Harsh Batra

Harsh Batra

Hello,

This week, a fire sale of a sought-after fund raised alarm over an Asia-wide PE slump – stress that may affect deal pricing and exits.

Meanwhile, it is rumoured RBI may be looking into a rejig of asset reconstruction in FY26 which could directly impact distressed deals. This, while others predict fewer deals and bigger bets as ticket sizes and buyer behaviour level up.

And finally, India’s first-ever ‘class action suit’ materialised, reported CapTable, which questions shareholder rights and may mean governance risk comes higher on investor checklists in the future.

I hope you enjoy this week’s roundup — please connect on LinkedIn to discuss your next M&A deal.

Let’s dive in.

Share your thoughts on AI for a chance to win $100

How are you currently using AI during M&A deals? We’re surveying top dealmakers on how they use AI as part of a major research project.

Please complete this short survey and you’ll be entered into a prize draw to win one of three $100 Amazon vouchers.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

The ratings game – why care?

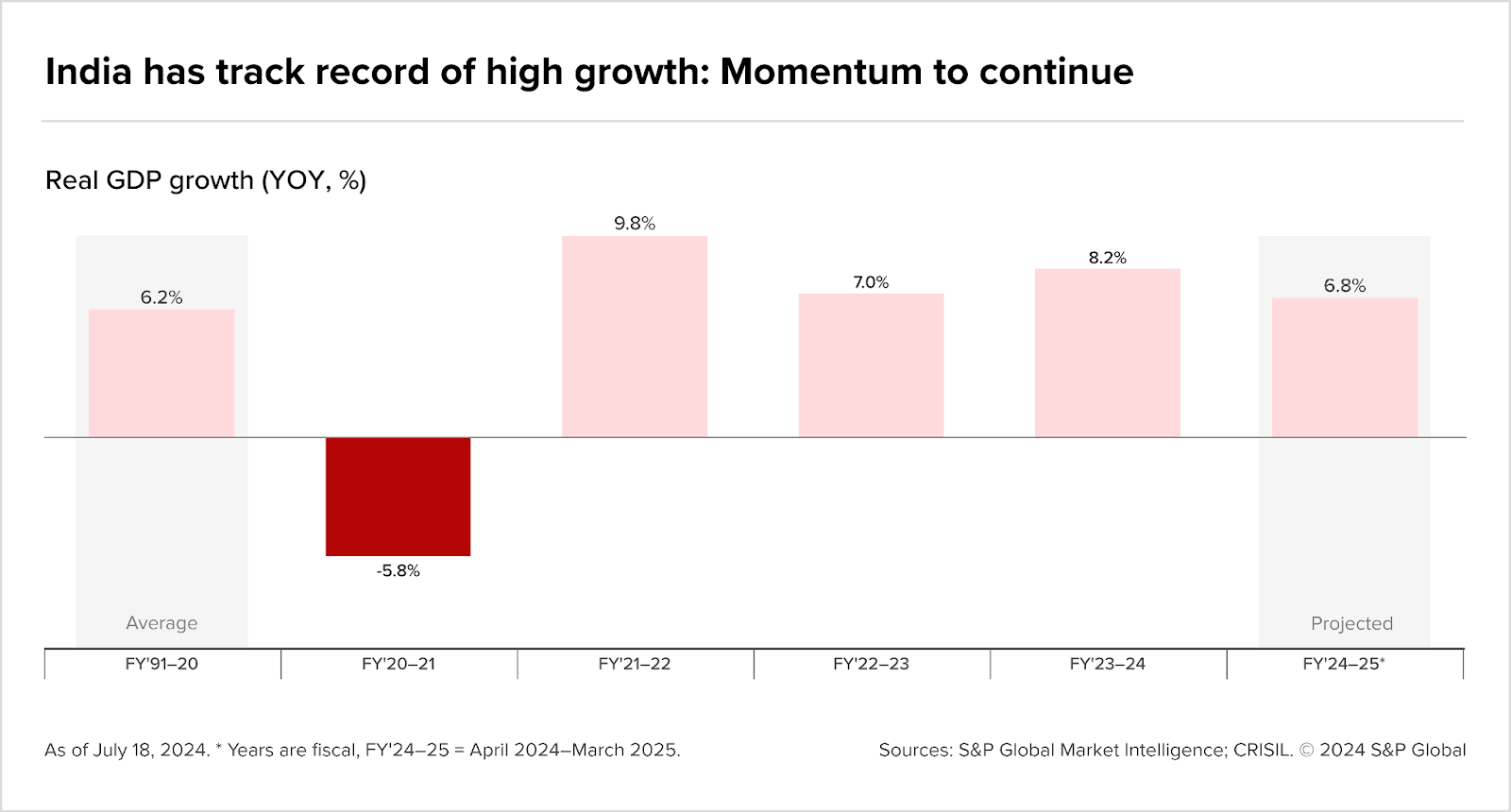

S&P Global’s recent reports are unequivocal about India’s momentum: the economy is on track for robust 6.5% growth. The subsequent credit upgrade from Japan’s R&I only reinforced this.

But the other big ratings agencies Moody’s and Fitch take a different view. They rate India at Baa3 and BBB-, the lowest investment grades, citing fiscal vulnerabilities and structural constraints. They believe public debt above 80% of GDP (FY24) and interest payments consuming a quarter of government revenues are both downers.

The curious case of banking and governance

While non-performing assets (NPA) may be falling, Fitch points to risks from credit concentration and under-capitalised public banks that may need government bailouts.

Further, dealmakers have long griped about lack of contract enforcement, regulatory unpredictability, infrastructure bottlenecks, and uneven regulation across states – India’s different and diverse geographic regions.

Yet, both agencies maintain a stable outlook, expecting fiscal consolidation and reform.

The S&P/CRISIL take

The agencies say India’s momentum is real and FY24-25 indicates growth will outpace its emerging market peers.

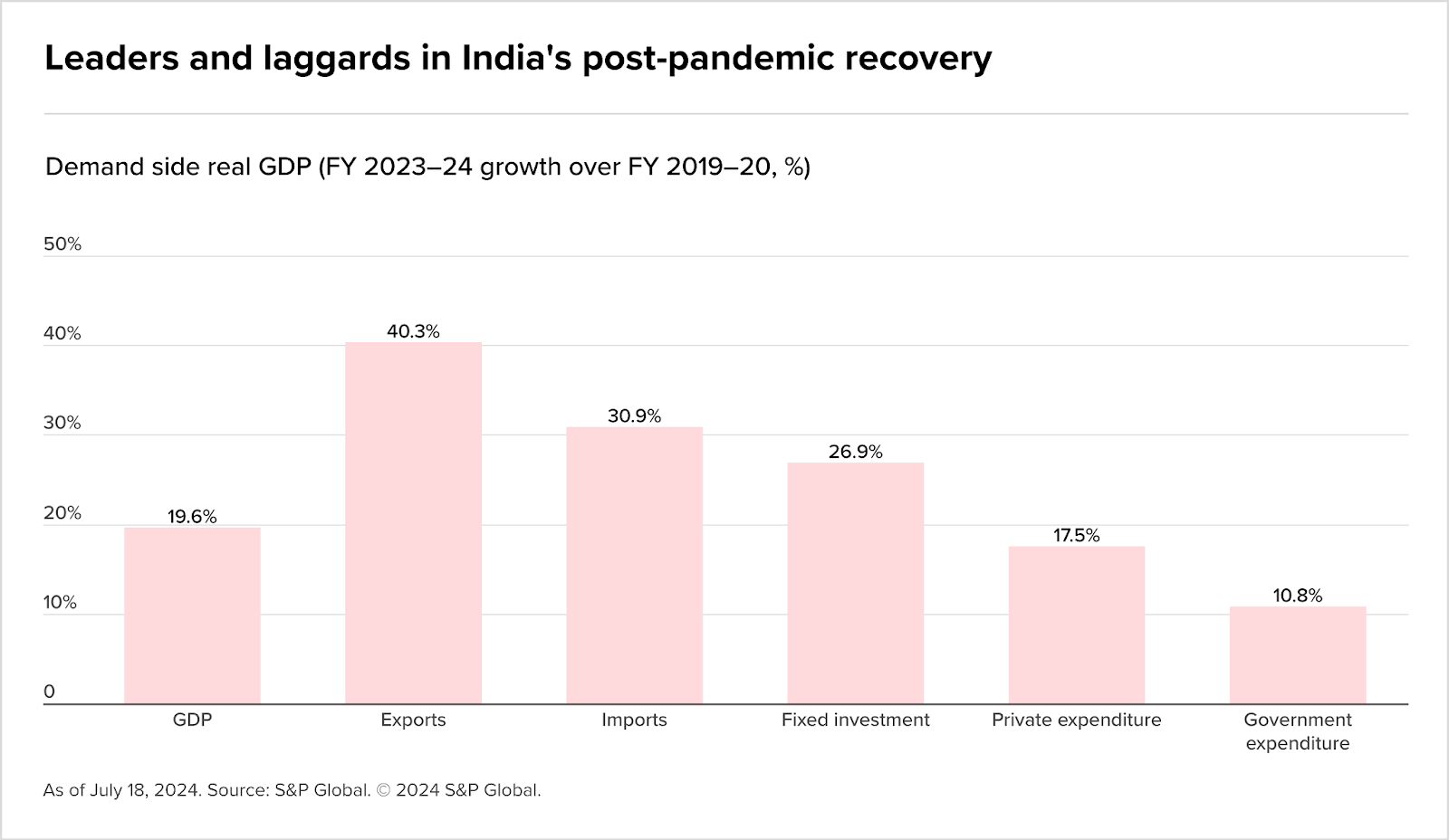

For M&A, this signals a strong domestic demand cushion for buyers in consumer, healthcare, logistics, and financial services.

Exports and fixed investment will continue to lead. For dealmakers this means two things: cross-border investors will chase export-linked manufacturing and supply chain plays, while capex-led activity in construction tech, energy transition, and industrial services creates space for private credit.

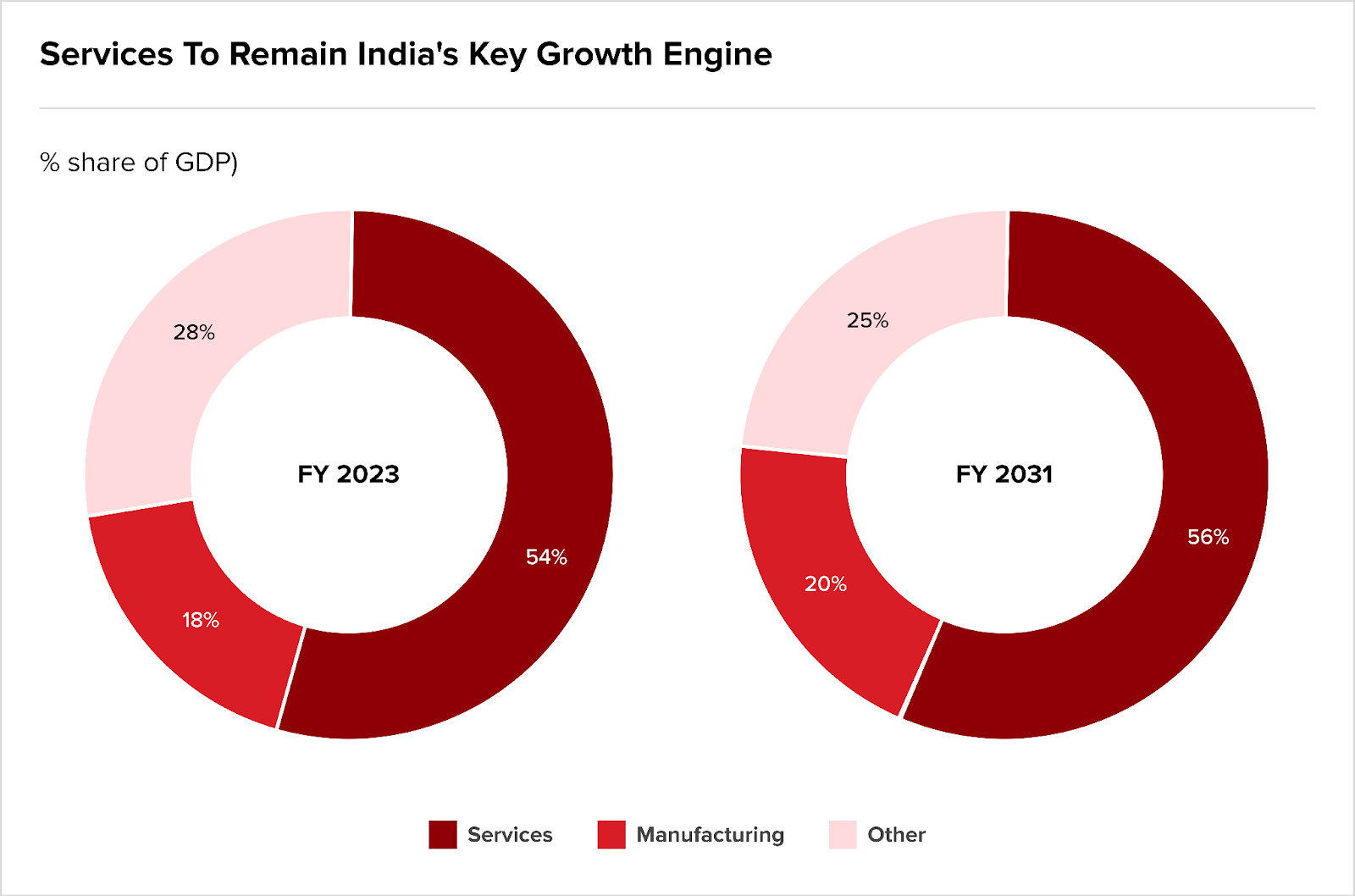

Back in 2023 (see chart below), CRISIL /S&P Global projected services to remain India’s growth engine into 2031 – but we all know a lot changed post-Trump, and matters remain mercurial.

And Jefferies places infra over IT

India’s growth engine for three decades was IT – delivering steady service exports, high margins, and jobs. Jefferies argues India must now switch its focus to infrastructure (roads, ports, railways, power, renewables, logistics, and data centres).

Already, the government is pushing high-value, on-shore manufacturing such as of electronics, semicon, batteries, EV components, pharma – not literally infrastructure, but these will need reliable power, efficient ports and last-mile logistics to thrive.

Domestic conglomerates like Adani, Reliance, Tata, and L&T know this and are looking to shape the remix needed in the coming era as adverse tariffs come into force.

Now the bet is, India can cash-in on the China+1 trend.

Ports on two coasts, expanding container capacity, and the Dedicated Freight Corridor all strengthen India’s prospects. The question: can it become a credible alternative to China?

India’s IT won’t vanish. It may pivot to powering logistics platforms, infra analytics, and smart networks, ensuring the sector remains ‘too big to fail’ as it contributes nearly more than 7% to India’s total GDP.

Why this matters for deals

Deal flow will be shaped by two cross-currents: a rotation toward infrastructure and manufacturing that demands patient capital, and persistent external risks (tariffs, trade slowdowns, geopolitical uncertainty) that will weigh on exits and valuations.

Japan’s upgrade fits here too: R&I’s decision consolidates S&P’s optimism and suggests more supply of infra and energy transition assets, more distressed opportunities, and more complex cross-border deal structures.

The rumour mill

- Climate-focused VC momentum capital eyes bigger fund

- Actis to exit residential real estate joint venture with Indian developer

- RBI considering major rejig of ARC industry norms in FY26, sources say

- Fire sale of sought-after fund raises alarm over Asia private equity slump

- India’s landmark GP-led marks a 3x return within 18 months

- Keppel to Sell One Paramount for Rs. 2,750 Crore

- Thyssenkrupp receives non-binding bid for steel unit from Jindal Steel International

- India’s pension regulator plans to widen investment options for better returns, chairperson says

- India’s Paytm unit partners with JioBlackRock to launch active equity fund

- SMBC to purchase additional 4.2% stake in India’s YES Bank

- Germany Woos Indian Workers Spooked by U.S. Visa Changes

- Piramal Enterprises sets record date for merger

- India’s insolvency reform aims for speedy resolutions. Is it also good for value recovery?

- Metropolis Healthcare’s acquisition spree deliver sustainable profits?

- Realty services company TCC Concept to acquire Pepperfry

- China’s SAIC Motor to cut stake in Indian JV – report

- Arnya RealEstate-Supreme Universal to set up ₹1000 Cr Real Estate Equity Platform

- India’s Somerset eyes healthcare access, affordability as Fund III nears close

- KKR closes third acquisition in India’s Kerala state with Meitra hospital: report

- India’s Swiggy to exit Rapido as ride-hailing firm forays into food delivery

- Indian Hotels shares in focus as company plans to exit New York’s Pierre Hotel at around $2 billion

- AMD open to acquisition of firms in India as part of expansion plan

- Strategic cross border synergies global brokerage firms Sumitomo Mitsui 20% stake in jefferies as a catalyst for Asian-market expansion and earnings growth

- Setback for Vedanta as govt denies extension for Cambay basin oil, gas block

- NTPC agrees to 49% in Chhabra plant JV, but wants mgmt. control

- Emaar Confirms No Stake Sale in India, Eyes Strategic Joint Ventures

- CRISIL to acquire McKinsey PriceMetrix

- Geopolitical Friction Leads SAIC Motor to Reconsider India JV

- CAM pilots Dassault Aviation’s India expansion, majority acquisition in Reliance ..

- EoI for Xalta Food and Beverages invited by Oct 7

- NCLT admits Reliance Home Finance into insolvency proceedings

- EoI for ARS Energy invited; Nov 8 is last date for submission of resolution plans

- CBI files chargesheet against Anil Ambani Group, Yes Bank officials in Rs 5,010 crore fraud case

- M&A deals: Valuno, PayU, Mindgate, Xplor Technologies, Ezypay, DecisionPoint Technologies

- Brigade Enterprises eyes Rs 1,200 cr sales from JV project in south Bengaluru

- Emaar Properties not to sell stake in Indian entity, may form JV with big firms including Adani

- NBFC Dhruva Capital announces merger with microlender Vector Finance

- India may see minority stake sales in half a dozen state firms, divestment secy says

Salaries and bonuses

M&A news

- How AI is quietly rewriting the M&A sourcing playbook in India’s startup ecosystem

- Markets extend losing streak, FMCG bucks the trend

- S&P retains India’s GDP growth forecast at 6.5% on strong domestic demand

- India’s Growth Outlook

- India’s Private Credit Market

- Side letter: Fund finance inflows

- Side letter: Cost calculation controversy

- Blackrock PE co-head: Semi liquids could facilitate model portfolio adoption

- Dr. Agarwal’s says merger valuation structured through fair and transparent process

- Owens-Corning’s acquisition by Triumph Composites, Quartz Fibre cleared in India

- The next era of private credit

- From potential to performance: Using gen AI to conduct outside-in diligence

- Jefferies bets India next big wealth engine will be infrastructure, not IT

- India secures third credit rating upgrade in FY26 as Japan’s R&I lifts outlook

- Toray Industries and MAS Holdings announce joint venture in Odisha, India

- India’s Urbanization Curve Attracts Private Equity

- S&P retains India’s FY26 GDP growth forecast at 6.5%, expects 25 bps RBI rate cut

- JSW Paints-Akzo Nobel India Acquisition: CCI nod for Rs 12915 crore stake sale – Details

- Privatisation is dead. Can disinvestment revive India’s fiscal fortunes?

- Singapore’s Duro Capital launches first India onshore fund

- Beyond the Buyout: SE Asia remains a mixed bag for PE investors

- Arnya, Supreme Universal set aside Rs 1,000-cr for redevelopment projects

- India to be world’s third-largest economy by 2030, says S&P Global Ratings

- SBI completes divestment of 13.18% stake in Yes Bank Limited (YBL) to Sumitomo Mitsui Banking Corporation (SMBC)

- Fewer deals, bigger bets: Is India’s M&A market leveling up?

- Mortality in hospitals rises after PE takeover, says Harvard study

- Inside India’s first class action against Jindal Poly Films

- CCI clears PNC Infratech’s bid to acquire Jaiprakash Associates

- Apollo restructuring CC clearance boosts healthtech scale

- India is more resilient against global shocks as its large domestic market provides a buffer: S&P Global

- Emerging Market Private Credit Steps Up

- REITs as equity: Ready for corporate action and M&A

- Spice and crunch: Why India’s namkeen market is hot

- Capital markets pivotal to India’s infrastructure growth: SEBI Chief

- Stock markets steady on SIP flows: Jefferies says mutual fund inflows preventing crash; stocks seen trading sideways

Job moves

IPOs

- InvAscent-backed Malladi Drugs planning Rs 1,200-crore IPO, holds talks with banks

- Walmart-backed Indian payment app Phonepe files for IPO

- India’s Purple Style Labs files DRHP for $75m IPO

- India’s Infra.Market raises Series G funding ahead of IPO

- JP Morgan sees India IPO value surpassing last year’s $20.5bn

- JPMorgan sees strong IPO pipeline in India despite high PE and promoter exits

- JPMorgan sees D-Street building on record levels of IPO activity

Fundraising

Compliance/regulatory update

- India not yet ready for single-rate GST: FM

- RBI unlikely to rush into rate cuts despite US Federal Reserve easing, say experts

- IBC amendments to push promoters into early settlements with creditors

- CCI Clears IRB InvIT Fund’s Acquisition of Key Tollway SPVs, Anahera Investment

- RBI likely to hold rates at 5.50% on October 1 and through 2025: Reuters poll

- CCI nod for Apollo restructuring healthco Keimed to merge into healthtech separate listing plan on track

- Another 25 bps rate cut best possible option for RBI: SBI study

- The Need for Speed – Fast Track Mergers

- The Four Pillars of Change: Unpacking India’s New Fast-Track Merger Regime