Harsh Batra

Harsh Batra

Hello,

This week, you might have heard that Indian markets were rewiring following the tariff shocker (see Market Trends below).

And an expected RBI rate cut in October, means financing mathematics will shift, while cheaper debt will make some deals more doable.

Nonetheless, India Inc is doubling down on overseas borrowing after a sovereign upgrade.

At the same time, net ECB inflows of $4.6bn from April to June suggest funding remains available, keeping cross-border bids and liquidity alive.

And finally, big tickets loom as the Ambanis plan to list Jio by mid-2026, which may reset benchmarks and haul in fresh liquidity; and Tiger Global-backed Urban Company is targeting a $1.7bn valuation for an IPO.

Yet, it’s not all positive business news, as Nazara pulled out of Moonshine after the recent gaming clampdown.

I hope you enjoy this week’s roundup — please connect on LinkedIn to discuss your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

Macro vs. M&A

Deal Street is no stranger to uncertainty.

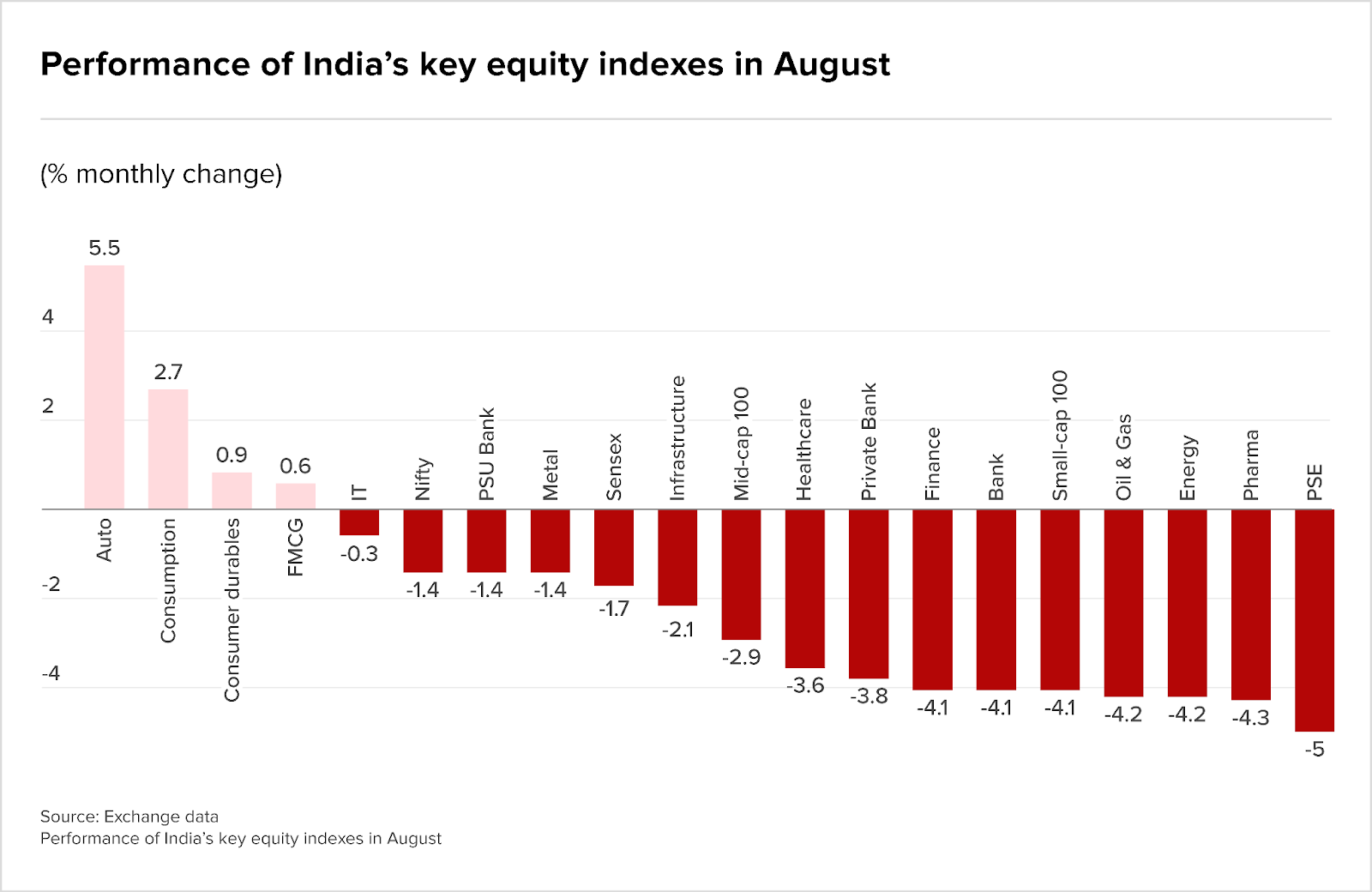

India’s 7.8% GDP growth this quarter and the US tariff shock have done two things at once: they’ve buoyed confidence in some pockets and added an instant risk premium to export-exposed assets in others. Capital-market signals are mixed (no one knows what’s about to happen next, though here is a helpful JPMorgan calendar to keep track).

Dealmakers are squirreling away: strategic plays such as Capgemini’s Cloud4C move and the expected Tata Capital IPO show companies will act when value is clear.

Still volatility is real. One tariff headline wiped out roughly ₹4 lakh crore ($48.2bn) of investor wealth in a session, and India underperformed Asian peers last week.

What this means for buyers

M&A will be used as a de-risking tool, not just a growth lever. Buyers are looking for three things: predictable cash flow; minimal tariff exposure (who bears the cost if tariffs change, for example?); and recurring revenue or loyal customers.

PE and strategics are active but picky: think autos and adjacent consumption plays, IT services with steady renewals, proven SaaS, and infrastructure contracts that pay rent.

Export-dependent textiles, small pharma and junior manufacturers sit on the distress pipeline and will likely be consolidation targets. That means roll-ups for buyers who can integrate quickly and keep unit economics intact.

The state of play (and peril) is such: macro trends remain supportive (e.g. growth and domestic demand) but policy shocks, FX swings and higher local yields will reprice risk, especially for export-exposed midcaps. Strategics and PE will keep buying, but they’ll choose resilient cash engines. Domestic demand names hold value; export exposure is getting discounted.

When the going gets tough, legal drafting may be the new alpha

Another impact of the tariffs is that deals will likely be re-engineered to survive shocks.

Expect earnouts and contingent value rights (CVRs) tied to tariff bands or volume recovery (a promise to pay if certain events happen). Price collars will limit who wins or loses from big swings; seller notes will bridge valuation gaps when cash is tight.

Diligence will pore over customer concentration, supply chains, and FX-hedging policies, potentially leading to extended deal timelines due to risk aversion and more intense negotiations.

Positive business sentiment will need clearer trade policy, softer rates and INR stability. Or the downside will be a prolonged tariff war, disorderly FX and rising yields. The best dealmakers can do is be ready to consolidate when markets hand them an opportunity.

The rumour mill

- India’s Emerging AI Ecosystem and Reliance’s Strategic Alliances: Assessing the Investment Potential of a High-Growth Infrastructure Play

- Authum Investment & Infrastructure approves divestment of up to 20% stake in Billion Dream Sports

- Blast-off for Indian spacetech, but growth funding stays grounded

- Temasek in talks to invest in Indian space tech startup

- IDBI Bank divestment: BIG update on LIC shareholding ahead of stake sale

- Billionaire Ambani plans to take Reliance Jio public by mid-2026

- 360 One PE fund settles Sebi proceedings on violating anti-layering norms

- Byju Raveendran faces $235M enforcement move by QIA

- AIBOC Opposes IDBI Bank Privatisation

- VC firms including Accel team up for $1bn-plus Indian tech dealmaking alliance

- Indian firms delay expansion plans amid demand, trade uncertainty: BofA

- Deutsche Bank puts India retail banking business up for sale

- India’s Nazara technologies terminates deal to buy Moonshine after gaming ban

- Krafton Plans $50m Yearly Investment in India as Real Money Gaming Banned

- Nalco Exploring Joint Venture Partnership With Coal India, NTPC: CMD Brijendra Pratap Singh

M&A news

- A forward-looking defence acquisition policy can unlock foreign tech transfer and investments

- TPG invests $150 million in Hero Electronix-owned Tessolve

- BSE Capital Markets Index: BSE gets a new index to track sector performance

- India Inc doubles up on borrowing overseas after sovereign upgrade

- Indian equities back in the green on improved GDP show

- Fresh registrations of companies surge despite tariff shock

- Capgemini seeks Competition Commission’s clearance to acquire Cloud4C

- Future Retail’s iconic brands Big Bazaar, Foodhall up for auction with ₹155 cr reserve price

- NCLT approves ₹614 crore resolution plan for stalled Acme Realities

- Writ Petitions Against Air India Not Maintainable Post-Privatization: Bombay High Court

- India’s eSports wins official backing, but the real game starts now

- Cumin Co secures $1.5 mn led by Fireside Ventures to accelerate innovation & manufacturing.

- Citibank Strengthens Asia-Pacific Investment Banking Leadership; Reports 15% Revenue Growth

- India’s Nutraceutical M&A Boom: Why Wellbeing Nutrition’s Strategic Sale Signals a High-Growth Opportunity

- Under Pressure: How Tax Insurance Supports Certainty in Cross-Border M&A

- At 59.3, manufacturing PMI rises to nearly 18-year high in August

- Net ECB inflows rise to $4.6 billion in Apr-Jun 2025, shows RBI data

- JPMorgan to boost corporate banking in India on investment jump

- India’s defence tech hits funding milestone, but exits remain a concern

- Editor’s take: Profit risks pricing out a third of India’s middle class

- India’s factory output grows at quickest pace in 17 years

- Top 100 Early-Stage VC Leaders Powering India’s Tech Innovation

- IBC reform moots skirting lender disputes for firms’ turnaround plan

- Texmaco Rail and RVNL to form new JV company

- India clears acquisition of stake in apparel and luggage maker

- Inox Wind redeems $6 billion preference shares held by promoter company

- Private Equity And Sports – Is It A Match?

- Sebi clears LIC’s reclassification as public shareholder in IDBI Bank amid divestment plan

- Indian markets tumble as US tariffs trigger heavy sell-off Rs4 lakh crore investor wealth wiped out

- In brief: Japanese LP commits to Indian impact manager

- Govt extends Export Obligation Period to provide relief to textile exporters

- Govt Must Allow Domestic Savings to Play a Greater Role in Private Markets, Says Gopal Jain

- Sudhir Variyar: Global Institutional LPs Back Platforms That Can Deliver

- India has global capital pursuing opportunities across asset classes

- Mapletree: India is becoming a compelling case for global investment

- India is coming of age, says Stepstone

- LP pressure drives GPs to digital onboarding

- Instant View: India’s economy grows 7.8% in April-June quarter

- CCI approves PSA India takeover, V.I.P. Industries stake deal

- Private capex likely to rise 21.5% to ₹2.67 lakh crore in FY26: RBI bulletin

- WNS Shareholders Overwhelmingly Approve Acquisition by Capgemini

Job moves

- Citi Nets Ex-J.P. Morgan Veteran Kaustubh Kulkarni as Co-Head of APAC Investment Banking

- Injeti Srinivas likely to be appointed NSE chairman

- Change of Cart: Tata plans CEO change at BigBasket

- Government appoints former RBI governor Patel as IMF ED

- HSBC AM joins peers with private equity fund targeting wealthy

- Andrew Scott, WPP’s global COO and M&A guru, to step down after 27 years

- CPPIB names new head for $20 bn India investment franchise

IPOs

- Cube Highways Plans $600 Million India IPO, Hires Four Banks

- GIC-backed Indian stock broking platform Groww get ipo nod

- Tiger Global-backed Urban Company targets $1.7b valuation in India IPO

- Upcoming IPO: Leap India files draft papers with Sebi to raise ₹2,400 crore via public issue

- IPOs targeting aggressive valuation will face resistance in volatile times: Ganeshan Murugaiyan of BNP Paribas India

- Tata Capital’s $2B IPO set for September 22 week

Compliance/regulatory update

- GST meeting, expiry shift and auto sales data among 11 factors that’ll steer D-Street this week

- Tariff tensions push rupee to record low: Why is the RBI holding back?

- Government bond yields BOB report pegs 10y in 6.50-6-60% range; RBI status quo, US rate cuts key drivers

- India bond market watchers expect RBI to step in as yields spike

- India’s economy resilient but US trade policies a risk: RBI bulletin

- Why RBI’s MPC may cut interest rates further in October

- RBI’s inflation targeting: What works can be tweaked to do better

- India’s top lender SBI taps dollar debt days after nation’s rating upgrade

- Uncertainties related to India-U.S. trade policies continue to pose downside risk: RBI Bulletin