Selling to a strategic or financial buyer is one of the most important choices for business sellers. These two buyer types represent distinct M&A approaches, each pursuing different goals and directly impacting sellers after transactions.

Knowing these differences can help you choose the buyer that best aligns with your business sale strategy. Let’s explore the motivations of financial and strategic buyers, key differences, and the pros and cons of selling to them.

Strategic buyer: Definition

A strategic buyer is an operating company that pursues M&A to complement its business expansion strategies — acquiring competitors, entering new markets, improving products and services, achieving economies of scale and so on. It usually integrates the acquired company into its existing operations to achieve its business goals.

Strategic buyer example: Microsoft and LinkedIn

Microsoft’s $26.2 billion acquisition of LinkedIn is a classic example of a strategic buyer in M&A. It is defined as strategic because it has:

- An operating company

Microsoft is an operating company that generates revenue from its products, including but not limited to software apps, hardware, and cloud services. It pursues M&A to complement its business strategy.

- Strategic M&A buyer motivations

Microsoft acquired LinkedIn to establish a new revenue stream, integrate LinkedIn users into Microsoft 365, and create cross-selling opportunities.

- Long-term vision

Microsoft has been extensively growing LinkedIn since 2016. This professional network currently generates over $16 billion in annual revenue.

Financial buyer: Overview

A financial buyer is an investment company that acquires other companies primarily for profit. Financial buyers, like private equity firms, investment banks, and investment funds, acquire businesses, manage them during a defined period, and sell them at a premium.

Financial buyers tend to pursue leveraged buyouts (LBOs) — putting forward a small portion of the required sum, making up the balance with borrowings. This allows for acquiring companies with minimal capital outlay.

Being non-strategic in nature, financial buyers don’t integrate acquired businesses into their own operations. They pursue M&A to realize a return on investment (ROI) rather than achieve operational synergies and other long-term strategic goals.

Financial buyer example: Blackstone and Hilton Hotels

Blackstone’s $26 billion acquisition of Hilton Hotels is a classic example of financial, non-strategic M&A. Let’s see how Blackstone qualifies as a financial buyer:

- Investment company

Blackstone is a private equity firm with over 240 portfolio companies and $1.1 trillion in assets under management. Unlike operating companies, it generates revenue from its investments rather than products and services.

- Leveraged buyout

Blackstone itself invested $6.5 billion in Hilton Hotels, while the rest was borrowed, meaning the acquisition was 80% leveraged.

- Return on investment in acquisitions

Blackstone acquired Hilton Hotels to develop it for a certain period and sell it at a premium.

- Holding period and exit

Hilton Hotels was Blackstone’s portfolio company for 11 years. Blackstone exited its investment in Hilton Hotels in 2018, earning over $14 billion from this acquisition, several times more than the initial investment.

The sale [of Hilton Hotels by Blackstone] will bring to an end an 11-year relationship of highs and lows that ended up as the most-profitable private equity deal on record

Gillan Tan

Senior Reporter at Bloomberg

Strategic vs financial buyer: Key differences

A strategic buyer is distinct from a financial buyer because their M&A decision-making processes are fundamentally different. Let’s explore how these two buyer types approach various investment stages.

M&A investment horizon

The investment horizon is how long strategic and financial buyers plan to hold onto acquired companies before selling them.

Strategic buyer

There is no traditional investment horizon when talking about strategic buyers. This is because strategic buyers usually aim for long-term value and integration.

Strategic buyers tend to transform acquired companies into divisions or subsidiaries and have no intention to sell them for profit after a certain period. Strategic M&A buyers often absorb acquired businesses entirely, becoming “surviving entities.” In this business model, the acquired business essentially dissolves, and a traditional exit strategy doesn’t apply here.

However, strategic buyers sometimes sell acquired companies in a process called divestment, mostly due to unfavorable market conditions, poor performance, and unrealized synergies. But this is clearly distinct from financial buyers because the sale was never planned from the start and has been driven by unfavorable factors.

Learn more about the divestment process in our dedicated article.

Financial buyer

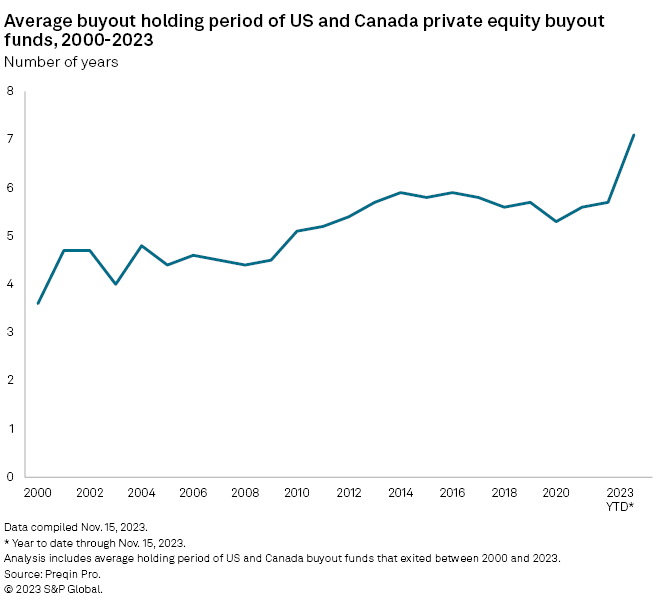

Unlike strategic buyers, financial buyers have a specific investment timeline – typically around five years. It is a holding period during which the financial buyer actively manages the acquired company to improve it and sell it at a higher price. A shorter holding period is typically a sign that a financial buyer has successfully improved its portfolio company more quickly and is ready to realize a favorable ROI.

Holding periods have become longer in recent years, particularly due to economic uncertainty and widening price gaps between buyers and sellers. This signals that institutional investors, including investment firms and hedge funds, wait for favorable market conditions and exit opportunities. That is why there is a clear distinction that, unlike strategic buyers, financial buyers only sell to capitalize on their assets.

Operational involvement

Operational involvement refers to how much strategic and financial buyers engage with the acquired companies’ decision-making and daily operations.

Strategic buyer

A strategic buyer generally aims for post-merger integration when acquiring a business. It is the main path to value creation in M&A deals for operating companies.

Integration activities begin on the first operational day post-merger and cover all the business functions of the acquired company — IT, HR, finance, sales, operations, R&D facilities and so on.

Successful business integration strategies ensure that cost and revenue synergies are unlocked within the combined company. Successful strategic acquirers typically spend over 6% of deal value on integration and transformation efforts. This is a significant investment, ranging from millions to billions of dollars and reflects the critical role of successful integration in M&A success.

Also, strategic buyers intend to retain senior executives of acquired companies to facilitate integration efforts. Thus, 44% of acquiring companies ask senior leaders of target companies to sign retention agreements.

However, the opposite can also be true. Acquiring firms often replace their targets’ C-suite, particularly when they believe their own management team is better suited to given circumstances.

Financial buyer

Private equity acquisitions are typically less invasive than strategic ones because financial buyers don’t aim to integrate portfolio companies into their own businesses. Instead, they undertake various initiatives that aim to improve financial performance.

According to the EY 2024 Private Equity Pulse Survey, 53% of private equity firms prioritize working capital improvements, while 57% focus on cost-cutting activities. These activities commonly include layoffs, departmental consolidations, inventory reductions, and debt financing.

Amid the macro turbulence of last year, firms were highly focused on managing liquidity and on cost reduction initiatives

Pette Witte

Lead Analyst at EY Global Private Equity

Financial buyers also influence the decisions of portfolio companies at the board level, driving initiatives such as mergers, acquisitions, and investments. Such involvement aims to maximize the acquired company’s value during the holding period.

Acquired public companies are often taken private to manage such transformations. This is more convenient, giving private equity firms flexibility in decision-making and lessening the burden of the strict regulatory requirements for public companies.

Acquisition targets

Strategic and financial buyers value different qualities in potential acquisition targets.

Strategic buyer

Strategic buyers approach targets that best complement their strategic endeavors, such as market expansion, product improvements, optimized supply chains, or cutting-edge technologies. They often look for:

- Competitors in the same industry, to gain greater market share

- Companies with complementary products and services, to enhance product lines

- Suppliers and distributors, for greater control over production and distribution

- Companies in new markets, for market expansion

- Companies with complementary technology, for technological advantage

- Companies in related industries with strong customer loyalty, for greater sales reach and an expanded customer base

- Firms with specific talent and expertise, for greater R&D capabilities

While it’s usually necessary for strategic targets to be financially healthy, strong cash flows and high profits may be secondary if such targets offer long-term benefits. For instance, Facebook acquired Instagram for $1 billion when it had only 13 employees and generated no money but offered a great competitive edge.

Financial buyer

Financial buyers consider high business profitability among other investment criteria and prioritize their exit strategies when selecting targets. They choose targets that align with their investment strategies, including but not limited to the following:

- Companies with strong cash flows, for stable returns

- High-growth companies, for greater exit proceeds

- Companies with easily scalable business models, for driving profits with minimal cost

- Companies in non-cyclical industries, for minimizing market factors in exit strategies

- Companies led by experienced executives, for minimal involvement in daily operations

Financial buyers typically prioritize financial health and conduct comprehensive financial due diligence on their targets using multiple business valuation methods. However, some private equity and venture capital firms specialize in distressed deals (e.g., real estate properties in financial hardship or facing foreclosure).

Strategic acquisition vs financial acquisition: A summary of key differences

Let’s summarize how strategic and financial buyers differentiate in their core approach to mergers and acquisitions.

| Aspect | Strategic buyer | Financial buyer |

|---|---|---|

| Motivation |

|

|

| Investment timeline | No investment timeline | Typically five years |

| Reason to sell | Financial distress, poor performance, unrealized synergies | An opportunity to realize high ROI |

| Level of operational involvement | Very high involvement; focused on integration and synergies | Moderate-to-low involvement; focused on financial improvements |

| Operational scope | Merges with the target company to realize synergies | Makes financial improvements |

| Approach to target selection | Seeks targets that complement strategic goals | Seeks targets that promise high ROI and easy exit |

| Critical traits in targets | Competitive advantage, market share, and synergies | Financial performance, non-cyclical market, exit opportunities |

Pros and cons of selling to a strategic buyer

Pros of selling to a strategic buyer

Higher purchasing price

Strategic buyers pay higher premiums more often than financial buyers because they aim at long-term value, revenue, and cost synergies. Another factor is that strategic buyers often pay high “control premiums” (20%–40% over the target’s intrinsic value), incentivizing sellers to give up ownership.

Clean exit

Strategic buyers are generally less inclined toward retaining management teams of acquired companies and don’t expect significant seller involvement post-acquisition. Such buyers tend to assume most (if not all) seller liabilities (particularly in stock acquisitions), making them much more favorable for sellers who want to exit the business entirely.

However, that is not the case in asset acquisitions. In fact, in asset sales, sellers may find themselves in less favorable circumstances. That is because asset buyers often leave sellers with liabilities tied to sold assets while requiring them to provide extensive warranties and representations.

Asset purchase agreement vs stock purchase agreement: Explore the difference in our dedicated article.

Job security for employees

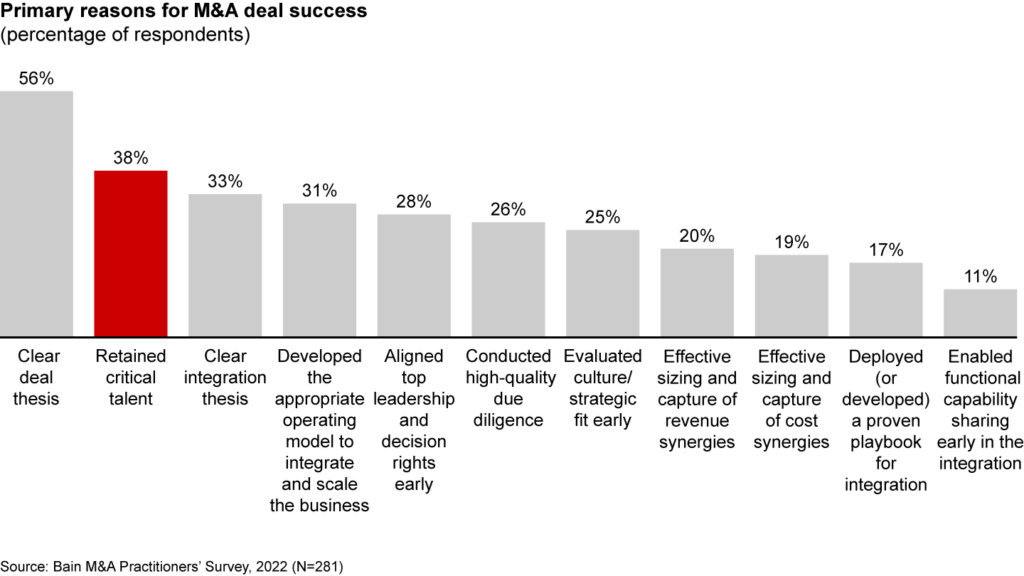

It’s common for strategic buyers to value their targets’ workforce as necessary for successful transformation. According to the 2022 Bain & Company M&A Practitioner’s Survey, executives consider talent retention the second biggest factor in M&A success. Such buyers are also more likely to pursue cultural fit in acquisitions because it helps in talent retention.

Strategic buyers typically incentivize sellers’ key employees to stay and invest in their cultural adaptation. Therefore, selling to a strategic buyer can be better than selling to a financial buyer if you are a business owner who cares about the job security of your employees.

Cons of selling to a strategic buyer

No future benefit for the seller

The opposite side of clean exit is that sellers generally lose 100% ownership in sold companies, including intellectual property rights. These sellers and their shareholders can’t benefit from the future growth of sold businesses, brand identity, and patents.

However, the outcome can be different in a stock-for-stock merger, where shareholders of the acquired company receive shares in the acquiring company. This allows them to retain interest in the acquiring company and benefit from its future performance.

Post-merger layoffs

Strategic deals, particularly mergers of competitors, mean certain employee roles will overlap. Such buyers generally cut overlapping roles to achieve cost savings. For instance, Microsoft laid off 18,000 employees following the acquisition of the Nokia devices division, 12,500 of which were former Nokia workers.

Pros and cons of selling to a financial buyer

Pros of selling to a financial buyer

Ongoing financial interest for sellers

Business owners are more likely to retain a stake in the existing business when selling to financial buyers than strategic buyers. This allows a seller to benefit from continued business performance of the existing portfolio company.

Ongoing support for sellers

Financial buyers improve portfolio companies in many ways that benefit sellers. Often acting as financial sponsors, they hire interim managers and M&A advisors, create finance optimizations and restructurings, invest in innovation, improve product offerings, and expand market reach. Some business owners are only capable of unlocking capital and making significant operational improvements when bolstered by private equity investments.

A quick path to IPO

The goals of financial buyers and sellers often align, particularly when both parties aim for an IPO as an exit strategy. While public offerings are not primary considerations for financial buyers, it’s possible to find those who are seeking them. For instance, IPOs accounted for 155 out of 1,700 private equity-backed exits through Q1-Q3 2024.In such cases, business owners leverage the financial buyer’s expertise and capabilities to achieve IPO goals more quickly than businesses that grow organically. For comparison, it takes nearly a decade for a startup to be ready to go public, while IPO preparations involve complex financial modeling and take between six and 12 months.

Learn more about financial modeling for M&A deals, including public offerings and leveraged buyouts in our dedicated guide.

Cons of selling to a financial buyer

No immediate return

Financial buyers generally expect sellers to continue running their companies. They seek maximum performance under given circumstances, often requiring sellers to achieve certain milestones to receive the full acquisition payment. This arrangement is known as an earnout.

In many middle-market deal structures where a private equity (PE) firm is the buyer, it’s common for 10% to 25% of the purchase price to be tied to an earnout

Jacob Orosz

President of Morgan & Westfield

Leadership conflicts

Sometimes the goals of financial buyers and sellers don’t align, potentially leading to leadership clashes. Sellers may experience ongoing stress as financial buyers push for decisions that prioritize short-term profit, sometimes at the expense of long-term company value.

Choosing the best buyer for selling your business

So who is the best buyer to seek out when selling your business? Here is a list of seller goals and the best buyer match:

| Best buyer | Seller goal |

|---|---|

| Strategic buyer | Sellers who seek high company valuation in M&A |

| Strategic buyer | Sellers who want to transfer liabilities and exit their business entirely |

| Strategic buyer | Sellers who aim for overall job security for their employees |

| Financial buyer | Sellers who aim to retain interest in the business and have certain financial flexibility in acquisitions |

| Financial buyer | Owners who seek a financial sponsor |

| Financial buyer | Owners who want to maximize business growth and aim for big proceeds from private equity exits |

Key takeaways

- Strategic buyers are operating companies that pursue mergers and acquisitions to achieve their long-term business goals, including market expansion and vertical integration.

- Financial buyers are investment companies that pursue mergers and acquisitions to generate a return on their investment.

- Strategic buyers are better for sellers who want to transfer liabilities, receive higher premiums, and ensure job security for employees.

- Financial buyers are better for sellers who want to retain a stake in the business and receive higher proceeds during exits.