Harsh Batra

Harsh Batra

Hello,

This week, private markets are bracing for a cycle test as Asia’s exit environment tightens, even as India stands out with continued deal momentum. Global GPs and LPs are recalibrating timing, secondaries, and valuations, hinting at a cautious but active close to the year.

Meanwhile, India’s private-sector banks are losing some of their post-pandemic shine amid renewed credit risk concerns linked to US tariffs, and a steady rupee supported by RBI intervention. The twin signals suggest both cost-of-capital pressures and a guarded lending stance for big-ticket transactions.

And finally, India’s services PMI dipped in September as demand cooled, tempering optimism in an otherwise resilient economy. Yet Axis Bank’s move to scale up acquisition financing points to growing domestic confidence in structured dealmaking, even as global liquidity remains choppy.

I hope you enjoy this week’s roundup — please connect on LinkedIn to discuss your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

How to spend it

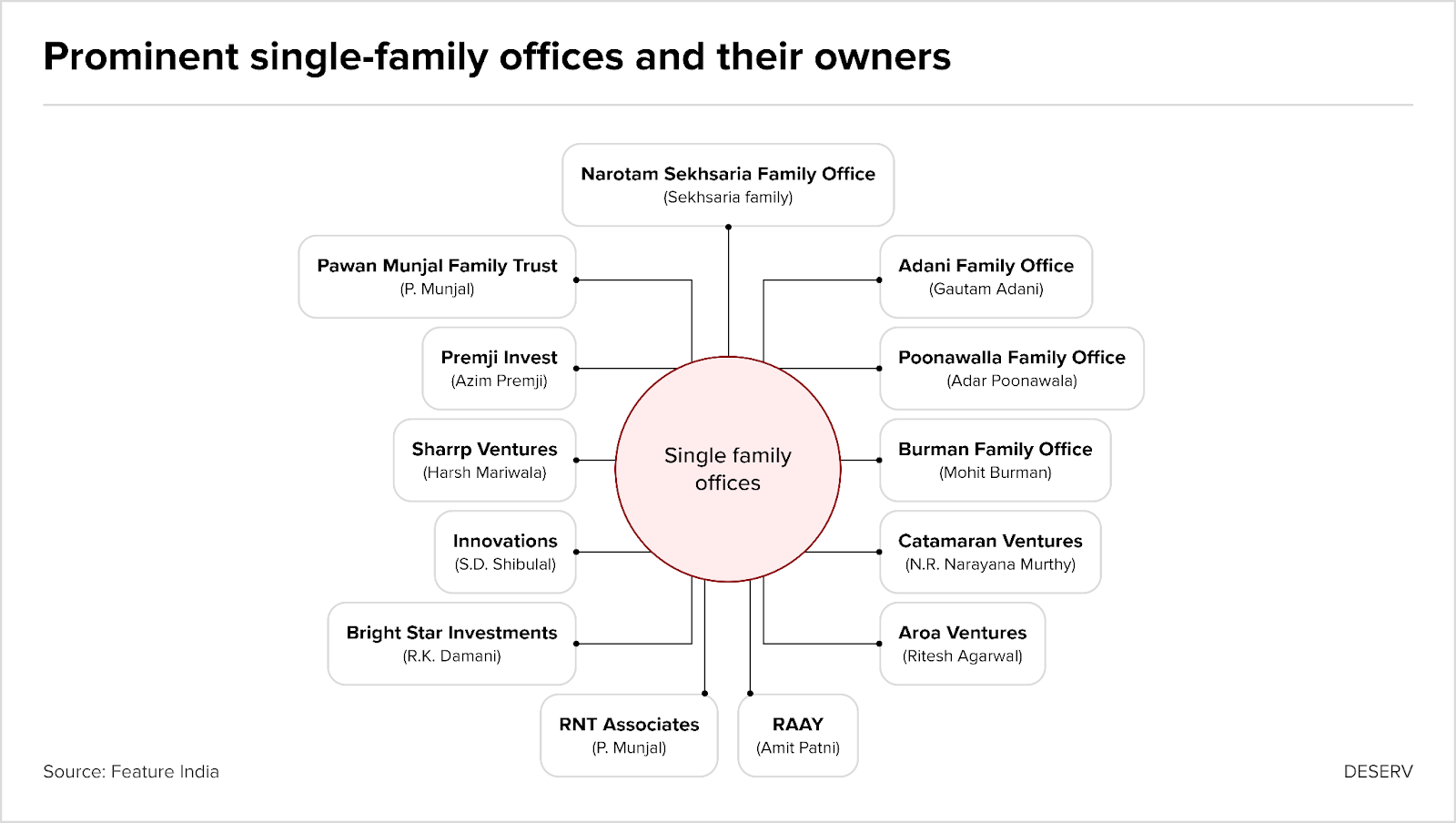

SEBI’s recent enquiries into family offices, publicly denied but widely reported, attracted a fair bit of attention. One journalist even said India was missing about $195 billion of its ultra-rich cash which could go towards nation-building.

A recent self-reported industry study on impact investment said family offices grew from about 45 in 2018 to 300 in 2024. The authors framed that evangelistically as an inflection point in how wealth was organised in India now, and how they could make a difference.

Another EY survey showed behaviour was mixed. About a quarter of the richest Indian families emphasised preserving wealth over growth, a defensive stance. Roughly 59% had formalised a will or constitution; 19% used trusts or LLPs for governance and ownership, signalling maturation.

Nearly half said changing tax laws for family offices concerned them, while 37% cited cross-border regulatory complexity. Close to 60% said they allocated less than 10% of their portfolio to PE and VC. So while stated ambition is bold, execution remains cautious.

Private credit has been emerging as a favoured sleeve because it offers yield with downside protection, especially as India’s distressed-asset frameworks improve.

So while headline deals sometimes painted family offices as risk-seeking or all-in on VC and PE, the survey suggested much of that was heat rather than light.

What is a private office?

Private family offices took many legal forms – trusts, private companies, LLPs, or offshore vehicles – and responsibility often sat across SEBI, RBI, IFSCA and tax authorities. That fragmentation slowed any single regulatory fix and made policy responses complex and slow.

The most visible investments

In recent times Premji Invest led WoodenStreet’s Series C, a large home-furnishing round, while Ratan Tata’s RNT Associates continued to make strategic angel investments, writing smaller cheques that carried high signalling value for founders.

Catamaran Ventures signalled a shift toward industry pointing to frothy startup valuations. Industry trackers showed family offices repeatedly participated in growth rounds and occasional buyouts over 2024–25, but many investments occurred through private vehicles, holding companies or evergreen vehicles and therefore escaped front-page coverage, but here is a well-intentioned but incomplete tracker.

What is stopping scaled cross-border deals?

Several things.

Legal form complexity and tax uncertainty raise transaction costs, and who wants those? Regulators and advisors worried about insider trading and conflicts when very large private pools participated in IPOs and block trades.

If unregulated family pools accessed the same privileges as qualified institutional buyers (QIBs) without governance safeguards, fairness and market integrity questions would follow.

SEBI’s consultations will seek stakeholder views on disclosures of legal entities, assets and periodic returns for very large private buyers. The regulator appeared to be weighing bespoke reporting and conflict-management rules versus folding SFOs into existing mutual fund or AIF regimes.

Rule changes may push family offices toward structured co-investment vehicles, which would make them more visible to banks and advisors.

Where could family cash go next?

Opportunities where patient family capital could add value include Byju and Punj Lloyd’s distressed assets and insolvency sales, plenty of those around; mid-market buyouts as India’s lenders entered acquisition finance, and industrial capex plays in li-ion cells, semiconductors and renewables.

Co-investment schemes under the AIF framework also offer a practical route for family offices to scale participation alongside experienced players like pension funds or other corporates.

M&A advisers may need to combine governance and flexibility, build rapid diligence teams for insolvency auctions and piecemeal sales; offer pragmatic tax and cross-border structuring, including compliant GIFT-City or feeder fund options.

SEBI’s eminent gaze (not policy, mind) could well lead to family offices – whether single or multi-family – toeing the line in the interest of IPO fairness and market maturity.

The rumour mill

- Adar Poonawalla adds fuel to fire as rumours of him buying Virat Kohli’s RCB gather steam: ‘At the right valuation…’

- Auro Realty eyes $225 million India bond issue to fund acquisition

- Billionaire family offices face deeper scrutiny in India

- Bush Foundation’s New Investment Head Eyes Emerging Markets and India for Growth

- Central Bank of India classifies Reliance Communications Rs 368-cr loan account as fraud

- Competition commission approves Saudi PIF stake in Olam Agri, paving way for full acquisition

- DCI Charts New Course with Strong FY25 Recovery and Strategic Growth Plans

- Dorf Ketal Eyes $1.6 Billion Acquisition of Italmatch

- Government confident of completing IDBI Bank stake sale this fiscal year

- HCL Infosystems awarded Rs 102 crore in arbitration case against UIDAI

- India’s private sector banks lose luster amid Trump tariffs

- India’s well-heeled get their AI kicks from secondary market

- Indian regulator denies reports on family offices oversight

- IT companies on alert as hyperscalers eye a slice of enterprise spends

- Jindal closes in on Thyssenkrupp Steel as EP Group checks out

- Largecap stock in focus after Govt plans to sell 3% stake via offer for sale

- List of Byju’s assets up for sale under insolvency resolution process

- Long liquidation battle of Punj Lloyd — failed going concern sale offset by piecemeal asset auctions

- PSB consolidation may resume by fiscal-end

- Rs 280-cr assets of bankrupt REI Agro go under the hammer in mega e-auction

- Rupee treads water as frequent RBI intervention dulls appetite for short sellers

- Ryan, Dhruva Advisors to form JV in India

- SEBI clears IHH’s long-delayed takeover of Fortis; shares jump

- Sembcorp to acquire India’s ReNew solar unit to boost renewables portfolio

- Asia’s Private Wealth Management Industry Anticipates Annual Growth of At Least 6% Over Next Five Years: Bloomberg Intelligence Survey

- Aster DM Healthcare gets BSE, NSE no objection for merger with Quality Care India

- Axis Bank aims to go big on acquisition financing

- Indian Supreme Court approves JSW’s $2.3 billion acquisition of Bhushan Power

- L&T to Exit Hyderabad Metro, Telangana Government to Take Over by FY26-End

- Lloyds Metal cleared by Indian watchdog to acquire stake in Thriveni Pellets

- The status quo that isn’t

- TVS Capital Funds elevates Suraj Majee and Ravi Krishnan

- Two Anil Ambani firms with Rs 830 cr dues get sold off for Rs 46 lakh

- Why Dunzo failed to defend itself against insolvency petition

- Why FDA certification is the new moat in India’s MedTech race

- Why Zepto’s private-label meat foray may just be a losing game

M&A news

- CCI approves the acquisition of business of production, bottling, marketing and sale of alcoholic and other beverages under the ‘Imperial Brands’ by Tilaknagar Industries Limited.

- Competition Commission Of India Approves Apollo Hospitals’ Restructuring Plan

- Deal Street snaps up $110 billion in first 3 quarters, reach 3-year high

- From BFSI to Healthcare: Key long-term themes for investors over the next 3-5 years from Unmesh Kulkarni

- GP stakes bring lighter touches

- Greylabs AI to channel bulk of ₹85 crore Series A funding into R&D to enhance voice AI capabilities

- ICG Enterprise bucks private equity downturn after selling £222m of investments in first half

- IHC will help Sammaan become a full-service finance company: Gagan Banga

- India Deal Review: Startup funding rebounds slightly in September

- India M&A Shows Resilience in the Face of Tariff Headwinds

- India’s 8% growth hinges on private investment revival, says Michael Patra

- India’s outbound FDI moderates to $4.41 bn in September, shows RBI data

- India’s Sammaan Capital to ramp-up affordable housing after IHC investment: CEO

- Investcorp’s new Rs 5,000 crore PE fund to target mid-market buyouts, says India head Gaurav Sharma

- Japan, India lead Asia-Pacific M&A as dealmaking slows

- Joint ventures, tech collaboration can help narrow India’s trade deficit with Qatar: GTRI

- Lending leeway to pave way for Rs 5 lakh crore credit demand

- M&As: Private credit funds unfazed by entry of banks

- Pakistan among top two emerging economies with major decline in bankruptcy risks: Bloomberg

- Partners Capital LPs need to watch out for co-investment style drift towards secondaries

- Precision Meets Purpose’: An Interview With Cross-Border M&A Specialist Arunima Motiwala

- Private markets brace for cycle test, Asia exits remain tight

- RBI unlocks bank finance | Who will run away with It?

- Resilient Dalal Street a boon for private investors

- Side Letter: Naive alts allocations

- Dishi Bhomawat strengthens Touchstone’s M&A team in Mumbai

- GrowXCD Finance secures ~INR 200 Cr (US$22.8m) funding

- India: JSW One Platforms raises $65m funding led by SBI, others

- INOX Air Products Invests ₹500 Cr in Dholera to Strengthen India’s Semiconductor Supply Chain

- Varmora promoters buy back 2% stake from Carlyle

- Veiva Scientific eyes PE funding amid MedTech sector boom

- Viewpoint: New wave of control deals redraws Indias PE exit map

- Wafra CIO: GP stakes in Europe is an educational process

Job moves

IPOs

- IPO-bound Boat turns around, posts Rs 60 crore profit

- IPO-bound Jio shifts gears from a focus on volumes to monetisation

- Lenskart, Wakefit get Sebi clearance for public issues

- LG Electronics India IPO draws Norway, Singapore wealth funds as anchor investors

- LG Electronics India IPO subscribed within hours of launch

- Tata Capital Takes Orders for India’s Largest IPO of 2025

Fundraising

- Bain Capital racks up 14bn for fourteenth PE fund

- Blackstone hits $10 billion Asia buyout fund goal amid PE chill

- Cleantech startup EcoEx secures $4 million led by Dovetail Global

- Global deep tech focused VC Celesta Capital ropes in key LP for maiden India fund

- Indian stock trading platform Dhan turns unicorn with $120m fundraise

- IOCL-GPS Renewables Joint Venture IGRPL Bags USD 95 million from Indian Bank

- SG’s Qapita confirms raising $26.5bn in series B funding

- Water treatment firm Membrane Group gets $50 m from GEF Capital Partners

Compliance/regulatory update

- M&As in AI space may need scrutiny: CCI

- Corporate Governance Issues in M&A

- Fed set to drive global rate cuts as Europe shifts to pause

- Fed turns dial as RBI keeps status quo

- How RBI’s nod puts banks at the centre of corporate deals

- India markets regulator seeks to boost lending and borrowing of shares

- India’s market regulator revises Sebi block deal norms

- Possibility of future rate cuts by RBI still open: Report

- RBI credit reforms: India’s central bank seems concerned about the state of India’s economy

- RBI MPC October 2025: Repo Rate Unchanged At 5.5% Amid Balanced Growth And Inflation Outlook

- RBI Policy Statement An Authoritative One Towards Market Reforms: SBI Chairman

- SEBI introduces co-investment scheme under AIFs framework

- The GP stakes secondaries stop-gap

- Why RBI Wants Rupee to Stand on Its Own Against the Dollar – Explained