Sebastian Montoya

Sebastian Montoya

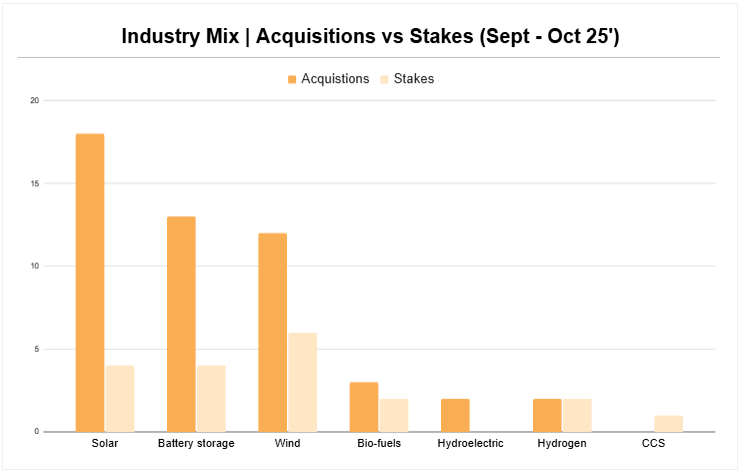

In the past two months, Europe’s M&A in renewables has largely been at the asset-level: full buyouts of specific projects and partial stake sales in project SPVs, while company-level acquisitions remain subdued.

Our analysis zooms in on that shift: since September through the first week of November we count 51 full project acquisitions versus 22 stake sales, with BESS/solar skewing to outright takeovers and offshore portfolios leaning on farm-downs/JVs.

We also bring the highlights of this week’s renewable energy M&A in Europe:

- Storage steps into giga-scale. Germany’s Green Flexibility and Hansa framework adds 500 MW of BESS across multiple sites, while Augwind enters Europe buying 509 MW (up to 4 GWh) in Brindisi for €230m. On the behind-the-meter edge, Enercity and HANOVOLT tie rooftop PV to smart storage in northern Germany.

- Molecules go modular. CIP buys Ørsted’s Northwich biogas plant with upgrades for biomethane and CO₂ capture by 2028. Also, EDL adds GWE Biogas and Estonia’s Infortar takes 60% of Oisu Biogaas.

- Wind splits by scale. Mega-offshore needs JV capital, and Apollo partners with Ørsted in a $6.5bn deal. Kansai sharpens pipelines by investing in Simply Blue. Onshore Germany mixes RTB and operational churn with a Engie’s 212 MW deal;

Connect with me on LinkedIn for more backstage insights from the sector.

Hispanics in London: M&A Cocktails & connections

M&A Community is delighted to invite you to an exclusive networking event dedicated to Spanish-speaking professionals in the City on November 19

Join us at the Black Lacquer: a stylish, intimate speakeasy nestled beneath the Hyde London City hotel, for an evening of crafted cocktails and high-level conversation. Spaces are limited.

Deals breakdown

Project acquisitions vs stake sales in energy M&A Europe

The purchase of specific projects (such as hydrogen facilities, BESS platforms and PV plants) has been a recurring theme in our curation over the past two months. Between September and the first week of November 2025, this type of transaction was prevalent across the market, especially when compared with company-level acquisitions.

Counting only confirmed transactions, we identified 51 asset-level full acquisitions and 22 stake sales.

We’ve covered some of these cases here in Teaser Energy Europe. In this edition, it’s worth stepping back to the wider picture to examine a few catalysts that help explain how these deals are being structured.

Stakes to scale: Partnerships, asset rotation and shared risk in European energy M&A

Scaling while sharing risk is among the key drivers behind stake negotiations. European utilities are using partnerships and asset rotation both to recycle capital and to split capex and accelerate timelines without losing operational control.

- Iberdrola has codified this approach: partnering with tier-1 players, reducing exposure and rotating assets as value levers. Aligned with this minority-stake strategy, a recent example was when the company partnered with NBIM to sell 49% of Iberian solar and wind portfolios.

- And Iberdrola isn’t alone: since 2024, farm-downs and JVs have become a sector standard across leading players such as TotalEnergies.

Offshore wind, as we’ve discussed previously, is the epicentre of this “stake-to-scale” model. The most recent example is Ørsted selling 50% of Hornsea 3 to Apollo for $6.5 billion. As Adam Petrie, Partner at Apollo Infrastructure, noted: “through this investment, we are proud to deliver a scaled and comprehensive solution for infrastructure that will promote energy security and the UK’s net-zero ambitions.”

Why full takeovers are winning in BESS and solar

The appeal of stake deals only gives way when there’s a chance to hold 100% control of an asset. BESS has become a classic target for those outright acquisitions, and the rationale neatly captures why this approach matters within European energy M&A.

- In the previous edition, we saw Cero Generation acquire a 100 MW battery-storage system in Gloucestershire, England.

- Cero’s CEO, Declan Deasy, highlighted this broader impact: “This acquisition demonstrates our continued investment in the UK’s renewable infrastructure, delivering further benefits for the UK’s energy system, communities and environment.”

These movements are also strong in solar, where these deals help consolidate pipelines. Risk reduction remains a priority, but it is achieved differently: assurance via end-to-end control, from generation through to dispatch.

Battery storage

- Germany | green flexibility and Hansa Battery Sign Framework Agreement for 500 MW of Large-Scale Battery Projects Across Multiple Sites, Combining Development and Operational Expertise to Accelerate Grid-Connected Energy Storage Deployment Nationwide

- Italy | Augwind Enters European Market with Acquisition of 509 MW / Up to 4 GWh Battery Energy Storage Project in Brindisi for €230 Million in Partnership with B7 Energy, Marking First Step in New Strategy to Become Leading Pan-European Storage Developer

Bio-fuels

- Estonia | Infortar Subsidiary OÜ Infortar Agro Acquires 60% Stake in OÜ Oisu Biogaas from Eesti Biogaas, Strengthening Integrated Agricultural and Biomethane Operations Linked to Recently Acquired Estonia Farmid and Expanding Infortar’s Domestic Renewable Energy Footprint

- Germany | Rheinmetall Launches ‘Giga PtX’ Consortium with Sunfire, Greenlyte, and INERATEC to Develop Network of Modular E-Fuel Plants Producing 5,000–7,000 Tonnes Annually, Enabling European Armed Forces to Locally Synthesize Green Diesel, Kerosene, and Marine Fuels for Energy Security and Resilience

- United Kingdom | Copenhagen Infrastructure Partners Enters UK Bioenergy Market with Acquisition of Northwich Biogas Plant from Ørsted via Advanced Bioenergy Fund I, Planning 2026 Refurbishment to Add New Digester, Biomethane Upgrading, and CO₂ Capture for 2028 Operations

- United Kingdom | EDL Energy Acquires GWE Biogas and Its Sandhill Biogas Plant in East Yorkshire, Adding 4.5 MW CHP and 750 m³/h Biomethane Capacity, Expanding UK Portfolio to 10 Sites and Strengthening Circular Economy Capabilities in Renewable Gas and Waste-to-Energy

Hydrogen

- Austria | Masdar Acquires 49% Stake in OMV’s €300M+ 140 MW Green Hydrogen Project in Bruck an der Leitha, Marking UAE’s First Clean Energy Investment in Austria and Advancing EU-Gulf Partnership to Produce 23,000 Tonnes of Hydrogen Annually by 2027

- Poland | Rockfin Partners with France’s Elogen to Integrate PEM Electrolyser Stacks into HyVentive Hydrogen Systems, Delivering Turnkey Green Hydrogen Solutions Across Europe, the Middle East, and Africa to Accelerate Clean Hydrogen Deployment

Solar

- Spain | Grenergy Completes €273 Million Sale of 297 MW Solar Portfolio (Tabernas 250 MW, Jose Cabrera 47 MW) to Allianz Entities, Generating €75 Million Capital Gain and Advancing Asset Rotation Strategy Toward Storage and Solar-Plus-Storage Projects

- United Kingdom | BOOM Power Sells 114 MW Portfolio Comprising Firsfield (71 MWp) and Osgodby (43 MWp) Solar Farms to Enray Power, Advancing UK Net-Zero Goals and Showcasing Design-Led, Biodiversity-Positive Development Across Suffolk and North Yorkshire

Solar + BESS

- Germany | enercity Acquires Stake in PV Specialist HANOVOLT to Form Strategic Partnership for Rooftop Solar and Smart Storage Expansion Across Northern Germany, Targeting Growth in Residential Energy Solutions and Supporting Grid-Integrated Renewable Adoption

- Spain | Brookfield Renewable Prepares Sale of Majority Stake in Solar and Storage Platform X-Elio Valued Above €2 Billion, Hiring Santander and Barclays to Lead Process Expected in Early 2026 After Full Ownership Consolidation from KKR in 2023

Wind

- Germany | ENGIE Acquires 212 MW Ready-to-Build Wind Farm in Bad Berleburg from WestfalenWIND, Doubling Its Onshore Wind Portfolio and Advancing Growth Strategy in Renewables and Storage Through Repowering, Greenfield Development, and Targeted Acquisitions

- Germany | Tion Renewables Acquires 30 MW Operational Onshore Wind Portfolio from Alterric, Including Four Sites Across Baden-Württemberg, North Rhine-Westphalia, Lower Saxony, and Hesse, Strengthening Its German Footprint and Advancing 3 GW Growth Target by 2030

- Ireland | Kansai Electric Power Co. Makes Strategic Investment in Simply Blue Group’s Offshore Wind Arm, Simply Blue Energy OSW Ltd., Marking KEPCO’s First Management-Participating Offshore Wind Partnership to Accelerate Global Portfolio Expansion and Advance Zero-Carbon Goals

- Netherlands | Eneco Acquires Prowind’s Dutch Wind Project Development Business, Adding 260 MW Pipeline and Six-Person Team to Expand National Onshore Wind Portfolio While Prowind Refocuses on Rapidly Growing German Market

- United Kingdom | Apollo Funds Invest $6.5 Billion for 50% Stake in Ørsted’s 2.9 GW Hornsea 3 Offshore Wind Farm, Forming Joint Venture for World’s Largest Project and Providing Long-Term Capital to Power Over 3 Million Homes and Advance UK Net-Zero Goals

- United Kingdom | Qair Acquires Full Ownership of 1 GW Ayre Floating Offshore Wind Farm in ScotWind Round, While Exiting Bowdun Project Transferred to DEME and Aspiravi, Streamlining Partnership Structure and Reinforcing Commitment to Scotland’s Offshore Wind Ambitions