Private equity (PE) offers a unique blend of financial rewards, intellectual challenges, and career acceleration, making it a magnet for high-achieving finance professionals. With 89% of PE firms planning to increase headcount in 2025 (Preqin), demand for skilled candidates is surging.

This guide explores the private equity interview process, from headhunter screenings and technical assessments to case studies and partner rounds, equipping you with actionable strategies to prepare effectively and avoid critical pitfalls.

Why choose a career in private equity?

Here’s why candidates from investment banking (IB), consulting, and corporate finance increasingly target PE roles:

Higher compensation & long-term incentives

Private equity professionals often earn significantly more than their counterparts in banking or consulting. For example, an average private equity associate role typically earns $277,266 a year, while an average financial consultant earns $89,156 a year.

However, the real appeal lies in carried interest, a share of fund profits that leads to seven-figure payouts for senior roles. This eat-what-you-kill model rewards deal performance, aligning compensation with value creation.

This [carried interest] percentage can range anywhere from 15 to 30% of the profits but generally hovers around 20%…

Josephine Koh

Director of Investor Services for Asia Pacific & Middle East at Carta

Deeper deal involvement & ownership

Unlike investment banking, where analysts execute transactions dictated by clients, PE professionals drive the entire investment lifecycle: sourcing deals, leading due diligence, structuring acquisitions, and managing portfolio companies. This end-to-end ownership attracts candidates seeking greater responsibility and strategic impact.

Exit opportunities & career trajectory

Private equity is a launchpad for senior finance roles. Associates often advance to vice president (VP) or partner positions within funds. Others may transition to C-suite roles at portfolio companies, start their firms, or move into venture capital or growth equity. The skills gained, such as financial modeling, operational due diligence, and stakeholder management, are highly transferable.

Overview of private equity interview stages

The private equity recruiting timeline is often relentless, especially mega-fund interviews (like KKR and Blackstone) with multi-stage evaluations that test candidates’ technical skills, strategic thinking, and cultural fit.

From initial screenings to high-stakes partner rounds, each stage is designed to identify those who can excel in PE’s fast-paced, high-reward environment. Below is a breakdown of the typical interview process with insights into on-cycle and off-cycle recruiting dynamics.

#1. Screening: The role of headhunters in private equity

Private equity headhunters are specialized recruiters who connect top finance talent with private equity firms. They typically target candidates with 2–3 years of investment banking or consulting experience, particularly those involved in M&A or leveraged finance deals. Headhunters identify prospects through LinkedIn profiles, deal databases (like PitchBook), and referrals from industry contacts.

Once a headhunter initiates contact, the process moves to a screening call with popular private equity interview questions. For example, they may assess your technical skills (“Walk me through a recent deal”) and motivations (“Why private equity over banking?”), while evaluating fit for specific fund types. These include mega-funds, sector-focused boutiques, and growth equity firms. Successful candidates are then presented to hiring managers, often securing interviews for roles not yet public.

Learn how to answer the ten most popular private equity interview questions.

#2. Technical assessment

After clearing the headhunter screening, candidates face a technical assessment. This stage is typically split into two parts:

Live modeling test

Candidates join a Zoom call with a senior associate or VP and receive a debt financing Excel prompt, often a simplified leveraged buyout (LBO) template or a blank workbook. For example: “Model the acquisition of a $500M revenue SaaS company with 40% EBITDA margins. Assume 6x debt/EBITDA and a 5-year hold.”

As you build the model (calculating internal rate of return (IRR), multiple on invested capital (MOIC), dividend recapitalization, and debt repayments), the interviewer may watch via screen share, probing assumptions like “Why did you set revenue growth at 8%?” or “How would a 50 basis-point (bps) increase in interest rates impact the equity check?”

Written valuation & scenario analysis

Post-modeling, you will defend your technical knowledge orally or in writing. There might be both technical and transaction questions, such as:

- How does the target’s customer concentration of 30% affect your investment thesis?

- If the exit multiple drops by 1x, what operational levers would preserve returns?

Most PE firms use these tests to gauge three traits:

- Speed. Can you deliver under time pressure?

- Accuracy. Are your formulas error-free?

- Judgment. Do your assumptions reflect real-world logic?

To better prepare for a technical interview, you can simulate test conditions. Practice building LBOs in 60 minutes using only Excel shortcuts (no mouse).

#3. Case study & investment committee (IC) simulation

Candidates who excel in the LBO modeling test may advance to the case study round. It’s a strategic evaluation of your ability to translate technical finance skills into real-world investment decisions. This phase simulates the day-to-day work of a PE professional, testing whether you can synthesize investment analysis, operational insights, and market trends into a compelling thesis.

The case study is typically conducted as a live interview over Zoom or in person, though some firms assign a take-home memo (24–48 hours to prepare). You will receive a 10–20 page investment memo detailing a hypothetical company (for example, a family-owned industrial distributor seeking growth capital) and have 1–2 hours to analyze the materials.

Next, you will present your recommendation to a panel of senior associates, VPs, or partners in a mock investment committee (IC) meeting. For example:

- Presentation (15–20 minutes)

Summarize your buy/no-buy thesis, highlighting risks (like customer concentration), value creation levers (like cross-selling synergies), and projected IRR.

- Q&A Grilling (30+ minutes)

Panelists role-play as skeptical partners, challenging assumptions like, “Why assume 5% organic growth when competitors are flat?” or “How would you handle management resistance to cost cuts?”

A private equity fund can test three core competencies here:

- Operational fluency

Can you move beyond spreadsheet mechanics to diagnose business model flaws?

- Communication under pressure

Can you defend your stance confidently?

- IRR-driven thinking

Are all recommendations tied to quantifiable returns (For example, “Renegotiating supplier contracts could lift EBITDA by $10M, adding 2% to IRR”)?

You can practice dissecting real-world PE acquisitions like these real estate case studies. Time yourself to mimic the pressure. You will need to prioritize insights over perfection.

Discover the essentials of real estate in private equity in our in-depth article.

#4. Partner interviews

After surviving the case study, candidates face interviews with partners of the PE firm (sometimes multiple rounds) focused on cultural fit and strategic alignment. Partners may talk about your deal experience (“Walk us through a transaction’s toughest hurdle”) and motivations (“Why choose us over competitors?”).

Behavioral questions test judgment (“How would you align conflicting priorities between management teams?”), while operational discussions assess your grasp of the firm’s investment strategy. Marrying technical depth with an authentic passion for the fund’s ethos is crucial for a candidate’s success.

#5. Reference checks & offer negotiation

Partner interviews are not the finish line. Even stellar candidates face meticulous reference checks, where firms discreetly contact former colleagues to verify technical skills, work ethic, and cultural fit.

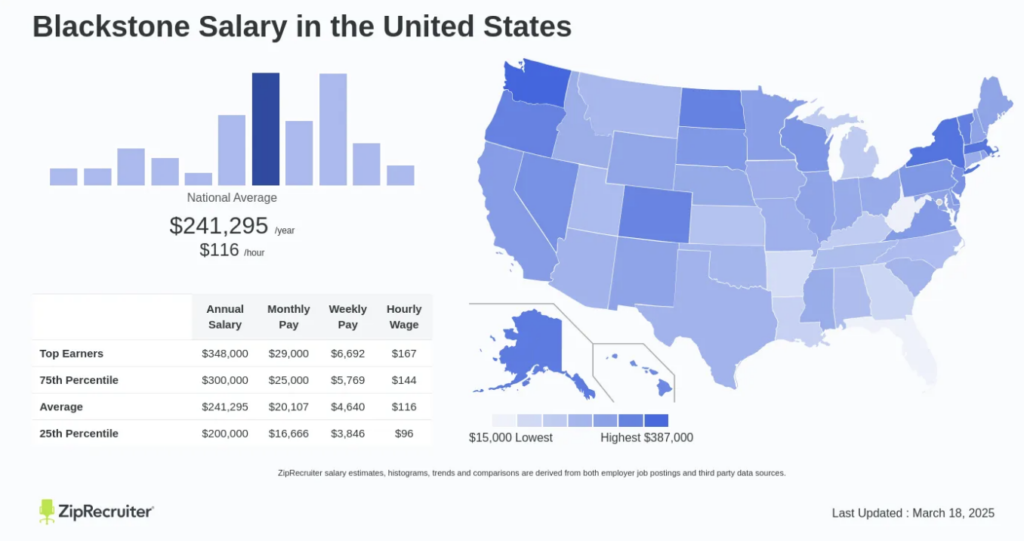

Only after references are cleared does the offer materialize. Compensation terms (base salary, bonus, carried interest) are then negotiated, with a mega-fund like Blackstone paying 20–30% more than a middle-market fund.

Niche expertise (like energy sector turnarounds) can boost leverage, while competing offers may secure signing bonuses. Final offers often expire within 72 hours, so acting decisively is crucial.

On-cycle vs. off-cycle private equity recruiting process: Key differences

The PE recruiting process follows two distinct paths: on-cycle interviews, which align with structured annual timelines for junior roles, and off-cycle interviews, which occur ad-hoc to fill immediate needs. Below, we contrast their timelines, candidate profiles, and preparation demands:

| Factor | On-Cycle | Off-Cycle |

|---|---|---|

| Timing | Structured windows (July–Aug for pre-MBA roles; Oct-Dec for post-MBA) | Rolling basis, often tied to fundraisings or unexpected attrition |

| Candidate Pool | Primarily current investment banking analysts | Experienced hires (consultants, corporate development, lateral PE associates) |

| Interviewing Speed | Fast-tracked (2–3 weeks from screening to offer) | Slower (1–3 months due to ad-hoc needs) |

| Interview Focus | Technical rigor (modeling tests) | Sector expertise and immediate deal impact |

Key topics covered in private equity interviews

Below, we outline critical focus areas of private equity interviews.

Expertise beyond LBO technical questions

Candidates must demonstrate advanced financial modeling skills, including stress-testing debt covenants, handling circular references (like management rollovers), and reconciling valuation methodologies.

For example, a discounted cash flow (DCF) method might undervalue a distressed asset compared to precedent transactions, requiring you to defend assumptions like terminal growth rates. This is vastly different from topics covered in investment banking interviews.

Compare private equity financial questions with questions asked during investment banking interviews.

Operational due diligence

Operational due diligence is central to private equity’s value creation ethos, demanding candidates to identify inefficiencies such as supply chain bottlenecks or pricing model misalignments.

Candidates are evaluated on their ability to bridge operational insights with quantifiable returns, such as linking cost restructuring to a 3% IRR uplift, mirroring the fund’s sector-specific playbook.

Behavioral & situational judgment

Cultural fit is tested through high-pressure questions like, “How would you handle CEO pushback?” Candidates are expected to demonstrate composure, strategic thinking, and adaptability.

Fluency in the private equity industry & strategic alignment

Sector-focused roles demand a strong grasp of industry trends, such as ESG in energy or artificial intelligence (AI) in healthcare. Generalists, on the other hand, must tackle broader macroeconomic questions like, “How would a recession impact our portfolio?”

In either case, demonstrating firm-specific knowledge is key. For example, referencing the firm’s recent acquisition and its strategic fit must be a part of a thorough private equity interview preparation.

Soft skills

Soft skills matter just as much as technical expertise. Structure responses with a clear thesis, supporting data, and a concise conclusion, avoiding long-winded monologues. In partner interviews, focus on strategic alignment.

For example, highlight how the firm’s renewable energy exits align with your investment thesis on grid modernization, demonstrating both industry knowledge and a strong cultural fit.

Mistakes to avoid in private equity interviews

Below are common PE interview mistakes and tips for avoiding them:

- Ignoring context in technical answers

Calculating a 25% IRR isn’t enough. Explain why it aligns with the fund’s hurdle rate or sector risk.

- Ignoring the “So what?” factor

Don’t just detail EBITDA adjustments. Tie them to the investment thesis. Example: “Normalizing EBITDA for one-time legal costs strengthened debt capacity, justifying a 12x purchase multiple.”

- Underestimating nuances of operational improvements

Instead of generic cost-cutting, propose specific strategies: “Repricing long-term contracts could lift margins by 300 bps in 18 months.”

- Misreading the firm’s strategy

Research the firm’s recent deals and align your answers accordingly: “Your focus on founder-owned businesses fits my experience with earnout negotiations.”

- Fumbling the “Why PE?” question

Avoid generic responses like “seeing the full-deal cycle.” Instead, show depth: “PE’s long-term ownership model rewards patience and operational problem-solving, unlike banking’s transactional nature.”

- Neglecting soft skills

Strong technical skills won’t save poor communication. Structure responses clearly: “I miscalculated a model, cross-checked with a senior, fixed the error, and improved our review process.”

How to excel in a private equity interview?

Here’s how to prepare for a private equity interview to differentiate yourself:

Pre-empt technical follow-ups

Anticipate why behind every calculation. For example, after building an LBO, add: “Assuming the exit multiple drops 1x, here’s how we’d offset it via working capital optimization.” This shows foresight beyond model mechanics.

Leverage proprietary insights

Research the firm’s private equity investments and cite underappreciated enterprise value drivers. Example: “Your recent acquisition in the logistics space could unlock cross-selling opportunities with Portfolio Company X’s SaaS tools.” This demonstrates that the initiative is comparable to that of private equity investors.

Frame stories with the “CARL” method

For behavioral questions, structure answers using the Context, Action, Result, Lesson (CARL) method. For example:

- Context: “A portfolio company faced customer churn.”

- Action: “I led a pricing segmentation analysis.”

- Result: “Retention improved by 15%.”

- Lesson: “Data-driven tweaks often trump sweeping changes.”

Ask differentiated questions

Move beyond generic queries. Ask: “How does your fund balance sector specialization against diversification in today’s volatile markets?” or “What’s one portfolio company where operational value creation exceeded initial underwriting?”

Simulate real-world scenarios

Practice “live” due diligence. Analyze a public company as if pitching it to the fund. Highlight risks, synergies, and hold period logic. This mirrors partner-level thinking.

Key takeaways

- Technical mastery and strategic insight are critical. Excel in financial modeling tests and link results to investment rationale and fund-specific strategies.

- Operational acumen drives value. Identify and quantify actionable improvements, aligning them with the fund’s expertise to demonstrate real-world impact.

- Cultural fit and preparation define success. Showcase adaptability, demonstrate firm knowledge, and negotiate offers decisively to secure your role.