € 17 Millionen erhalten. Neu dabei sind Ravensburger Next Ventures und Summiteer, während bestehende Investoren wie DN Capital und Tengelmann Ventures ihre Beteiligungen ausbauten.

- Das Berliner B2B-Gebrauchtwagen-Startup CarOnSale hat € 70 Millionen in einer Series-C-Finanzierungsrunde erhalten. Lead-Investoren sind Northzone und HV Capital, beteiligt sind u. a. Insight Partners, Stripes, Creandum und Ex-Daimler-Chef Dieter Zetsche.

- Lieferando-Co-Founder Christoph Gerber hat für sein neues Startup Talon One € 115 Millionen eingesammelt. Das LoyaltyTech-Unternehmen zählt bereits Adidas und H&M zu seinen Kunden und positioniert sich als Alternative zu Salesforce.

- Das in München und Nürnberg ansässige Energie-KI-Startup Avoltra hat € 2,3 Millionen in einer Pre-Seed-Runde eingesammelt. Angeführt wurde die Runde von Project A; auch der neue CDTM Venture Fund ist beteiligt.

Börsengänge

- Die Swiss Marketplace Group (u. a. Ricardo, Homegate, Autoscout24) erwartet 2025 ein Umsatzwachstum von bis zu 15 % und plant laut Medienberichten möglicherweise einen Börsengang noch in diesem Jahr.

- Aebi Schmidt ist nach einer Fusion mit der US-Firma The Shyft Group an der Nasdaq gelistet. Der Schweizer Fahrzeugbauer wird damit zum weltweit führenden Anbieter von Spezialfahrzeugen.

- Am 23. Juni 2025 ging das abgespaltene US-Geschäft von Holcim unter dem Namen Amrize an die Börsen in Zürich und New York. Mit einem Börsenwert von rund CHF 22 Milliarden ist Amrize neu im SMI gelistet.

- Der Börsengang von Reploid im Direct Market Plus der Wiener Börse ist vollzogen. Zunächst gab es zwar keine Trades, laut dem Gründer war die Nachfrage jedoch hoch. Ein IPO mit Kapitalerhöhung über € 50 Millionen ist für die kommenden Monate geplant.

Hello,

This week we’re seeing AI, disinvestment, and consolidation define India’s capital moment.

Case in point: Capgemini’s $3.3 billion acquisition of WNS, a definitive sign that generative and agentic AI are becoming boardroom priorities (we explore this in detail under the Market Trends section).

Meanwhile, in public markets, Jio BlackRock’s $2.1 billion fund debut hints at a brewing price war in India’s asset management business, making fund fees, not just fund performance, a competitive moat.

Together, these moves suggest India’s capital flows are shifting decisively from growth capital to control plays, from VC gloss to strategic scale.

In healthcare, Temasek-backed Manipal Hospitals has acquired a majority stake in Maharashtra-based Sahyadri Hospitals, continuing the consolidation wave in the sector.

And finally, Asian Paints’ full exit from rival Akzo Nobel India suggests a broader trend: listed firms are cleaning up balance sheets and doubling down on core strengths.

Across the board, strategic exits, institutional scale-ups, and public–private crossovers are giving India’s capital ecosystem a quieter, but firmer, shape.

I hope you enjoy this week’s roundup, and please do connect with me on LinkedIn to find out how I can help with your next M&A deal.

Let’s dive in.

How AI agents are reshaping M&A

Artificial intelligence (AI) agents have huge potential to make deal processes faster and more efficient. But how do you separate the tangible use cases from the marketing hype?

On July 16, we’re hosting a webinar with Ideals and Comparables.AI to look at how dealmakers are using AI to gain a competitive advantage and how these use cases will develop in 2026.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

No small change

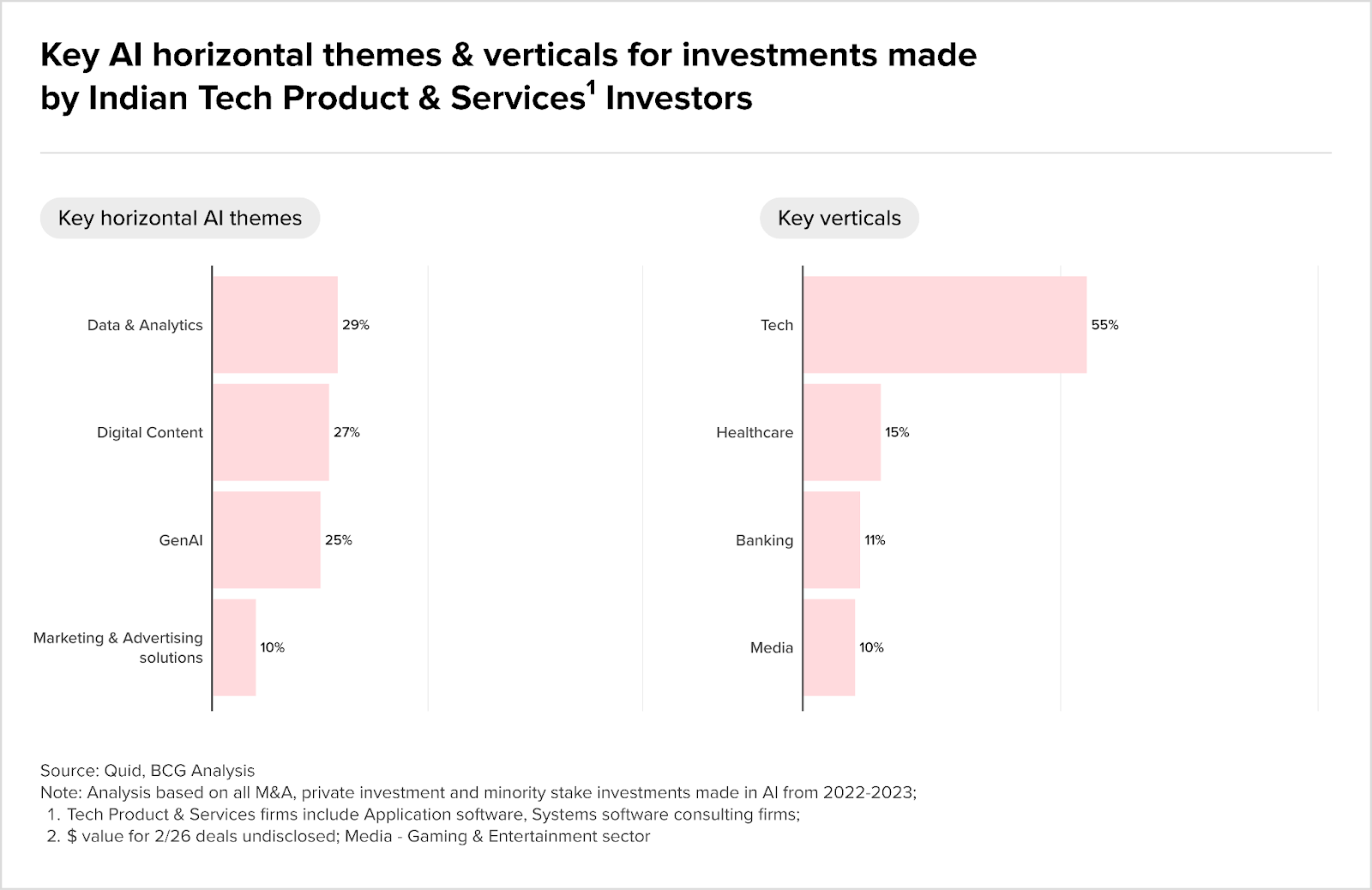

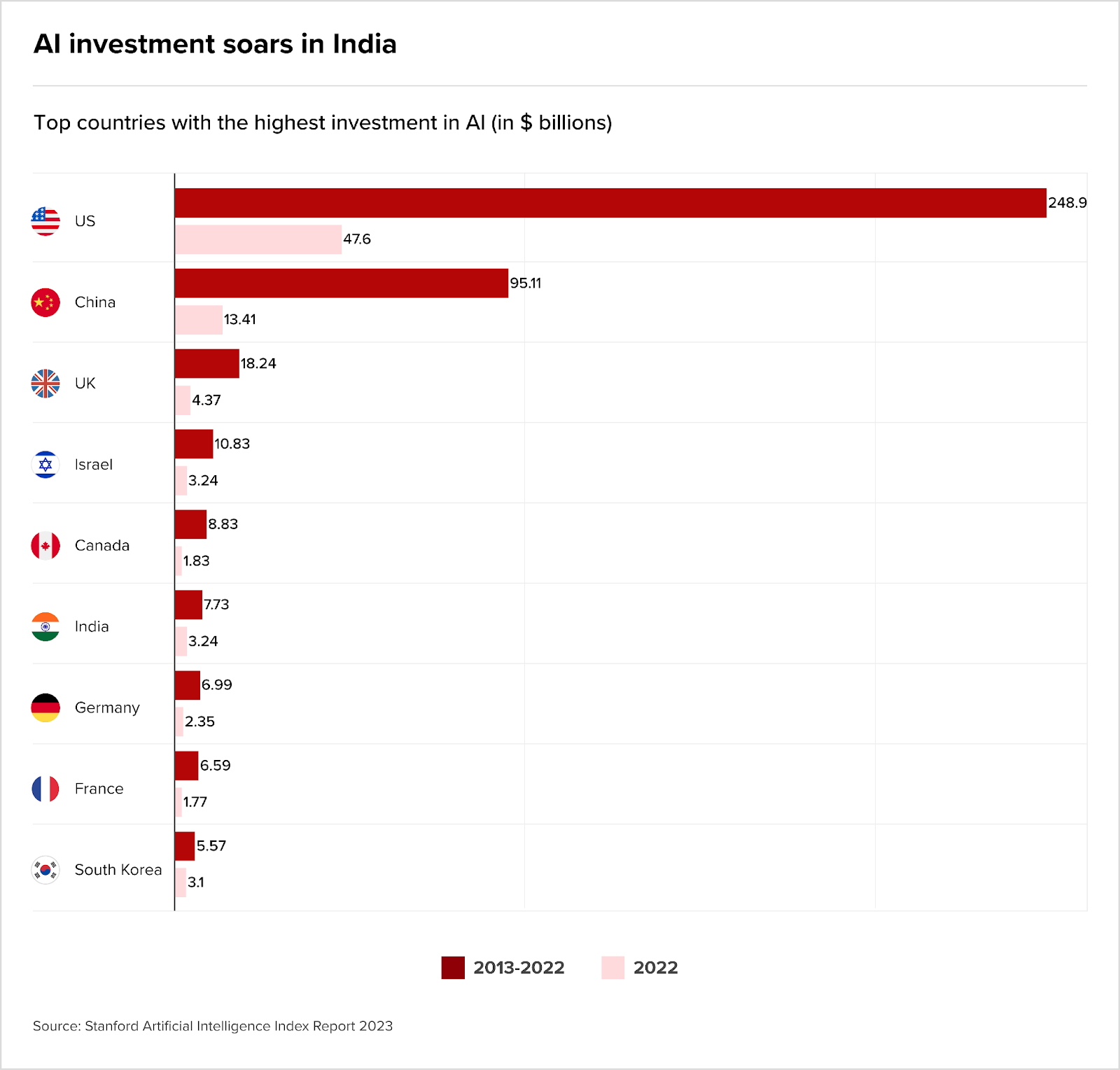

India’s AI sector may no longer be underestimated as a sunrise sector, though in terms of compute power the country is still a minnow.

Deal activity in the last 18 months indicates a course quite different from the typical startup trajectory in other sectors. AI is an investment thesis for serious, strategic capital, a high-conviction play that global funds are beginning to treat with the same seriousness they once reserved for oil, telecom, and semiconductors.

Look at the big-ticket consolidation, infrastructure build-outs, and industrial alignment taking place. It is BIG money in motion as recent deals and MoUs indicate.

The image below tells us where the smart corporates are putting their cash, prioritising AI capabilities across verticals like healthcare and banking, and placing bets across data and analytics with GenAI not far behind.

Indeed, sovereign-aligned funds and pension capital are circling the foundational layers of India’s AI stack:

- NIIF, Digital Edge & AGP have partnered to build a $2 billion hyperscale data centre in Navi Mumbai (Bombay), part of a pan-India strategy

- Last year, Singapore’s ASMPT and Tata Electronics signed an MoU for high-end semicon equipment, strengthening the chip ecosystem under the India Semiconductor Mission, a domestic policy effort.

- HCL and Foxconn’s JV, with $445 million in government support, will set up an OSAT (outsourced semiconductor assembly and test) in Delhi NCR.

- Large industrial house L&T Semiconductor’s MoU with C‑DAC (Centre for Development of Advanced Computing, an Indian government concern) aims to commercialise homegrown VEGA processors, linking public R&D with private industrial scale-up.

Consolidation overtakes innovation

In a business process outsourcing (BPO) reset, AI-led platform consolidation is now overtaking incremental innovation in those services: just this week, French consultancy Capgemini acquired Indian BPO WNS for $3.3 billion, a move that signals that agentic AI is more than a buzzword and will become core to BPM (business process management) strategy.

To push the assertion further, there is Japanese SoftBank, long associated with tech VC, exploring direct buyouts in AI-led BPO and IT services, indicating a pivot toward modernising India’s legacy outsourcing stack.

High-value hardware and semicon facilities are now AI enablers, and crucial compute assets seem to be emerging.

For instance, India-US Shakti fab, a joint initiative between Bharat Semi and the US Space Force, aims to produce power electronics, photonics (a branch of optics that involves the manipulation of light), and sensor materials.

Tata Semiconductor’s $3.6 billion greenfield facility in Assam, a state in eastern India, will be the country’s first domestic chip assembly and test plant.

India joins global AI league (almost)

The country now ranks fifth globally in AI startup funding, with $3.24 billion raised in 2022, signalling that international capital views the country as more than a back office, it’s a growing hub of scalable, strategic AI investment.

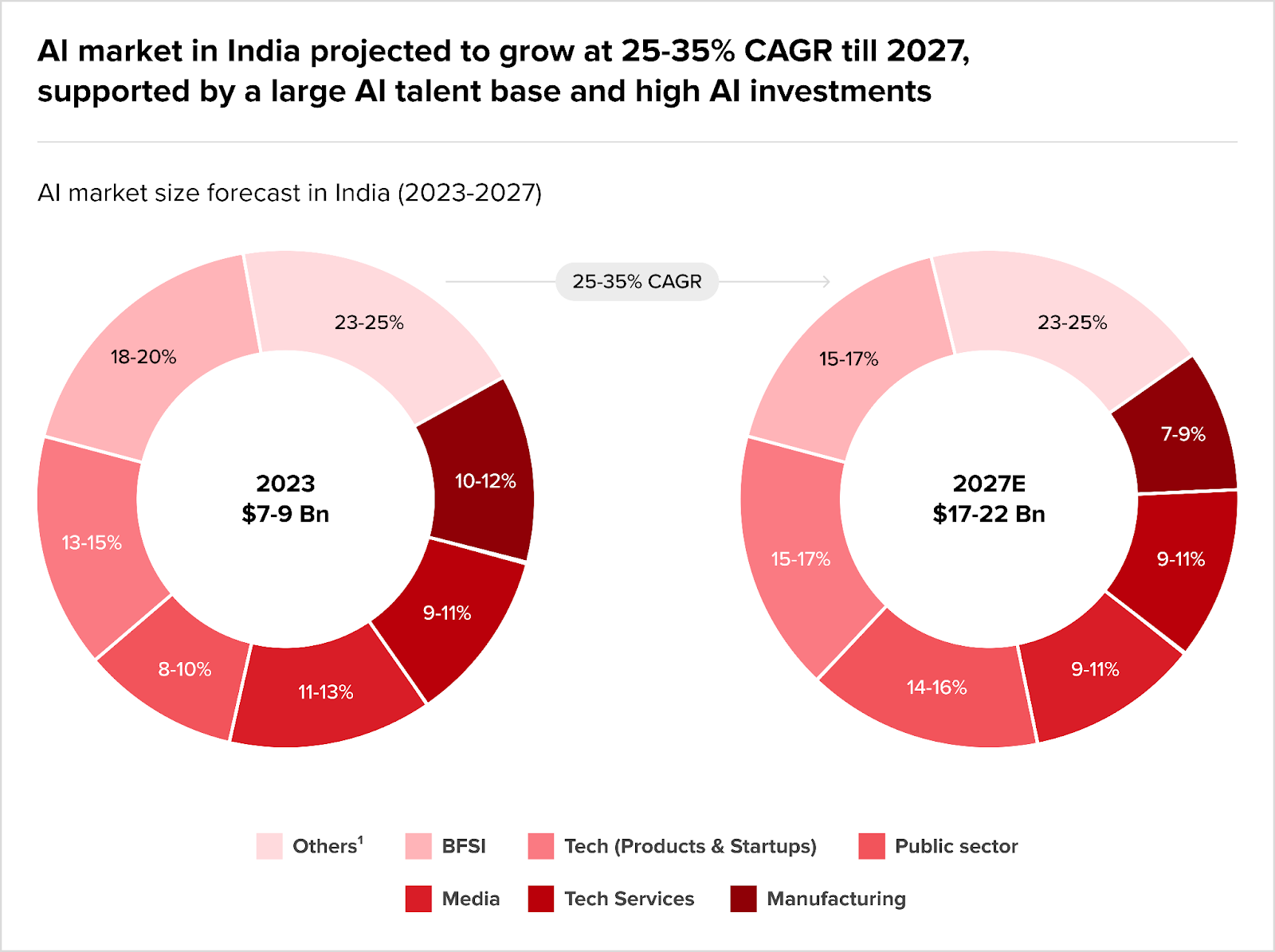

Market growth, capital depth

The Indian AI market is projected to reach $17 billion by 2027, growing at 25-35% CAGR in both corporate spending and talent. This structural growth is precisely the traction institutional investors seek.

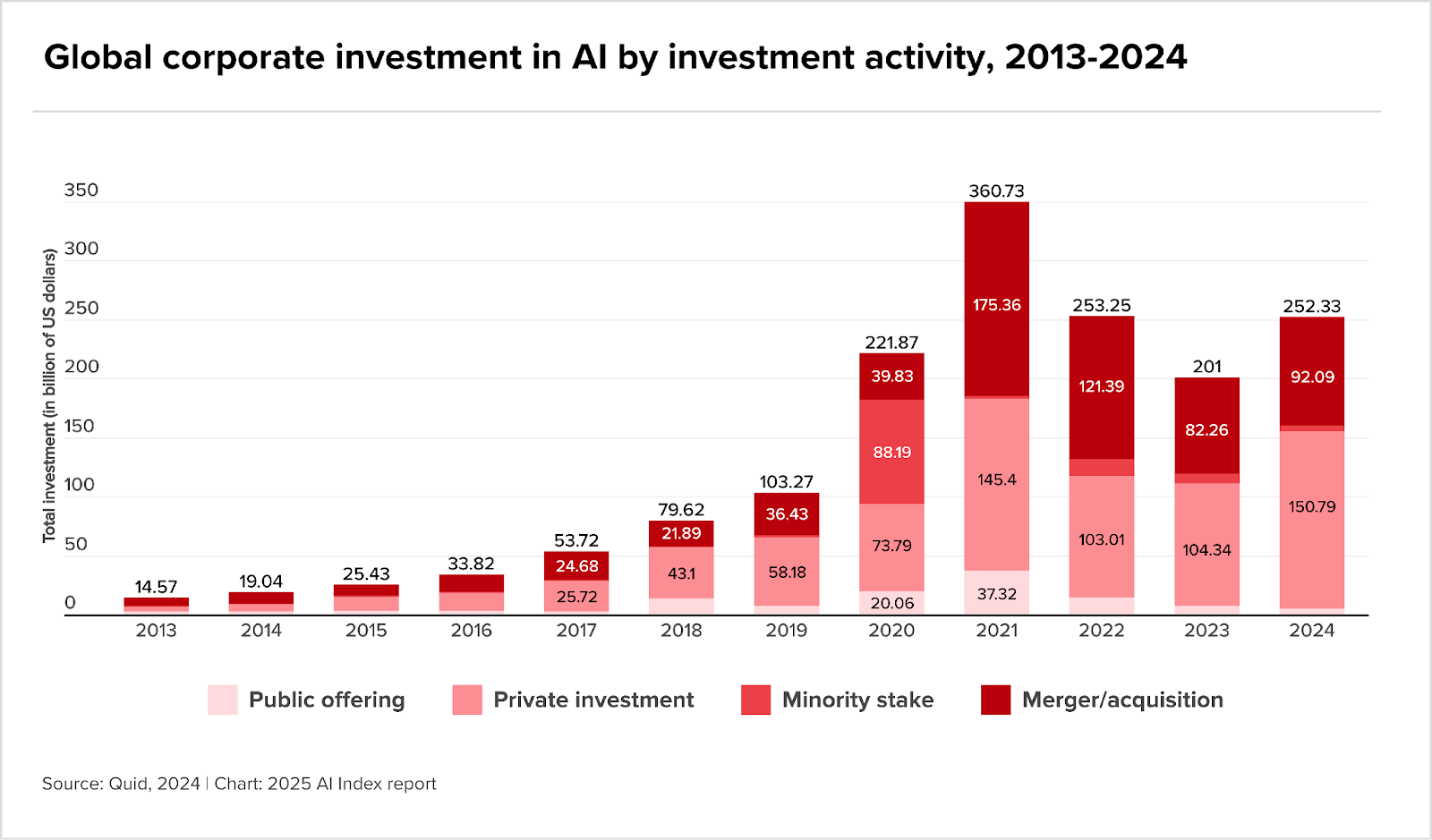

Global AI investment stood at $252 billion in 2024, with $33.9 billion in generative AI alone, suggesting the capital intensity of the sector. AI is now a high-stakes, billion-dollar bet – one increasingly mirrored in India’s M&A landscape.

With sovereign funds, global strategics, and long-term institutional capital in play, this is a moment of infrastructure-building, not ideation, as the country’s tech outgrows the startup narrative. The many deals mentioned above reflect this, and more importantly it seems, big money demands it.

The rumour mill

- Credit Wise Capital to raise Rs 200 crore through share sale

- Defence Acquisition Council clears 10 capital acquisition proposals worth over Rs 1.05 lakh cr

- SoftBank eyeing buyout deals in India to push AI-led IT, BPO operations

- Hamilton Lane launches Asia-focused evergreen fund

- Barclays announces key leadership appointments in Asia Pacific Investment Banking

- Anil Ambani’s Reliance Media Works to face insolvency proceedings

- Aakash sends legal notice to EY alleging conflict of interest, professional misconduct

- Base Corporation up for sale ‘again’ at reserve price of Rs 67.57 crore

- IBC needs urgent reform: Monsoon session may clear clouds of confusion

- India M&A Deal Value Plunges 48% in Q2

- Fewer Investors Than Expected Jumping On Steel Authority of India Limited (NSE:SAIL)

- Data settles the debate: IIT Delhi leads in both unicorn numbers and startup jobs

- FATF Endorses India’s Institutional Mechanisms like JAM in Latest Norms

- Fertilizer stock jumps 5% after receiving CCL approval to acquire 53% of stake worth ₹820 Cr in NACL

- BlackRock’s India Joint Venture to Launch Dozens of New Funds

- IBBI’s recent CIRP reforms: Analysis of India’s evolving corporate insolvency regime

- Brookfield PE arm sells stakes to fund for wealthy

- 3G Capital, Singapore’s GIC seek CCI nod to acquire Skechers

- Capgemini acquires WNS for $3.3bn cash deal to expand agentic AI

- CCI approves 360 ONE’s acquisition of select UBS AG businesses in India

- IDBI Bank divestment: Govt panel likely to finalise draft SPA today, sources say

- Asian Paints sells entire stake in rival Akzo Nobel India

- Carlyle looking to sell up to 10% stake in India’s Piramal Pharma

- IFC mulls up to $60m investment in AEW -Natixis’ $500m green infra fund

- For India’s young and rich, private markets are the new happy hunting grounds

- Falling rupee stirs debate over local v foreign capital in India’s private mkts

- Fundraise after 1st-ever stock split: Shares hit 52-week high ahead of board meeting; check schedule here

- Foreign Investors’ are betting big on India. Just not the stock market

- CII sees 6.7% growth in FY26, pitches for reforms, disinvestment, FTA leverage

- India attracts FDI but fails to retain it

- Hinjewadi’s IT workforce and villagers divided on merger with PCMC

- Can the RBI governor’s tie colour predict rate moves? What SBI report says

- From Cross-Border M&A to Catalyzing Growth in India’s Mid-Market: A Conversation with Mahesh Parasuraman, Partner & Co-founder, Amicus Capital

- 15 Successful Spin-Off Companies and Their 2025 Returns

- Cross Border Mergers And Acquisitions: An Analysis

- GCF approves $200 million for ADB India clean energy program

- ILJIN Electronics forays into BESS, buys majority stake in Power One

- Govt defers divestment of former Air India subsidiaries amid regulatory hurdles, weak investor sentiment

- India defence panel starts process to buy arms worth $12.3 billion

- Jio BlackRock to disrupt India’s funds sector with low-cost strategy: sources

- Declining private equity dry powder; Asia-Pacific deal value on the rise

- TAM to maintain BARC JV Role, sets sights on Big Tech and DPO alliances

- Ares Asia taps key LP for new special situations fund with India mandate

M&A news

- Modi-Milei talks explore ventures in critical minerals, shale, defence

- ONGC picks Mitsui O.S.K. Lines as JV partner for owning two very large ethane carriers

- Insolvency regulator amends rules to enhance disclosure on avoidance transactions

- NCLT initiates insolvency proceedings against Gstaad Hotels over Rs 666 crore default

- OPINION | Reform with Restraint: India’s Legal Strategy Strikes Global Balance

- Private capex is on the rise: CII President Rajiv Memani

- Indian Billionaire Mukesh Ambani’s 50-50 Joint Venture With Larry Fink’s BlackRock Raises $2.1 Billion In Debut Fund Offering

- India warming to larger private credit deals, Cerberus says

- India’s Q2 Deal Activity Falls 48%, But Resilience Emerges

- JSW And Renault In Talks To Build Cars In India: New Details

- India plans BSNL revival, Vi aid to enhance telecom competition

- Indian dairy startup Country Deligh said to be in talks with GIC, TPG

- Interview: Real estate fund manager Hines sees Asia as next growth engine, driven by India

- Mutual fund manager ICICI Prudntial Asset file $1.2b India IPO

- Indian e-commerce platform Meesho confidentially files for $497m IPO

- Leapfrog, Kedaara in talks to pick majority in India’s Surya Hospitals

- Peak XV’s second act: From record returns to a reinvention around AI

- Interview: Quadria Capital marks strategic shift with majority stakes, deeper involvement

- India’s Reliance Jio to postpone planned 2025 IPO

- Pan-Asian funds reshaping SE Asia’s PE landscape says LP GreenBear

- Institutional investors shore up Travel Food Services’ $234m IPO

- India’s TVS Capital targets higher stakes, larger cheques from Fund IV

- PE giants circle Axis finance in potential $1 billion deal

- Jane Street Banned in India Highlights: Strategies, profits and other details of Jane Street’s alleged manipulation

- Mahindra Holidays shares to be in focus on Friday after acquiring 100% stake in Finland-based real estate firm

- Metropolitan Stock Exchange to raise ₹1,000 crore from Peak XV, Jainam Broking, others

- PSU banks disinvestment moves ahead, govt panel to appoint advisers today

- Narayana Murthy’s Catamaran eyes Amazon-like joint ventures in precision manufacturing

- India’s M&A, PE Deal Value Slumps 48% To $17 Billion In April-June On Global Headwinds

- India’s M&A deals rise 3.3% in H1CY25

- OBIT: ‘Merger magician’ Susim Mukul Datta

- LevelBlue to Acquire Trustwave, Becoming Largest Pure-Play Managed Security Services Provider

- Inflation likely to align with RBI’s projection in Q1: BoB report

- Local investors overtake offshore peers in LP money flow into Indian PE, credit funds

- PE-backed Kanakadurga Finance’s fundraising plan gathers pace, eyes bigger cheque

Job moves

IPOs

- Renault in talks with JSW for India partnership as Nissan ties unwind: Report

- S&P Global Services PMI Signals a Goldilocks Economy: Navigating Rate Risks and Sector Shifts

- Sapphire Foods India shares rise over 10% on reports of merger with Devyani International

- Reliance Spins Off Consumer Business as Direct Subsidiary Amid Retail IPO Buzz

- Restaurant India News: Rebel Foods Shuts Offices, Weighs Exit from Smoor Amid Restructuring

Fundraising

Compliance/regulatory update

- Ukraine war, sanctions cast shadow on Indo-Russian joint venture

- TATA AutoComp, Skoda Group set up JV to manufacture railway components in India

- With 8.05% interest rate, the RBI Floating Rate Savings Bond is the best hope for conservative investors

- The Strategic Divide: How Reliance’s FMCG Spinoff Could Reshape India’s Consumer Landscape

- Temasek-backed Manipal Hospitals to buy majority stake in Sahyadri hospitals

- TR Capital prioritises asset quality, market nuances in India investment strategy

- Torrent Pharma to Buy Additional 2.41% Stake in JB Chemicals for ₹620 Crore

- The world’s top two PE firms are scouting for secondary portfolio deals

- Telecom triumphs in infrastructure deals

- Yum Brands in talks to facilitate merger of its two Indian partners, ET reports

- Tata Capital names co-head for sector agnostic PE fund

Hello,

It looks like private equity’s annual bun fight over new recruits could be a thing of the past. After JP Morgan said it would fire junior bankers who had lined up a future role through PE’s ‘on-cycle’ recruitment process, Goldman Sachs has started demanding loyalty oaths every three months.

Coincidentally, it comes in the same week that Goldman welcomed back an ex-employee who left to join a hedge fund after only a few years as a junior analyst. However, Rishi Sunak’s advisory role with the firm will be limited so as not to conflict with his recent stint as PM.

And in other news:

- Athora is nearing a £6bn takeover of pension insurer PIC

- Octopus Energy plans to demerge tech arm Kraken

- Q2 dealmaking crashed to its lowest level in a decade

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Dealmaker spotlight

Nitya Srivastava, an Engagement Manager at EY-Parthenon, was kind enough to share insights from her career this week.

She discussed her path into private equity advisory, the power of networking, and how technology adoption is accelerating value creation.

Read the article to find out more, and get in touch if you’d like to be profiled in our newsletter.

How AI agents are reshaping M&A

Artificial intelligence (AI) agents have huge potential to make deal processes faster and more efficient. But how do you separate the tangible use cases from the marketing hype?

On July 16, we’re hosting a webinar with Ideals and Comparables.AI to look at how dealmakers are using AI to gain a competitive advantage and how these use cases will develop in 2026.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

Industry news

- Britain’s blue chip index hits record high

- Bank of England sees ongoing financial stability risks from global tensions

- Neil Woodford: UK stock market is ‘dying before our eyes’

- Global 3C warming would hurt UK economy much more than previously predicted, OBR says

- UK shares mixed as investors assess fiscal worries, rate cut path

- UK faces ‘daunting’ risks to public finances, OBR warns

- UK insurance distribution M&A has ‘slowest half year’ since H1 2019 – MarshBerry

- Most UK companies would withstand sharply higher tariffs, BoE says

- UK officials hopeful steel industry will avoid 50% US tariff

- Forcing pension funds to buy UK assets is ‘form of capital control’, says Lloyds boss

- JPMorgan-owned Nutmeg posts £40m loss

- Schroder family is facing defining moment for City Dynasty

The rumour mill

- Banks start pitching $4.25bn in debt for Boots buyout

- Blackstone bumps bid for Warehouse REIT after Tritax offer

- Too big too fast: how $10bn UK energy challenger Prax unravelled

- Apollo-backed Athora nears £6bn takeover of UK pension insurer PIC

- UK BNPL fintech Zilch reportedly searching for overseas acquisition opportunities

- Jupiter strikes £100m deal to acquire CCLA

- UK homebuilders are hit with £100m bill after antitrust probe

- Pretium walks away from UK residential deal talks for Sigma

- Masdar strikes €5.2bn UK offshore wind deal with Iberdrola

- Thames Water dismisses last-minute rescue backed by ex-Lib Dem peer

- Triton to acquire Prenax

- Wood Group accounts flagged by watchdog as far back as 2017

- UK set to hold minority stake in Sizewell C nuclear project

- Octopus Energy plans to demerge tech arm Kraken

- US-based distributor agrees to acquire $1.3bn GWP Lloyd’s insurer

- Merck strikes $10bn deal for respiratory drugmaker Verona

- Grant Thornton US and UK compete for German sister firm

- DPI to invest $190m in Egyptian private healthcare group Alameda Healthcare

- Rhône in talks to acquire Direct Healthcare Group and Invacare

- BGF pumps capital into UK’s Rapidrop Global

- Santévet Group is to buy stake in Tedaisy

Job moves

- Goldman asks analysts to swear they haven’t lined up private equity jobs

- UBS names new US ECM head in leadership reshuffle

- Citigroup bolsters European leveraged finance with Deutsche Bank hire

- Deutsche Numis eyes office switch for all staff by 2026

- Morgan Stanley names Esteve head of equity syndicate in Europe

- Man Group announces leadership shake-up across discretionary

- BP bolsters board with former Shell executive Simon Henry

- Napier AI appoints Kenneth Paqvalén as CFO

- WPP hires Microsoft executive Cindy Rose as new chief

- Perwyn makes Partner promotions

- PPRO appoints Michelle Eischeid as new CFO

- Barclays’ recent cuts included a man who made MD in 2022

Market trends

Dealmaking has worst Q2 in a decade

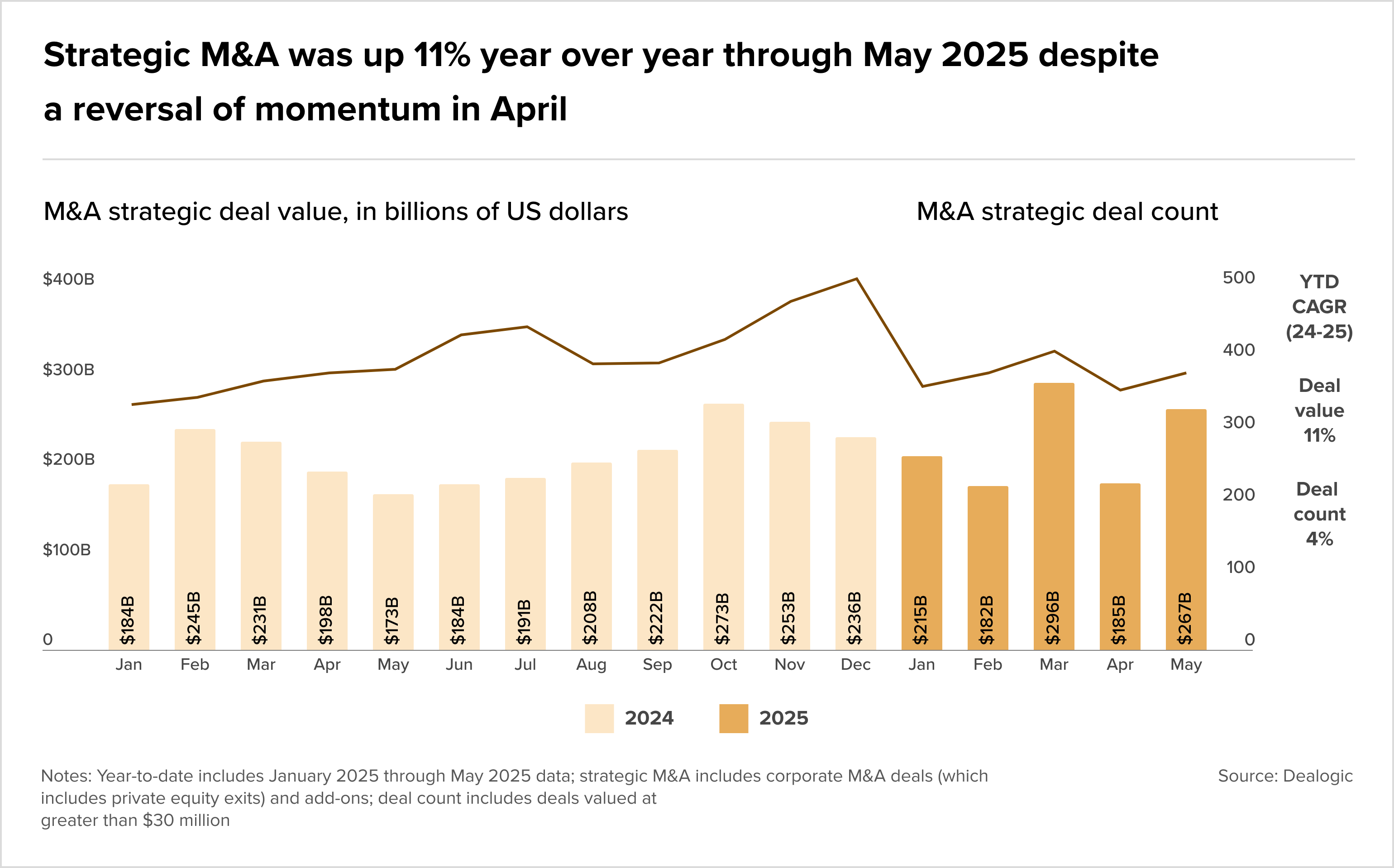

It feels like the M&A market is experiencing a bit of an identity crisis. Bain’s midyear report shows strategic dealmakers strutting about with 11% YoY growth through May, bouncing back from April’s tariff tantrum. The deal count marched upward from 182 in January to 267 in May, proving that some execs have mastered the art of turning chaos into strategic opportunity.

But zoom out to the overall picture, and the Financial Times tells us a completely different story. Q2 dealmaking crashed to its lowest level in a decade (excluding the early months of the pandemic) with just 10,900 deals announced. PE shops have gone particularly quiet, with deals plummeting from 2,500 in Q1 to 1,850 in Q2.

The split is telling: Strategic buyers are plowing ahead with transformative moves and snapping up AI assets like Salesforce’s $8bn Informatica pursuit, even as the broader market has hit pause with pent up demand being held back by an uncertain outlook for growth and inflation.

European GPs happy to store up dry powder

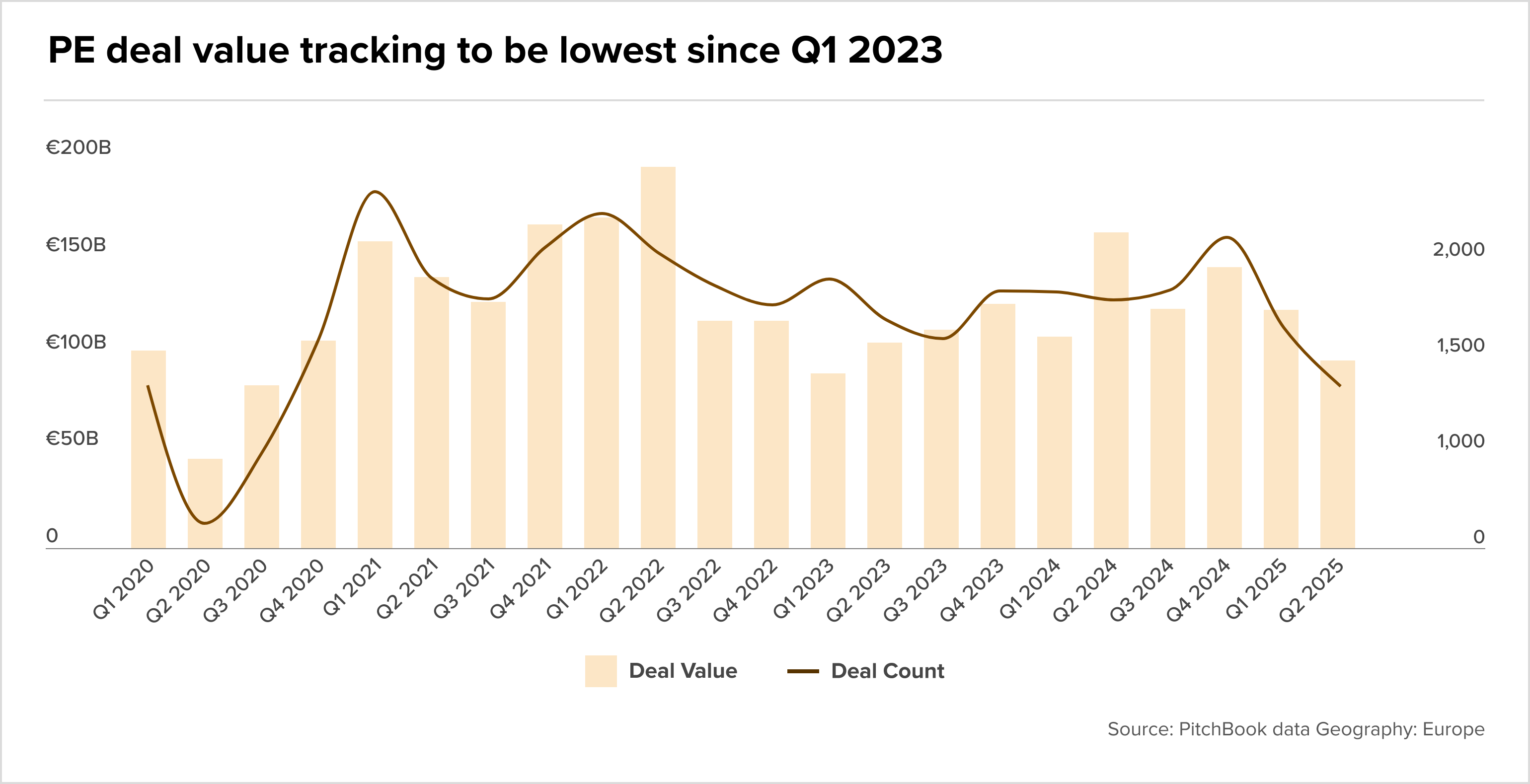

Narrowing down to the European PE scene, it becomes clear that Trump’s ‘Liberation Day’ tariffs have turned capital deployment into a frustrating waiting game. European GPs are sitting on a mountain of dry powder, €324bn to be exact, but they’re showing little appetite to deploy it.

PitchBook data shows only €97bn was transacted in Q2, making it the slowest quarter since Q1 2023, with deal count hitting its lowest point since Q3 2020.

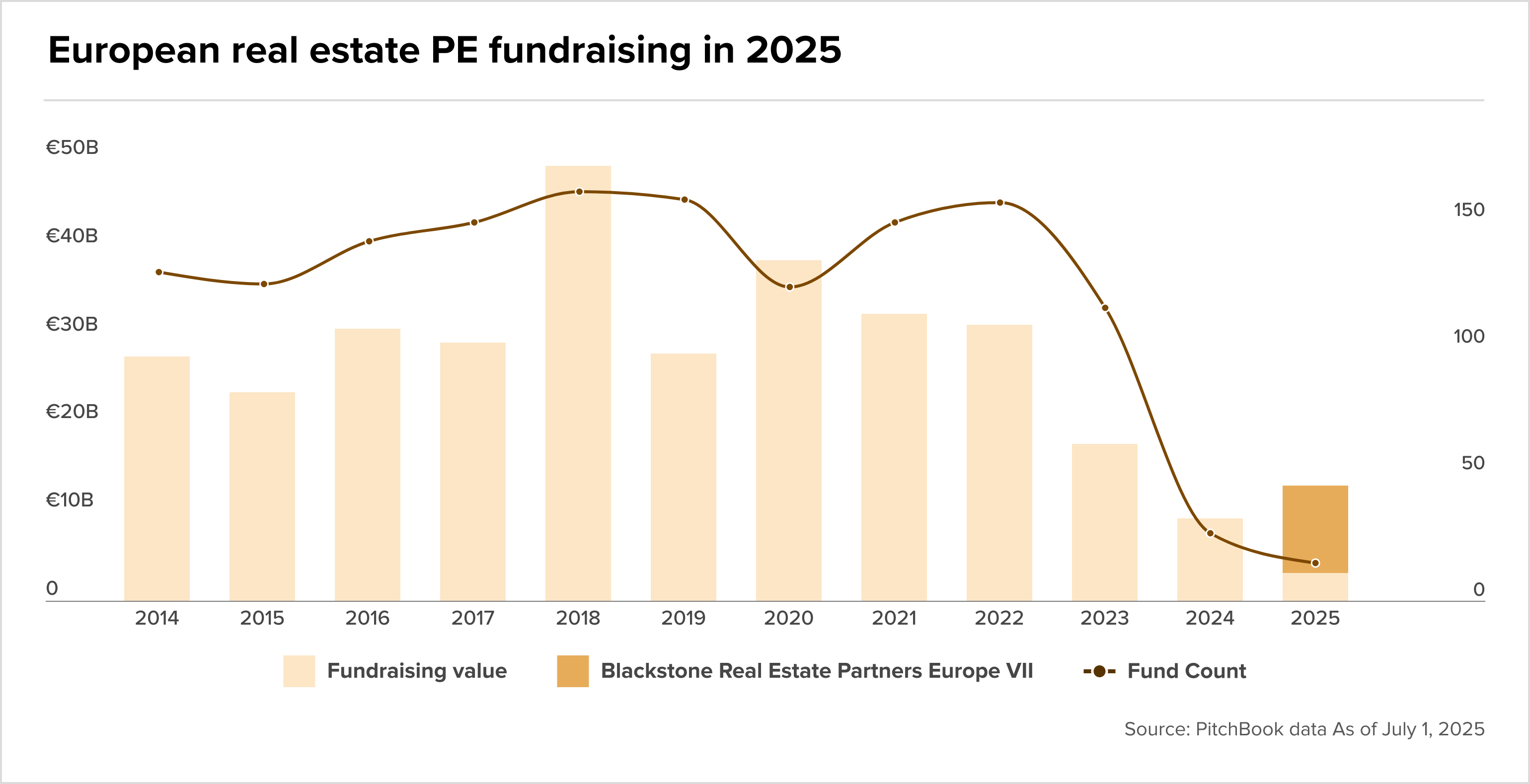

European real estate fundraising builds momentum

However, the European real estate market is having quite the comeback story. After what can only be described as a rather bruising couple of years, the sector has managed to raise €13.1bn in just six months, already eclipsing 2024’s full year tally of €9.5bn.

While Blackstone’s record €9.8bn vehicle did most of the heavy lifting, the broader trend suggests investors are finally ready to believe that “the real estate recovery is coming into view.”

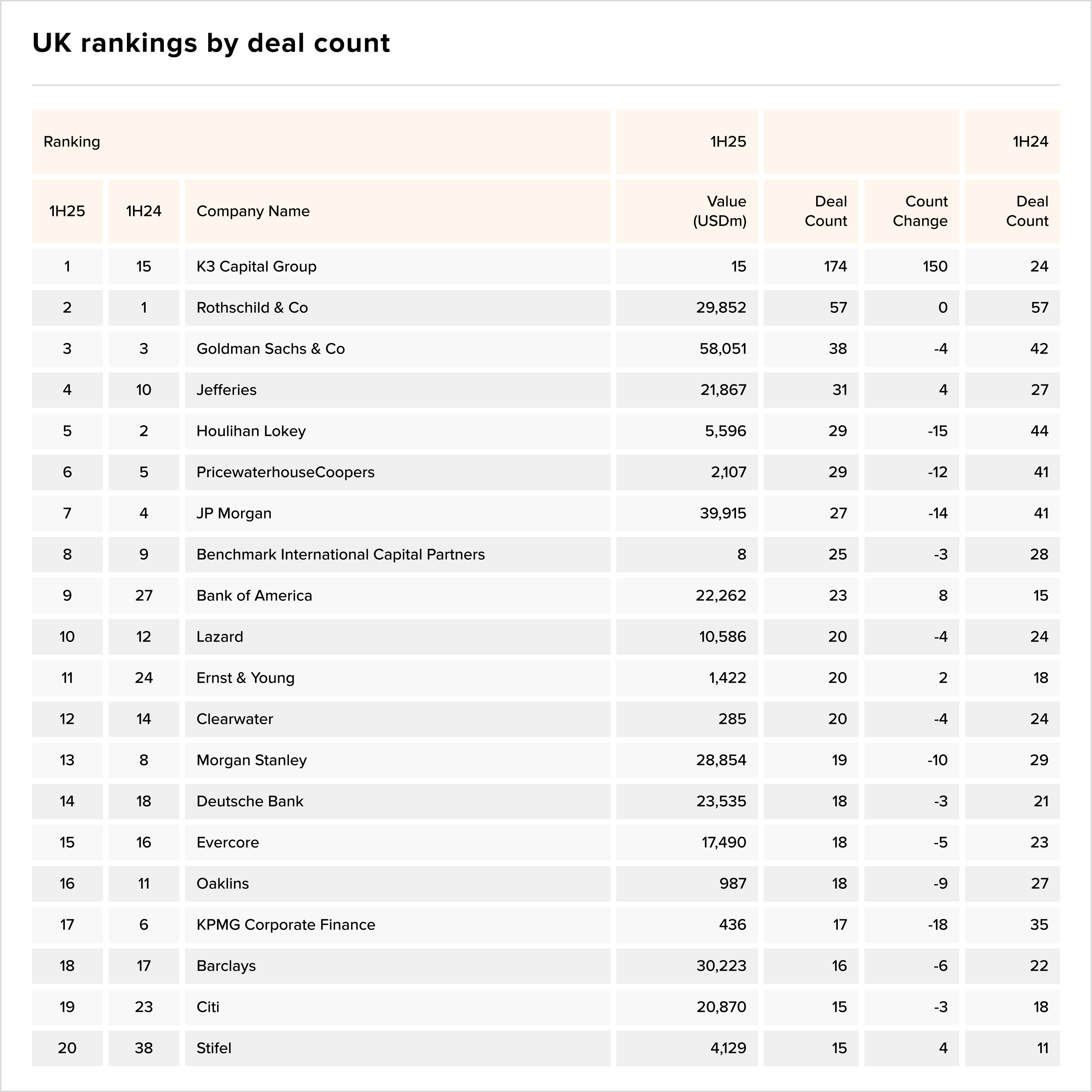

K3 stacks up low value deals

And finally, according to Mergermarket’s H1 25 global and regional M&A rankings, K3 Capital Group stormed to the no.1 spot for the most active dealmakers in Europe, with 174 deals. However the total value was $15m, proving K3’s reach in the SME market.

Fundraising

- Revolut in talks to raise new funding at $65bn valuation

- MML closes latest B2B-focused fund at $1.2B

- Exponent exceeds target with €1bn+ close for fifth flagship fund

- Coller Capital closes record $6.8bn private credit secondaries fund

IPOs

- Hg-backed Visma targets London for IPO

- SHEIN IPO shine should not force UK to abandon its principles

Le ultime due settimane sono segnate da UniCredit che, considerando la sua quota in Generali come un investimento non strategico, ne ha iniziato la cessione. Valeo Foods, controllata da Bain Capital, acquisisce lo storico marchio Melegatti, azienda fondata dal creatore del pandoro; ed in fine, il report dell’AIFI segna come l’Italia stia guadagnando terreno nel mondo del Private Equity, nonostante la golden power e l’eccesso di regolamentazione.

Ecco i dettagli sulle informazioni più rilevanti:

- UniCredit ha avviato la cessione di una quota significativa di Generali, in un’operazione che potrebbe valere oltre 2 miliardi di euro. La mossa rientra nella strategia di razionalizzazione degli investimenti non core della banca.

- Bain Capital Private Equity, tramite Valeo Foods, acquisisce Melegatti (nota per il Pandoro) dalla famiglia Spezzapria, che l’aveva rilevata nel 2018. L’operazione rafforza il portafoglio di dolciari premium del gruppo.

- L’Italia conferma la sua attrattività per il private equity con 6,2 miliardi di investimenti nei primi 5 mesi del 2025 (+18% YoY), ma secondo l’AIFI le golden power e l’eccesso di regolamentazione stanno rendendo il Paese meno competitivo rispetto ad altri mercati europei. In particolare, il 40% dei deal sopra i 100 milioni subisce ritardi autorizzativi, con costi aggiuntivi che possono arrivare al 2-3% del valore dell’operazione.

Troverete questo e molto altro in questa edizione di M&A Teaser Italia.

Trasferimenti

- Moroello Diaz della Vittoria Pallavicini assume la presidenza della holding italiana di Aon, succedendo a Sergio Erede.

- Nicola Cattarossi è il nuovo chief financial officer e responsabile corporate affairs di Fabrick.

- Giuseppe Bernardi è stato nominato presidente e referente per le funzioni di controllo di Atlas SGR.

- Davide Elli è stato nominato condirettore generale di Fideuram Intesa Sanpaolo Private Banking (Fideuram ISPB).

- TIM ha nominato Emanuele Rimini (già AD di Banca Finnat) come rappresentante degli azionisti retail, segnando un passo verso una governance più inclusiva.

- AM (gruppo spagnolo specializzato in M&A) rafforza la sua base italiana con l’arrivo di Marco Turelli (ex Equita) alla guida della Corporate Finance. Obiettivo: capitalizzare sul boom di operazioni in Italia (+15% YoY), con focus su tech e healthcare.

- LeoVegas Italia ha nominato Carmine Giordano (ex Sisal e Snai) come nuovo AD per potenziare la crescita nel mercato italiano del gaming online, valutato oltre 2 miliardi di euro.

- Alvarez & Marsal, il big del restructuring, lancia in Italia una divisione M&A dedicata alle mid-cap, guidata da Turelli. Primo obiettivo: 10 operazioni/anno nel range 50-300 milioni, con focus su energia e healthcare.

- Siparex amplia il team di Milano con due nuovi senior, puntando a 3-4 deal/anno in Italia nel range 50-200 milioni.

Global trends

-

Secondo l’analisi di Grant Thornton, le aziende italiane del mid-market (fatturato 50-500 milioni) stanno dimostrando una forte resilienza nonostante l’impatto dei dazi commerciali, con il 68% che mantiene margini EBITDA stabili o in crescita. La risposta strategica è un’accelerazione degli investimenti in tecnologia, che raggiungeranno i 2,5 miliardi nel 2025 (+30% vs 2024), concentrati soprattutto su AI (35% del totale), automazione industriale (25%) e cybersecurity (20%). Il settore manifatturiero guida questa trasformazione, rappresentando il 45% degli investimenti tech, mentre il 60% delle aziende sta riorganizzando le catene di approvvigionamento per mitigare i rischi geopolitici.

- Secondo l’analisi di PwC, il mercato globale delle fusioni e acquisizioni ha registrato una sorprendente crescita del 15% nel primo semestre 2025 in termini di controvalore, trainato soprattutto dai settori tech ed energia. Tuttavia, le exit del private equity sono in stallo (-20% YoY), con tempi di realizzo medi che superano ora i 5 anni rispetto ai tradizionali 3-4, a causa delle condizioni di mercato più complesse e della ridotta appetibilità per gli IPO.

-

L’Italia conferma la sua attrattività per il private equity con 6,2 miliardi di investimenti nei primi 5 mesi del 2025 (+18% YoY), ma secondo l’AIFI le golden power e l’eccesso di regolamentazione stanno rendendo il Paese meno competitivo rispetto ad altri mercati europei. In particolare, il 40% dei deal sopra i 100 milioni subisce ritardi autorizzativi, con costi aggiuntivi che possono arrivare al 2-3% del valore dell’operazione.

- I mercati emergenti rallentano l’emissione di bond sostenibili (GSSS – green, social, sustainability, sustainability-linked): nel primo trimestre 2025, il volume è sceso del 18% rispetto allo stesso periodo del 2024. In calo anche la quota di emissioni ESG rispetto al totale del debito emesso, segnalando un raffreddamento degli investitori verso i titoli a impatto.

- Ad aprile il fatturato industriale in Italia aumenta dell’1,5% mese su mese in valore (e 1,6% in volume), mentre i servizi mettono a segno un +0,5% in valore, +0,4% in volume. Su base annua +1,1% il fatturato industriale, +2,1% nei servizi: il commercio all’ingrosso traina con +1,2% su base annua.

- Secondo Assifact, il factoring cross-border italiano vola: +20% nel primo trimestre 2025, spinto dal commercio globale e dalla digitalizzazione delle piattaforme. L’export factoring vale 7 miliardi, con crescita a doppia cifra per le PMI. L’Italia si conferma terzo mercato UE dopo Francia e Germania.

- Nonostante i venti di recessione in Germania (-0,2%) e USA (+0,3%), l’Italia cresce dello 0,8% nel Q2, trainata da export e turismo. La Banca d’Italia però avverte: “Rischio inflazione e debito pubblico restano critici”.

- Boom dei family office in Italia (oltre 200), ma la mancanza di un quadro normativo chiaro crea confusione tra advisor indipendenti, multifamily, single office e boutique patrimoniali. Solo 1 su 10 gestisce direttamente asset, mentre gli altri fungono da hub strategici senza licenza finanziaria. Serve una riforma strutturata per dare forma a un mercato da oltre 100 miliardi in gestione.

Bancario/Assicurativo

Landscape

- Banco BPM ha lanciato una strategia integrata per supportare le PMI nella transizione digitale ed ecologica, con 2 miliardi di euro di finanziamenti dedicati entro il 2026. Il piano prevede soluzioni tailor-made che combinano credito agevolato (tassi dal 2,5%) e consulenza specialistica, puntando a coinvolgere 5.000 imprese nei prossimi 18 mesi.

- BPER Banca migliora la sua proposta di acquisizione su Banca Popolare di Sondrio (BPS), passando a 1 azione BPER ogni 9,85 azioni BPS (contro il precedente rapporto 1:10,5). La nuova valutazione implica un prezzo implicito di 7,5 euro per azione BPS, con una capitalizzazione complessiva di circa 1,1 miliardi di euro. L’operazione, sostenuta da Unipol, mira a creare il quarto gruppo bancario italiano per dimensione, consolidando la presenza nel Nord Italia.

- Monte dei Paschi di Siena (MPS), dopo l’upgrade di Fitch, accelera i piani per un’alleanza con Banco BPM, mirando a creare il terzo polo bancario italiano. L’operazione dipenderà anche dalle valutazioni di Borsa e dalla regia del MEF.

- Si scioglie il patto di consultazione tra i principali azionisti di Illimity Bank, tra cui Sator, FG2 e ICP. La mossa spiana la strada all’OPA promossa da Banca Ifis, che punta a rafforzarsi nel settore corporate banking con sinergie su credito distressed e servizi alle PMI.

- Cherry Bank ha finalizzato una cartolarizzazione da 375 milioni di euro su un portafoglio di crediti performing verso PMI italiane. L’operazione rientra nella strategia di rafforzamento della liquidità e ottimizzazione patrimoniale, con il supporto di investitori istituzionali internazionali.

- Unipol ha deciso di aderire all’OPA lanciata da BPER su Banca Popolare di Sondrio, accettando l’offerta di 10,50€ per azione. L’operazione, sostenuta da BNP Paribas, potrebbe accelerare il consolidamento nel settore bancario italiano, con BPER che punta a rafforzare la sua quota di mercato.

- Poste Italiane avvia l’accorpamento di BancoPosta, Poste Vita e Poste Assicurazioni per tagliare costi (obiettivo: 300 milioni di risparmi in 3 anni) e semplificare l’offerta finanziaria. Il titolo Poste sale del 2% in Borsa dopo l’annuncio.

- Il MEF ha nominato i liquidatori per Banca Progetto dopo il fallimento del piano di salvataggio. Aidexa e Compagnia Finanziaria (CF) sotto la lente, con esposizioni superiori a 500 milioni di euro. I creditori temono un recovery rate sotto il 30%.

- Il fondo da 1 miliardo gestito da Invitalia è accessibile solo ad aziende in crisi con requisiti precisi: almeno 50 milioni di ricavi, 50 dipendenti e piani di ristrutturazione approvati. Vietato l’accesso a chi ha debiti verso la PA o pendenze fiscali. Il fondo investirà in equity e quasi-equity, solo a fianco di investitori privati.

- La BCE ha approvato l’OPA su Monte dei Paschi condizionandola alla cessione di attività non-core e al rispetto di stringenti target di capitalizzazione (CET1 al 14%). Mediobanca, advisor dell’operazione, prevede chiusura entro Q1 2026.

- Ifis alza l’offerta a 3,20€/azione (+6% vs precedente) dopo lo scioglimento del patto di sindacato che bloccava il 25% di Illimity. L’operazione, ora valutata 1,2 miliardi, punta a creare un polo digitale leader in NPL e fintech.

- Gli investitori assicurativi italiani sono tiepidi sui Fondi Rilancio: solo 2 hanno partecipato a FITD e FRI, frenati da vincoli Solvency II, orizzonti temporali lunghi (fino a 12 anni) e scarsa liquidità. Serve un maggiore allineamento tra politiche pubbliche e esigenze di rendimento attuariale.

- UniCredit ha avviato la cessione di una quota significativa di Generali, in un’operazione che potrebbe valere oltre 2 miliardi di euro. La mossa rientra nella strategia di razionalizzazione degli investimenti non core della banca.

M&A

- Il fondo americano JC Flowers prosegue la sua espansione in Italia con l’acquisizione del veneto Intermedia B, specializzato nella gestione assicurativa per la Pubblica Amministrazione. L’obiettivo è creare un polo da 500 milioni di premi.

- Banca Ifis ha raccolto adesioni all’OPAS su Illimity per l’84,1% del capitale. Obiettivo: superare il 90% per procedere allo squeeze-out e offrire un extra premio del 5% sul corrispettivo (1,6835 € cash + 0,1 azioni Ifis per ogni azione Illimity). La finestra si riapre dal 7 all’11 luglio.

- La insurtech italiana Lokky entra nel gruppo assicurativo Hiscox, puntando a crescere nell’underwriting digitale e nei prodotti parametrici.

- Il broker assicurativo PIB Group, sostenuto dai fondi Apax e Carlyle, rafforza la sua presenza in Italia con l’acquisizione di Nemesi, società milanese specializzata in assicurazioni cyber e rischio tecnologico. L’operazione segue l’ingresso di PIB nel mercato italiano nel 2022 con l’acquisto di Diana Assicurazioni e conferma la strategia di crescita nel segmento delle polizze specialistiche.

- Banca Popolare Pugliese ha ceduto un portafoglio NPL a uno special purpose vehicle garantito al 70% da Akros, con rating BBB. L’operazione migliora il CET1 ratio di 50 bps e libera risorse per nuovi finanziamenti a PMI.

- Il private equity britannico ICG è in trattativa per subentrare a Xenon Private Equity nel controllo di Excellera Advisory Group, valorizzata 200 milioni di euro. L’operazione mira a rafforzare la presenza in Italia nel wealth management.

Consumo

Landscape

M&A

- Illycaffè rafforza la sua presenza in Svizzera acquisendo la maggioranza di Sietz AG, storico distributore elvetico. L’operazione consente di presidiare direttamente il canale horeca e premium retail nel mercato svizzero, strategico per l’espansione europea del marchio triestino.

- Campari ha ceduto il brand Cinzano al Gruppo Caffo 1915 per 50 milioni di euro, focalizzandosi su portafoglio premium. Advisor d’eccezione: Lazard per Campari, KFinance per Caffo. Un passo strategico per entrambi: Caffo rafforza il suo catalogo, Campari snellisce il portafoglio.

- Dexelance, fondo specializzato in foodtech, entra nel capitale di Roda (leader in macchinari per cioccolato) con un’operazione da 60 milioni, valutando la società 240 milioni (10x EBITDA). PwC ha curato due diligence e strutturazione.

- Carlyle sta negoziando la cessione del brand di protezioni sportive Dainese ai creditori del gruppo HPS Investment Partners e Arcmont Asset Management. L’operazione potrebbe chiudersi a una valutazione superiore ai 500 milioni di euro.

- Demeglio, gruppo orafo premium sostenuto dal fondo Equita Smart Capital ELTIF, rileva il 100% di RF Jewels, rafforzando la sua presenza nel segmento high-end. L’acquisizione punta a sinergie produttive e commerciali.

- Il fondo Oakley Capital cede il brand di pelletteria luxury Smythson al gruppo Tivoli per 15 milioni di sterline, con una perdita rispetto ai 18 milioni di sterline spesi nel 2009. La mossa riflette una razionalizzazione del portafoglio.

- Il fondatore Pedini riacquista l’azienda di arredamento dal gruppo cinese Hua Wei Mei Lin, chiudendo un’era di gestione asiatica. Obiettivo: rilanciare il brand storico con focus su design e mercato europeo.

- Bain Capital Private Equity, tramite Valeo Foods, acquisisce Melegatti (nota per il Pandoro) dalla famiglia Spezzapria, che l’aveva rilevata nel 2018. L’operazione rafforza il portafoglio di dolciari premium del gruppo.

- Pernigotti e Walcor si uniscono in un nuovo polo cioccolatiero, sostenuto da JP Morgan e Invitalia. L’obiettivo è competere a livello globale, ottimizzando produzione e distribuzione.

Energia

Landscape

- Il governo italiano accelera su eolico, fotovoltaico (+12 GW entro 2027) e mini-reattori nucleari per ridurre la dipendenza dal gas (oggi al 40%) e contenere la volatilità dei prezzi. L’obiettivo: portare le rinnovabili al 45% del mix energetico entro il 2030.

- Nel 2023 gli investimenti spagnoli in Italia sono cresciuti dell’8,5%, generando 77mila nuovi posti di lavoro. Settori trainanti: energia rinnovabile (Iberdrola) e fintech (BBVA). L’Italia è ora il 3° mercato UE per FDI dalla Spagna.

- CH4T e Suma Capital ricevono un finanziamento project financing da 100 milioni di euro da BBVA per riconvertire 7 impianti biogas italiani in biometano, allineandosi alla transizione energetica.

M&A

- IRR Solar, controllata da NRGFarm, ha acquisito due impianti fotovoltaici in Italia da Hanwha Europe, con una capacità combinata di 10 MW. L&B Partners ha assistito l’acquirente, mentre LMCR ha seguito i venditori. L’operazione rafforza la presenza di IRR nel mercato delle rinnovabili.

- Il fondo Ardian (ACEEF) rileva da E2E 117 impianti fotovoltaici in Italia (116 MW), consolidando il suo portafoglio di rinnovabili. L’operazione valorizza asset operativi in Lombardia, Veneto e Puglia.

- Altea Green Power ha ceduto a un investitore europeo un progetto fotovoltaico ready-to-build in Molise per 13 milioni di euro. L’impianto ha una capacità prevista di 50 MW e l’operazione rientra nel piano di rotazione degli asset per finanziare nuovi sviluppi.

- Acea vende Acea Energia a Eni Plenitude per 460 milioni: l’operazione, approvata dal CDA, consente ad Acea di ridurre il debito mentre Eni rafforza la sua posizione nel mercato retail dell’energia, integrando 500.000 clienti. Chiusura prevista entro Q3 2025.

- Vivi Energia consolida la sua posizione nel mercato green acquisendo la maggioranza di PlanGreen, operatore specializzato in efficienza energetica, dal Fondo FIEE. L’operazione valorizza PlanGreen a 15 milioni di euro, con un EBITDA multiplo di 7x.

- La holding dei Benetton ha approvato un piano da 1 miliardo per acquisizioni in logistica, food e infrastrutture, dopo la cessione di Autostrade. Primo target: partecipazioni in società di energie rinnovabili in Sud Europa.

Healthcare

Landscape

-

Il settore biotech italiano mostra un’accelerazione impressionante con 127 milioni di investimenti nella prima metà del 2025 (rispetto ai 221 milioni di tutto il 2024), portando il totale raccolto dal 2022 a 730 milioni. Il 60% dei finanziamenti è concentrato in terapie avanzate e diagnostica, con Milano che consolida la sua posizione di hub principale (45% dei deal).

- La società farmaceutica Otofarma, con un fatturato stimato di 50 milioni di euro, sta valutando il debutto in Borsa, sfruttando il rilancio del mercato per il settore healthcare. L’operazione potrebbe attrarre investitori istituzionali, puntando sulla crescita nel mercato otologico.

M&A

- Neopharmed Gentili, sostenuta da Ardian e NB Renaissance, acquisisce per 264 milioni di dollari il business europeo di Orladeyo da BioCryst Pharmaceuticals. L’accordo rafforza il portafoglio farmaceutico per le malattie rare e amplia la presenza in mercati chiave come Germania, Spagna e UK.

- Armonia SGR ha completato il secondo investimento del suo Fondo II acquisendo tre aziende nel settore healthcare e servizi, per un valore complessivo di 50 milioni. Il fondo punta a raggiungere 300 milioni di raccolta entro fine 2025.

Immobiliare

Landscape

- A maggio 2025 i mutui residenziali sono schizzati a 4,2 miliardi (+50,2% YoY), spingendo le compravendite immobiliari a +18%. Il mercato beneficia dei tassi fissi sotto il 3,5% e degli incentivi fiscali sul 110%.

- Kervis SGR riqualifica l’ex padiglione NATO a Milano (investimento 4 milioni). Il fondo GO Italia V ha locato l’asset riqualificato, acquistato da DEA Capital Real Estate, con un rendimento netto del 5,5%. Strategia: riconversione di immobili dismessi in spazi polifunzionali.

- Borgosesia ha completato la cartolarizzazione del progetto residenziale “Abitare Lainate” a Milano, con un finanziamento di 72 milioni erogato da BPER Banca. L’operazione copre l’85% del valore dell’investimento, con tasso fisso al 4,5%.

M&A

- Il fondo di Dea Capital ha venduto l’immobile storico di Banca MPS a Roma a Corso Gestioni Alberghiere e Talia Gestioni per 123 milioni, con un rendimento netto del 5,5%. La banca resterà in locazione per 9 anni.

- La gioielleria Fasoli lancia un hotel a 5 stelle nel centro storico di Brescia, con un investimento di 25 milioni. L’operazione riqualificherà un palazzo del ‘500, puntando su turismo high-end.

- Il gruppo spagnolo Arcenpreix ha venduto lo shopping center Talenti Village, situato nella capitale, a un investitore internazionale non rivelato. L’operazione conferma l’interesse per l’immobiliare retail italiano, nonostante le sfide del settore post-pandemia.

Industriale

Landscape

-

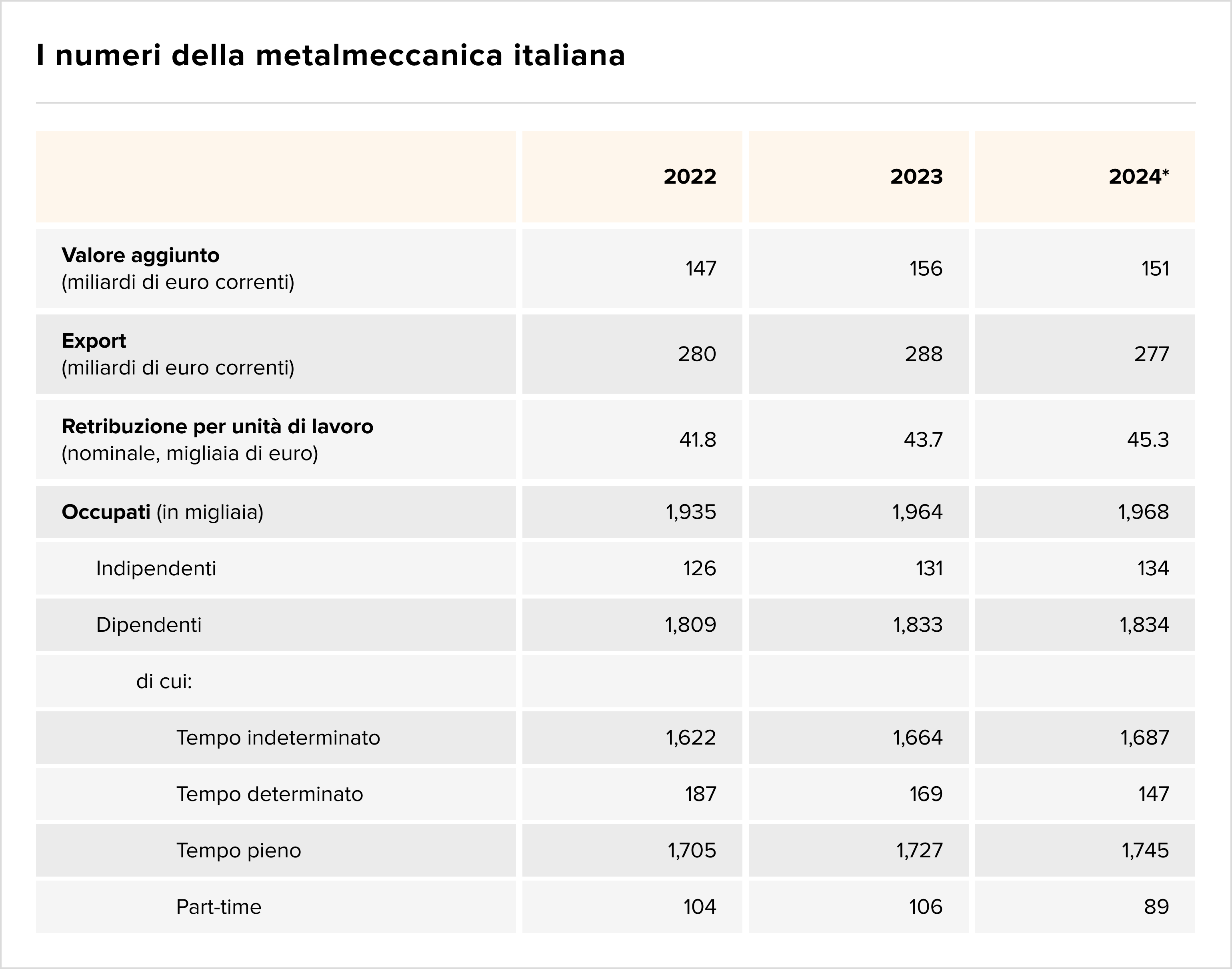

Il “Cruscotto FIM‑CISL” rileva una crescita del lavoro a tempo indeterminato e delle retribuzioni nel comparto metalmeccanico, con salari che hanno recuperato quasi totalmente l’inflazione grazie a clausole ex‑post. Tuttavia, Irpef + contributi gravano per il 32,4% sui salari (era 32% nel 2015), erodendo i guadagni netti.

- Fincantieri si è aggiudicata un contratto da 700 milioni di euro per la costruzione di navi da crociera in Indonesia, facendo schizzare il titolo in Borsa (+5,2%). Gli analisti prevedono ulteriore upside, con target price a 0,85€ (+12% dal corrente livello).

- Le immatricolazioni UE a maggio segnano +19% (1,1 milioni di vetture), trainato da elettriche (+28%). Nonostante il rimbalzo, il mercato è ancora -12% vs 2019. Tesla domina con il 18% dell’EV market share.

- Il governo sta valutando nuove strategie per Ilva (Taranto) e l’ex Rixi (Genova), tra riconversione industriale e possibili investitori. L’obiettivo è salvaguardare l’occupazione e rilanciare i siti, con Urso (MISE) in prima linea.

M&A

- Armonia SGR ha rilevato Ceresoli Utensili, Dorigo Utensili e Lamev (settore metalmeccanico), puntando a creare un polo industriale con 120 milioni di fatturato aggregato e margini EBITDA del 18%.

- Il gruppo IT italiano SESA (controllato da Var) acquisisce l’80% della tedesca Visicon, specializzata in soluzioni Industry 4.0, per 28 milioni. L’operazione rafforza la presenza europea dopo le acquisizioni in Spagna e Francia.

- Clerici Group ha completato l’acquisizione di un player nel settore packaging (valore 120 milioni, 7x EBITDA) e la vendita di una divisione non-core, ottimizzando la struttura. Obiettivo: focalizzarsi su mercati high-growth con margini superiori al 20%.

- Cellulose Converting Solutions, specialista italiano in packaging sostenibile, è stata ceduta alla multinazionale JOA con un multiplo di 8x EBITDA. L’operazione include un earn-out legato alla crescita nel mercato USA.

- Il gruppo tessile Salico, controllato da Monte Calvo Inversiones, sarà acquisito dalla austriaca Andritz, attiva in soluzioni high-tech per il nonwoven. L’accordo vincolante rafforza la posizione di Andritz nel mercato europeo e apre sinergie industriali nella filiera tessile green.

- Ognibene cede la maggioranza a Renold Group per 85 milioni: il gruppo inglese rileva il 60% del produttore di trasmissioni industriali, con Ethica come advisor. La valutazione (85 milioni) riflette un EBITDA margin del 18% e una posizione leader in Europa.

- Il fondo Redfish (controllato da Expo Inox) acquisisce il 100% della tedesca Steegmüller Kaminoflex, specializzata in canne fumarie in acciaio inox. L’operazione rafforza la presenza nel mercato industriale europeo, con l’obiettivo di espandere la produzione e la distribuzione.

- Il gigante statunitense Ingersoll Rand entra in Italia acquisendo Termomeccanica Compressors e Adicomp, leader nei compressori industriali ad alta efficienza energetica. L’affare, valutato 160 milioni di euro, mira a rafforzare la filiera europea della pneumatica industriale.

- Il gruppo ferrarese Incico, attivo in ingegneria civile e impiantistica, acquisisce Italiana Sistemi, specializzata in infrastrutture ferroviarie e stradali. L’operazione consolida la presenza nel Sud Italia e amplia l’offerta tecnologica.

- Il PE G Square Capital acquisisce la maggioranza di G.21, azienda italiana di dispositivi medici, dalla famiglia Foroni. L’obiettivo è accelerare l’espansione internazionale nel settore healthcare, sfruttando il know-how storico del brand.

- Il fondo Eliance, joint venture tra Swiss Life Asset Managers e Riverrock, ha rilevato la quota residua del 30% di EliFriulia, diventandone unico proprietario. La società controlla un portafoglio logistico e industriale in Friuli-Venezia Giulia, con potenziali ulteriori investimenti nella regione. L’operazione rientra nella strategia di Eliance di espansione nel mercato immobiliare italiano.

- Il gruppo turco Baykar, noto per i droni militari Bayraktar, con il supporto di EY come advisor, è in trattativa per rilevare i complessi industriali di Piaggio Aerospace, in amministrazione straordinaria. L’operazione potrebbe portare a un rilancio del sito italiano, con possibili sviluppi nella produzione aerospaziale.

- Il gruppo britannico Concentric ha acquisito O.M.P. Officine Mazzocco Pagnoni, attiva nella lavorazione di metalli. L’affare consolida la presenza di Concentric in Europa, puntando sull’export italiano.

Servizi

M&A

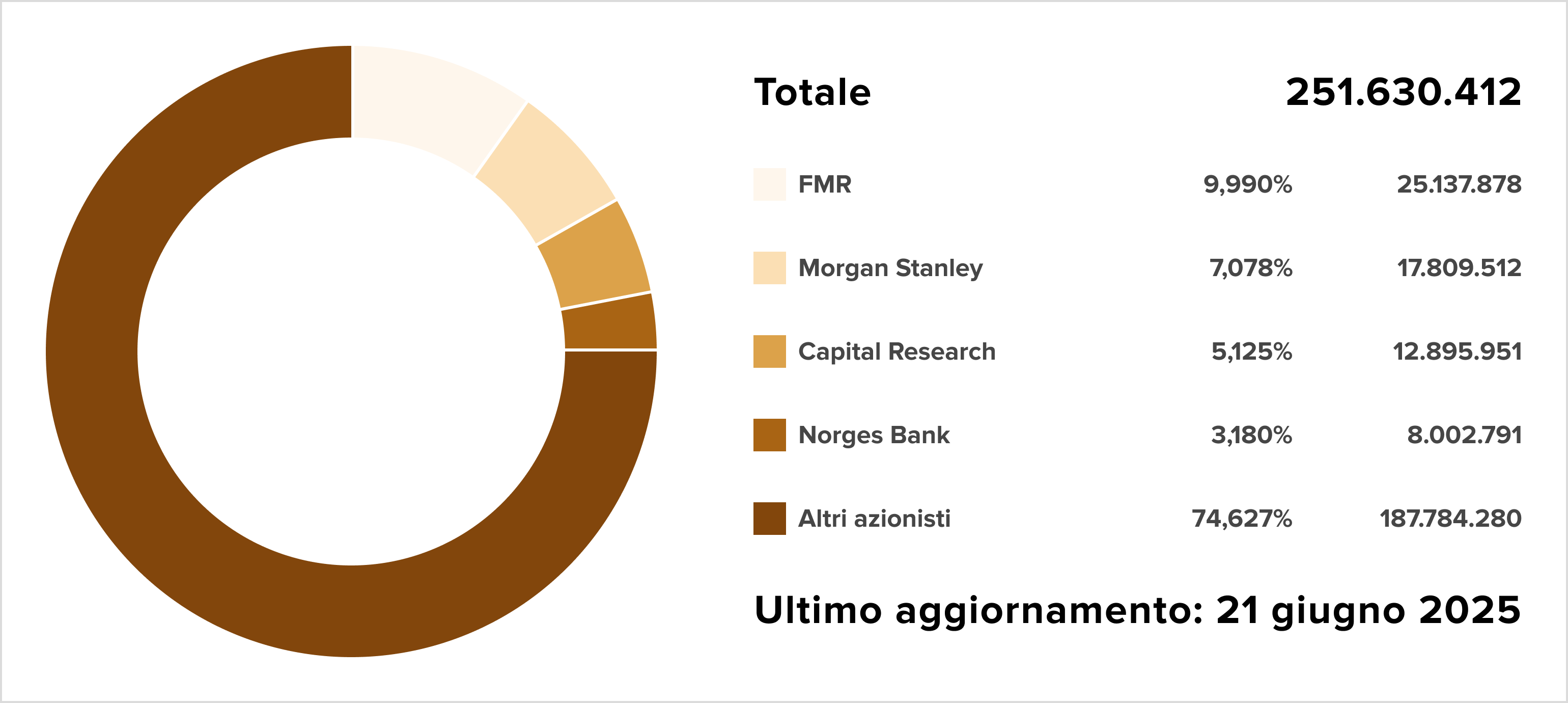

-

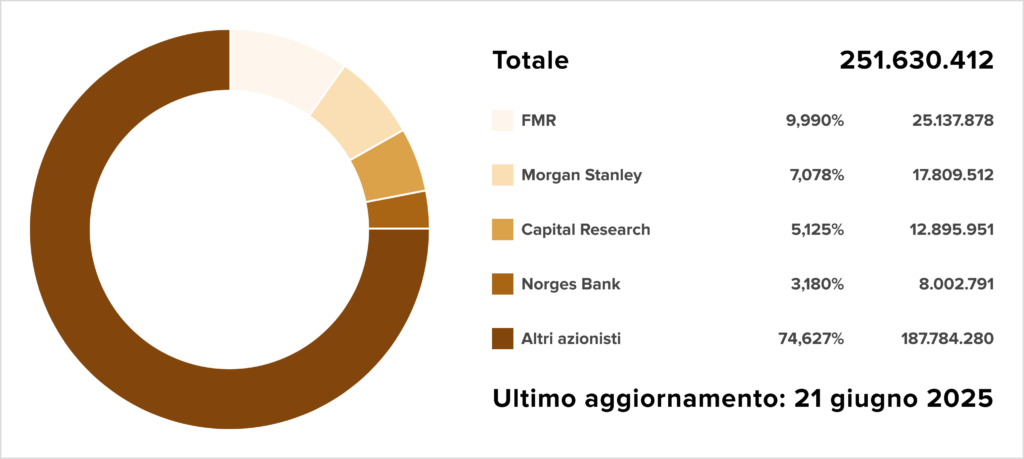

Fidelity sale al 9.990% di Lottomatica dopo l’uscita di Apollo Global Management 9 giorni prima. L’investimento per raggiungere la posizione di maggiore azionista è pari a €565m.

- Oltre Impact, fondo di impact investing, ha acquisito il 60% di My English School, catena italiana di scuole di inglese. L’obiettivo è espandere il modello in Italia e all’estero, puntando su un approccio ibrido tra digitale e fisico.

- Ambienta ha acquisito No-Dig Alliance, gruppo attivo nelle tecnologie di scavo non invasivo per infrastrutture. L’operazione, sostenuta da advisor come Ethica e Chiomenti, mira a cavalcare il trend della sostenibilità nei lavori pubblici e reti idriche.

- Moltiply ha collocato il 2,5% del proprio capitale a 8,50€/azione (-6,6% vs prezzo di mercato), incassando 45 milioni. Nonostante lo sconto, il titolo mantiene un rendimento del +20% nell’ultimo semestre, grazie alla crescita nei servizi finanziari digitali.

- Nextalia Private Equity completa l’exit cedendo il 55% di Firstance (software finanziari) alla francese Harvest per 185 milioni di euro. Un ritorno significativo sull’investimento.

- Il fondo Koinos Capital SGR acquisisce People Design e ManganoRobot, creando la piattaforma FuturA Group per l’innovazione digitale. L’obiettivo è consolidare servizi avanzati di design e automazione, puntando a un’espansione internazionale.

- Sella Investment Banking e Chiomenti hanno guidato la cessione di Codd Date (controllata da Fabrick) a Links Management and Technology, con LRV Legal come advisor legale per l’acquirente. L’affare valorizza il know-how del fintech italiano nel data processing per il credito, settore in forte crescita.

- Il consorzio HOFI, formato da Antin Infrastructure Partners e Augens, ha acquisito Silve, operatore italiano di servizi idrici e ambientali. L’operazione è stata supportata da LMS e Martinez & Partners come advisor finanziari, mentre EY ha curato la due diligence. I venditori, rappresentati da RTZ e NRTZ, cedono un asset strategico nel settore delle utilities.

- Air France-KLM ha perfezionato l’acquisizione di Scandinavian Airlines (SAS), consolidando la sua posizione nel mercato europeo del trasporto aereo. L’operazione mira a creare sinergie sui voli transatlantici e rafforzare la competitività del gruppo.

- Equita e la boutique padovana BZM avviano una partnership per potenziare l’advisory nel Nordest, puntando su M&A e finanza strutturata per PMI e mid-cap.

Sport

Landscape

M&A

- Bernardino Passeri e Andrea Londono Osorio rilevano il club Ascoli Calcio da Massimo Pulcinelli (Bricofer). Sponsor tecnico e obiettivi di crescita in Serie B i prossimi step.

- Fininvest cede il Monza al fondo Beckett Layne Ventures per 45 milioni di euro, con Adriano Galliani probabile presidente. Valorizzazione del club dopo la promozione in Serie A.

TMT

Landscape

- Il settore dei data center attira sempre più private equity, con transazioni globali già a 45 miliardi di dollari nel 2025 (+25% YoY). Fondi come Blackstone e KKR puntano sull’infrastruttura cloud, con rendimenti stabili al 8-10% annuo.

- I colossi del private equity (Blackstone, KKR) stanno scalando il settore dei data center, attratti da rendimenti stabili all’8-10%. In Italia, il mercato vale 1,2 miliardi con crescita annua del 15%, trainata dalla domanda cloud.

M&A

- Il fondo USA Performant Capital acquisisce Wine Suite, software CRM per cantine sviluppato da Divinea. L’operazione punta a scalare la piattaforma nel mercato vitivinicolo globale.

- Txt e-Solutions, specializzata in software finanziari, ha rilevato una quota del 10% di Altilia, startup italiana di intelligenza artificiale, per 1 milione di euro, con l’obiettivo di arrivare al controllo totale. L’operazione rafforza l’offerta tecnologica di Txt nel settore fintech.

Fundraising

- Ambienta ha chiuso il nuovo fondo “Nexus II”, targeting aziende da 20-150 milioni di fatturato. Già in pipeline 3 investimenti in circular economy e energy efficiency.

- Azimut lancia un nuovo ELTIF da 100 milioni di euro focalizzato su energy-tech, con advisory di Eni Next. Il fondo investirà in startup innovative nel settore energia e decarbonizzazione.

- Ream SGR ha avviato un nuovo fondo immobiliare dedicato allo sviluppo di un resort di lusso in Piemonte, in partnership con Club Med. L’operazione punta a capitalizzare sul turismo premium nelle Alpi italiane, con un investimento stimato in decine di milioni di euro.

Se na Edição #88 nós já te trouxemos o insight de que “os tradicionais estão saindo da zona de conforto”, na leitura desta quinzena temos a repercussão prática dessa percepção. E, dessa vez, quem foi o exemplo de disrupção foi o setor de Real Estate.

Entre a fusão de gigantes criando titãs entre as administradoras e portfólios inteiros sendo vendidos, nossa curadoria identificou mais de BRLm 880 de valor divulgado no setor durante a quinzena. E não faltam exemplos de movimentações estratégicas para todos os perfis de investidor.

- Talvez a maior movimentação em Real Estate foi a fusão entre a Argo e Replan, que criou a terceira maior administradora de shoppings do Brasil. A Argoplan, resultado da operação, terá 30 shoppings e 5 mil lojas. Com o deal, as marcas almejam capilaridade, mais barganha com fornecedores e a atração de novas parcerias.

- Mas quando falamos sobre o maior cheque da quinzena, o título sem dúvidas vai para a Diamante Energia, que comprou 100% da termelétrica do Pecém por BRL 1 bi. A operação incluiu, além da planta de 720 megawatts de capacidade instalada, projetos de novas térmicas a gás natural licenciadas para participação em futuros leilões de energia.

- Ainda falando sobre Energia, o CADE aprovou a venda da Usina Leme, da Raízen, para Ferrari Agroindústria e Agromen Sementes Agrícolas por BRLm 425. A companhia está fazendo uma reciclagem do portfólio de ativos, com o intuito de reduzir o endividamento e capturar eficiência agroindustrial.

- Também há novidades em Logística: a GEF e Vinci compraram a operadora da Femsa e vão relançar a AGV. A transação de BRLm 700 traz o antigo CEO de volta ao mercado e incorpora Logvett.

Boa leitura!

Como agentes de IA estão remodelando o M&A, do sourcing ao due diligence: exemplos e cases study

Agentes de inteligência artificial (IA) têm um enorme potencial para tornar os processos de M&A mais rápidos e eficientes. Mas como separar os casos de uso tangíveis do mero hype de marketing?

Em 16 de julho, realizaremos um webinar em parceria com Ideals e Comparables.AI para discutir como os dealmakers estão usando IA para conquistar vantagem competitiva (e como esses casos de uso devem evoluir até 2026).

Deals Highlights

Curadoria entre 25 de Junho e 8 de Julho.

Número de deals identificados: 29

Valor total divulgado: BRL 3,87 bi

No xadrez global, o Brasil não é apenas peça; ele está no centro do tabuleiro

Donald Trump voltou ao centro das atenções. Às vésperas do prazo para renegociar tarifas com parceiros comerciais, o presidente afirmou que qualquer país que “se alinhe com as políticas antiamericanas do Brics” sofrerá uma tarifa adicional de 10%. A ameaça não veio por acaso: no Rio, os líderes do bloco retomaram as discussões sobre desdolarização e criação de um novo sistema de pagamentos.

No Brasil, o cenário interno também é delicado. A derrubada dos decretos que aumentariam o IOF criou um rombo fiscal de BRL 10 bi para 2025. O custo do capital segue alto, e o apetite por transações diminuiu. Ainda assim, o 1º semestre movimentou BRL 170 bi em M&A, com dois terços do volume vindo de investidores estrangeiros, puxado por infraestrutura e setores com receita previsível.

Segundo o BR Partners, o 2º semestre deve trazer mais tração. O ritmo não será acelerado, mas a direção está clara: setores com caixa forte, disciplina financeira e modelos resilientes continuam no radar. Não se trata mais de volume, mas de estratégia. E, em tempos de guerra tarifária, escolher o lado certo pode fazer toda a diferença.

Mercado dividido: EUA resistem enquanto Europa e Ásia sentem o peso das tarifas

Voltar a falar sobre tarifas não faz bem para ninguém. Enquanto o já mencionado cenário interno adiciona cada vez mais pressão no custo do capital, no cenário global as recentes declarações de Trump somam a um panorama que, em sua essência, é intimidador.

A pressão sobre os valuations voltou com força em 2025. A combinação de incerteza econômica crescente, impulsionada principalmente pelas tarifas e juros altos, derrubou os múltiplos médios globais para 10,8x, queda de 14% em relação a Q4 2024.

Mas o impacto não é uniforme: enquanto os múltiplos nos EUA avançaram na Q1, Europa e Ásia-Pacífico registraram queda. Curiosamente, os índices acionários dessas regiões seguiram quase em sintonia, indicando que o mercado aposta na resiliência americana frente à guerra tarifária.

Surpresa? Nem tanto. Os dados parecem mostrar “mais do mesmo”, e isso está começando a ser preocupante

Se 2025 tivesse um resumo, seria uma “imprevisibilidade previsível”. Como esperado, o ano começou com otimismo cauteloso, mas tensões geopolíticas, juros contrários e incertezas regulatórias abalaram o mercado rapidamente. Os negócios seguem, mas com menos transações (-9% vs 2024) e valores maiores (+15%).

Começamos o ano falando sobre essa lógica de menos deals e tickets mais altos, e conforme a Q3 avança, parece que estamos ficando monotemáticos.

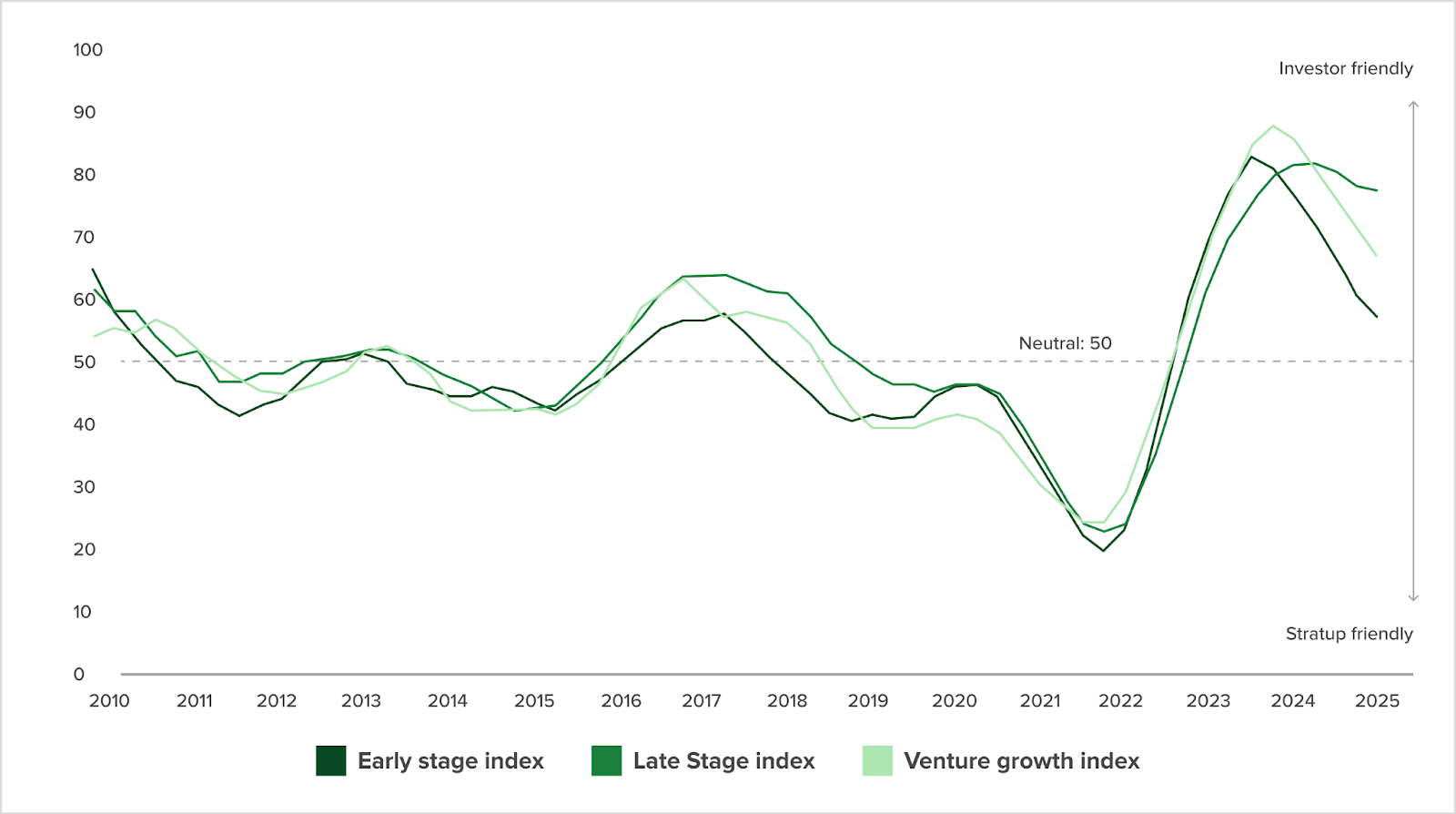

Como vimos na Edição #88, o middle market é quem mais sofre: empresas médias lutam para justificar preços pré-2023 e precisam escolher entre ajustar expectativas ou esperar na arquibancada. O VC Dealmaking Indicator, do Pitchbook, montou um frame de como está o cenário para o Venture Capital em âmbito global: ele parece estar mais favorável aos investidores, mas não sem ressalvas.

Early e Late Stage continuam sendo os mais visados, e isso já nos aponta para como realmente está o clima do mercado.

- Quando falamos de retornos, eles estão mais claros para os negócios que envolvem cheques menores em empresas que ainda possuem bastante terreno livre para conquistar.

- Por mais que essa cautela seja necessária, garantindo que ainda existam ilhas de capital mesmo em um cenário econômico incerto, não é algo sustentável á longo prazo. Afinal, o que acontece quando esses negócios precisarem escalar e não acharem dinheiro nas Series B em diante?

No caso do middle market, o efeito chega com mais intensidade. Com menos apetite para risco, empresas médias enfrentam dificuldades para justificar preços pré-2023. Ou ajustam suas expectativas, ou ficam no banco de espera.

Setores em choque: quem cresce e quem afunda no turbilhão das tarifas

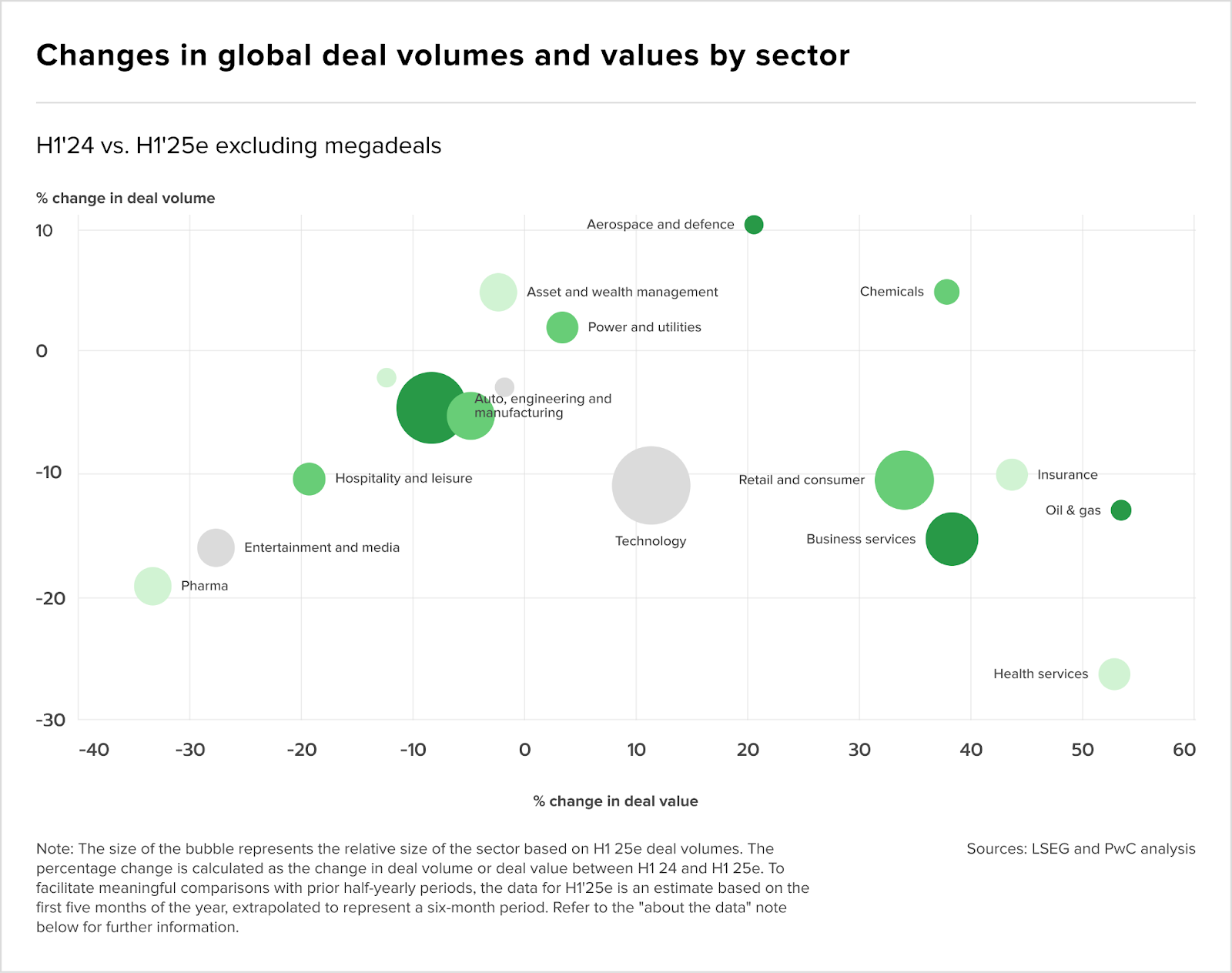

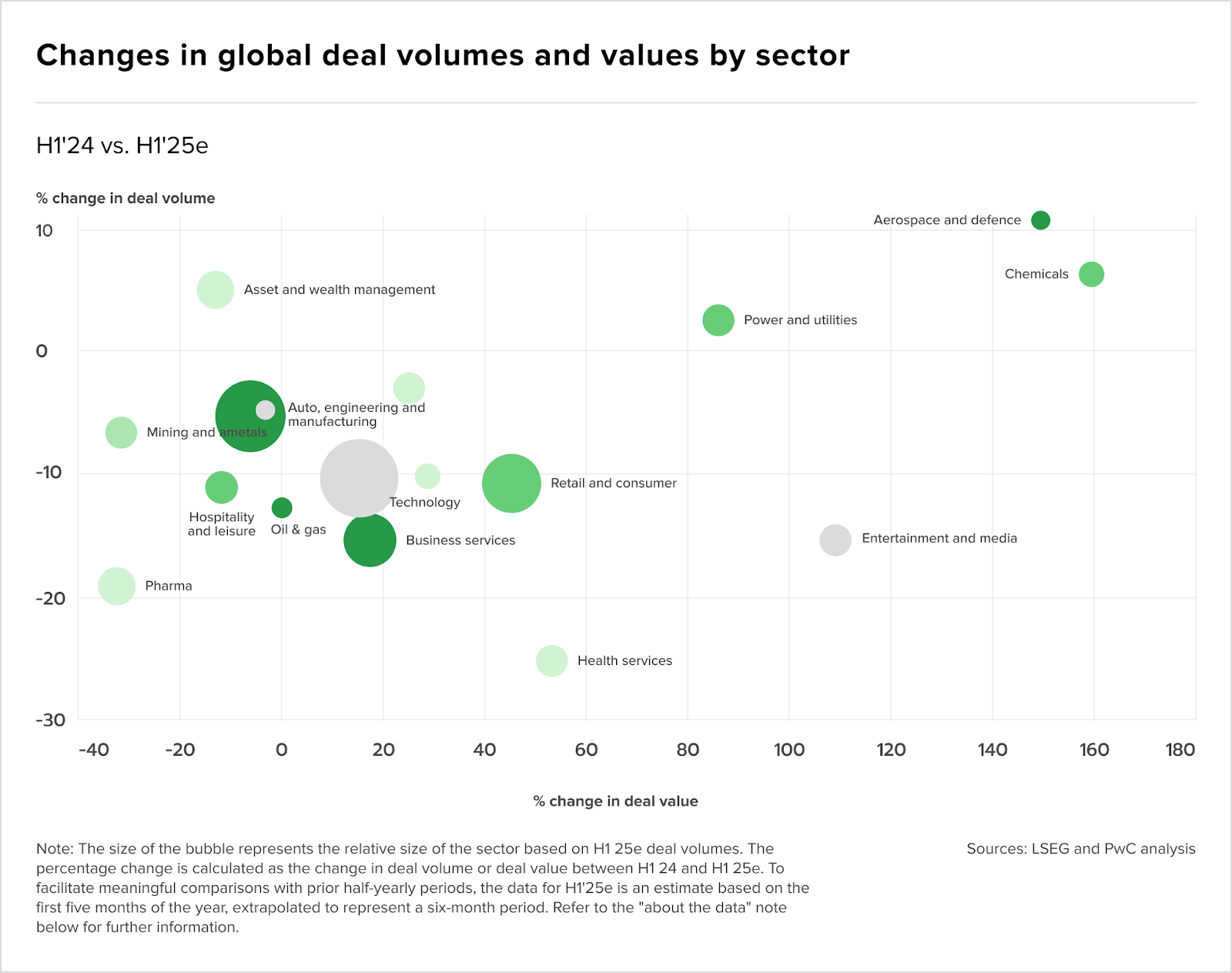

As tarifas, mudanças políticas e incertezas regulatórias têm impacto desigual entre setores. Aeroespacial, defesa, químicos, gestão de ativos e energia cresceram em volume e valor, atraindo investidores. Em contrapartida, varejo, farmacêutico, automotivo e indústria pesada recuaram.

Tarifas são um fator-chave, mas não o único.

- Automotivo, Manufatura e Pharma enfrentam barreiras comerciais e desafios regulatórios, tornando os negócios mais cautelosos;

- Defesa se fortalece com orçamentos maiores;

- Setores de serviços (TI, consultoria, gestão) negociam a múltiplos elevados, apoiados por modelos leves e caixa previsível.

Nos megadeals, o diferencial entre grandes operações (>US$1 bi) e o mercado geral desapareceu desde 2023, refletindo maior exposição tarifária e expectativas de crescimento moderadas, alinhadas ao cenário cauteloso.

Nossa avaliação? Com a aproximação do período de eleição presidencial no Brasil e o tom, que continua elevado nos corredores internacionais, a expectativa é que a pressão no M&A continue consistente.

Enquanto uns torcem por mudanças de ventos, vale uma atenção especial pro middle market. Na sede por capital competitivo, vale avaliar se as transações represadas no mercado vão achar vazão em negócios ou se vão voltar para nos assombrar nos próximos períodos. Um lembrete silencioso daquilo que poderíamos ter sido.

Novas captações

- TRXF11 levanta BRLm 1,3 na 11ª emissão, 125% acima da meta, e se consolida entre os 5 maiores FIIs de tijolo do IFIX

- O GGRC11 captou BRLm 341,5 em sua 9ª emissão, elevando a PL a BRLm 1,7 bi e reduzindo a alcancagem para ~14%. Agora, fundo mira novas aquisições até o fim de 2025

- A JiveMauá captou BRLm 1,2 para um fundo de galpões logísticos

Deu o que falar…

- Na briga que tomou a Azzas 2154, a queda de braço Alexandre Birman e Roberto Jatahy cobrou seu preço. Até o momento, integrações e sinergias foram prejudicadas e a ação da empresa já caiu 60% em um ano.

- A última reunião do conselho do GPA terminou em briga. Quatro conselheiros reclamaram na CVM, alegando remunerações diferenciadas entre membros e irregularidades no registro de ata.

- Há 11 anos o Cade afirma que a participação da CSN na Usiminas é prejudicial à concorrência, e parece que agora eles perderam a paciência. O órgão deu 60 dias para a CSN apresentar um plano de venda das ações.

- Depois de ter 3 pedidos de recuperação judicial negados, o controle do Grupo Safras passa para fundo da AM Agro. A do grupo chega até BRL 2,2 bi.

- Grupo Santa Fé anuncia recuperação extrajudicial e prorroga dívidas por até dez anos – o acordo foi fechado com BRLm 191,2 em dívidas.

Market Trends

Gargalos de Transmissão: O novo filtro de valor para M&A em renováveis

Prepare-se: cortes de geração renovável (o temido “curtailment”) devem crescer até 300% no Brasil até 2035, atingindo 8% da energia gerada e até 11% no Nordeste, epicentro da expansão solar e eólica.

O sonho de crescimento ilimitado das renováveis agora esbarra em gargalos crônicos de transmissão: mesmo com 76 GW de nova capacidade previstos, a infraestrutura não acompanha, e grandes linhas como o bipolo Graça Aranha–Silvânia não serão suficientes para evitar perdas crescentes de receita e projetos represados.

O investidor atento deve ler o sinal: o risco de desvalorização de ativos renováveis aumenta. Mas há oportunidades: se abre uma janela estratégica para M&A. Ativos resilientes, com contratos robustos e menor exposição ao curtailment, tendem a ser disputados; já projetos vulneráveis podem ser adquiridos com desconto, impulsionando movimentos de consolidação e reestruturação de portfólios.

A insuficiência na transmissão é hoje um dos maiores catalisadores de oportunidades (e riscos) para M&A no setor energético brasileiro. Mapear gargalos, antecipar regulações e apostar em inovação será decisivo para capturar valor em um mercado cada vez mais dinâmico e competitivo.

Agronegócio sob pressão: recorde de recuperações judiciais e crédito sustentável ainda tímido

O agronegócio brasileiro encerrou 2024 com um salto preocupante nos pedidos de recuperação judicial: foram 1.272 solicitações, mais que o dobro do registrado em 2023.

O avanço foi puxado por produtores rurais pessoa física, que viram os pedidos saltarem quase 350% em meio à alta dos juros, custos de insumos pressionados por inflação e câmbio, além de adversidades climáticas. O último trimestre do ano confirmou a tendência, com 320 novas solicitações e sinal de represamento de demandas.

Apesar do volume recorde, o número absoluto ainda é pequeno frente ao universo de 1,4 milhão de produtores que acessaram crédito rural nos últimos dois anos.

Enquanto isso, o crédito sustentável avança a passos lentos: descontos em juros para práticas ESG atingiram apenas 0,45% dos desembolsos do Plano Safra 24/25, travados por entraves regulatórios e baixa adesão. O desafio para 2025 é claro: alinhar gestão de risco, inovação em crédito e incentivo real à sustentabilidade para destravar valor no agro brasileiro.

Fonte: Serasa e Globo Rural

AI domina venture debt e investimentos, mas uso corporativo ainda é tímido

Startups de IA e ML já capturaram 38,4% dos USD 30 b em venture debt nos EUA e Europa em 2025, impulsionadas por custos crescentes de infraestrutura e pressão para manter valuations elevados. O setor de venture debt bateu recorde de USD 53,3 bi em 2024, com destaque para grandes rodadas lastreadas em ativos como GPUs, refletindo a corrida por capacidade computacional. O apetite por risco é notável: mesmo startups sem receita estável conseguem crédito relevante, embora haja alerta sobre a rápida depreciação desses ativos.

No Brasil, IA generativa já está presente em 80% das médias e grandes empresas, mas 75% ainda utilizam a tecnologia de forma incipiente. A prioridade estratégica cresce: 67% das companhias brasileiras já colocam IA entre as cinco maiores prioridades para 2025 e 17% têm IA como principal destino de investimentos, com ganhos médios de 14% em produtividade e 9% em resultados financeiros.