The adoption of cell phones, wireless connectivity, smartphones, and 5G technology has transformed the telecommunications industry over the last 20 years. These transformations didn’t occur on their own but were fueled by the biggest telecom mergers of that period.

The historical context and impact of the major telecom deals are significant and indicative of what the industry has become today. So in this article, we explore the 12 biggest telecom acquisitions and their impact on the regulatory environment, competition, and innovations of the telecom industry.

Brief overview of M&A in telecommunications

High interest rates, political uncertainty, and low valuations have slowed global M&A activity in the last several years. However, deals are anticipated to bounce back due to a growing strategic demand.

If there is one certainty in all this uncertainty, it is that M&A activity will bounce back…

Brian Levy

Global Deals Industries Leader, Partner, PwC United States

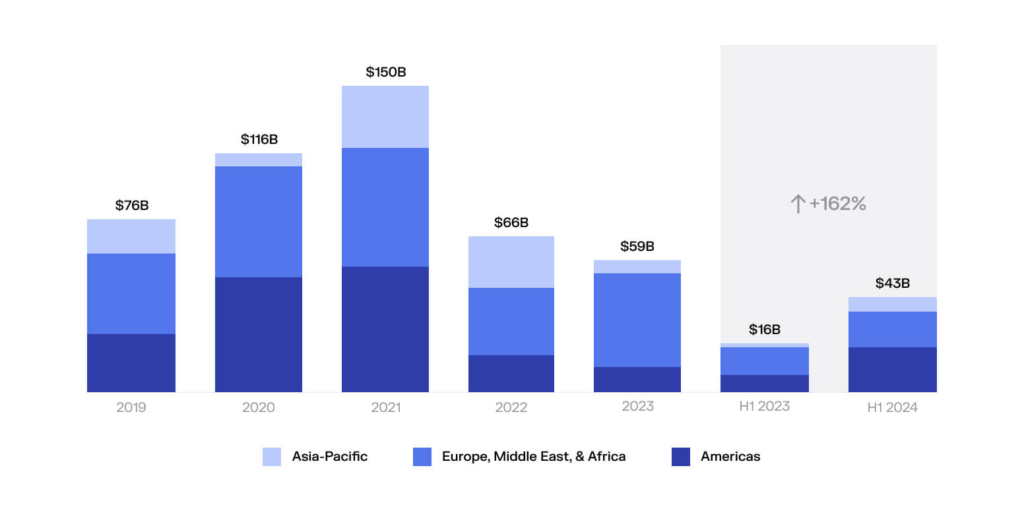

We have already seen a surge in M&A activity, particularly in the telecommunications industry, where deal values have increased 162% in the first half of 2024. The uptick in telecom M&A reflects broader trends, where telcos seek transformations and innovations to meet market demands. So let’s dive deeper into these trends.

Source: Bain & Company

Demand for transformation

As much as $22 billion out of $43 billion announced TMT deals in the first quarter of 2024 are infrastructure, mobile, and fixed divestments. That is a huge spike compared to the third quarter of 2023 (telecom M&A declined 39% during Q1-Q3 of 2023, according to Bain & Company’s early 2024 M&A report).

Telecom companies have not only optimized their portfolios to unlock capital and channel efforts into core operations and technologies but have also begun improving cyber defenses. The adoption of the FCC 7-day notification rule has made telecom companies spend more resources on cybersecurity as part of their transformation strategies.

Check the largest cybersecurity acquisitions in our dedicated article.

Pursuit of innovation

Telcos continuously pursue innovations, developing new capabilities and technologies to stay ahead of the competition. A notable example is the joint venture of NTT Docomo, NTT, NEC, and Fujitsu to make ultra-fast 6G transmission technology.

Recent telecom mergers reflect the willingness of businesses to adopt artificial intelligence as well. For example, HPE expects to acquire Juniper Networks for $14 billion, which develops AI-native networking equipment. It was one of the largest tech acquisitions announced in 2024. Innovative joint ventures are also on the rise. Juniper Networks recently partnered with Quantum Bridge Technologies to make the world’s first quantum-safe networking solutions.

Historical context of telecom M&A

Let’s briefly observe the events that shaped the telecom market in the past years.

Deregulation and liberalization (1980s–1990s)

The breakup of AT&T’s monopoly in 1984 created several independent companies and boosted competition. The 1996 Telecommunications Act also fostered developments in U.S. telecom services. This trend relieved many restrictions on broadcasting, radio, and TV sectors, and M&A deals and tech investments exploded.

The dot-com bubble (2000)

M&A liberalization and mass adoption of the internet created a bubble of overvalued tech companies from which investors anticipated a high return on investment.

Lacking sustainable value-creation models, these companies crashed amidst higher interest rates, and the telecommunications market crashed afterward. The Nasdaq index lost nearly 80% during that period, and telecom companies focused on divestments and restructuring to stabilize finances.

Convergence (2000s)

Networking advancements and post-bubble market recovery helped strategic buyers and private equity firms gain scale and create more consolidation in the market. Telecom giants pursued horizontal and vertical mergers to scale operations, complement services, and create bundled products. The formation of Verizon Communications was among the most notable historical mergers.

Digital transformation (2010s)

Fiber network and data center advancements, widening internet coverage, the rise of cell phones, and increasing content consumption channeled dealmaking activity into product integrations. Verizon’s acquisition of Verizon Wireless reflected the demand for wireless networks. Similarly, AT&T’s acquisition of Time Warner exemplified the intent to capitalize on content consumption.

5G and technology-driven M&A (2020s)

The early 2020s responded to growing demands for mobile devices with cheap, high-speed 5G connections. Key telecom players, like NTT and T-Mobile, invested heavily in 5G infrastructure and networks to meet such demands. Advanced connectivity also opened new opportunities across numerous sectors, including automotive.

In 2023, T-Mobile announced a 5G-based vehicle-to-everything (V2X) project to support road safety. This project highlights the increasing role of 5G technology in the automotive industry and delivers new opportunities for automotive mergers and acquisitions.

12 biggest telecom mergers and acquisitions

Our list of mergers and acquisitions in the telecom industry enumerates 12 deals:

1. Vodafone + Mannesmann

- Year: 2000

- Deal value: ~ $183 billion

Vodafone AirTouch PLC, the British telecom giant, acquired German telecom behemoth, Mannesmann AG, for approximately $183 billion (~$328 billion adjusted for inflation) in February 2000. It was one of the biggest acquisitions of all time.

The combined telecom operator served over 43 million customers across Europe and the United States. This takeover secured Vodafone’s dominant position in the European wireless communications market.

However, was it that good for Vodafone? Multi-billion deals like this make companies vulnerable to market disruptions. Vodafone’s stock lost nearly 80% in 2000-2002 (the dot-com bubble burst), and the telecom behemoth recorded over $23 billion in losses connected to the Mannesmann deal.

This acquisition also impacted Europe’s antitrust developments. In 2004, the EU adopted the EC Merger Regulation, responding to the potential anti-competitive harms of gigantic mergers.

2. AOL + Time Warner

- Year: 2000

- Deal value: ~ $182 billion

The $182-billion merger of America Online Inc. and Time Warner was one of the biggest deals in history and also one of the worst. AOL Time Warner had $350 billion in combined market cap, 130 million subscribers, and 1.4 billion monthly TV viewers. The rationale was to create an ultimate media entertainment company with TV, movie, music, publishing, and cable network services.

However, the merger was doomed by cultural clashes, management disagreements, and debt amidst dot-com disruptions and the rise of the Internet. By 2002, AOL Time Warner lost $98 billion, and eventually, Time Warner decided to sell AOL to Verizon.

The former media executive behind the merger, who was referred to as the “Time Warner Chief in a Merger Debacle” by The New York Times said:

AOL was the Google of its time. It was how you got to the Internet, but it was using some old media business ideas that were undone by the Internet itself, and that’s why Google came along.

Gerald M. Levin

3. Verizon + Verizon Wireless

- Year: 2014

- Deal value: ~ $130 billion

Verizon Communications acquired Vodafone’s 45% stake in Verizon Wireless for $130 billion in February 2014. The combined entity had nearly $100 million subscribers and was among the largest wireless service providers in the US.

The buyout from Vodafone helped Verizon Communications secure its market position and reduce competition. Verizon aimed to generate higher cash flows from mobile networks, catering to the growing demand for cell phones.

This acquisition was strategically and financially successful for Verizon. The company reported an 8.2% growth in wireless revenue and a 5.4% growth in total operating revenue. Verizon also reported an increase of 6 million wireless retail connections, totaling 106 million in December 2014.

4. AT&T + BellSouth

- Year: 2006

- Deal value: $86 billion

AT&T acquired BellSouth Corp. for $86 billion following regulatory approval from the Federal Communications Commission (FCC) in December 2006. The combined entity had over 136 million customers, including home telephone owners, internet subscribers, and wireless phone customers.

While approved, the deal faced antitrust criticism, aggravated by AT&T’s announced plans to cut 10,000 employees by 2009 (over 26,000 job cuts in 2007-2009). In the successful attempt to get regulatory approval, AT&T agreed to freeze prices for competitors who use its networks for two years post-deal. The FCC did, however, respond to market consolidation later with new net neutrality regulations.

We got substantial concessions that are going to mitigate a lot of the harms that would otherwise have resulted from this merger.

Jonathan Adelstein

Former Commissioner of the FCC

This acquisition was successful for AT&T and its shareholders. The company reported a 20.3% annual return from stock appreciation and dividends, record-breaking operating income, and a 15% increase in service revenue in its 2007 annual report.

5. AT&T + Time Warner

- Year: 2018

- Deal value: $85 billion

AT&T completed the acquisition of Time Warner for $85 billion in 2018 after over a year of hurdles around competition concerns. This mega-merger resulted in AT&T consuming Time Warner’s Warner Bros., HBO, and CNN brands. This merger would expand AT&T’s media portfolio and complement its broadcasting services with nearly 3.5 million corporate customers alongside consumers.

Still, the union between the two companies was unsuccessful, and AT&T sold Time Warner for $43 billion in 2022. Anticipated merger synergies weren’t realized because of debt, leadership differences, and management mismatches. Financial analysts didn’t expect the merger would face so many cultural clashes. However, with time, more experts believed the human element was the dominant factor in this failure.

…the corporate personalities of the merging firms. They did not fit. It was a bad marriage that looked good on paper and in photographs.

Victor Glass

Professor at Rutgers Business School

6. Charter Communications + Time Warner Cable

- Year: 2016

- Deal value: $67 billion

Charter Communications completed a $56.7-billion merger with Time Warner Cable and a $10.4 billion acquisition of Bright House Network in 2016. Charter aimed to broaden its reach and compete against Comcast and AT&T. The resulting entity combined over 25 million customers.

This deal faced scrutiny from the FCC and the Department of Justice. Charter Communications agreed to provide high-speed internet access to 1 million customers of a smaller competitor. It also agreed to include over 140,000 homes and phone companies in New York’s less populated areas in its high-speed coverage area.

In 2018, the company faced several challenges from the New York State Public Commission attempting to dissolve the merger as Charter Communications failed to meet its obligations. Still, Charter was financially successful with this acquisition. Its fiber infrastructure and cable networks generated over 24% more revenue between 2017 and 2021, while its stock doubled in the same period.

7. Bell Atlantic + GTE

- Year: 2000

- Deal value: $52.8 billion

Bell Atlantic announced the acquisition of GTE in 1998, and the $52.8 billion transaction was approved in 2000, resulting in the birth of Verizon Communications. Verizon combined over 250,000 employees, 25 million wireless customers, and over 95 million line connections, becoming one of the largest telecom providers.

Verizon formed at the peak of the early wireless technology era and enjoyed growing demand among cell phone users. It had the resources and market power to dominate and innovate.

Speed, customer service and innovation are the hallmarks of the Verizon team.

Charles R. Lee

Former Verizon chairman

Now it delivers services to 210 countries. Verizon Communications is the largest U.S. telecom provider by revenue and the world’s third telecom company by market cap at the time of writing.

8. Sprint + Nextel

- Year: 2005

- Deal value: $46.5 billion

Sprint Corporation acquired Nextel Communications, Inc. in a merger of equals for $46.5 billion in 2005. Sprint and Nextel aimed to combine customers, revenues, and tech capabilities, including iDEN and CDMA networks.

The combined entity had around $70 billion in joint value and over 40 million subscribers. However, the merger was unsuccessful for a few reasons.

One was integration challenges. iDEN and CDMA networks were inherently incompatible, and most customers didn’t seem interested in outdated iDEN handsets. Strategic disputes between Sprint, Nextel, affiliates, and partners also dragged Sprint down. In 2008, Sprint wrote down nearly all of the merger’s value, making it one of the worst deals in corporate history.

The company has been in declining condition ever since.

Jonathan Chaplin

Managing partner at New Street Research

9. NTT + NTT Docomo

- Year: 2020

- Deal value: $40 billion

Nippon Telegraph and Telephone Corp (NTT) acquired NTT Docomo for 4.25 trillion yen ($40 billion) in a take-private deal in the midst of 2020.

The rationale for the deal was to follow the Japanese government’s policies to cut wireless internet prices for consumers. As a private entity, NTT Docomo would be compelled to lower the prices as shareholders no longer dictated its decisions.

Post acquisition, Docomo will no longer be answerable to shareholders. If the government instructs it to cut prices, it will oblige

Atul Goyal

Analyst at Jefferies Group

Another analyst said this buyout would make 5G developments easier as NTT sought less regulated revenue streams. This acquisition was successful, although it initially faced some dips in NTT’s stock.

In December 2020, NTT Docomo launched its first 5G mobile service, supporting internet speeds of 4 Gbps and higher. By 2021, Docomo had over 85 million customers in the country and generated an additional 17 billion yen in net income compared to 2020.

10. T-Mobile + Sprint

- Year: 2020

- Deal value: $26 billion

T-Mobile acquired Sprint for $26 billion after nearly two years of regulatory scrutiny. Sprint merged with and into T-Mobile. The surviving entity, T-Mobile, had over 100 million wireless customers at the time of the merger.

It also aimed for Sprint’s “true 5G” technology, released a year before the deal closure. Sprint’s networks would alleviate high infrastructure costs and make it easier for T-Mobile to develop 5G services and compete with AT&T and Verizon. Consequently, it launched the first nationwide standalone 5G network around four months post-merger.

T-Mobile, now a 5G phone provider, has been doing exceptionally well since then. Its net income increased from $3.1 billion in 2020 to $8.3 billion in 2023, and it added nearly 20 million customers in the same period. Its stock also grew 154%+ in the past five years.

11. Vodafone + Liberty Global Europe

- Year: 2019

- Deal value: €18.4 billion

Vodafone acquired Liberty Global’s business in Germany and Central and Eastern Europe (CEE) for €18.4 billion in 2019. Vodafone had 54 million households directly connected to its network and over 120 million homes potentially covered after the merger.

As of June 2019, Vodafone was the largest operator of high-speed networks in Germany and CEE. The merger’s rationale was to compete with Deutsche Telekom, Telefónica, and Orange.

Like many horizontal telecom mergers and acquisitions, Vodafone’s deal potentially threatened competition. The European Commission approved the merger under specific conditions. Vodafone committed to allowing Telefonica Germany to access its networks and freeze prices for air-to-air TV operators, to name a few.

This acquisition wasn’t disastrous. But it didn’t deliver €1.5 billion in expected cross-selling revenue either. Moreover, Vodafone’s stock price has not recovered since 2020.

In March 2024, Vodafone announced a €8 billion sale of Vodafone Italia to Swisscom as part of its restructuring strategy.

The disposal in Italy is one of a number of steps that the chief executive, Margherita Della Valle, has taken to reposition Vodafone as the firm restructures in markets where its returns are below the cost of capital.

The Guardian

12. Comcast + NBCUniversal

- Year: 2013

- Deal value: $16.7 billion

Comcast acquired the remaining 49% of NBCUniversal for $16.7 billion in 2013, two years after it acquired its controlling stake for $13.8 billion. Comcast aimed for border reach and higher returns from cross-selling, reinforcing its status as the biggest media company in the United States.

Comcast financed both acquisitions with mostly cash and assets, and it didn’t take a toll on its financials. Additionally, NBC generated 12% more consolidated revenue in 2012 and 9.7% more operating income in 2014. Comcast’s stock also grew for nearly eight years after its first acquisition of NBCUniversal.

Final words

- The telecom industry impact of 1900s regulatory easing was huge. Mergers and acquisitions in the telecom sector exploded, and key players, like T-Mobile, AT&T, Verizon, and Comcast, emerged.

- Horizontal and vertical mergers historically prevailed in the telecom landscape. Companies aimed to reduce market competition through market expansion, bundled products, and innovations.

- Big deals often exhibit integration and management issues that dampen anticipated synergies. AOL & Time Warner and Sprint & Nextel are telecom merger examples that went seriously wrong.

- The current telecom M&A landscape strives for innovations. Companies have been actively divesting underperforming assets to focus on core operations and invest in new capabilities, such as AI, 6G, and cybersecurity enhancements.