When it comes to valuing a business in an acquisition, the seller and the bidders start with very different goals:

- The seller, in most cases, will tend to overvalue their company. They want the deal to go through at the highest price.

- The bidders, in most cases, will tend to undervalue the company. To get their best return on investment out of the deal.

Bringing these two contradictory positions together can be tricky, but it’s doable.

More importantly, how we could get to a mutually acceptable price, i.e: realize the acquisition, by finding the overlapping values both seller and buyer can embrace.

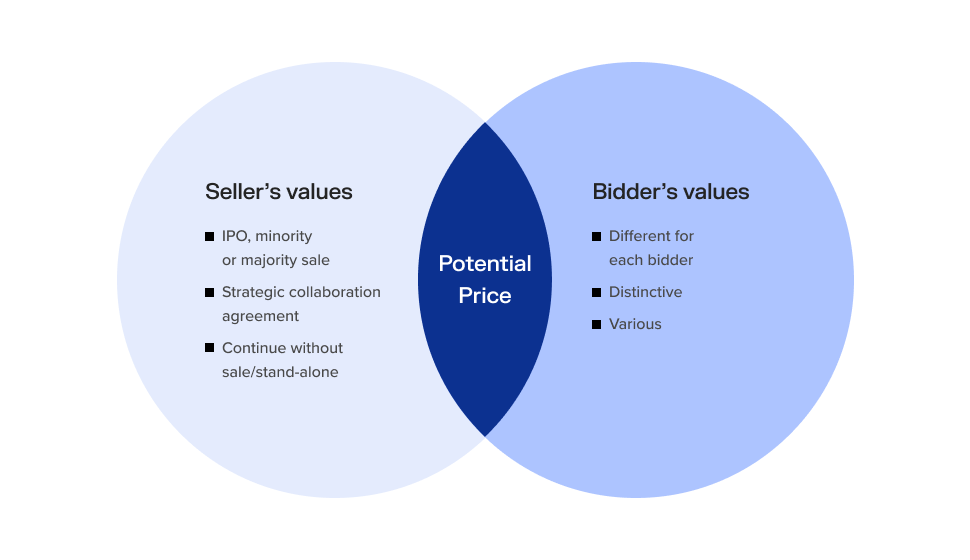

The two universes of seller’s and bidders’ distinct values

Universe of seller’s values

On the left side of the diagram, you have the universe of seller values. It’s singular since there’s only one owner of a company, but they can have multiple options to get value from the company. This determines what is in the seller’s possible universe of values or what a seller is willing to accept.

The bullet points in the circle are unique to the seller. There’s one seller with multiple options, such as initiating an IPO, splitting up, and selling only parts to just continue the business as-is. All of these options have a certain value to the seller. It might be monetary, but it can also be non-monetary.

The seller will determine what is best for them based on the sum of all benefits. Money might be an obvious factor and easy to measure, but there are many other motivating factors that decision-makers may have. These include intrinsic motivation, personal reputation, or other perspectives. All forms of human motivation, such as belonging and hubris, can be involved when it comes to selling a company.

Universe of bidders’ values

On the right side of the diagram, you have the universe of the bidder’s individual and distinct values. This is plural because, normally, there are multiple bidders. Each of them has distinct values determined by who they are, where they are, and what they can do with the company after they’ve acquired it.

All these values are distinct and unique to each bidder.

The overlapping values of seller’s and bidder’s universes equals price

In the middle of the diagram, the overlap emerges. If the highest of the seller’s values and some of the bidder’s values overlap, an agreement can be reached. We call this overlap purchase price.

You can only agree on a purchase price after you recognize both the seller’s and the bidders’ values, and where they potentially overlap. An acquisition can only be realized once the seller and at least one bidder have overlapping values.

In that space of value overlap, a seller-bidder relationship arises. This is the point when one bidder’s value becomes realized as the seller accepts their offer. Unrealized values of non-winning bidders are no longer relevant due to this exclusive relationship.

The work of M&A is trying to find overlapping values between seller and bidders

M&A work is mostly an iterative process of trying to find the overlap between those value universes, and then identifying how and where in the overlapping space you can find an agreement. If there is no overlap between what the seller is valuing and what bidders are valuing, there is just no reason to follow through with the acquisition.

The process of determining values and finding that overlap is probably the most important part of M&A work and is usually done during negotiations. The necessary check of company information, i.e., due diligence, is what many people think M&A work is all about.

Start with due diligence

Due diligence is the first, preparatory piece of the process, since only after checking the company can you really deduct overlapping values. And only with overlapping values can you finally agree on the corresponding price of the companies’ assets or shares via a sales purchase agreement.

The price is probably the most wanted and most visible information about any deal. It’s the only visible and quantifiable overlap of the two values that are agreed upon between the seller and buyer.

Look for overlapping values beyond price

Although price is important, for good M&A work it’s critical to understand the whole universe of sellers’ and bidders’ values and to also have sellers and bidders who are aware of what they want to do after the transaction. Only with this is it possible to quantify their perspectives and then be able to bring that to the one value overlap that can lead to the purchase agreement.

Much of M&A work is actually focused on trying to identify this potential overlap. Of course, there are scenarios where it’s not possible because there is no overlap existing. And, if for some reason you continue with the deal, you would even destroy value because you’re trying to do something that will never materialize, and can be damaging to the stakeholders.

A summary and three perspectives to realize an acquisition

To find the intersection of two values, it’s necessary to consider three different perspectives: the universe of seller’s values, the universe of bidders’ values, and finally, what we call the realization, which is when these two values overlap.

Let’s dwell on each point a little more:

In M&A, value cannot entirely be measured by price

Value is highly dependent on the individual perspective of the seller or different bidders, and the price is the ultimate overlap of those values. Price only happens when those values are overlapping, agreed upon, and executed.

So, price is a limited value indicator that you probably see most when you read a press release or a valuation that is based on comparable transactions.

Value is a lot more than just money; it has many factors we cannot quantify

The immediate needs and current circumstances, the probability, or certainty of what the future brings, the risk of adversity, and hubris are just some of the drivers that can define value. Some of these factors may or may not overlap between seller and buyer.

The acquisition is realized only when

the price is paid

You can have many valuations and a lot of data points on your values. But, eventually, it’s only one single act where both seller and buyer are meeting under the same agreement to realize the deal.

Price can only be realized after this work is done

Often at the beginning of the M&A thought process, someone will ask me how much they can get for a company, or how much they need to pay for a company.

I say it’s impossible to answer that question because even if I have all the information about the company itself and know the seller’s perspective or the bidder’s perspective, I am always missing the other universe that would allow me to answer if it’s even possible to sell or buy this company.

Finally, when there’s just one data point available, you’re left with a subjective analysis using statistics. For example, when you look back at previous transactions and try to equate them across time based on this single data point of price, all you can do is expect what will happen next rather than making specific calculations about what will happen.

To put it bluntly, you’ll only know for sure when you’ve got both of your hands in the cookie jar. Even then, there are too many other variables to predict which hand will go home with what kind of cookie.

So, instead of focusing only on the cookie, good M&A work needs to focus also on both hands.