Harsh Batra

Harsh Batra

Hello,

This week, JSW Steel finally secured Supreme Court clearance for its long-pending Bhushan acquisition.

Meanwhile, Infra.Market filed for a ₹5,000 crore ($602 mn) IPO through the confidential route.

And finally, India’s semiconductor policy push seems to be working with JVs from UST–Kaynes and SEALSQ–Kaynes which aim to localise advanced manufacturing.

I hope you enjoy this week’s roundup — please connect on LinkedIn to discuss your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

Startups: ‘Who moved my lunch?’

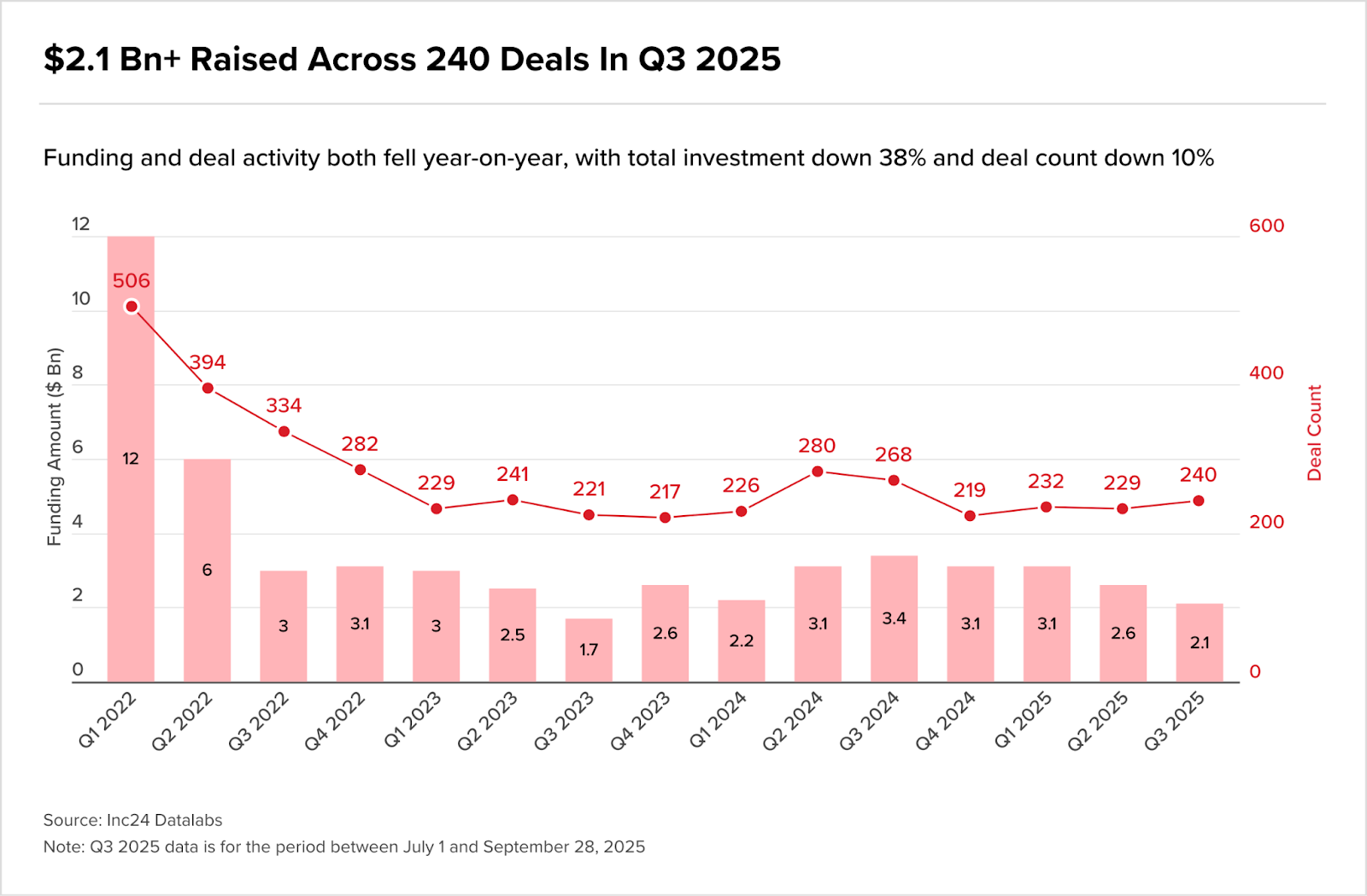

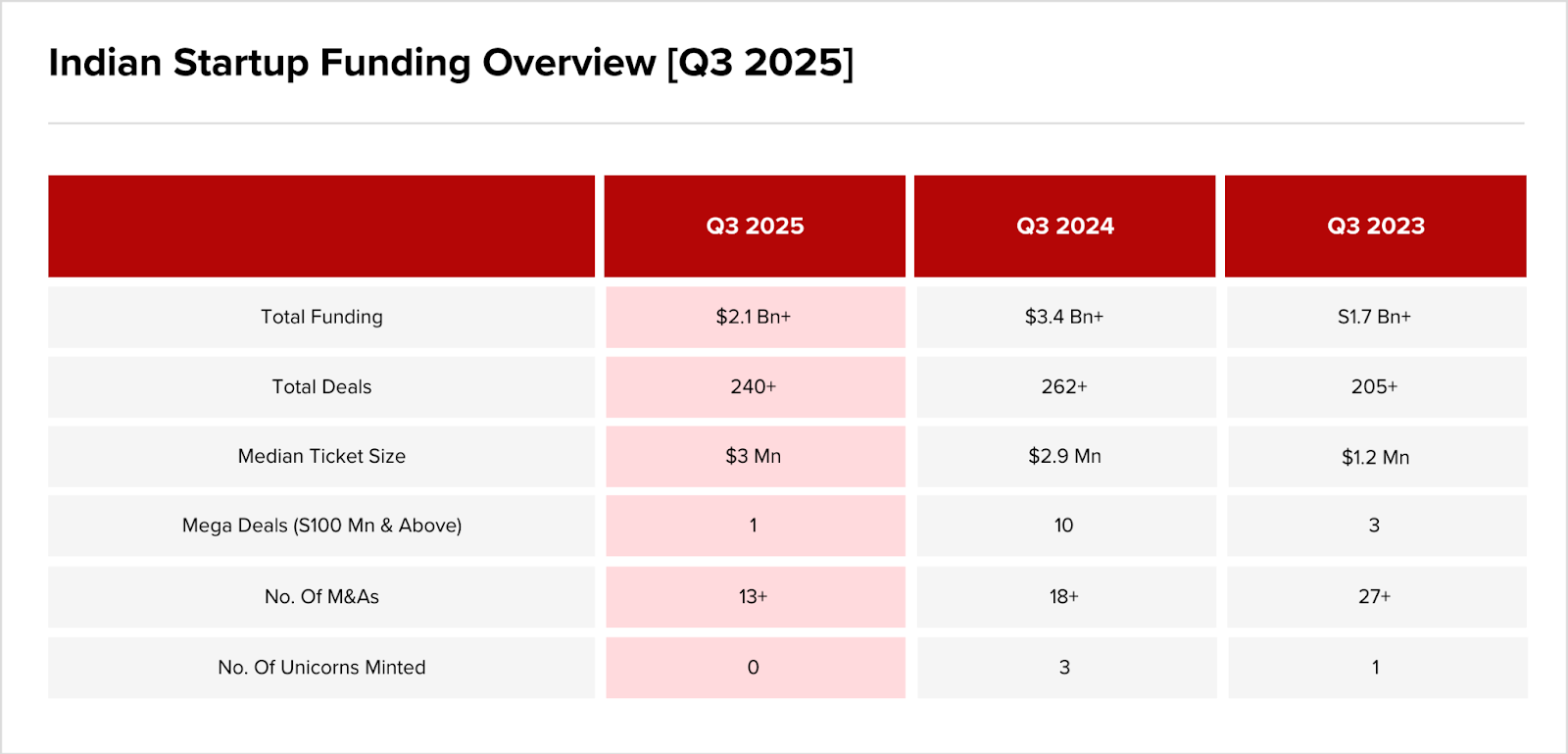

Startups are facing a challenging fundraising environment. In India, data shows that startup funding fell by almost a quarter in the first nine months of 2025 (to $7.7 bn, down 23% YoY), with early-stage deals particularly hard-hit.

Further: Regard the downward trend in Q3.

But despite bad weather, a handful of IPOs offer a silver lining. PhonePe, Urban Company, Groww, Capillary Tech, Infra.Market, Simple Energy and Aequs are all in the public listing pipeline.

Some founders have even boosted stakes ahead of listings, signalling conviction. Plus, the RBI’s recent bulletin on the surge in UPI transactions bodes well for the country’s fintech, as policy momentum around semiconductors appears to be delivering.

Exits look steady: the VIP Industries promoter sale (₹343 crore) and Somerset Indus’ 4x exit are notable markers. KKR is zooming in on hospitals with several deals, while JV activity hums along with Bharti-Warburg raising $450 million in debt. Rumoured cross-border transactions such as Indian Oil–Vitol and Reliance/Meta may yet carry hope.

India’s secondary sales markets are also maturing as we discussed in a previous edition of Teaser.

The country’s startup ecosystem remains an important cog in its capital markets and more IPO- and M&A-driven liquidity may be expected, even as VC inflows slow. For now, sector bets in mobility, commerce, infrastructure and clean-tech look reassuringly meaningful.

Yet notwithstanding India’s $7.7 bn haul in the first nine months of the year, zooming out a bit, one does wonder, where the real global capital actually is.

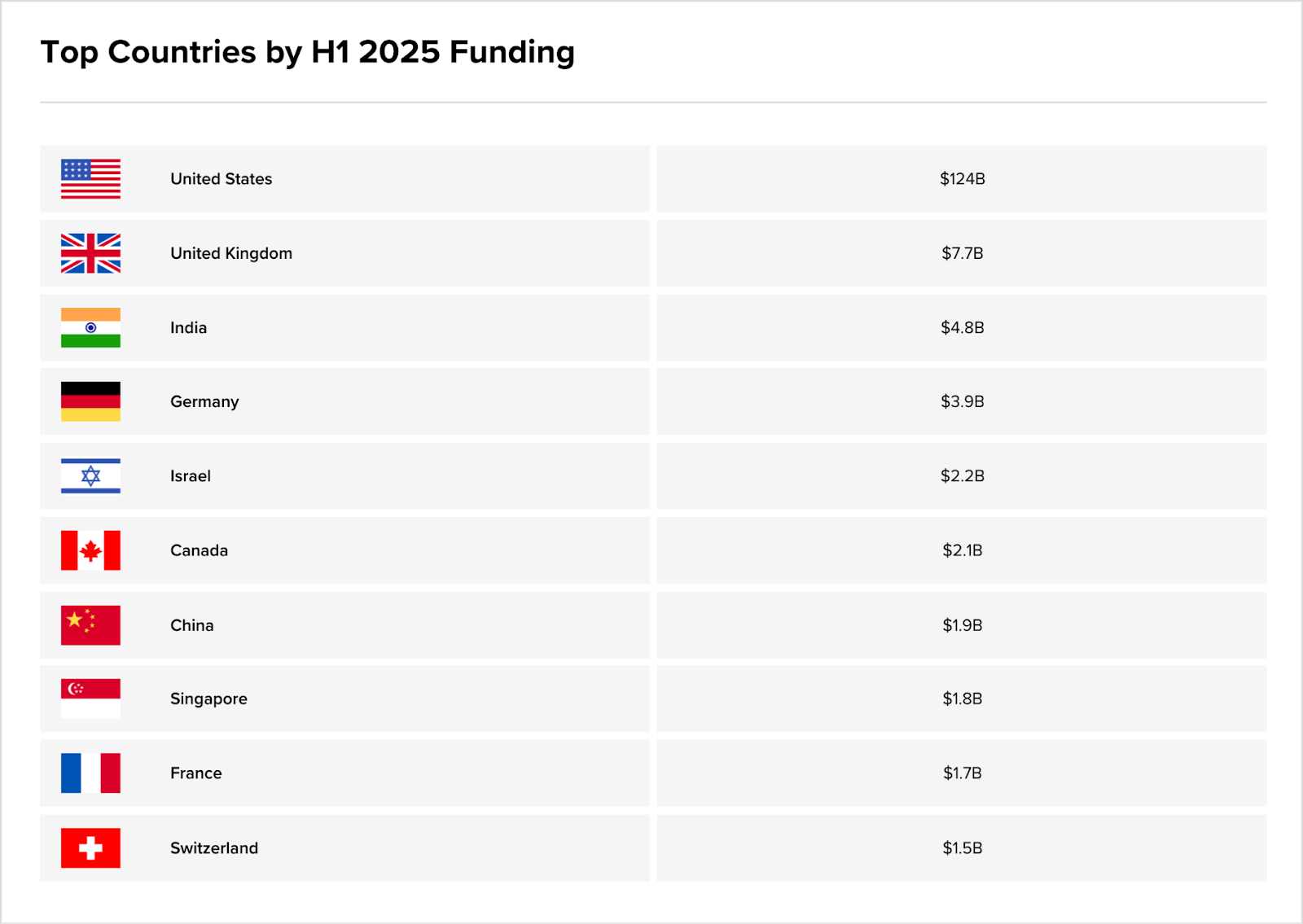

Mostly, America.

This league table says more than any single datapoint: the gravitational pull of global capital is uneven to say the least, reflecting the real intention of international finance, deal-making and investor conviction with AI as the dominant magnet.

Indeed, Crunchbase reported that North America claimed about 70% of all global startup funding in H1 2025. Of the total $124 bn invested, nearly $90 bn went to AI startups – mega deals which included Meta’s $14.3 bn into Scale AI, Anduril’s $2.5 bn, Safe Superintelligence’s $2 bn, and Anysphere’s $900 mn financing.

This represented a 43% jump YoY, and the region’s strongest half-year in three years.

By contrast, the UK attracted $7.7 bn, Germany $4.8 bn, and France even less. While India remains ahead of Germany and France, it is a comparative featherweight.

In conclusion, AI is eating the world’s lunch. What can be done to help Indian startups compete on this global scale?

The rumour mill

- Swiggy to sell stake in Rapido to Prosus, WestBridge for Rs 2,399 Cr

- Rabo India PE set to monetise 9 yr-old bet

- Indian Oil Corp plans trading tie up with Vitol; sources say

- Bharti–Warburg JV plans $450m bond issue to finance Haier India stake acquisition

- Are LPs really in the dark when it comes to fund charges?

- Private equity fund True North exploring sale of controlling stake in pharma firm Integrace

- Adar Poonawalla in talks to buy RCB stake? United Spirits shares update

- SEALSQ and Kaynes SemiCon Announce Joint Venture to Establish India’s First Secure Semiconductor Center for Onshore Personalization and Quantum-Resistant Technology

- Videogame maker Electronic Arts to go private at roughly $50b

- Beyond the Buyout: What happens when PE owns the ICU

- Circular resolving IBC-PMLA clashes soon, says IBBI chief Ravi Mital

- L&T to complete Hyderabad metro stake divestment by FY26 end

- UST and Kaynes Semicon Partner to Set up a Rs 3,330 Crore Joint Venture for Semiconductor Manufacturing in India

- Apollo restructuring, CCI clearance boosts healthtech scale

- Coty explores sale of CoverGirl, Rimmel as it pivots to fragrances

- EU clears Mukesh Ambani-led Reliance’s ₹855 cr-JV with Zuckerberg’s Meta

Salaries and bonuses

M&A news

- Bradley Houston Team Named Finalists for the 24th Annual M&A Advisor Awards

- Why India needs more women-led funds to unlock capital for female founders

- Did Somerset Indus Capital meet the benchmark in exit from North India hospital?

- Deals Digest PE/V activity jumps on big ticket transactions; M&As stay tepid

- Indian economy resilient despite global headwinds; RBI bulletin flags growth, fintech, UPI surge

- India Inc. Holds Firm – Can It Navigate Global Turbulence Ahead?

- AI, power, and sustainability: Inside Colt DCS’s data centre strategy in India

- Japan, India lead Asia-Pacific M&A as dealmaking slows

- Private equity and sovereign wealth funds revive large leveraged buyouts

- GP M&A brings upside potential but obstacles abound

- Longer hold periods stretch GPs’ plans

- Privatisation is no substitute for industrial policy

- Private credit gears up for biggest year in emerging markets

- Why Trump’s ‘Ambiguous’ 100% Tariff May Not Hurt Indian Pharma Cos

- India-led Development Financial Institutions for Global Green Finance

- Cross-border transactions, wealth management will remain focus areas: PD Singh, Standard Chartered’s India & South Asia CEO

- The M&A Dance: Orchestrating Synergies And Value Creation In Public Company Acquisitions

- South And Southeast Asia M&A Report | Q3 2025

- Funding and M&A roundup: Cornish Lithium raises $47 million

- Mint Explainer: Why the govt wants private players to build and run highways again

- Shriram Finance Infuses ₹300 Crore into Subsidiary Shriram Overseas

- Asia’s private capital landscape shifts

- India ready to rev up chipmaking, industry pioneer says

- Somerset Indus exits Apex Hospitals with 4x return, marks first Fund II exit

- Global PE giants take over top Indian hospitals

- KKR buys Meitra Hospital — its third acquisition in India’s Kerala state with deal: report

- VIP Industries block deal: Promoters sell 6.2% stake for ₹343 crore

- In Conversation with Srividhya Sridhar, Head Legal, Vivriti Capital: Insights on the IBC Amendment Bill 2025

- Mixed bag: Evergreens increasingly drive demand for multi asset CVs, many LPs won’t be pleased

- India’s M&A deal value falls 10% in September quarter on valuation caution

- Hong Kong and India drive banner year for equity capital markets

- Smartphone maker Nothing to spin off its affordable CMF brand

- Visa Steel exits insolvency as NCLT allows withdrawal of CIRP proceedings

- Spiritual Tech Startup VAMA Bags INR 22 Cr To Enter Offline Travel Segment

- Jefferies Q3 results top estimates, as advisory sales climb on increased M&A boom

- Alvarez & Marsal Appoints Bharadwaj Rallabandi to Expand Consumer and Digital Practice in India

- India, Japan stand out in Asia’s private equity fundraising

Job moves

- OneAssist, Unacademy, and Allen Online Announce New CEOs

- USAC Director Anj Balusu removed as board weighs bankruptcy versus reforms

- Afcons makes board-level appointments

- Seasoned tech pros partner VCs for a piece of the startups action

- Backed by 19 unicorn founders, VC Bipin Shah launches Rs 159 crore Solo GP Fund, Zeropearl VC

- Baijayant Panda to head Select Committee on Insolvency and Bankruptcy Code Amendment Bill 2025

- Capgemini India CEO Ashwin Yardi to retire; become non-executive chairman from January 1

- Govt appoints Shirish Chandra Murmu as RBI Deputy Governor, to replace Rajeshwar Rao

- Govt appoints Asheesh Pandey as MD of Union Bank, Kalyan Kumar as head of Central Bank of India

IPOs

- White & Case advises on Urban Company’s IPO – a first of its kind in India

- PhysicsWallah reserves Rs 460 Cr from IPO proceeds for offline expansion

- Walmart-backed PhonePe files for India IPO, targets mid-2026 listing

- IPO-bound Indian EV startup Simple Energy plans aggressive expansion by 2029

- Amicus Capital and Amansa Investments-backed Aequs files updated DRHP for IPO with fresh issue of Rs 720 crore

- India’s Clean Energy IPO Wave powers ahead despite headwinds

- RBI allows banks to fund acquisitions, lend more for IPOs

- Infra.Market files for Rs 5,000 crore IPO via confidential route

- LG Electronics Indian unit seeks valuation of up to $8.7b in IPO

- Sony Financial opens 37% above reference price in trading debut

- India’s Tech Funding Slips 23% In 9M 2025 To $7.7 Bn, But Unicorns And IPOs Signal Resilience

- KKR-backed Advanta Said to Tap Banks for $500 Million India IPO

- Capillary Technologies gets Sebi nod for IPO

- WeWork India IPO: Price band, other details

- Groww founders boost stakes ahead of November IPO

- Indel Money appoints investment banker Lincoln International to raise $30-40 million ahead of IPO

Fundraising

- India’s startups go thirsty as the world drowns in AI money

- Financial data intelligence platform Ignosis raises $4 million

- Battery manufacturer Xbattery raises $2.3 million in seed funding

- Arnya, Supreme Universal Launch Rs 1,000 Cr Private Equity Fund

- Dry powder dwindles: Private equity exits surge, war chests shrink

- GrowXCD Finance raises Rs 200 Cr led by Blue Earth Capital

- Family management app SuperFam raises $400,000 from Fundamental VC

- Business messaging firm Fyno expects $2m rev in FY26, in talks with 10 more banks

Compliance/regulatory update

- Dr. Reddy’s Laboratories Ensures Compliance with SEBI Regulations

- India tax reforms to ease retail prices, boost consumption, RBI bulletin says

- CCI approves the Saudi Agricultural and Livestock Investment Company’s (SALIC/Acquirer) proposed indirect acquisition of Olam Agri Holdings Limited (Olam Agri/Target)

- Rates unchanged, but RBI governor brings a loaded cannon of strategic measures

- Divestment Not On The Cards, But Govt Open To Rationalisation, Efficiency Gains For Its Oil Firms

- Supreme Court Clarifies Key Insolvency Issues In Bhushan Power & Steel

- Guarding Homes, Not Profits: Supreme Court On Speculative Buyers Under IBC Regime

- Supreme Court clears Rs 20,000-crore JSW acquisition deal for Bhushan Steel

- Less than 10% Indian households invested in securities markets: Sebi survey

- NCLT Approves Merger Of Star Television Productions With Jio Star India

- India’s Central Bank holds interest rates despite tariff blow

- S&P Global warns taking out Russian oil would turn price dynamics upside down; Trump tariffs driving India to economic-independence

- Piramal ent, fin arm merger gets NCLT nod

- Centre’s H2 limit for Ways and Means Advances at Rs 50,000 cr: RBI