Harsh Batra

Harsh Batra

Hello,

This week, Equirus Group merged with Sapient Finserv creating a Rs35,000 crore AUM wealth management platform, a large consolidation in wealthtech that reshapes distribution and deal activity.

Meanwhile, LG Electronics’ India IPO attracted $50bn in bids, setting a near two-decade record.

And finally, Quadria Capital planned to invest up to $800m from its third fund in Indian healthcare, which could help accelerate existing healthcare M&A, PE exits and capacity expansion.

I hope you enjoy this week’s roundup — please connect on LinkedIn to discuss your next M&A deal.

Let’s dive in.

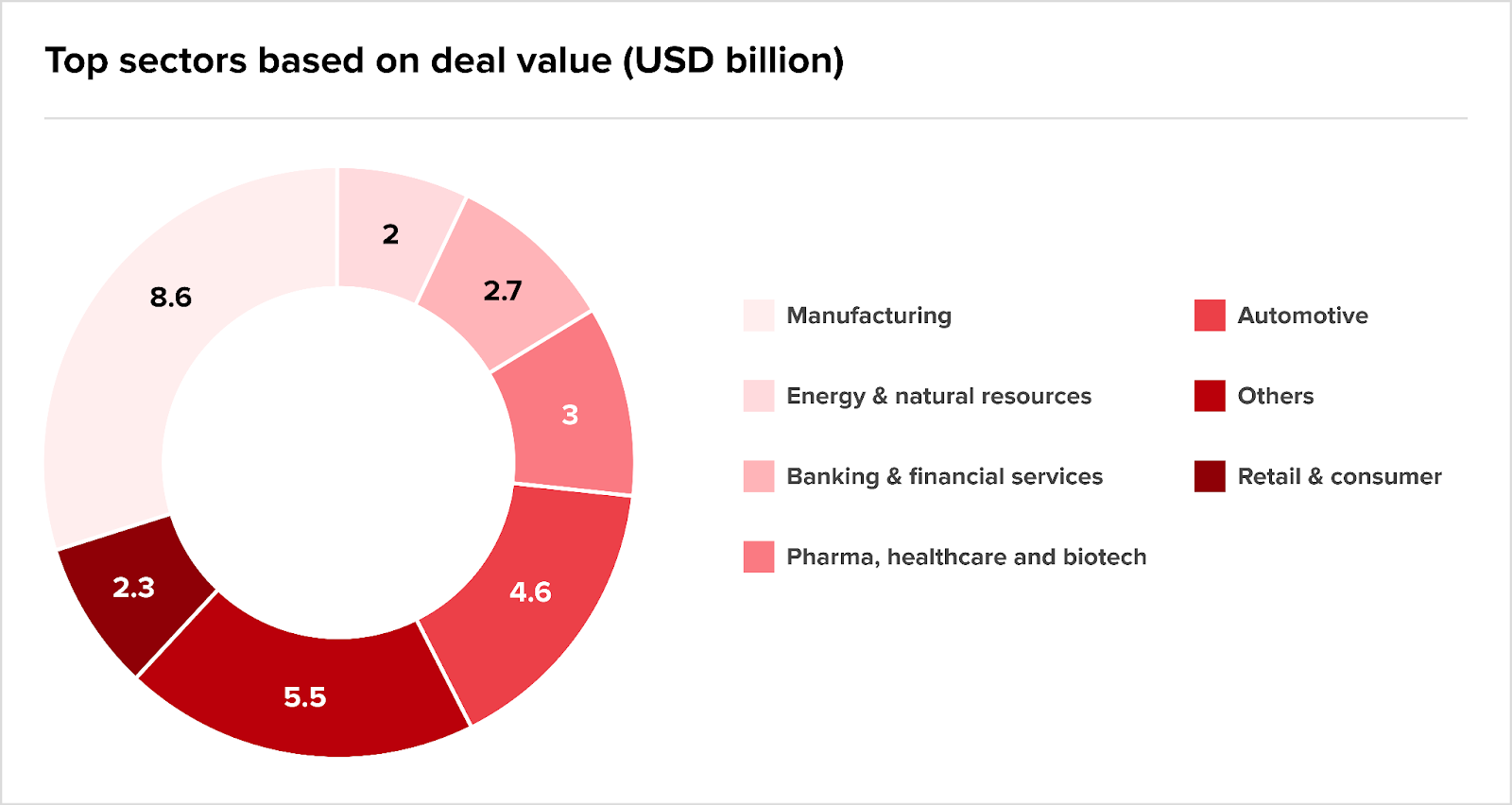

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

The post-tariffs calculus

There is much being said about India’s economic resilience. Let us examine the proof of this pudding.

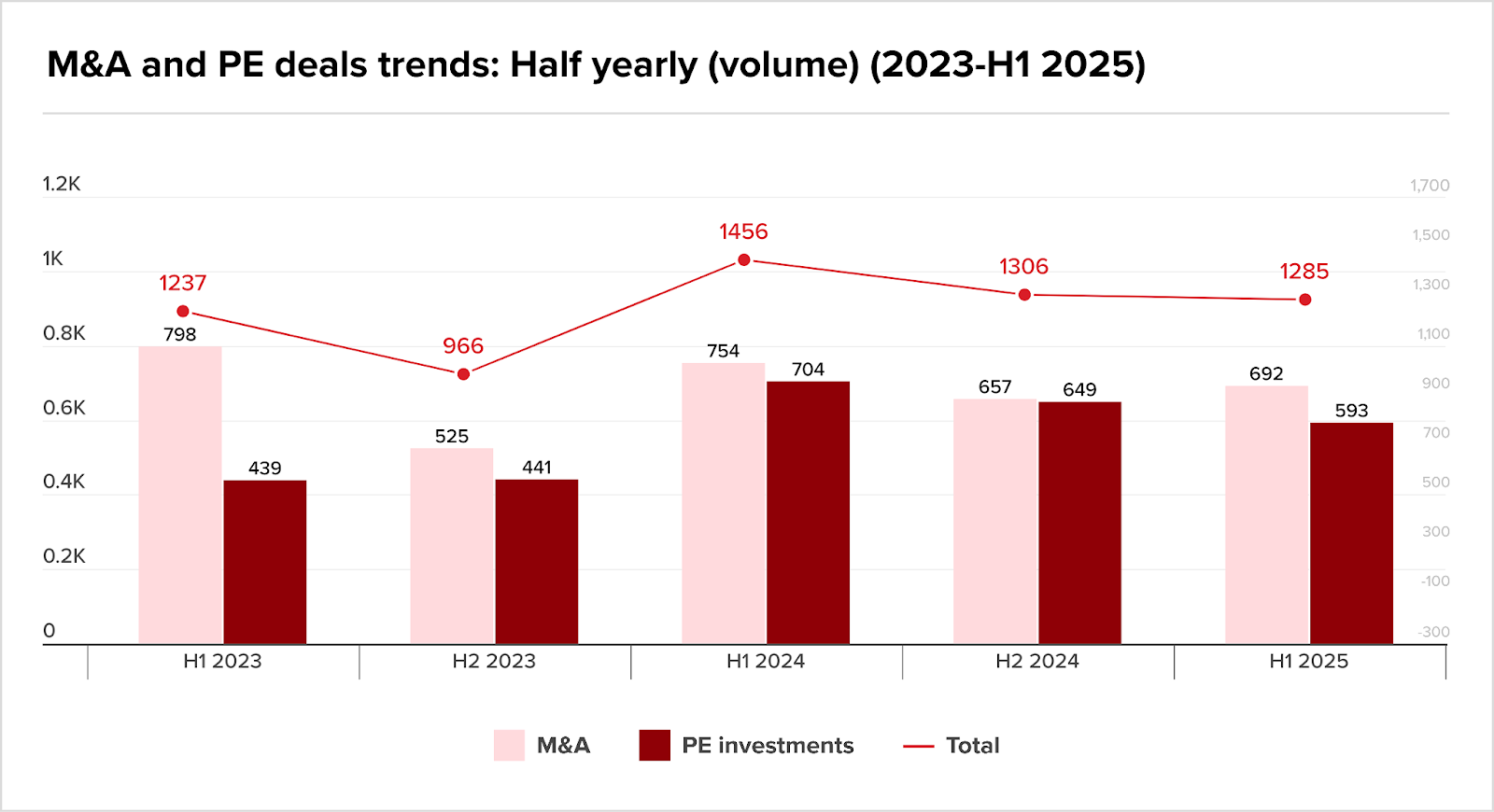

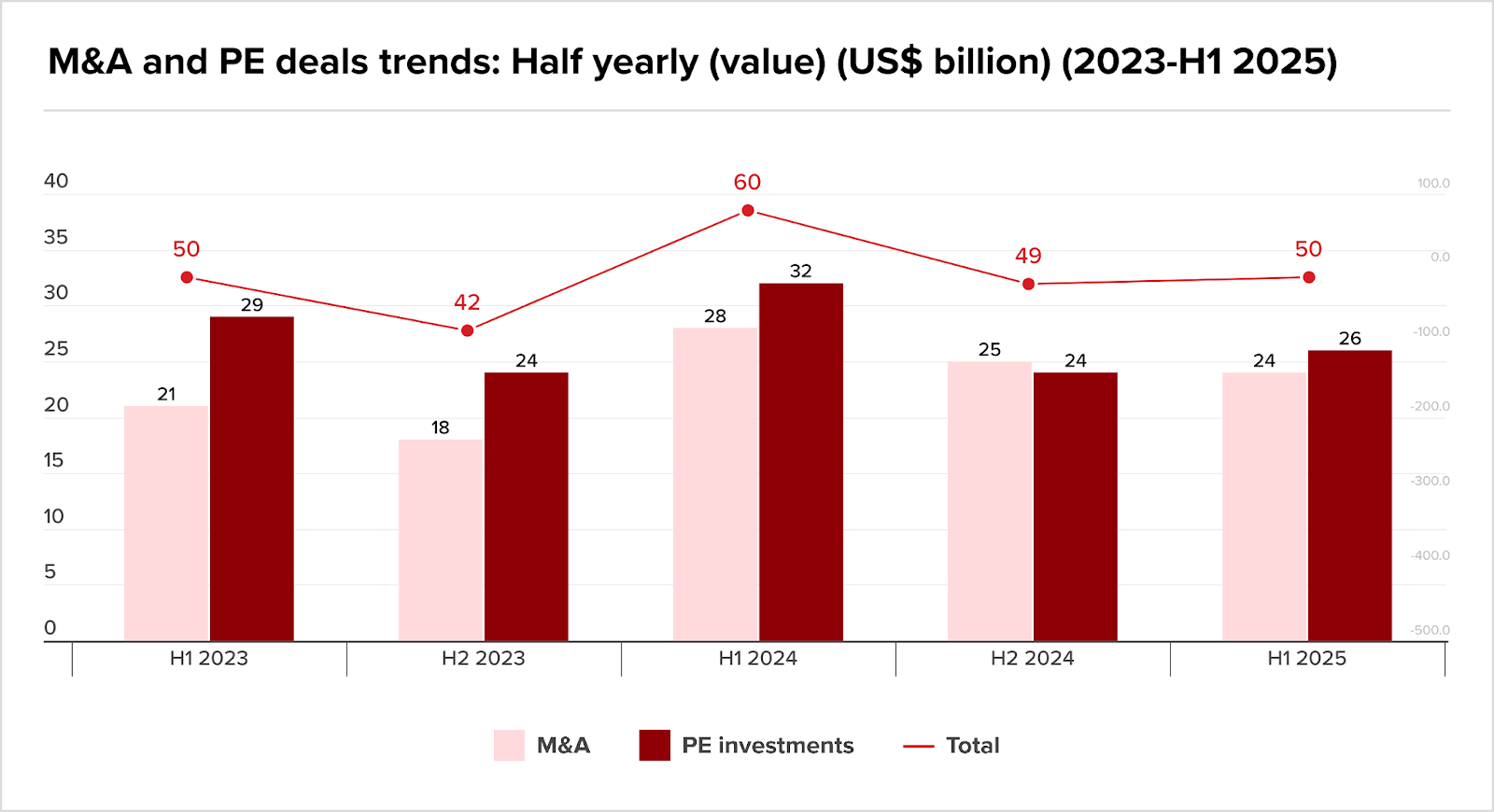

FDI inflows to India stood at $81.04 billion this May. Not bad as real capital and M&A finance go.

M&A in the same period showed overall deal value at $50.5 billion, with fewer but larger transactions dominating, a consolidation of deal value in fewer hands. A notable example: the Porteast–Shapoorji $3.1 billion deal.

Similarly, private credit surged to $9 billion in H125, up 53% YoY, driven by very large transactions, including large financings in infrastructure, real estate, renewables, and manufacturing. These point to the instruments’ growing capacity to support refinancings and acquisitions.

Experts insist that sectors such as electronics, consumables, semiconductors, and renewables are likely to see a rise in M&A volume, driven by demand, fresh capital deployment and policy impetus. Similarly, valuations in standout companies may rise under competitive bidding for high-quality assets; coupled with tighter scrutiny of inbound capital from geopolitically sensitive sources.

But here is what the Q3 numbers from GT Bharat said this October:

Macro vs. micro

Globally as well as in India, trade protectionism and greater investment screening are creating economic headwinds, while subsidies to reshape supply chains are acting as the tailwinds.

In June, the RBI governor noted that FX reserves, sufficient to cover 11 months of goods imports, were stable. But we know foreign currency value fluctuates weekly.

And this month the central bank flagged potential downside risks to GDP growth in late FY26.

Yet India’s apex bankers managed to miss the government’s given target of a 4% inflation, which is now down to about 3%. While prices have softened on the back of easing food and fuel costs, this moderation leaves limited room for aggressive monetary loosening.

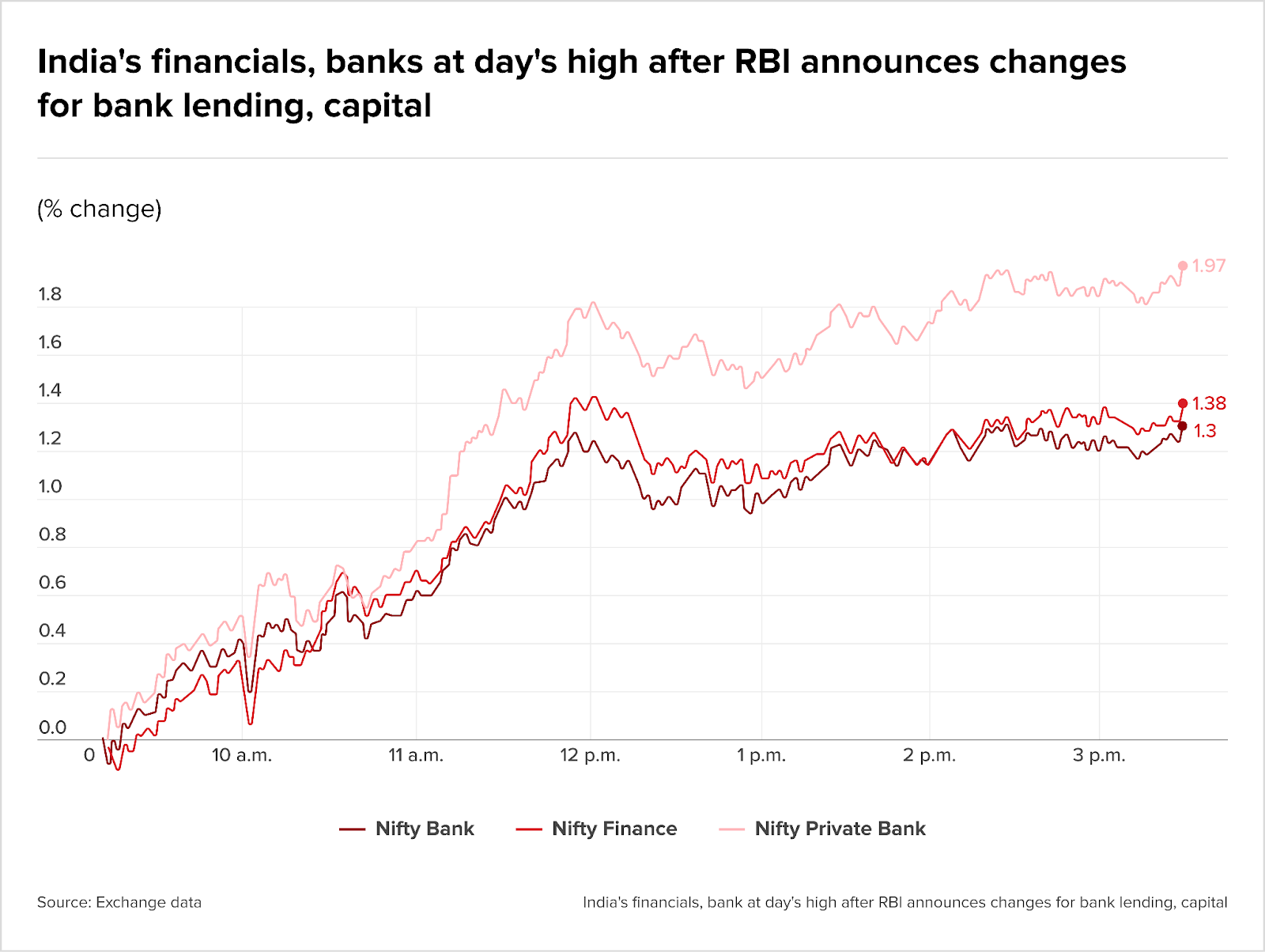

Lender-friendly finance

A new framework will allow Indian banks to fund domestic corporate acquisitions, relaxing limits on lending against listed debt and equity (more on this in the next edition of Teaser).

As part of a broader package of 22 measures to deepen bank lending and capital markets, this move could lower the cost of funds for acquisition finance.

Yet private capitalists remain largely unfazed, citing their complex, bespoke, higher-risk structures and execution speed as enduring advantages over local banks. Indian lenders, some argue, will serve more as a backstop than a competitor for domestic acquirers.

This is how the markets reacted:

An alternate asset manager said his business will benefit from deeper domestic capacity. But Mint urged prudence on asset-liability mismatches (ALM), growing leverage risk, and spread compression of private credit yields and the economics of sponsor deals.

Give or take

We should also consider the impact of US tariffs. Corporates are being forced to re-route supply chains and exporters are pivoting to different markets, while policymakers have promised bailouts for key industries. The medium-term picture looks promising, but this realignment could delay deals and affect near-term valuations.

India’s cunning recalibration of relations with China have positioned it uniquely as both a beneficiary and participant in this new order. This is how: Multinationals diversifying to hedge against China are re-routing to India as the country welcomes ‘friendly’ capital, and its financial watchdogs and interest groups face new tests of openness and discipline.

Authorities will also allow joint ventures (JV) with Chinese firms as deals evolve toward Indian ownership and tech transfers. Supply-chain diversification is likely to proliferate inbound factory and asset acquisitions in electronics, semiconductors, and the EV ecosystem, such as the upcoming Dixon–Longcheer and HCL–Foxconn announcements.

A war chest

Finally, the PE ecosystem remains flush with dry powder. VCcircle said LPs committed $86 bn to India’s PE/VC funds in Q1 of 2025. This can be interpreted as the optimistic light in which India is viewed as an investment destination, though capital deployment has been cautious amid shifting valuations.

Funds are also increasingly focussing on control deals, secondary transactions, and buy-and-build strategies across healthcare, financial services, and consumer tech.

Easy exits

What does all this say about the resilience of India’s economy and M&A market?

We can see that new realistic and diverse pathways are emerging with a thriving intra-fund secondaries scene – as seen in developed market economies – and blockbuster IPOs such as Urban Company driving liquidity events.

India remains a singularly volatile market, but its deepening domestic capital markets and sponsor financing may yet anchor a stable exit environment. Watch this space.

The rumour mill

- Vijay Mallya withdraws application for annulment of UK bankruptcy order

- Torrent Pharma–JB Chemicals deal under CCI lens over possible monopoly risk

- This $400M PE fund is investing in founder-led mid-market service businesses

- Thane land of Sapphire Space Infracon set for e-auction; reserve price fixed at Rs 42 crore

- Temasek in talks to invest in Indian space tech startup

- Samhi Hotels Confirms Compliance with SEBI Regulations for Q3 2025

- Samena Capital changes deal terms for India BFSI bet

- Prosus to buy 10% stake in Indian travel platform Ixigo for $146m

- Polaris Selling Indian Motorcycle Majority Stake

- Morgan Stanley PE-backed Omega Hospitals in talks to buy rival

- Minfy bets on AI and homegrown talent to push cloud growth

- Ludhiana: PSPCL unions protest asset divestment plan

- Kotak Mahindra Bank finalizes merger of microfinance subsidiaries

- India’s fraud-hit PMC asked other major banks for merger – Administrator

- India moving ‘cautiously’ on oil refiner BPCL’s privatisation

- India and South Korea Forge Strategic Alliance in Electronics, EV Components, and Digital Supply Chains

- IIMA Ventures, Jaivel to invest in 8–10 deeptech start-ups through new defence fund

- IDBI Bank declares date to announce Q2 results; update on LIC, GoI’s divestment to be in focus

- ICICI Prudential AMC Seeks CCI Approval to Acquire ICICI Venture’s AIF and Advisory Units

- General Catalyst leads $6m funding in Meolaa and other India deals

- General Atlantic bets more on India portfolio firm to help finance m&a deal

- Concord Control Systems to raise stake in railway tech firm Progota India to 46.5%

- Automotive Axles Limited Confirms Compliance with SEBI Dematerialization Regulations

- Another rate cut likely this fiscal: Crisil’s FCI

- Coinbase to increase stake in CoinDCX, valuing Indian crypto exchange at $2.45 billion

- Paytm brings entities under direct ownership to simplify its structure

- Anand Rathi Wealth Approves Disinvestment of Subsidiary

- Debt capital desks may leak as banks start M&A financing

- Dr Agarwals hospital possible acquisition of smaller rival

- RBI reform plans to strengthen bank operating environment, boost credit flow: rating agencies

- Adani to partner with Google for India’s largest AI hub in Visakhapatnam

- From a sprawling marketplace to a hyperlocal model: Has Udaan found its winning formula?

- J&J to spin off orthopedics business, sees 2026 sales growth of over 5%

- Govt draws up mega bank merger plan; smaller lenders to be clubbed with big banks by FY27

M&A news

- SpeakX raises $16 million from WestBridge, others, pivots to an English-learning app

- Sembcorp to acquire ReNew’s 300MW solar unit for US$246 million

- Quadria Xapital to invest up to $800mn from third fund in Indian healthcare

- Private equity in Indian real estate declines 15% in H1 FY26, deal sizes remain steady: ANAROCK Capital

- PE real estate investments fall 15% in H1 FY26 amid global crises: Report

- M&A financing to heat up in India

- India’s Natco Pharma takes $226m strategic stake in Adcock Ingram

- India’s Financial Services Deal Value Jumps 39% In Q3 2025: Report

- IBC a business advantage not an obstacle

- HSBC bets big on India’s startup boom launches $1 billion innovation banking platform

- GlobalData reports 320% rise in pharma M&A deal value in September 2025

- Elpro International Boosts Stake in Ganesha Ecosphere with INR 6.53 Crore Investment

- EA strikes deal to go private: how much will shareholders receive?

- Data Vantage: Ideation3x in focus and other updates

- CCI Greenlights Lloyds Metals’ Strategic 49.99% Stake Acquisition in Thriveni Pellets

- BXCI launches India private credit with first local head

- Bond yields steady as RBI holds rates; accrual strategies favoured going ahead: Devang Shah

- Asian stock markets step up reforms to woo foreign capital

- AI, consumer tech and pharma poised to redefine India’s investment landscape: Rahul Bhasin

- ABL partially acquires Macquarie-SBI’s stake in ACL

- Aavishkaar patners wih Jamwant for $60m Indian defence, deep-tech fund

- India is one of the best places to deploy capital, says ACTIS chairman Torbjorn Caesar

- Sheppard Mullin Represents Carolwood in Acquisition of Indian Motorcycle

- Adani, Google forge $15 bn partnership to build India’s largest AI data centre in Visakhapatnam

- Medi Assist Healthcare gets new investor on board after Bessemer’s exit

- World Bank Commits $2.3 Bn To India For Fiscal 2025

Job moves

- WeWork India drops 5% in debut trade amid valuation governance concerns

- Sonali Sen Gupta Appointed as Executive Director of the Reserve Bank of India

- Shambhavi Mishra appointed as Head of Marketing at Gourmet Investments Pvt. Ltd.

- RBI appoints Sanjay Kumar Hansda as Executive Director

- NACL Industries Appoints Arun Alagappan as Additional Non-Executive Director

- Mahavir Lunawat Founder of Pantomath Capital Unanimously re-elected as Chairman of Association of Investment Bankers of India (AIBI)

- Blackstone hires Deutsche Bank veteran to lead India private credit push

- DL Appointed Jacob George as CMD, Mathew Chandy Continues to be Executive Director

IPOs

- US-based Tryfacta plans IPO at GIFT City to raise up to $150 million

- Norfund invests $20m in India’s IPO-bound SAEL

- LG Electronics’ India IPO attracts $50b in bids, sets near two-decade record

- Indian non-bank lender Tata Capital makes subdued listing

- Canara Robeco’s India IPO full subscribed on final day

- Winro Commercial India Reaps Rs 2.15 Crore Profit from LG Electronics IPO

- Tata Capital Debuts Higher After India’s Biggest IPO of Year

- India’s Canara HSBC Life IPO fully booked on final day, led by institutional buyers

Fundraising

- Membrane Group secures USD 50-mln investment from GEF Capital to boost water treatment solutions

- Indian heealthtech firm Tricog Health raises funding

- India: Dezerv raises funding co-led by Premji Invest, Accel;s Global Growth Fund

- India Digest: Rusk Media secures funding, potential investor eyes stake in Ixigo

- India Digest: Ekaa Electronics, Reo.Dev raise funding

- D2C brand Two Brothers Organic Farms raises 110 crore from 360 One Asset, others

- Kalaari, Endiya co-lead funding in Matters.AI