Harsh Batra

Harsh Batra

Hello,

This week, Carlyle bought into Edelweiss India’s home finance arm, showing continued appetite for loan solutions from global PEs.

Also, IFC pledged capital to support global firms expanding into India and is eyeing $50 million in equity and debt for NDR Smart Spaces continuing the lender’s interest in growing India’s infra development.

Meanwhile, India (and Japan) bucked a wider APAC slowdown last year in insurance dealmaking.

However, regulatory meddling and momentum continue: the competition court (CCI) reported 149 merger filings in 2025, while the government proposed divesting a 3% stake in BHEL via OFS.

And finally, LPs committed $30 billion to alternative assets in India in 2025, according to VCCEdge data.

I hope you enjoy this week’s roundup – please connect on LinkedIn to discuss how Ideals VDR can help with your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

What do 10 union budgets tell us about India’s tax landscape for dealmaking?

Tax receipts inform dealmakers about the general pulse of the formal economy of any country, which is mainly what they concern themselves with. These factors – other than leverage or borrowings at the geographic or sovereign level – shape valuations and deal appetite.

The happy news is that India has steadily gained in health in the course of the last 10 years, which is well after the late Dr Manmohan Singh’s privatisation drive got underway, and something the current finance minister of nine years has kept going, too.

One of Dr Sitharaman’s biggest agenda items is a vigorous but cautious disinvestment initiative, including bids to privatise public sector banks and insurers. Also important were the GST reforms introduced in 2017 to the annoyance of some small businesses (not always transparent about their earnings) which showed political will, given how much mum and pop shops mean for vote banks.

Rich tax receipts tell investors about corporate profitability, income growth, consumption trends while also enabling strategic acquisitions. Further, greater fiscal room for government lets it spend on priority development agendas over the next financial year.

Naturally, weak receipts do the opposite: demand is likely slow, budget targets remain unmet, and financing is tighter.

These numbers influence deal structuring, valuations and deal timing.

So what’s the score?

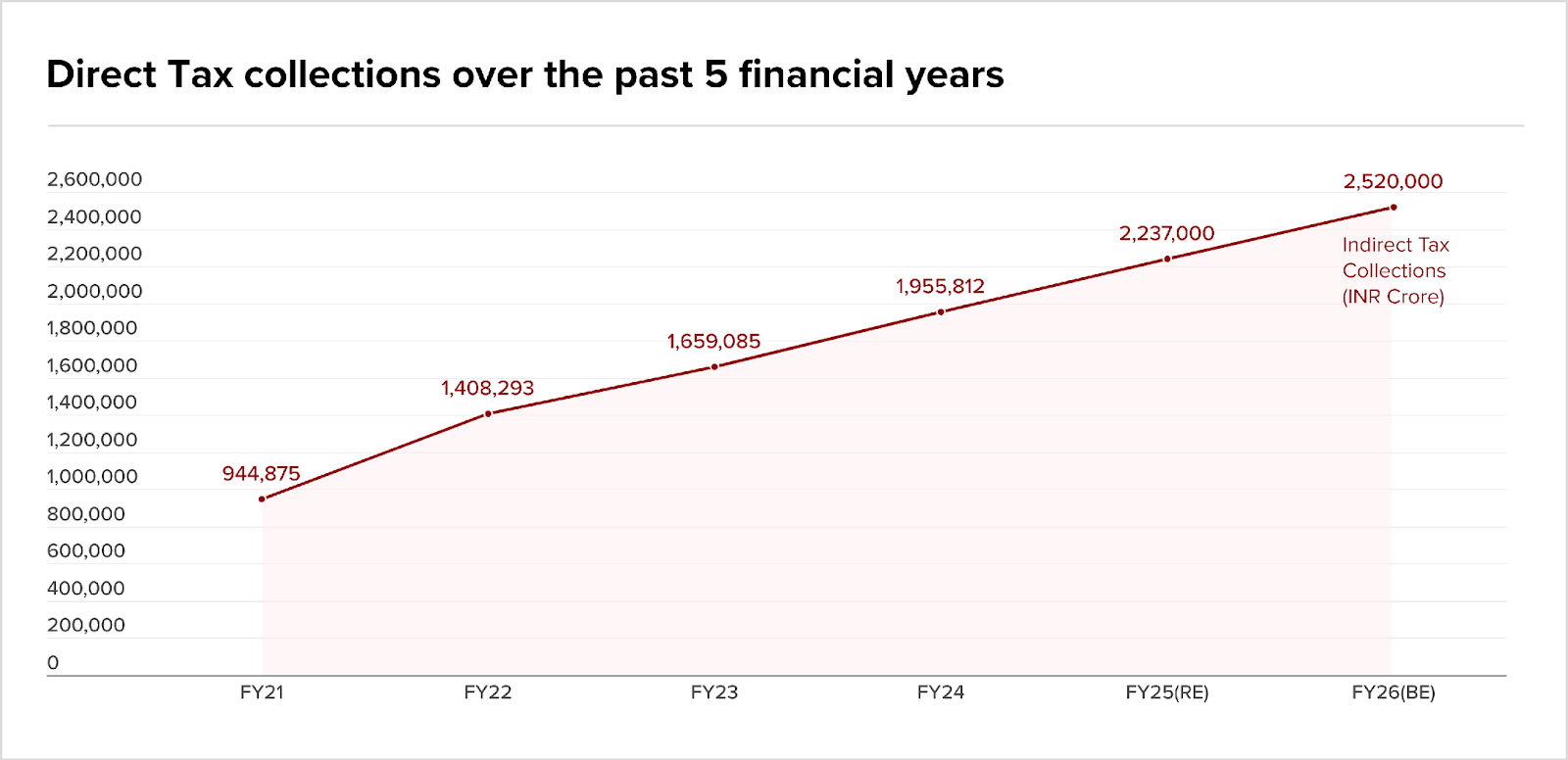

The most recent RBI numbers reveal total tax revenue grew from ₹19.19 lakh crore ($211.9 billion) in FY 2017-18 to ₹44.04 lakh crore ($486.2 billion) this FY.

The share of direct taxes (income and corporate tax) grew to 55% of gross receipts in FY 2023–24, outpacing indirect taxes such as GST due to improved compliance.

Net direct taxes rose from ₹9.45 lakh crore ($104.3 billion) in FY21 to ₹25.2 lakh crore ($278.2 billion) in FY26 (BE), showing consistent upward momentum despite pandemic disruptions.

Direct tax collections rose 9.4% YoY to ₹19.44 lakh crore ($214.6 billion) net until February 10, 2026 driven by corporate tax up 14.51%; but this missed the revised ₹24.84 lakh crore ($274.3 billion) target, with even refunds down 18.82%.

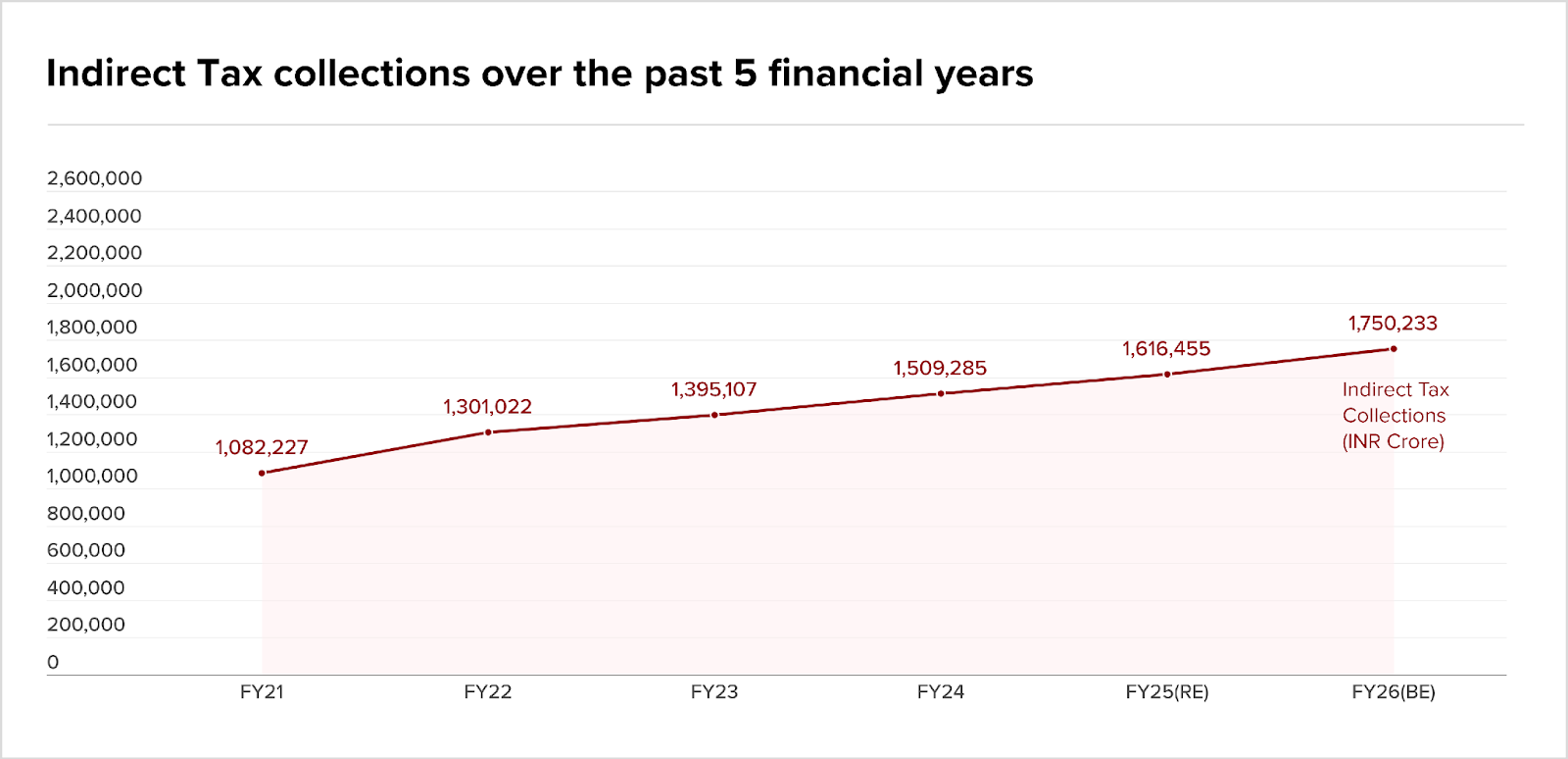

January 2026 recorded GST inflows at ₹1.93 lakh crore ($21.3 billion), up 6.2% YoY, and net GST revenue was up 7.6%.

Similarly, indirect tax collections climbed from ₹10.82 lakh crore ($119.5 billion) in FY21 to ₹17.50 lakh crore ($193.2 billion) in FY26 (BE).

Corporation tax jumped from ₹5.71 lakh ($63.0 billion) crore in FY18 to ₹12.31 lakh crore, a budget estimate ($135.9 billion) in FY27, while GST grew from ₹4.43 lakh crore ($48.9 billion) in FY18 to over ₹10 lakh crore ($110.4 billion) in recent years, per budget data.

What it means for dealmakers

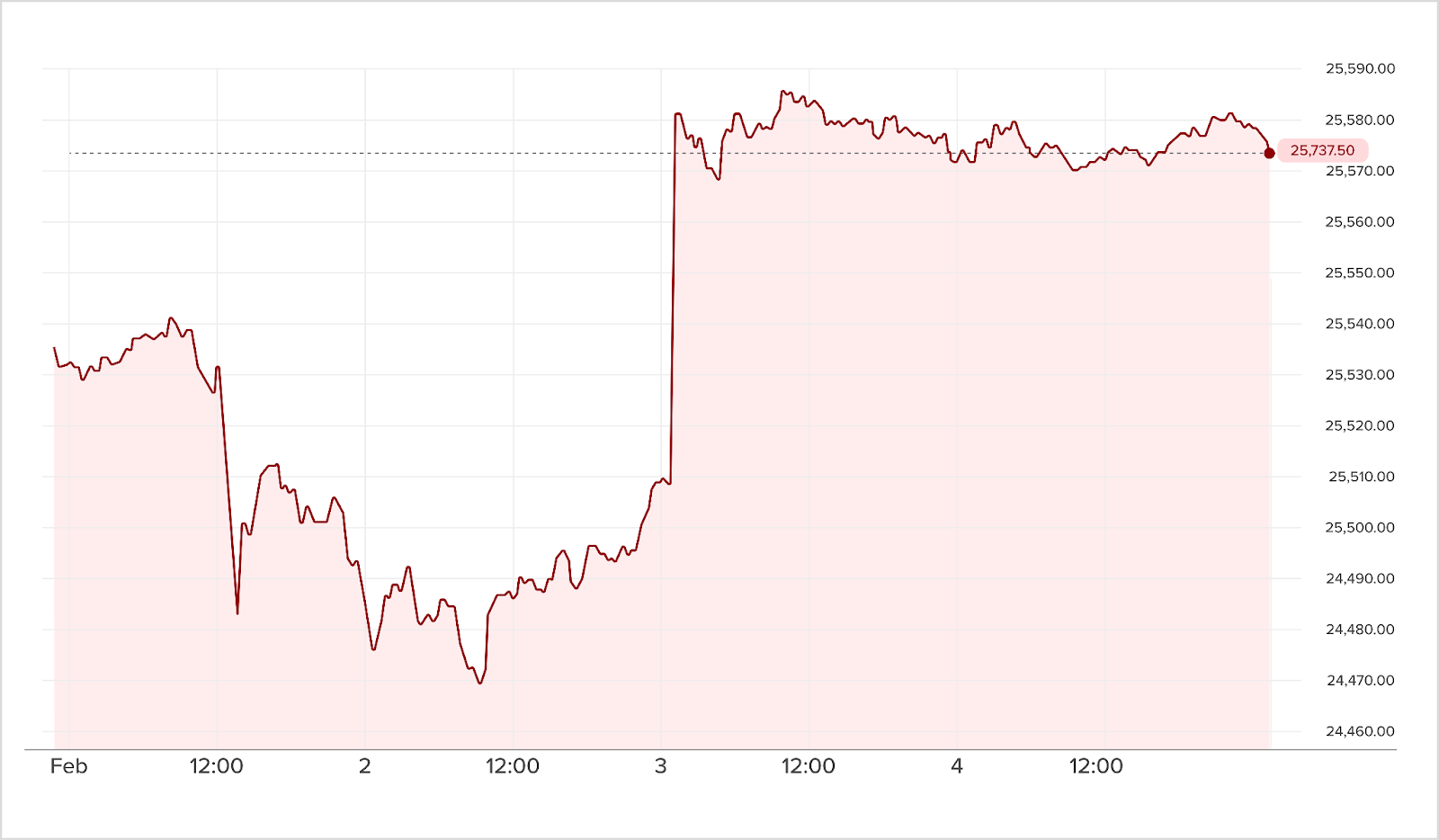

Meanwhile, this is how the markets reacted to the budget:

Buy-side transactors are likely impressed by the strong fundamentals in both GST and direct taxes but that also complicates valuation conversations as Indian sell-side often seek multiples premised on healthy macro indicators.

India will likely continue to see increasing (value if not volume) transactional activity this FY. Sellers can benefit from strong corporate-tax receipts during exit negotiations, while softer growth can accelerate strategic, opportunistic deals. The policy focus on manufacturing and digital services is understandable given their robust tax contributions.

The direct-taxes calculus points to corporate profitability and formal growth. GST resilience signals sustained consumption, and a broader tax base post-GST rule changes in 2017 reflects good policymaking.

These point to a solid pipeline for M&A activity, but missed targets and softer-than-expected direct-tax growth will not go unnoticed by cautious LPs.

Policymakers still need to balance growth, redistribution and fiscal prudence. For dealmakers, that means a generally favourable backdrop but with the usual caveat: stay alert to timing and be prepared for tighter valuation discussions where macro strength has already been priced in.

The rumour mill

- World Bank’s IFC pledges capital for global firms’ India push

- Why PVR-INOX’s popcorn exit signals a deeper multiplex reset

- What founders say versus what filings reveal

- What drove Nykaa’s strong third-quarter performance

- UIDAI mulls seed fund to back startups building Aadhaar-linked solutions: Chairperson

- SMBC’s Strategic Investment In Yes Bank

- SBI overtakes TCS for the first time in decade

- REC-PFC Merger: A Look At Expected Benefits, Deal Mechanics

- Qcommerce platform FirstClub launches service in Bengaluru, plans to enter more cities in coming months

- Preqin billionaires pounce on HgCapital with £69m stake after Anthropic scare hits private equity fund

- Pharma deal value falls in January 2026 amid lower M&A activity: GlobalData

- Over 100 Indian AI startup founders moving to US for funds and talent

- Less is more for AI companies scaling their revenues with a lean workforce

- Large fintechs press the pedal on marketing spends to boost growth

- Investors catch a big whiff of money in D2C fragrance firms

- India’s IIFL Finance set to launch its largest public bond sale

- India credit boom: Private debt, NCDs, ECB reforms, GIFT City

- IFC eyes $50m equity, debt funding for India’s NDR smart spaces

- ICICI Prudential AMC Secures RBI Nod for IDFC FIRST Bank Stake

- Hackers breach govt systems in 37 countries in vast spying plot

- Dream Sports swings to Rs 479 crore loss in FY25 as revenue falls 15%

- Bertelsmann Next enters India with acquisition of Let’s Transport

- Agentic AI breaking IT’s billing model

- True North in talks to invest around $45m in Indian pharma company

- 108 BioCapital leads $20m funding in Pinwheel Therapeutics

M&A news

- VC-backed wealth management startups see revenue rise, losses widen

- Sun Pharma to Maintain Disciplined Approach for Merger-Acquisitions: Dilip Shanghvi

- PFC–REC merger: MOFSL sees operating synergies, retains ‘Buy’ on both PSU stocks

- JIO-Blackrock Joint Venture: Reshaping Investment Landscape

- India and Japan buck trend amid fall in 2025 APAC insurance deal activity: S&P

- IDBI Bank sale: Just two foreign bidders in the fray as Kotak quits the race

- Goldman’s India push bears fruit in India’s crowded Wall Street field

- Goldman Sachs leads construction M&A deal value for 2025

- Getting the call: Chandhiok’s head on winning India’s M&A mandates

- Domestic MFs double their holdings in new-age startups over a year

- Deal Roundup: Carlyle buys into Edelweiss India home finance arm, Court Square sells Kodiak in $2.25bn deal

- The return of the zombie fund

- PeakXV partners leads $15m funding in quick commerce Zilo

Job moves

- Veritas India Board Meeting: Key Appointments and Resignations Approved

- Two EY India partners promoted to global roles

- Svaraj Trading and Agencies Limited Announces Board Changes with New Independent Director Appointments

- Kotak Mahindra Bank CTO Resigns, New CTO & AI Head Appointed Effective February 9

- JCorp establishes sustainable finance framework with Maybank IB as sole structuring adviser

- Grasim Industries Board Approves Re-appointment of Two Independent Directors for Second Term

- EPFO looks for new custodian after 15 years

- DLA Piper adds two partners and a team from Sidley and Weil

- Amazon expands SVP Amit Agarwal’s role to include global selling partner services

Salaries and bonuses

IPOs

Fundraising

- PE/VC firm Jupiter Capital to launch $150 million Asian Private Equity Fund

- EQT gears up to launch new Asia mid-market fund

- Venturi partners leads to $30m funding in Indian pet care startup Supertails

- Sanitary waste recycler PadCare Labs raises $3 million from Nithin Kamath’s Rainmatter, others

- Petcare startup Supertails raises $30 million led by Venturi Partners

- LPs pour $30bn as fresh commitments into alternative assets in India during 2025

- Indian digital finance form Olyv raises $23m from Fundamentum, SMBC Fund

- ImpactAlpha LP/GP: Apollo, TPG and KKR are raising big bucks for energy, infrastructure and impact

- Food delivery startup Swish in talks to raise $30-35 million from Bain Capital Ventures, Accel: Sources

- Flexiloans raises another Rs 375 crore from Fundamentum, Accion and others

- Fintech startup Fibe raises $35 million from IFC in series F round

- E-NAM Economics: Why 1.7 Crore Farmers + 1.3 Lakh Traders = ₹50,000 Crore TAM

- Care.fi raises $8 million in equity-debt funding round

- Actress Samantha Prabhu’s perfume brand Secret Alchemist secures $3 million from Unilever Ventures, others

- TPG gets another LP for $1bn climate fund with India mandate

Compliance/regulatory update

- Wingtech-Luxshare dispute over India asset sale enters arbitration as broader divestment nears completion

- USD/INR Dips as Indian Rupee Gains Momentum from Robust Equity Inflows and Strategic Trade Deals

- The Budget scripts a role for creators but the real test is the performance

- Swaps shut the door on India rate cuts, growth-inflation outlook lifts longer tenors

- Steering The Finance Function Through Union Budget 2026–27

- SGB premature exit date of these bonds today: Rs 1 lakh investment in this gold bond has turned into Rs 3.84 lakh

- RBI is buying time by not cutting the repo rate. Past policy needs a breather to work

- Overnight swap rates suggest RBI pause, hint at possible rate hike

- New Antitrust Framework Strengthens CCI’s Grip on Market Practices

- India’s earnings in focus as US trade deal redraws winners and losers

- Govt proposes new defence acquisition procedure aligned with evolving geo-strategic landscape

- Govt assures equal tax treatment for domestic, foreign data centre players; industry seeks deeper value capture

- Government to divest 3% stake in BHEL through OFS, option to sell additional 2%

- Exclusive: India regulator stalls new exchanges’ entry into options market, sources say

- Economic Survey 2026 – Highlights

- Domestic and foreign investors to get equal tax benefits on data centres: Union minister Ashwini Vaishnaw

- Cian Healthcare Limited Constitutes New Board Committees Following NCLT Resolution Plan Approval

- CCI sees 54 antitrust cases, 149 merger filings in 2025; New rules aim to speed up approvals

- Budget tax tweaks to revive buyback momentum of cash-rich IT large caps