Sebastian Montoya

Sebastian Montoya

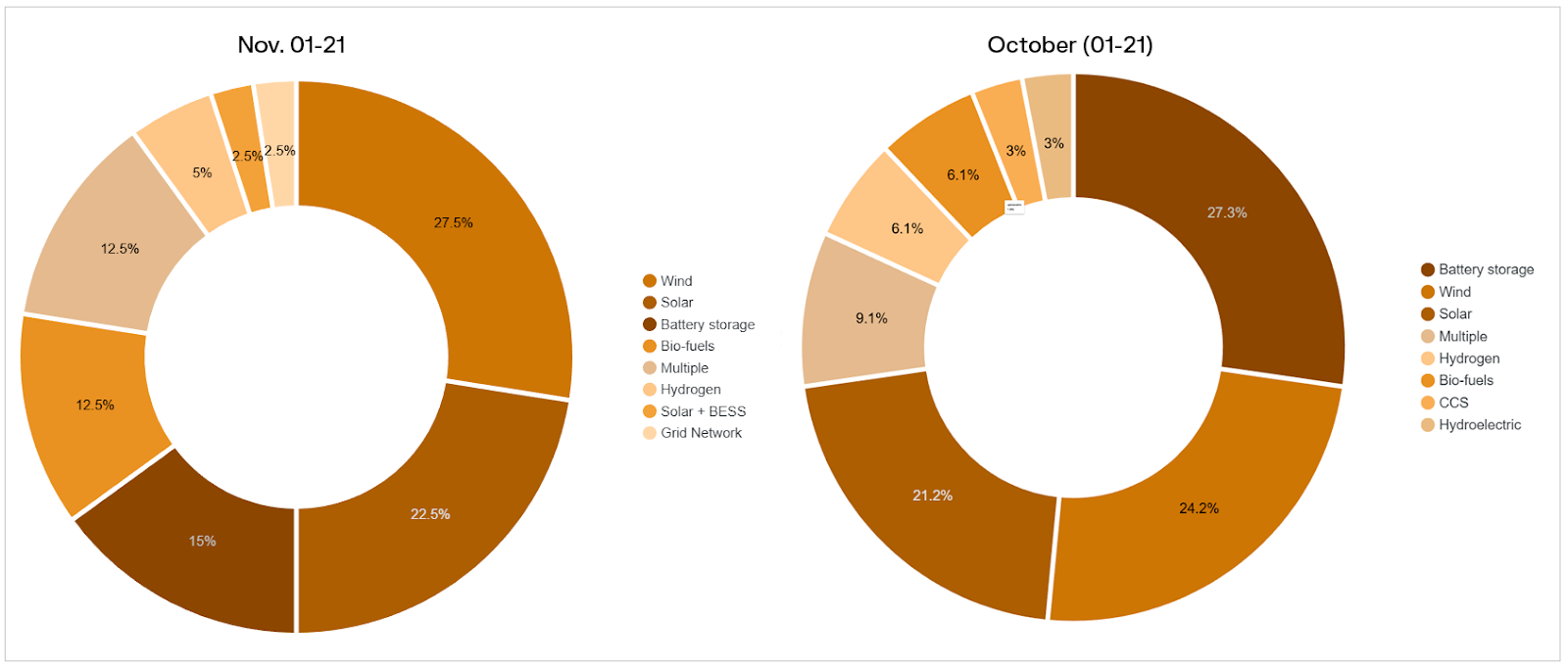

This week, renewable energy M&A in Europe picked up the pace, with 19 announced deals. As winter sets in, Wind and Solar are gaining traction. BESS is down in November, marking its lowest share of dealmaking since August.

In other developments:

- A mega joint venture has emerged in flexible generation. TotalEnergies has acquired 50% of EPH’s 14 GW platform in Western Europe, and integration could have multi‑market impact.

- The UK’s largest infrastructure fund has been launched. The £5.3bn merger between HICL and TRIG brings together core infra and renewables portfolios and is notable for its AUM.

- The Solar sector is heating up with a sizeable raise, a case that’s getting hard to find in November. HoloSolis raised €220m to accelerate a 5 GW TOPCon gigafactory, backed by 20 GW of LOIs. The deal is a boost to Europe’s photovoltaic reindustrialisation.

Are you an experienced dealmaker or just getting started in the sector? Connect with me on LinkedIn and let’s talk.

Deals breakdown

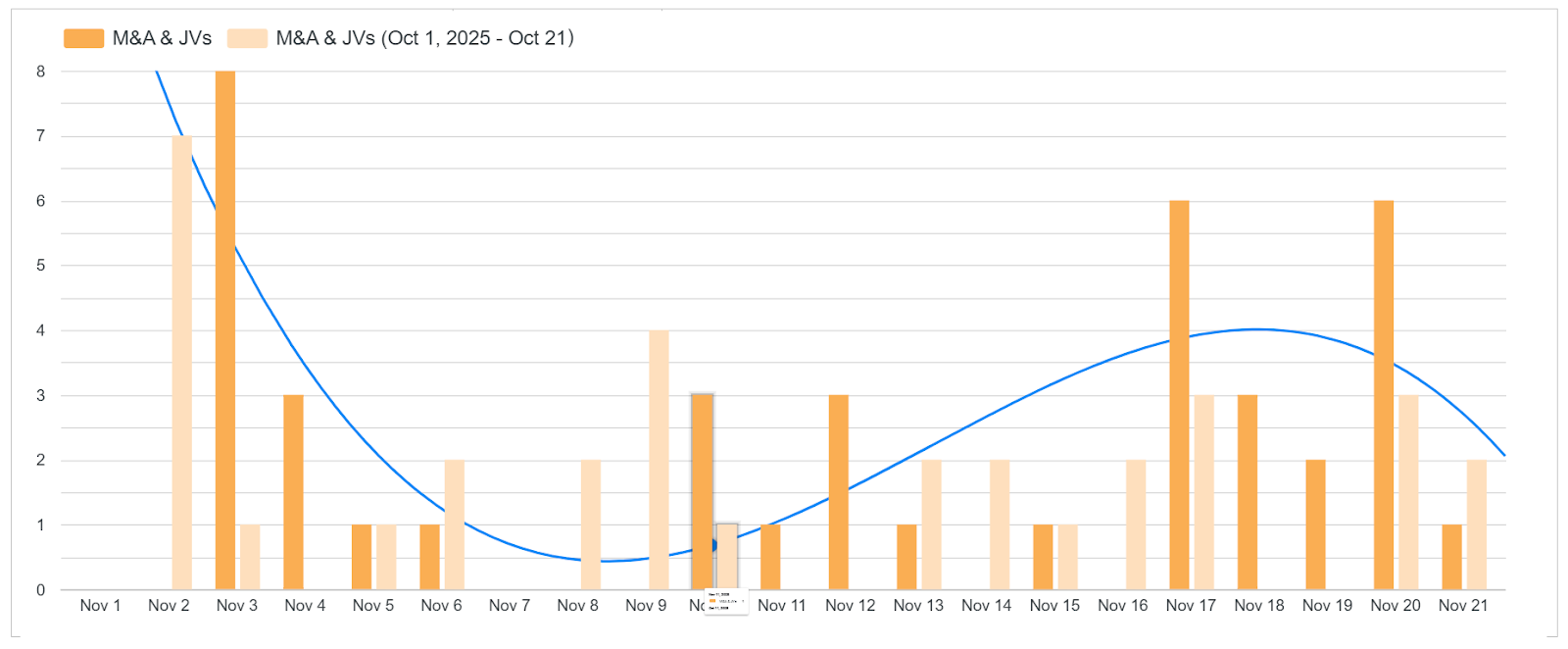

Weekly snapshot | November gathers pace and dealmakers prepare for year‑end

After a quiet start to the month, business has picked up this week. We’ve now recorded 40 renewable energy M&A and JV announcements in Europe (November 1-21). In October, the same window saw 33 deals announced.

This follows the typical pattern we’ve been seeing: announcements bunch around the beginning of the month, followed by calmer weeks.

If that holds, we can expect a softer finish to November in terms of deal flow, something likely to be accentuated as we head into the final month of the year.

Battery‑storage M&A cools in early November; Solar and Wind gain ground

What stands out is less BESS in the headlines. The industry gained global momentum in 2023 and 2024, in step with the energy transition. In 2023 there were BESS 227 M&A transactions worldwide, 5.8% up on 2022.

We’ve seen 2025 hold much of that momentum, but in broad terms the year has cooled for renewables. Although we don’t yet have accumulated 2025 data on deal volume, in terms of deal value reports like PwC’s show a cooling trend in clean energy M&A globally.

PwC also observed a mixed investment climate, which caused global M&A deal value in BESS to show a slight decline in Q2 25, compared to Q1 and the same period last year. Taking a closer look at our November curation seems to reflect this trend. October was a good month for battery-storage, but the number of deals announced in November was noticeably lower.

M&As and JVs involving battery storage went from 12 deals between October 1–21 to 6 in the same period of November. The drop is more pronounced when you look at its share of renewable energy M&A in these two month periods: from 27% to 15%.

December is close and, as negotiation tables empty out for the holidays, deal volumes typically taper off. It’s a good moment to look at 2025 in the round and think about the challenges and opportunities Q1 will bring.

Battery storage

- Germany | Econergy secures option to acquire 435 MW grid-licensed BESS portfolio in Saxony-Anhalt, expanding German platform to 353 MW pipeline and advancing coal-to-clean flexibility hub at Bad Lauchstädt

- Norway | Hydro exits maritime battery sector with USD 30m sale of its full Corvus Energy stake, completing portfolio pivot away from batteries after 2024 strategy reset

- Poland | Northland acquires 300 MW / 1.2 GWh late-stage BESS portfolio from Greenvolt, advancing first large-scale storage build-out and deepening presence in a core coal-to-renewables market

- United Kingdom | Gresham House acquires 100 MW / 200 MWh Elland 2 BESS in West Yorkshire, advancing near-term construction and expanding portfolio with adjacent two-hour project under NESO queue reform

Bio-fuels

- Italy | VisionEdgeOne acquires joint-controlling stake in RE2Sources’ 200 GWh biomethane platform, expanding circular-waste portfolio across six anaerobic digestion plants

- United Kingdom | Vital Energi acquires Port Clarence biomass plant after £175m Nordic Bond raise, accelerating shift into energy-from-waste asset ownership with 30 MWe Teesside project

Multiple

- Europe | TotalEnergies acquires 50% of EPH’s 14+ GW flexible generation platform in €5.1bn all-stock JV, accelerating gas-to-power integration and strengthening clean-firm power position across major EU markets

- France | Neoen sells 760 MW portfolio of 52 operating solar, wind and storage assets to Plenitude, unlocking capital for accelerated growth while retaining long-term asset management role

- Poland | R.Power sells minority stakes in 56 MWp solar and 51 MW BESS portfolio to Eiffel, accelerating capital recycling and scaling PV-storage buildout amid Poland’s coal-to-clean transition

- United Kingdom | HICL and TRIG agree £5.3bn merger to form UK’s largest listed infrastructure fund, combining core infrastructure and renewables portfolios ahead of Q1 2026 completion

Solar

- France | HoloSolis raises €220m to advance 5 GW TOPCon PV gigafactory in Moselle, adding new industrial investors and securing 20 GW of customer LOIs ahead of 2026 construction start

- Greece | JUWI sells 156 MW Clover solar portfolio to Mirova and secures full EPC and O&M mandate, deepening role in large-scale PV delivery across Kozani and Grevena

- Iberia | SDCL acquires 68 MW C&I behind-the-meter solar portfolio from Capwatt, marking fund’s first Iberian entry and enabling €100m deployment push across high-yield PPA-backed assets

- Spain | Solaria launches asset-rotation plan with 42.7 MW PV sales across Recore-backed Spanish sites and PPA-backed Uruguayan plants, funding 10% share buyback and advancing 2028 growth strategy

- Türkiye | Alfa Solar and Astronergy form 50–50 JV for $200m integrated wafer-to-cell plant in Balıkesir, launching 2.5 GW domestic manufacturing hub under HIT-30 high-tech investment program

Solar + BESS

- Italy | Zenith Energy acquires 12 MWp Puglia solar project with 3 MW BESS, expanding national PV portfolio to 110.5 MWp and advancing build-and-monetize development strategy

- Romania | Windin’ Capital acquires 50% of 67 MW solar + 180 MWh storage project in Sebeș, marking fund’s first strategic foothold in local market with hybrid PV-BESS investment

Wind

- Germany | Verbund acquires 140 MW early-stage wind portfolio from Enova in North Rhine-Westphalia, advancing 2027 build-out and supporting utility’s shift toward 25% wind-solar generation

- United Kingdom | National Wealth Fund, Great British Energy and SNIB take stakes in Pentland Floating Offshore Wind Farm, backing CIP-led project set to power 70,000 homes and scale Scotland’s FLOW supply chain

- United Kingdom | Tokyo Century enters UK onshore wind with stake in 122.5 MW operational portfolio from Equitix, adding four ROC-backed farms in England and Wales to its international renewables footprint