The valuation of equity interests in private companies, especially those with significant leverage, presents many challenges and intricacies.

A detailed case study, in line with the Financial Accounting Standards Board (FASB) and Accounting Standards Codification (ASC) 820, sheds light on these complexities, offering key insights for valuation practitioners.

The case study, or example, provides a clear illustration of the impact of change in control provisions and the importance of considering the time horizon and investment strategies in valuation.

Framework for equity valuation in leveraged: 9 key considerations

- Fair value measurement and market participant perspective: Central to the valuation process is the measurement of fair value from a market participant’s perspective. This involves estimating the price at which knowledgeable and willing parties would agree to transact, ensuring that both buyer and seller act in their economic best interests and possess complete information about the asset.

- Complexity in valuation of leveraged companies:The valuation intricacies of companies with a mix of debt and equity are highlighted. It’s crucial to consider both the rights and obligations of debt and equity holders, inclusive of any specific terms such as change in control provisions.

- Impact of change in control provisions: There are significant effects of change in control provisions in debt agreements on equity fair value. These provisions, often entailing prepayment penalties, can diminish the net sale proceeds, thereby influencing equity valuation.

- Time horizon and investment strategy considerations: The expected duration of equity holding and the associated strategies play a pivotal role in valuation and can considerably sway the value of the investment.

- Calibration to transaction price and subsequent adjustments: Valuations commence by calibrating to the initial transaction price, followed by adjustments in later periods to mirror changes in expected cash flows and market conditions. This method ensures that valuations stay attuned to market dynamics.

- Diverse valuation approaches and scenarios: There are many valuation methodologies, including direct cash flow assessments and indirect approaches like adjusting enterprise value for debt. There is also the need to explore different scenarios, such as immediate sale versus longer-term holding, each leading to distinct fair value estimations.

- Incorporation of market liquidity and risks: The liquidity of the equity position and associated investment risks, both market-related and specific to the company, are essential in the valuation. They influence the required return rate and, by extension, the valuation.

- Probability-weighted scenarios in uncertain conditions: In cases with regulatory or financing uncertainties, the use of probability-weighted scenarios is demonstrated. This method considers the likelihood of various outcomes and their impact on valuation.

- Bid-ask spread and fair value determination: The concept of bid-ask spread is employed to show the range in which fair value might reasonably fall. The selected fair value should represent the most realistic value within this range, considering current market conditions and inherent uncertainties.

Case study – 100% of equity held within a single fund (single reporting entity)

This breakdown explains the process and considerations the fund goes through in valuing the company’s shares they purchased, considering the market conditions and specific terms of the deal.

The context

- December 31, 2019 Purchase Details:

A fund buys all (100%) of a company’s shares. The total value of the company (called “enterprise value”) is $500 million. This $500 million is made up of $200 million from shares (equity) and $300 million borrowed from others (third-party debt). The borrowed $300 million must be paid back in 5 years. If the company is sold within these 5 years, the debt must be paid back with extra charges: 10% more in the first year, 5% more in the second year, 3% more in the third year, 1% more in the fourth year, and no extra charge in the fifth year. - What is being valued (unit of account) and assumed future sale: The focus is on the value of the shares the fund owns (100% equity). It’s assumed that these shares might be sold to someone else in the future, based on what a typical buyer or seller would pay under normal market conditions.

- How the fair value is determined: The fair value (the price that would be agreed upon in a normal sale) is based on what’s expected under usual market conditions at the time of valuing. This value isn’t based on a rushed sale, selling during tough times, or when the company is in trouble.

- Checking if the purchase price was fair: Next, it’s checked whether the $500 million paid was a fair price. This involves three parts:

- The company was bought for $500 million

- $200 million was for buying all shares,

- $300 million was for taking on the company’s debt.

To see if this was fair, they checked: Was it not a deal between family or friends? Was the deal not forced? Does the $200 million for shares match with the value of all shares the fund now owns? Was this the usual kind of deal in the private equity market?

- Confirming fair value and using market assumptions: The fund concluded the $200 million was a fair price for the shares. When deciding the value of these shares, they consider what typical buyers and sellers in the market would think, not just what the company believes. If there’s better information available, they would use that to adjust their assumptions.

Valuation models alignments

In summary, the passage explains how the fund adjusts the valuation model for their investment to match the price they paid and how they regularly update this model. It also describes how the fund considers the viewpoints of other potential investors, especially concerning the debt and its terms, to ensure the valuation aligns with their initial strategy and expectations.

Ramifications of a change in control on the measurement date

- “Day 1” Sale impact: If the investment (the company bought by the fund) is sold immediately after purchase, it activates the ‘change in control’ clause in the debt agreement.

- Change in control provision: This clause includes a prepayment penalty, which is an extra cost for paying off the debt early.

- Financial consequence: The prepayment penalty increases the debt repayment amount. For example, if the company is sold right away, the debt repayment would be $330 million instead of the original $300 million because of a 10% penalty.

- Effect on equity value: This increased debt repayment reduces the money that would go to the equity holders (the fund in this case). So, instead of getting more money, the equity holders end up with $170 million.

- Inconsistency with initial assumptions: This outcome doesn’t match what was initially expected when the company was bought, as it goes against the usual thinking of market participants, who usually aim to avoid immediate losses.

Expected time horizon for the investment on the measurement date

- Measuring equity value: When determining the value of the equity interest, it’s assumed that other investors (market participants) would think about how long they plan to keep the investment.

- Day 1 Fair value determination: If we consider selling the equity right after buying it, its value is thought to be $200 million. This value includes the effects of the change in control provisions.

- Knowledge of change in control provisions: Both the equity and debt investors knew about these change in control conditions when they decided on the price for the equity ($200 million) and the debt ($300 million). Therefore, this $200 million value already considers what other investors would think about the chances and timing of a change in control and what return they would expect from this investment.

- Overall deal context: Typically, investors agree to such a change in control conditions as part of a larger negotiation, which also involves discussing other terms like the interest rate on the debt, how much debt is allowed, and various rules or restrictions (covenants).

Summary in numbers

- Total Enterprise Value: $500 million

- Value of Debt (for calculating equity value): $300 million

- Fair Value of Equity: $200 million

In simple terms, this part of the passage explains the financial effects of selling the company immediately after buying it, especially due to the extra costs from the change in control clause in the debt agreement. It also describes how the value of the equity is calculated, considering the expectations and knowledge of investors about the future of the company and the terms of the deal.

Calibration

Valuation model adjustment: The value of the investment (the company bought by the fund) needs to be adjusted or ‘calibrated’ to match the price paid for it.

Using the income approach

- Estimating cash flows: The fund predicts how much money the investment will make in the future while they own it.

- Determining rate of return: They figure out the rate of return they expect to get from this investment, starting from the day they bought it.

- Regular updates: This calculation isn’t done just once. As time goes on, the fund updates their predictions about future cash flows and the return they expect, based on what’s happening in the market.

- Market approach consideration: This kind of thinking (looking at future money made and required returns) is also used in other valuation methods, like the market approach.

Analogous situations

Comparison with other dituations:

- Change of Control Provision: The way the fund thinks about the ‘change of control’ clause in the debt (extra costs if the company is sold) is similar to how they would consider other kinds of restrictions or limitations.

Measuring debt value for equity valuation:

- Considering market participant views: When figuring out the value of the equity (the part of the company the fund owns), they also look at the debt’s value from the viewpoint of other potential investors or market participants.

- Expectations and timing: This includes thinking about how likely and when a change of control might happen, and what kind of return these other investors would want considering these conditions.

- Consistency with original transaction: This method of estimating the equity’s value is in line with the original plan and the interests of the fund when they first bought the company.

Situation two years later

After two years, the company faces significant problems.

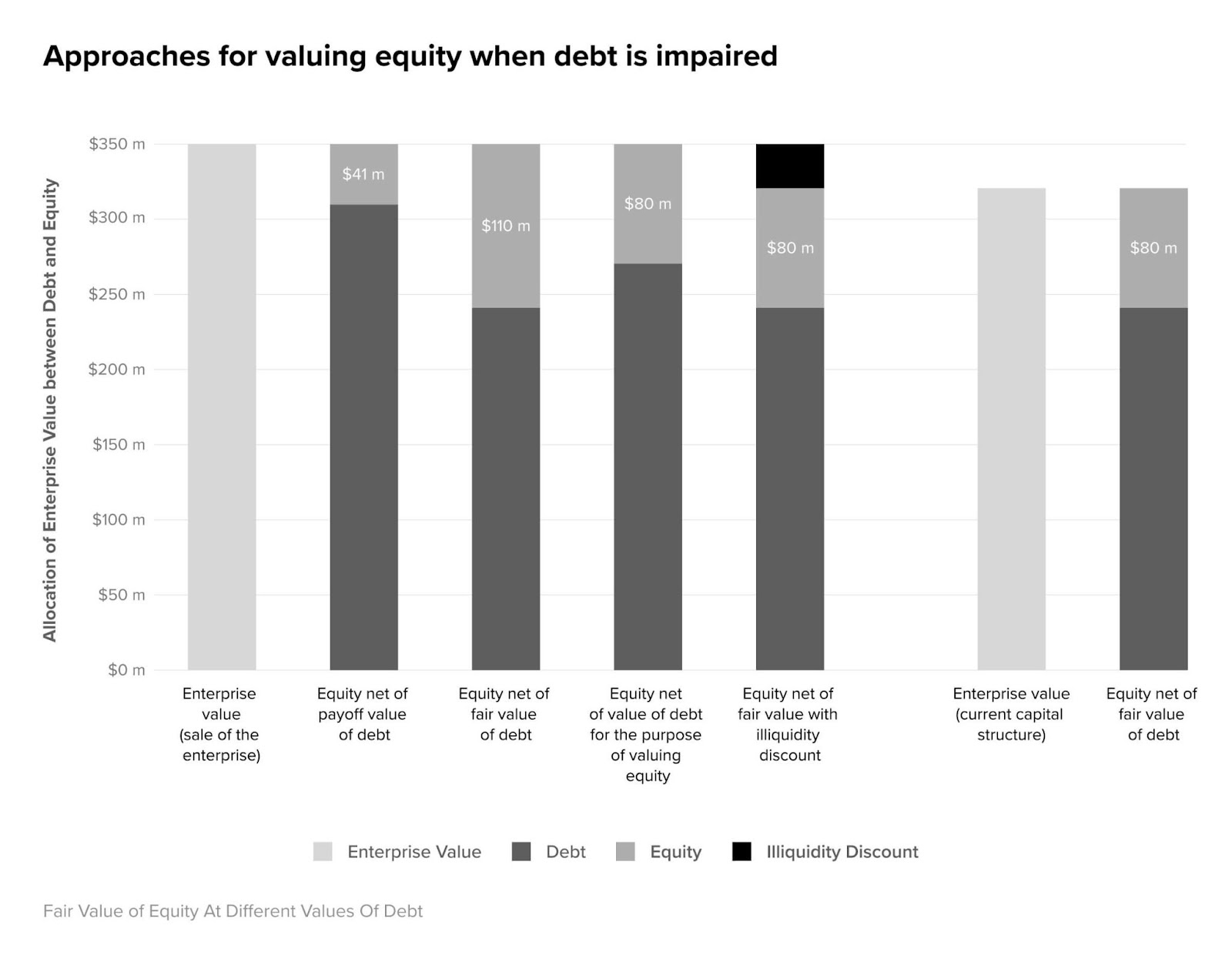

- Debt payoff value: The value needed to pay off the debt has increased to 103% of the original amount, which means paying off the debt would now cost $309 million.

- Fair value of debt: The market value of the debt is now lower, at 80% of the original amount, or $240 million. This is based on how much the debt would sell for in the market, considering the expected cash flows from the debt and the current interest rates.

- Enterprise value: The total value of the company, if sold now, is estimated at $350 million. This considers the cost of capital for a new buyer who might use different debt.

- Equity value: The value of the company’s equity is calculated to be $80 million. This takes into account the cash flows that would go to equity holders and the required return on equity in the current market conditions.

- Comparison of equity value: This $80 million is more than what would be left after selling the company and paying off the debt at $309 million, but less than the total value if a new buyer could benefit from the existing debt conditions.

Considerations for valuing the equity

- Focus on equity enterest: The main focus is on the value of the equity interest held by the fund.

- Assumed sale to market participant: It’s assumed that the equity would be sold to another investor who would keep it for a while, based on what such investors typically expect and would pay for it.

- Fair value measurement: The value is based on a hypothetical orderly sale, not in a forced or distressed situation. This valuation considers the current market conditions, the investment risks, and how easy it would be to sell the investment.

Change of control feature and fair value—Detailed analysis:

- Expectations of market participants: The value of the change of control feature in the debt (the extra cost for early repayment) depends on whether investors think the company will change ownership soon or closer to when the debt is due.

- Valuation model calibration: Initially, models were used to figure out what returns investors would want, considering the chances and timing of early debt payoff. Over time, these models are adjusted to reflect changes in what investors expect regarding a change of control.

- Differing assumptions for equity and debt: Investors in equity might think differently about the value of the company and the debt compared to those who are just looking at buying or selling the debt. This means the value of the debt when estimating equity value might be different from its standalone market value.

Ramifications of a change in control on the measurement date

- Triggering change in control provision: If the investment (the company bought by the fund) is actually sold, a special rule in the debt contract (change in control provision) gets activated.

- Effect of change in control provision: This rule means that if the company is sold, the debt must be paid back at a higher amount than its current worth (a premium), which would reduce the money received by the equity holders (the fund).

- Immediate loss for equity holders: This situation would result in the equity holders getting less money than they would if they held on to the investment for the planned time, leading to an immediate loss.

Expected time horizon for the investment on the measurement date

- Fair value measurement based on time horizon: The fair value of the equity interest (how much the equity is worth) is estimated by considering how long the fund plans to keep the investment.

- Income approach for valuation: Under this method, the fund thinks about the money it expects to make from the investment (cash flows) until it decides to sell (liquidity event). The fund uses this information to adjust (calibrate) its model for calculating the investment’s worth, based on the initial purchase price and any changes in value up to the current date.

Calibration – Cash flows to equity

- Valuation on December 31, 2021: On this date, the fund updates its expectations about future profits from the investment (expected cash flows) and considers how much return investors would now require, given the current market conditions.

- Determining fair value of equity: Based on this updated information, the fair value of the equity interest is calculated to be $80 million. This value assumes that if the equity were to be sold to another investor, they would expect to get value from the investment over the time they plan to hold it.

- Factors included in valuation: This $80 million valuation takes into account the profits the company is expected to generate in the future and the return that investors would demand in the current market situation.

In summary, the passage explains how the sale of the investment can trigger specific provisions that affect its value, how the investment’s value is calculated based on how long it will be held, and how the fund updates its valuation over time, considering expected future profits and current market conditions.

Calibration – Net equity value (contractual debt payoff)

- Debt repayment at contractual value: The debt holders can be paid back $309 million as per their agreement. This is the amount they are owed.

- Selling the company and paying off debt: If the company is sold on the valuation date, the debt would be paid off at this $309 million amount.

- Resulting equity value: After paying off the debt, the value of the company’s equity (the part owned by investors like the fund) would be $41 million.

- Inconsistency with market participant assumptions: However, selling the company immediately and paying off the debt like this might not align with what typical investors (market participants) would do. They usually wouldn’t sell the asset right away if it meant getting less value.

- Lower bound of equity value: So, this $41 million can be seen as the lowest possible value of the equity under these conditions.

- Higher required rate of return: This situation also suggests that the return investors want from this investment, given current market conditions, might be higher than expected. It might be reasonable in some cases to sell earlier for less money if the risk of waiting longer is too high.

Calibration – Net equity value (fair value of debt)

- Valuing the company and subtracting debt: Another way to find the equity’s value is to first calculate the whole company’s value ($350 million) and then subtract the debt’s fair value ($240 million).

- Potential fair value of equity: Using this method, the equity could be worth $110 million if the company were sold on the valuation date and the debt paid off at this lower fair value.

- Upper bound of equity value: However, this $110 million might be the highest possible value of the equity. This is because investors might not want to pay this much due to the equity being less liquid (harder to convert into cash) because of the change in control provision in the debt agreement.

In simple terms, these paragraphs discuss two different ways to calculate the fair value of the company’s equity. One way considers the contractual payoff amount of the debt, leading to a lower equity value. The other way uses the fair value of the debt, resulting in a higher possible equity value. These values represent the lowest and highest potential worth of the equity, considering various market conditions and investor expectations.

Calibration – Net equity value (negotiated debt payoff)

- Negotiating debt payoff: The equity investor (the fund) might talk directly with the people who lent the money (debt holders) to agree on paying back the debt at a price that’s lower than the official amount due but higher than its current market value.

- Benefit of negotiation: This would be good for both the equity investor and the debt holders because they can end the investment earlier than planned.

- Example calculation: Let’s say they agree that the debt will be paid back at $270 million instead of the full $309 million. Then, the value of the equity (what the fund owns) would be calculated as $80 million.

- Estimating values: This method assumes you know the total value of the company ($350 million) and the negotiated debt value ($270 million). The equity value is found by subtracting the debt from the company’s total value.

- Practicality of the approach: It’s often easier to use this method because information about overall costs (like interest rates and returns) is more available than specifics just for the equity.

Calibration – Net equity value (fair value of debt), adjusted for illiquidity

- Adjusting foriIlliquidity: When estimating the equity value, the method first looks at the company’s total value minus the current market value of the debt. However, it then reduces this amount to account for the difficulty in selling the equity quickly (illiquidity).

- Calculation example: The company’s value is $350 million, and the debt’s market value is $240 million. So, the equity value before adjustment is $110 million. But because it’s hard to sell quickly, this might be reduced by $30 million, making the equity worth $80 million.

- Reason for illiquidity discount: This discount is because investors can’t easily get the full value of the company minus the debt unless they keep the investment for a while. They might want a higher return for this risk and difficulty.

Overall Summary

- Different valuation methods: The passage describes various ways to figure out the equity’s fair value, considering how much return investors want and how long they plan to keep the investment.

- Bid and ask price concept: The lowest value (bid price) for the equity might be $41 million (if the debt is paid off fully at $309 million). The highest value (ask price) could be $110 million (based on the company’s total value minus the debt’s market value). The fund chose $80 million as the fair value, which fits within this range and is based on expected profits and required returns.

- Importance of specific transactions: The actual fair value might be more if the fund can negotiate an even better deal for paying off the debt (like paying $265 million instead of $270 million).

- Market conditions and rates of return: The fair value of the debt ($240 million) reflects current interest rates compared to what the company offers. This affects the overall cost of the company and, therefore, the equity’s value.

In summary, the passage explains different ways to calculate how much the equity in a company is worth, considering negotiations, market conditions, and the challenges in selling the equity.

Four years since buying the company:

- Market recovery: Two years after the last valuation (four years since buying the company), the market conditions have improved.

- Sale agreement: The fund has an agreement to sell the company for $800 million, expected to close in three months.

- Chance of deal falling through: There’s a 25% chance the sale won’t happen. If it doesn’t, the company is estimated to be worth $700 million.

- Debt repayment: If sold, the debt would need to be paid off at 101% of its original amount, totaling $303 million. If the sale doesn’t happen, the debt’s fair value would be its original amount, $300 million.

Evaluating the unit of account and the transaction

- Focus on equity interest: The valuation considers the entire equity interest held by the fund.

- Type of transaction considered: The valuation assumes a transfer of the equity interest to someone else, planning to keep it for only three months if the sale happens.

- Prepayment penalty: If the sale happens, the fund must pay a penalty for paying off the debt early, affecting the equity’s value.

Fair value calculation

In summary, this section describes how the fund evaluates the worth of its equity in the company, considering the likelihood of a sale happening soon and its impact on the value of the company and its debt. This calculation takes into account both the increased value if the sale goes through and a lower value if it doesn’t, along with the associated debt in each scenario.

- The valuation looks at two scenarios:

- If the sale happens (for $800 million)

- If it doesn’t (value drops to $700 million)

- Debt value in each scenario: If the sale happens, the debt payoff is $303 million. If not, the debt value is $300 million.

- Equity value calculation:

- If the sale happens, the company’s value ($800 million) minus the debt ($303 million) equals an equity value of $497 million

- If the sale doesn’t happen: The company’s value ($700 million) minus the debt ($300 million) equals an equity value of $400 million

- Probability-weighted value: Since there’s a 75% chance the sale will happen and a 25% chance it won’t, the fair value of the equity is calculated using these probabilities. This results in a weighted value of $464 million.

Conclusion

The journey of understanding the complexities of equity valuation in leveraged, privately held companies underscores several key takeaways for valuation practitioners.

I navigated through the intricate details of fair value measurement, considering market participant perspectives and the nuances of dealing with leveraged companies.

I also delved into the necessity of calibrating the valuation model to the transaction price and adjusting it according to changes in market conditions and expected cash flows. The exploration of different valuation approaches and scenarios highlighted the versatility required in equity valuation. Moreover, the incorporation of market liquidity, risks, and the use of probability-weighted scenarios in uncertain conditions emphasized the depth of analysis needed for accurate valuation.

The bid-ask spread concept served as a reminder of the range within which fair value might lie and the importance of selecting the most representative value in given circumstances.

The insights and methodologies discussed herein equip valuation practitioners with the tools to tackle the challenges inherent in the valuation of leveraged, privately held companies.