Harsh Batra

Harsh Batra

Hello,

This week, the Torrent Pharma-JB Chemicals $3.1 billion merger was cleared, representing a sector-defining consolidation in pharma, and one of the largest M&A transactions this year.

Also, Kotak Bank completed due diligence on IDBI. If a purchase materialised, it could be an outlook-defining moment for the sector.

Meanwhile, Tata Motors’ Iveco deal led the investment charts in an exciting quarter for India’s auto M&A as the sector’s supply chains slowly consolidate. But Tata Motors PV (passenger vehicles) business slipped by 0.25% because of a cyberattack, as S&P Global revised the stock’s outlook to Negative.

And finally, Softbank-backed Lenskart said it seeks to raise $829m in an India IPO which may become the country’s largest consumer tech listing.

I hope you enjoy this week’s roundup — please connect on LinkedIn to discuss your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

The bitter taste of over-supply

This month, India’s government announced a ₹37,952 crore ($4.55 billion) fertiliser subsidy for 2025–26 to shield farmers from input costs, as record rice harvests languished in overflowing warehouses, pressuring domestic prices.

Exporters struggled to find buyers of the unsold commodity in new markets such as Iraq, Indonesia and Saudi Arabia. Soybean‑meal exporters also failed to compete with global suppliers’ value chains and crusher margins.

Government subsidies cushion farmers but repel global private equity appetite. Many agritech investors pulled back this year, reducing rounds and cheque sizes versus 2024 as early stage funding slowed.

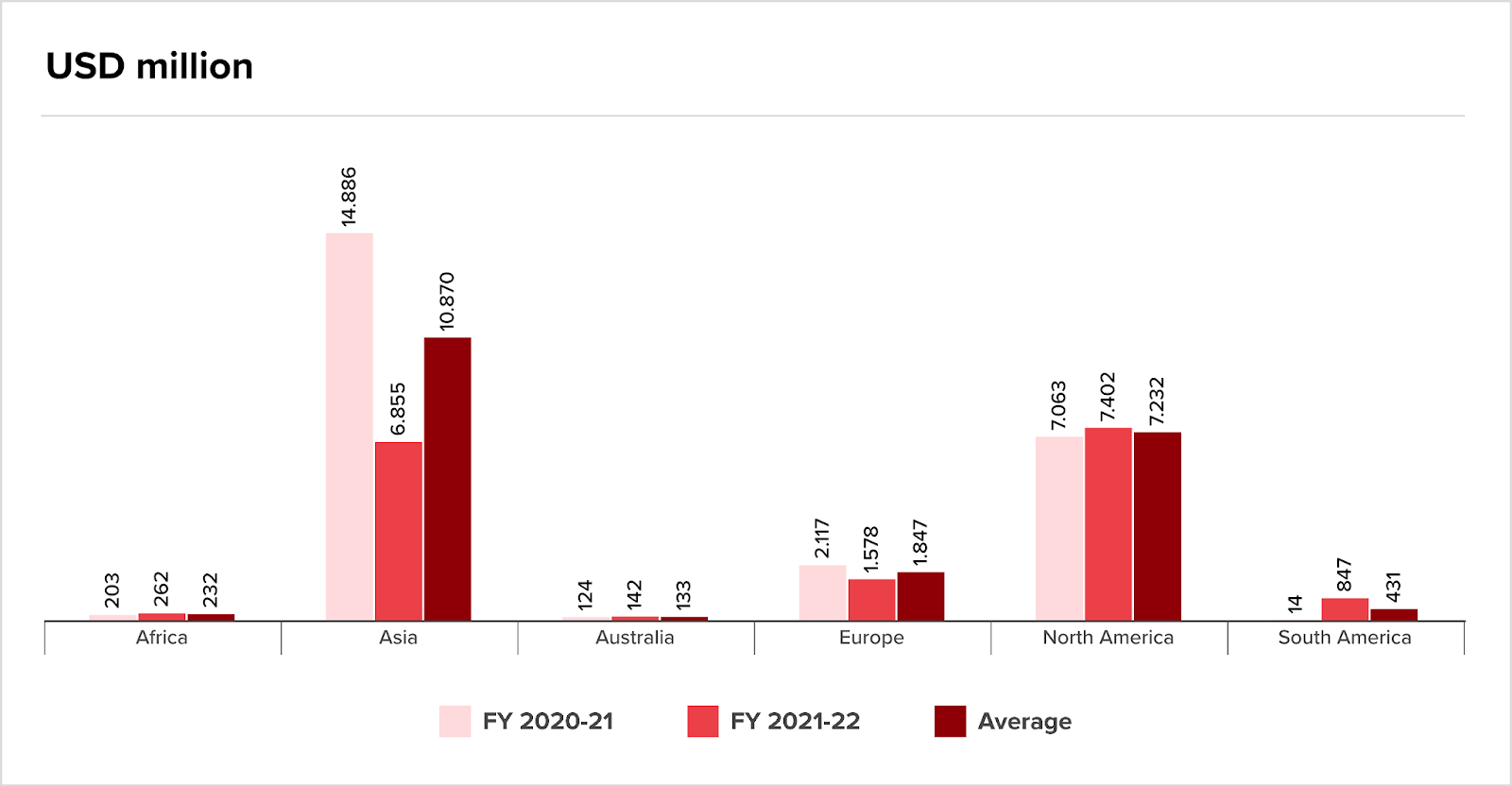

Global capital concentration by region

A key industry

Agriculture anchors India’s economy, employs nearly 43% of the workforce, contributes about 17–18% of GDP, and underwrites the country’s food security, rural incomes and inflation stability.

Every fluctuation in farm output or fertiliser prices ripples through the consumer basket. It also shapes India’s export earnings from rice and cotton to spices and marine produce, determining how much disposable income circulates in rural markets that drive demand for two-wheelers, housing, and FMCG.

In short, farm policy isn’t just about farmers; it’s the foundation of India’s growth and macroeconomic balance. But it’s not hard to see the sector is lagging.

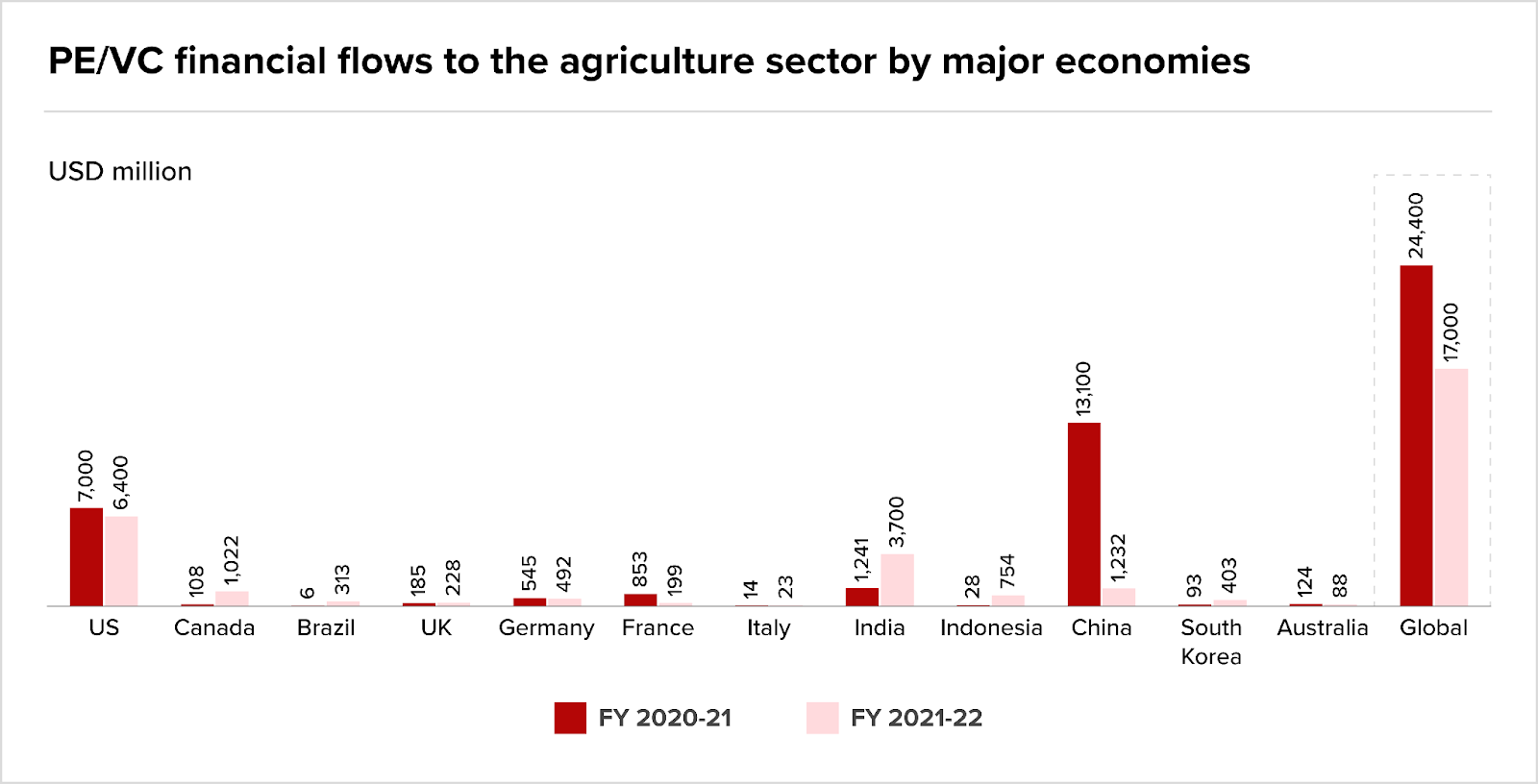

Investors see an underbuilt agritech market. Indeed, PE/VC interest fell from roughly $24.4bn in 2020 to about $17bn in 2022, as capital deserted India for the US and China..

This map shows the US/China concentration and India’s smaller share, showing the challenge facing the country’s start-ups when competing with counterparts in larger markets.

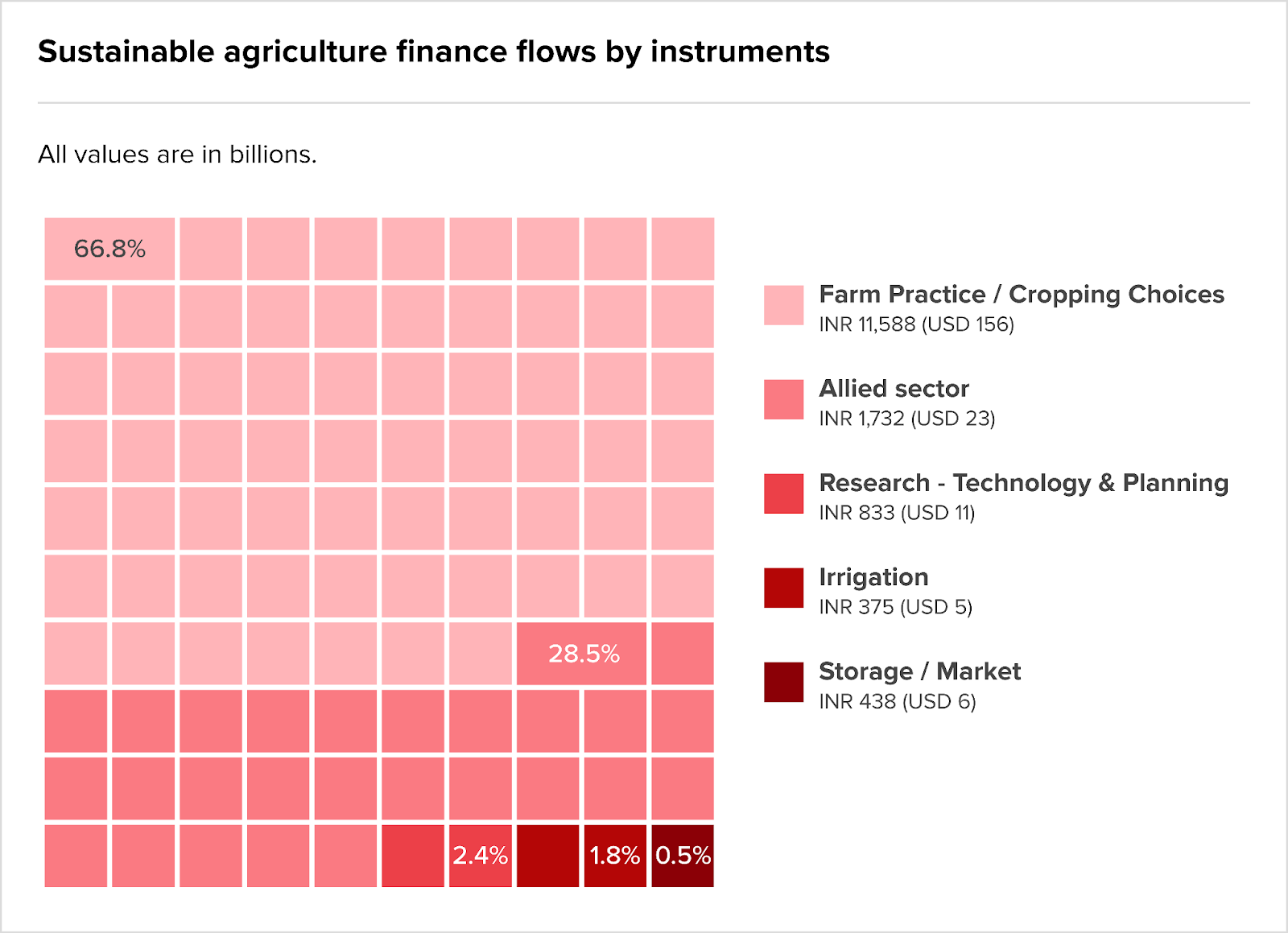

The instrument mix constrained innovation

Indian farmers relied on loans and public budgets as equity abandoned India’s innovators. Debt finance figured at 66.8%, while government cash accounted for about 28.5%. Equity and other instruments together contributed a tiny sliver.

In practice, this pushed capital into lower‑risk, revenue‑proximate plays rather than into Indian R&D or tech-led scale‑ups.

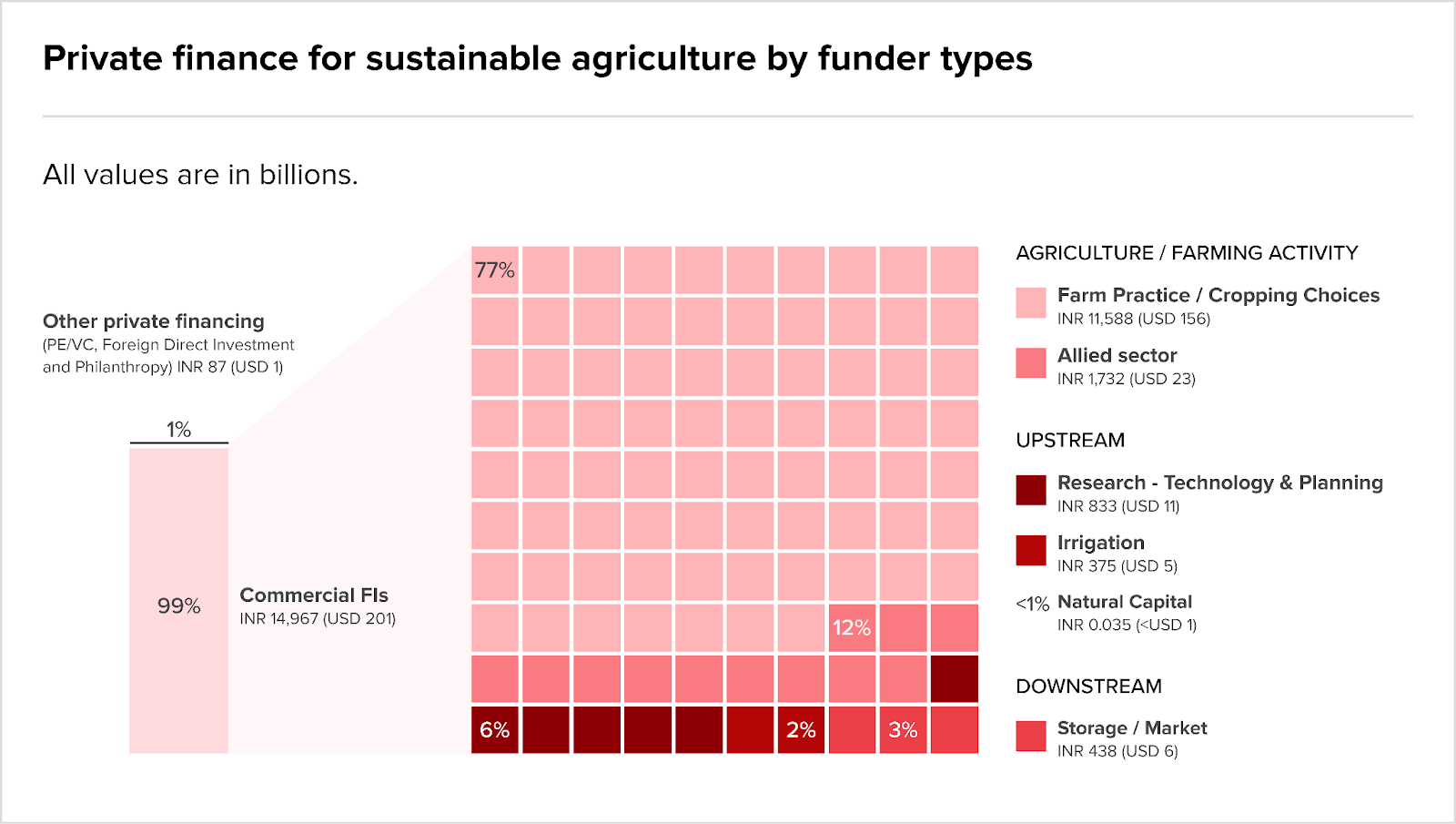

Where did the money go?

Within the private finance pool, commercial financial institutions accounted for about 99% of flows. This indicates private capital skewed toward credit products rather than VC equity and upstream R&D and irrigation as potential tech investments suffered.

In conclusion, India’s agriculture capital (mostly government subsidies) reinforced existing models instead of underwriting the risk of introducing precision agriculture, sensors, data platforms, cold‑chain robotics or irrigation engineering.

If policymakers rechanneled a share of subsidies and guarantees into outcome‑based investments, they might catalyse private investment into upstream agritech rather than merely providing current income flows.

The rumour mill

- US shutdown impact on India IT- Infosys buyback and Hindalco deals stuck in logjam

- TPG-owned digital engineering company Altimetrik completes acquisition of SLK Software

- Torrent Pharma-JB Chemicals $3.1 billion merger cleared

- Temasek in advance talks to back Indian healthcare fund manager

- Tata Motors’ Iveco Deal Powers Record Quarter for India’s Auto M&A at $ 4.6 Billion

- Tata Motors PV slips after S&P Global revises outlook to ‘Negative’

- Supreme Coated Board Mills Tamil Nadu plant put on the blocks; reserve price fixed at Rs 85.56 crore

- SBI, other PSU banks stocks rise up to 3% on reports of government move to raise FDI limit to 49%

- S&P cuts India’s Tata Motors passenger vehicles outlook on slow JLR recovery from cyberattack

- Reliance Retail to acquire insolvent Future Supply Chain for Rs 171 crore

- Prized European assets up for grabs as India Inc. looks abroad

- Premier to acquire solar inverter firm KSolare and transformer company Transcon

- Pavna Sports Ventures and Kri Entertainment Unite to Create India’s First Integrated Sports and Entertainment Powerhouse

- OIL Stake Sale On Feb 1, Govt Eyes Rs 3,000 Cr

- NCLT rejects Byju’s plea to stay rights issue of Aakash Educational Services

- NCLT admits Kamachi Steels to insolvency over Rs 40.77 crore debt

- NCLAT dismisses GLAS Trust’s plea against Aakash AGM, rights issue

- Kotak Bank complete due diligence to buy IDBI bank

- Kedaara Capital, General Atlantic eye 6-7% slice of Balaji Wafers

- Jana SFB’s universal bank bid hits pause as RBI returns application

- Indian rupee traders eye RBI, flows before fully priced in Fed rate cut

- India: BII commits $75m to Blueleaf Energy to boost renewable energy production

- India roundup: Tie-up with Dixon marks renewed Taiwanese investments in India’s EMS

- IDBI Bank divestment: Centre may soon invite financial bids as IMG set to meet on Oct 31 to finalise process

- Govt may top ₹50,000 cr from divestments, IPOs

- Gaming startup Giga Fun Studios files for voluntary liquidation

- Citibank Sets Sights on India with Planned Investment Boost

- Choice International Expands Wealth Management Business, Adds ₹635 Crore AUM Through Strategic Acquisitions

- China VC gap presents opening for investors: The Dietrich Foundation

- Canada’s CPP Investments eyes bigger India play after tripling portfolio

- Bank of Maharashtra classifies Reliance Communications loan account as fraud

- Asha Ventures in talks to invest in dairy startup

M&A news

- Why is the world betting big on Indian banks?

- Reliance & Meta create ₹8.55 billion enterprise AI JV in India — what it means

- Merging for Strength or Shrinking for Sale? Inside the Govt’s PSB Merger Plan

- Merger buzz: PSBs yet to hear from govt, focused on diluting stakes to meet norms

- M&A financing norms empower banks, with guardrails

- Indian tech sector records deals worth $1.48 billion in Q3: Report

- Indian markets slightly expensive but poised for long-term expansion: Kamal Ahmed

- Indian banking outlook to improve next fiscal as margin declines halt, says S&P arm

- Indian Auto Sector Saw Deals Worth $4.6 bn in Q3: Grant Thornton Bharat

- India’s Financial Sector Sees 127% Surge in M&A Activity, Reaching $8 Billion

- India’s banking story back on global radar as foreign deals pick up

- India on a balancing act between coal and renewables: S&P Global

- IMF Sees India’s Economy Growing At 6.6% In 2025–26

- Govt mulls Union Bank-Bank of India merger to form India’s second largest PSU lender: Report

- Deals in Flux: Thacker & Associates’ CA Prashant Thacker on How Tariffs Are Rewriting Cross-Border Valuations

- Blackstone’s India bank dream is a stretch

- Blackstone invests $706 million for 10% of India’s Federal Bank

- Aakash shareholders clear increase in authorised share capital

- ‘We have a robust loan pipeline of over Rs 70K cr,’ Rajneesh Karnatak MD & CEO Bank of India

Job moves

- Vivek Joshi Appointed as Director on State Bank of India’s Central Board

- Suzlon Energy shares jump 4% as Rahul Jain appointed as new CFO; what management says

- Former Standard Chartered India CEO Zarin Daruwala appointed as Group CEO of PL Capital

- BofA makes executive changes in technology and telecom investment banking teams, memo shows

IPOs

- Rebounding Indian IPO market shows governance, preparation now define success

- Indian stock broker Groww aims for $7bn valuation in IPO

- Indian eyewear retailer Lenskart seeks valuation of nearly $8bn in IPO

- Softbank-Backed Lenskart Solutions Seeks to Raise Up to $829 Million in India IPO

- Lenskart IPO Opens on October 31. How Much Its Early Investors Will Make

- India’s Akasa Air targets IPO in 2-5 years

Fundraising

- Uniphore raises $260m in Series F round led by strategic AI and tech investors

- True North Private Credit leads $40.8m funding in Innova Rubbers, Vee Tee Auto

- Torrent Pharma eyes India’s biggest bond issue of FY26 to fund JB Chemicals acquisition

- Smart Grid Analytics raises $3.3 million from strategic investors

- Secondary funds emerge as vital bridge in India’s maturing private capital market

- Realty Sector Sees over 2-Fold Jump in Capital Market Fundraising at $1.15 bn in Jul-Sep: Report

- RBI’s nod for bank-funded M&As comes at a great moment for the Indian economy

- Radiance and Sunsure secure Rs 6.8 billion funding from NIIF IFL

- Mandala Capital ropes in climate-focussed fund as LP for latest vehicle

- Indian fintech Optimo Capital raises $17.5m led by Blume, Omnivore

- India’s solar sector attracts $17.3 billion in corporate funding in Q3 2025: Report

- India’s Neo nears $250m final close on debut secondaries fund

- India’s green transition: Nation leads South, Southeast Asia, says S&P Global; private funding, policy push key drivers

- India: Prosus partners Accel to invest in early stage startups

- India: Asha Ventures, BII invest in snack brand Wonderland Foods

- India: AI memory infra startup MemO raise $24m led by Basis Set Ventures

- India regulator bars mutual funds from investing in pre-IPO placements

- India Quotient raises $129m for Fund V

- India Digest: CapitalXB Finance raises Premier Energies in M&A news

- ImpactAlpha LP/GP: Investors signal a renewed appetite to reduce food waste

- Honda Motor buys stake in India’s OMC Power to develop clean energy

- Global solar sector attracts $17.3 billion corporate funding in 9M 2025, down 22% YOY

- EaseMyTrip cofounder Prashant Pitti’s NBFC Optimo Capital raises Rs 150 crore in equity funding

- Blume Ventures logs initial close of fifth fund at $175 million

Compliance/regulatory update

- The untold story of operational creditors under IBC: How small players are left out in the recovery game

- Rs 19-crore land of Future Retail to go under the hammer

- Rethinking India’s Monetary Policy Framework: A response to the RBI Review

- RBI Unleashes Banking Power: New Capital Market Rules Set to Reshape India’s M&A Landscape

- RBI to exempt real estate rescue fund from AIF rules

- RBI regulatory arc for banking can be explained by weak animal spirits in the economy

- Overall financial conditions remain benign in October; says RBI bulletin

- Mint Explainer: RBI unveils draft norms for M&A financing: What it means for corporate buyouts

- Limitations of the IBC Amendment Bill, 2025: Speed at the cost of balance?

- How safe are cooperative bank deposits after recent RBI crackdowns?

- Government Securities market grows over twofold to Rs1,812 lakh crore by 2024: RBI

- Gold reserves vs dollar assets: Why is RBI buying gold and reducing investments in US Treasuries

- Gaja Capital gets Sebi nod for India’s first IPO by a private equity firm

- Calibrating Oversight: SEBI’s Consultation Paper To Overhaul Related Party Transactions Under The LODR Regulations

- AIBOA Raises Concern Over Growing Foreign Control in Indian Banking System