In the ever-evolving landscape of venture capital (VC), it is crucial to understand the current trends and dynamics of capital allocations.

Q1 of 2023 saw a general improvement by 37% over Q4 of 2022 in terms of VC investment, rising to $44.1 billion compared to $32.3 billion for Q4 2022. However, Q1 of 2023 has also confirmed:

- The high volatility of the market

- The weaker conditions of the economic environment (until March 2023 there were three major bank failures)

- The existence of macroeconomic patterns following unpredictable paths influenced by global geopolitical changes, like the war in Ukraine.

In the light of this, it is interesting to ask what are the recent shifts in VC investments happening, who are the key players and which factors are influencing their decision-making?

James Heath, Investment Principle at dara5, analyzes the VC scenario, focusing specifically on who, at the moment, has opted for allocating capital to VC and also who has not.

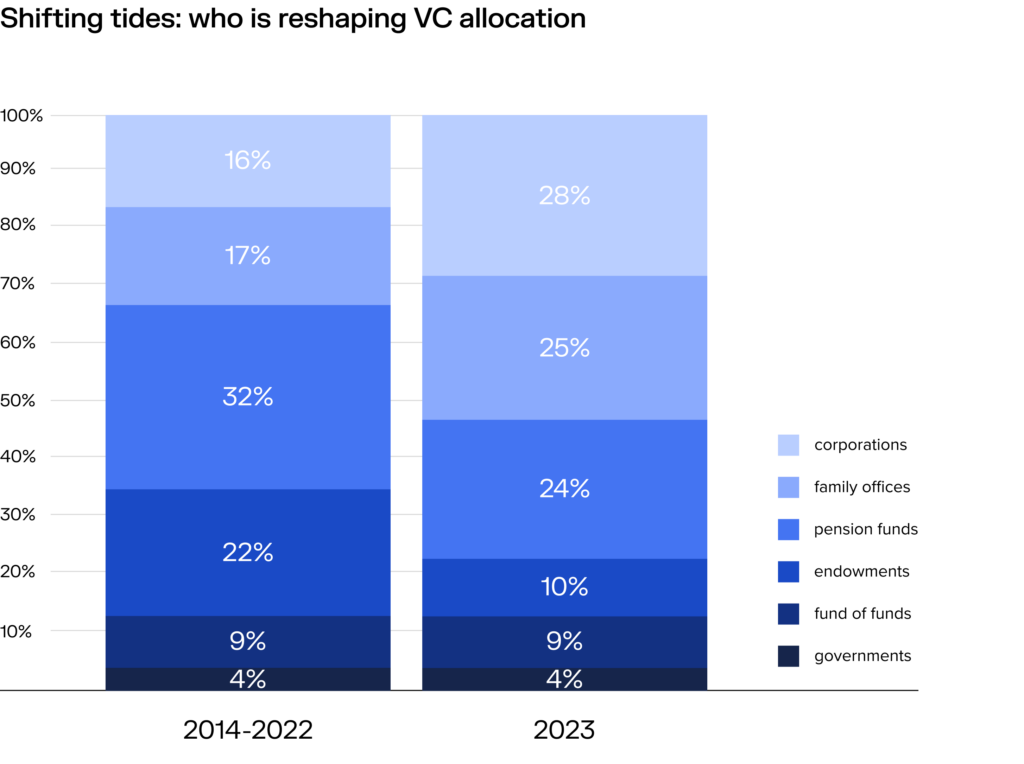

The VC scenario

Drawing upon a comprehensive analysis of over 10,000 limited partner (LP) commitments to VC in Europe and the U.S. from PitchBook Data, this is the current VC scenario.

Decreased commitments in 2023

2023 has witnessed a significant decline in VC commitments, with nearly 70% fewer investments compared to the average of the previous decade. This sharp reduction in allocations has raised concerns and prompted a closer examination of the factors influencing LPs’ decision-making processes.

Pension funds and endowments

Notably, pension funds and endowments, traditionally significant contributors to VC funding, have been allocating less capital in recent times. This trend may be attributed to two key factors:

- First. These institutional investors may have over-allocated their funds in 2021, prompting a more cautious approach in subsequent years

- Second. Underperformance in the public markets has adversely impacted their risk appetite and overall investment strategies.

Rise in family offices and corporations

Conversely, family offices (FOs) and corporations have emerged as increasingly prominent participants in the VC ecosystem. FOs and corporations with sufficient liquidity are capitalizing on the opportunities presented by exceptional vintage years for investments. It is important to note that FOs tend to exhibit a binary approach, either actively investing or refraining from VC allocations altogether.

Fund of funds

Special attention must be paid to the role of fund of funds (FoFs) in the current landscape. FoFs that possess deployable capital are proving to be excellent allocators of funds. However, caution is advised when evaluating FoFs, as some may obscure their inability to deploy capital effectively while simultaneously raising new funds. Thorough due diligence is imperative to ensure a productive partnership.

Acknowledging successful fund closures

In light of the prevailing market conditions, it is essential to recognize the accomplishments of those currently achieving successful fund closures. Despite the wider market activity and reduced commitments, reaching closure on a fund is a noteworthy achievement that merits commendation.

Looking ahead

The VC scenario for 2023 is far from being written in stone. There are at play many factors that will contribute to its definition, such as:

- High inflation

In most economies, inflation will end the year above target. According to the Department of Economic and Social Affairs of the United Nations, the global inflation is expected to decline from 7.5% in 2022 to 5.2% in 2023.

- Central banks

Will central banks abandon their tightening cycles as an answer to the financial stability risk increase or will they keep policy tight to lean against inflationary pressures?

- Sustainability and ESG

In Q3 2023, trends reveal that VCs will be increasingly focused on sustainability, renewable energies, and ethical growth.

- Recession risk

According to the IMF, the forecast global growth is expected to slow to 3.2% in 2022 and 2.7% in 2023 from 6.0% in 2021. This represents the weakest growth profile since 2001, except for the global financial crisis and the acute phase of the COVID-19 pandemic.

Given all that, it is very likely that VC will maintain a prudent and more selective attitude at least in the immediate future and it is not improbable that the VC investment in general will drop off from the levels seen in 2021 and 2022. This will clearly have a profound impact, for example, on the startups scenario and also on the timing of new deals closing, making it longer.

Follow us on our social media channels and on the M&A Community webpage to stay up to date about VC trends and much more.