Harsh Batra

Harsh Batra

Hello,

This week, Emirates NBD announced it was set to acquire a majority stake in RBL Bank for $3 billion, in what would be the biggest FDI banking acquisition in a while.

Meanwhile, the bankruptcy court approved Future Supply Chain Solutions’ acquisition by Reliance Retail, a significant distressed deal in logistics.

And finally, Singapore Keppel takes full control of Cleantech Solar after buying Shell’s 49% stake, reflecting strategic consolidation in clean energy.

I hope you enjoy this week’s roundup — please connect on LinkedIn to discuss your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

Leverage returns to the boardroom

First a reminder. In 2010, the Dodd–Frank Act asked the SEC to define rules around insider share pledging, or loans against securities (LAS), but specifically company shares – when executives or business owners borrow against their own stock.

Fifteen years later, the US agency still hasn’t. Into that vacuum, proxy advisors like Institutional Shareholder Services (ISS) and Glass Lewis stepped in with their own soft laws encouraging corporate boards to justify, monitor, or ban pledging altogether.

The practice can be harmless as a means to diversify wealth or fund liquidity needs, until falling share prices trigger margin calls – the margin on a loan increases when a borrower is downgraded on the principle that higher risk should equal higher returns for the lender, compelling insiders to sell in panic and crash their own stock.

The dotcom bust, the Great Recession, and the disruptions of the Covid-19 pandemic – all revealed how billions can be wiped out and companies lose governance credibility after margin-triggered fire sales.

By 2012, US financial advisors were urging investors to vote against directors who pledged stock. However, by 2015 policy evolution reflected a softening from outright prohibition to a case-by-case review that weighs how much stock is pledged, how volatile the company’s shares are, and whether insiders have disclosed these risks transparently.

Why the resurgence?

Two drivers: rich public valuations that make shares attractive collateral, and constrained bank balance sheets that have pushed promoters toward NBFCs (non-bank financial institutions), private credit and structured lenders. Firms like Bajaj Finance, 360 ONE and Nuvama have expanded LAS exposure; offshore credit houses are also participating via trustee structures. That expands supply – and complexity.

Perhaps, the US is hands-off now, but India’s economy is not bottomless like the US’s seems to be (the difference in size between the US economy and the next-largest economy, China, is roughly $11 trillion in nominal GDP terms).

Corporates borrowing against their own stock remains under-regulated. But if this behaviour proliferates in Indian boardrooms, will the country’s regulators be ready to confront the governance challenges that come with financial leverage built on equity valuations.

Regulatory guardrails exist. RBI maintains minimum margin norms (50% for advances against shares) and restricts banks from financing buy-backs or holding equity beyond prescribed thresholds. NBFCs face LTV (loan-to-value) and reporting requirements, but their perimeter is wider, letting them finance unlisted, promoter holding companies with larger haircuts and bespoke covenants.

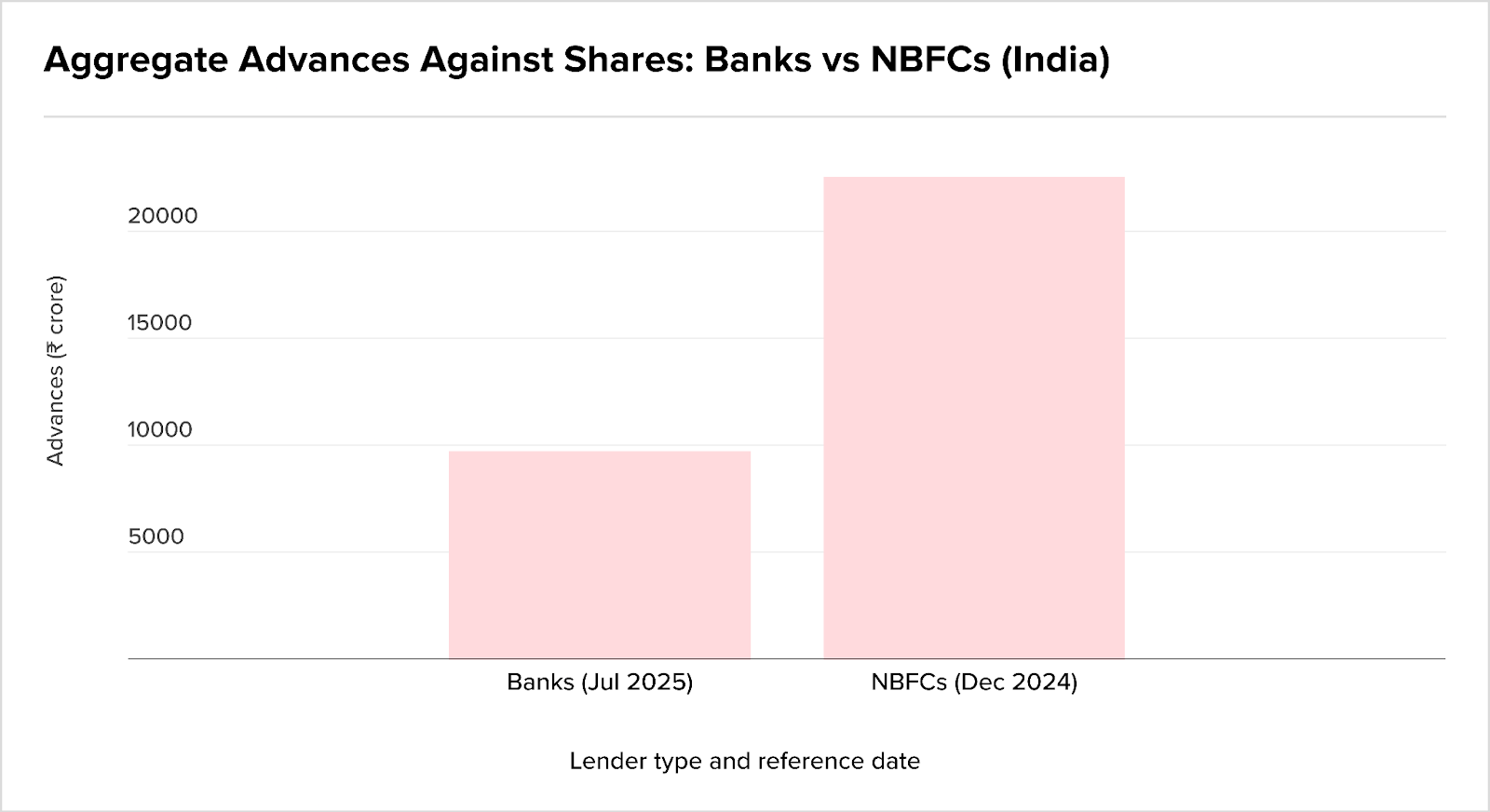

Lending against shares by Indian NBFCs dominates this market currently, whose advances against shares were approximately ₹22,000 crore ($2.64 bn) in 2024, versus roughly ₹9,700 crore ($1.6bn) for banks, as per RBI. And this trend is set to grow as RBI allows Indian banks to participate. Previously only NBFCs and foreign lenders could.

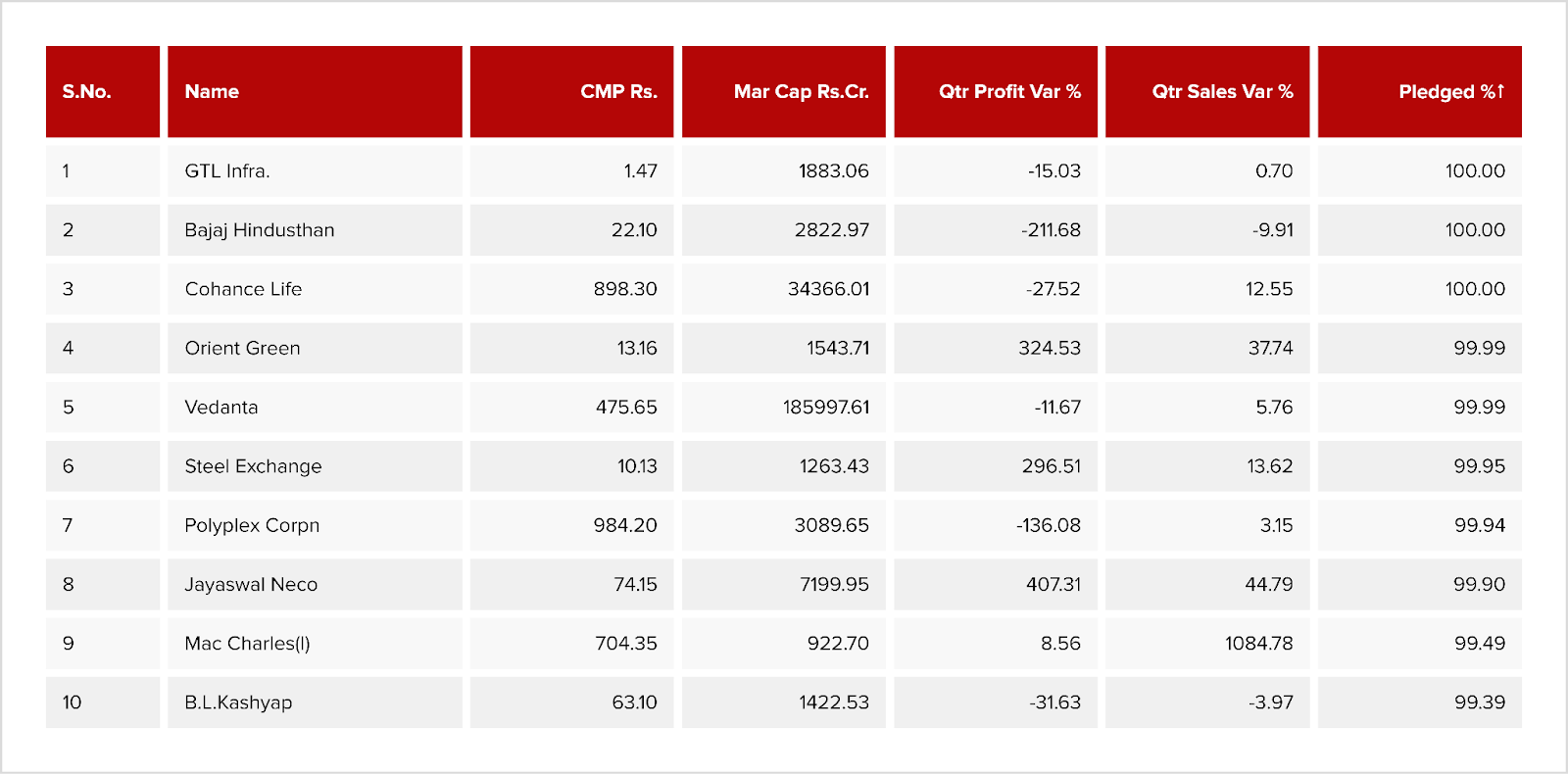

Promoters are using non-bank credit rather than traditional lenders for liquidity. Recent exchange disclosures show extreme concentrations in large caps such as Vedanta, Hindustan Zinc and Oberoi Realty, with pledges exceeding 50% and in several cases north of 90%.

This table shows top-listed companies by market cap and pledged percentage. Those figures are not merely academic but change control risk, margin sensitivity and recovery.

A separate view of the market, with companies ranked by the proportion of pledged shares, highlights the tail risk. Smaller names whose promoters have effectively encumbered near-total holdings.

These securities are the most price-sensitive; and a modest drop can force multiple margin calls and cascade selling across correlated lending books.

Contagion risk?

Advisors, consultants, and the financial regulators have all shaped this debate, encouraging clarity in pledging policies as to their purpose (an education or a home loan, for medical emergencies only, for example); with caps on the trading value of pledged shares as a percentage of total outstanding equity; monitoring board-level oversight and progress disclosure on reducing pledged shares; and robust compliance such as excluding pledged shares from ownership targets.

High pledge percentages amplify downside correlation between promoter stress and market value. In M&A or recap deals, pledge data now routinely shifts pricing, covenant design and escrow requirements. Private-credit shops prize the yield; acquirers discount for execution risk.

LAS delivers liquidity without immediate dilution, but when leverage stacks on equity valuations the structure is fragile.

Best to keep in mind that pledged shares are collateral, but also a contagion channel.

The rumour mill

- Japan Post Seeks CCI Nod for 19.9% Stake Purchase in Logisteed Holdings

- BluSmart tech arm pushed into insolvency over Rs 5.8 crore dues

- NCLT admits Bhilai Jaypee Cement for insolvency over Rs 45-crore coal debt

- Bankruptcy court approves Future Supply Chain Solutions’ acquisition by Reliance Retail

- IDBI Bank’s Q2 Profit Soars 97% to ₹3,627 Crore, Boosted by Strategic Divestment

- Elpro International Seeks Shareholder Approval for Rs 355 Crore Related Party Transactions

- Decoding Meesho’s DRHP: a solid ecommerce story, but does it have a strong public market one

- The great IPL valuation reset as consolidation meets regulation

- CCI clears Torrent Pharma’s proposal to buy stake in JB Chemicals

- IOB bets big on M&A financing, moves to address CASA concerns: MD & CEO

- European Investment Bank commits $60m to India’s EAAA Alternatives fund

- IFC mulls $200m loan to Indian education finance firm Credila

- India’s Ola Electric founder, senior exec named in police report over employee suicide

- Yes Bank shares tumble as SMBC rules out raising stake beyond 25%

- Billionaire Gautam Adani, Google To Build $15 Billion AI-Power Data Center Hub In India

- Volkswagen Group in renewed talks with JSW Group over possible India JV

- Vedanta taps lenders to back Rs 17,000-crore bid for Jaiprakash Associates

- Mega Bank Merger: These 4 Public Sector Banks May Cease To Exist

- Investor Intentions: MBOI to continue growing its private investments portfolio

- Market sentiment towards retail opportunities heats up

- India’s ONGC eyes JV trading entity, shortlists four companies

- Dubai’s Emirates NBD to buy 60% stake in India’s RBL Bank for $3 billion

- Here’s the Letter Indian Motorcycle’s New Owners Sent To Its Employees

- RBL Bank Targeted in Public Acquisition Announcement

- Thirumalai Chemicals Confirms Compliance with SEBI Regulations

- Granite Asia leads $85 m funding in Indian storytelling platfom Kuku

M&A news

- JSW Steel board approves reorganisation of US entities & merger of some Indian subsidiaries

- Gabriel India Limited signs joint venture with SK Enmove, part of the SK Group US $148 Billion- among South Korea’s two largest conglomerates

- Adani bid for Sahara assets: Recalling the journey of the beleaguered empire

- Dixon Technologies Completes Joint Venture with Inventec for IT Hardware Manufacturing in India

- Global Investors Pour $15 Billion into Indian Financial Sector Amid US Credit Concerns

- Fintellix Joins ICRA: Strategic Acquisition to Strengthen RegTech & Data Analytics Offerings

- Zen Tech up 3% on 24% stake buy in Applied Research; how will it benefit?

- Trump tariffs may cost firms $1.2 trn, consumers to bear burden: S&P Global

- Perpetuus Expands in India Through Joint Venture with Asiatic Rubber to Scale Graphene Rubber Masterbatch

- Data Vantage: Oppdoor, Konvy, Wego in focus and other updates

- FMO proposes investment in India’s IIFL Home Finance

- India: Startup megadeals see 38% QoQ drop amid global uncertainty

- RBL Bank eyes launching wealth management business after ENBD deal: CEO

- Foreign firms being allowed to acquire Indian banks imprudent, poses substantial risks: Congress

- PTC Industries shares in focus on Bharat Dynamics JV to develop missiles

- Hedge fund-style funds set to transform $900bn Indian mutual fund market

- Transactional risk insurance claims rise in India as M&A deals grow

- India’s equity capital market volumes see heightened activity next year, Citi Group says

- India’s sovereign rating upgrade is earned — but not assured

- Lightrock bags 7x return on Indian logistics partial exit

- Beyond the Buyout: APAC capital in spotlight; Indian LPs bet on healthcare

- Do private markets require a rebrand

- MoFo, Freshfields drive SoftBank’s USD5.4bn ABB robotics buy

- Godrej Industries raises stake in Godrej Capital to 91.11%

- CCI clears Capgemini’s full acquisition of Singapore-based Cloud4C to strengthen hybrid cloud services

- L Catterton partners with Healing Hands in bet on India’s fast-growing specialised care market

Job moves

- Eight Capital Partners appoints new executive leadership team

- Former US ambassador to India Richard Verma appointed as independent director at T Rowe Price

- Nirmal Kumar Minda appointed ASSOCHAM President; Amitabh Chaudhry joins as Senior Vice-President

- Apollo appoints new APAC head

- Summary Of Asia-Pacific Senior Wealth Management Moves – August 2025

IPOs

- Meesho IPO: Ecommerce platform files updated papers for $800 million IPO; eyes December 2025 listing

- ARCIL set to go public as Sebi clears IPO plan of India’s oldest ARC

- India’s Canara HSBC Life IPO fully sold on final day, led by institutional buyers

- Shares of Canara Robeco jump in India trading debut

- LG Electronics India surges 50% in trading debut

- White & Case advises on Rubicon Research’s India IPO

Fundraising

- Mid-sized consumer brands like Wingreens, Wow! Momo, Curefoods eye PE funding amid revival in investor interest

- Torrent Pharma plans Rs 14,000 crore bond sale for JB Chemicals acquisition

- Indian quick commerce firm Zepto raises $450m at $7b valuation

- India Digest: Airbound, Houseeazy raise funding

- NIIF India-Japan Fund invests $57m in EKA mobility

- India Digest: Olyv, Maieutic Semiconductors in funding news

- India Digest: SpeakX.ai, Two Brothers Organic Farms raise funding

Compliance/regulatory update

- RBI’s gold pile tops $100 billion on surging bullion prices

- RBI cuts interest rate for second time as US tariffs kick in

- An Indirect Transfer In An Offshore Two-tier Structure Is Not Taxable In India – Tax Tribunal Rules In EBay-Flipkart Case

- RBI gold reserves cross $100 billion mark for first time amid price rally, highest share in forex reserves in 20 years

- Does it matter if India’s trends of nominal and real GDP growth diverge

- Rupee to take cues from RBI after assertive action; bonds seen rangebound

- RBI sold $7.7 bn in August to check rupee volatility