Harsh Batra

Harsh Batra

Hello,

This week a record $2.2bn ChrysCapital PE fundraise opened to Indian LPs for the first time – fresh dry powder that can accelerate buyouts, sponsor-led M&A and cross-border acquisitions in India, shifting bidding dynamics.

Meanwhile, American TGH eyed a potential $6bn investment in Vodafone Idea, contingent on a government package: PE capital plus state-policy conditionality that could trigger sector consolidation and contestable restructurings.

And Indian regulators reportedly blocked SBI’s bid to increase its stake in Investec JV, which could affect deal structures, valuations, and the willingness of buyers to pursue similar cross-border or JV-related M&A.

I hope you enjoy this week’s roundup – please connect on LinkedIn to discuss your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

The truth is somewhere in between

This week, BCG’s M&A report, Upside of Uncertainty, and a CSEP article about India’s Private Investment Paradox piqued interest for reasons which will become clear.

BCG’s core thesis is that uncertainty doesn’t have to be the enemy of M&A. The study says that while volatility suppresses deal values, it creates outsized opportunities for experienced, disciplined acquirers. In uncertain markets, success shifts from expansion to precision, favouring smaller, same-industry, and local deals.

The global context

The post-2020 era has normalised volatility. Trade tensions, tariffs, geopolitical conflicts, and supply disruptions drive unpredictable markets.

BCG uses Semi-SDRET, a global downside-only volatility measure, to track uncertainty more accurately than the VIX. In 2024-25, Semi-SDRET was 20–30% above long-term medians, signalling widespread turbulence.

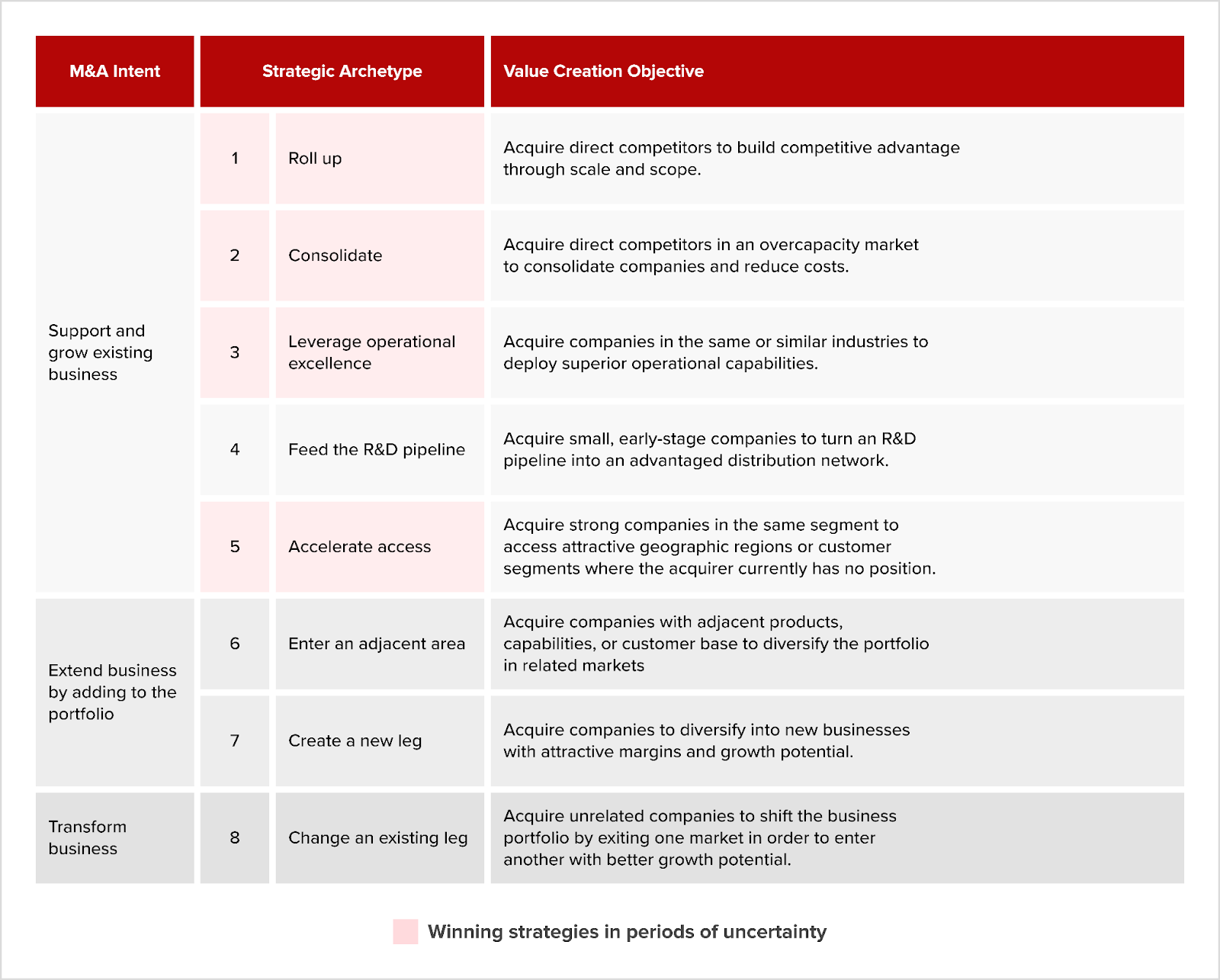

The report notes several M&A trends that occur during periods of economic uncertainty:

Deal size and volume: Average deal size, the report discovered, falls by about a third (34%) from $280m to $186m during uncertain periods.

Sectoral differences: Cyclical sectors such as materials or tech see more consolidation while defensive sectors such as healthcare, and consumer remain steady.

Cross-border and industry patterns: Domestic, same-industry deals surge approximately 200%. Cross-border and cross-industry deals fall 31% and 70%, respectively. Familiarity is preferred over diversification.

Financing: Stock-based deals rise from 21% to 36% of value (cash falls, debt rises).

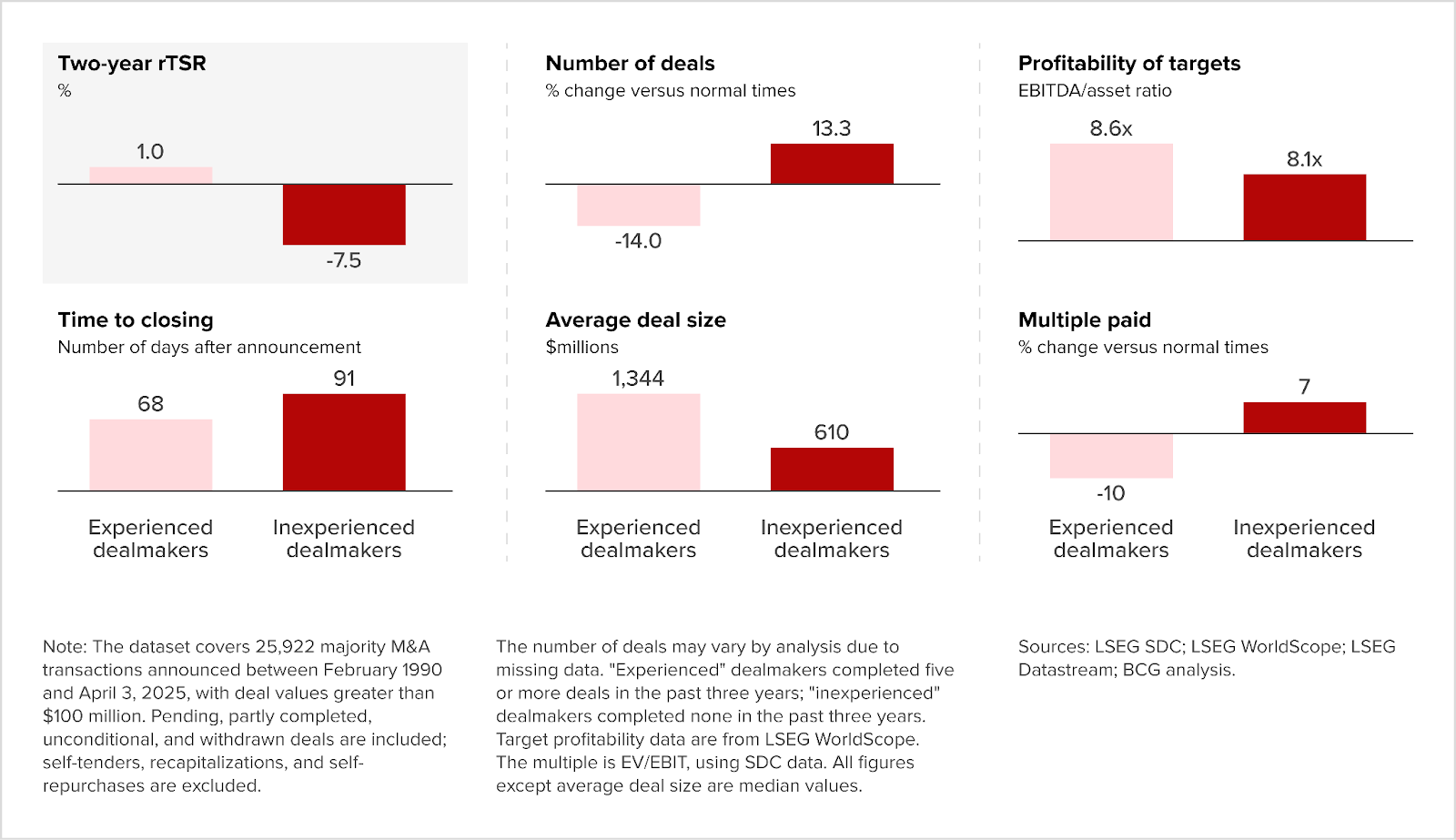

Time to close lengthens modestly: From 68 to 91 days, reflecting slower diligence and cautious negotiations.

Returns: During volatile periods, the median two-year total shareholder return (rTSR) from M&A turns slightly negative at -0.4%. Yet experienced acquirers still generate about +1%, while inexperienced ones lose around -7.5%, making professional dealmaking experience the single biggest driver of performance.

The consultancy also says the most typical deals are roll-ups and consolidations as businesses acquire similar firms to improve efficiency and scale.

Sector data

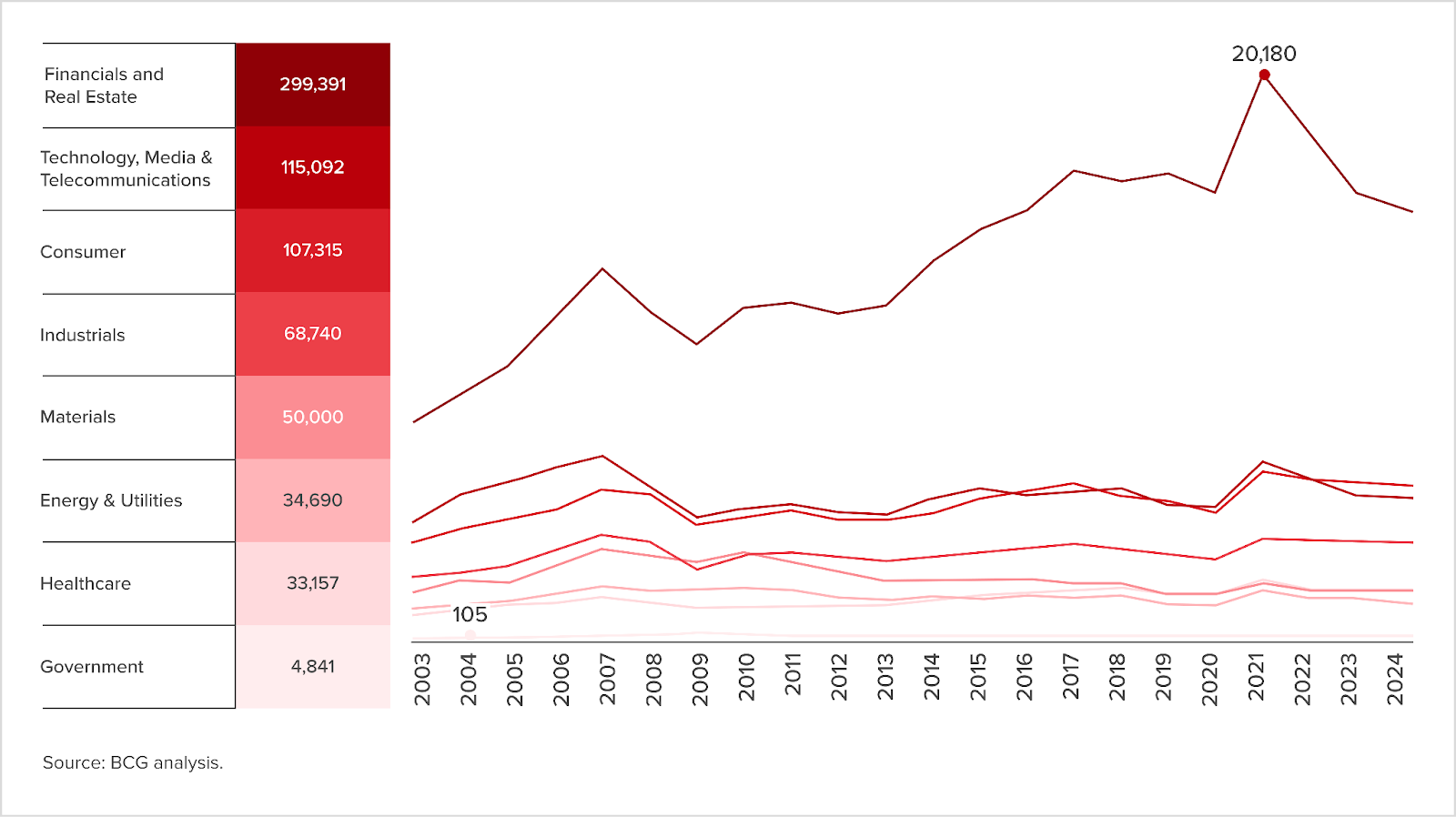

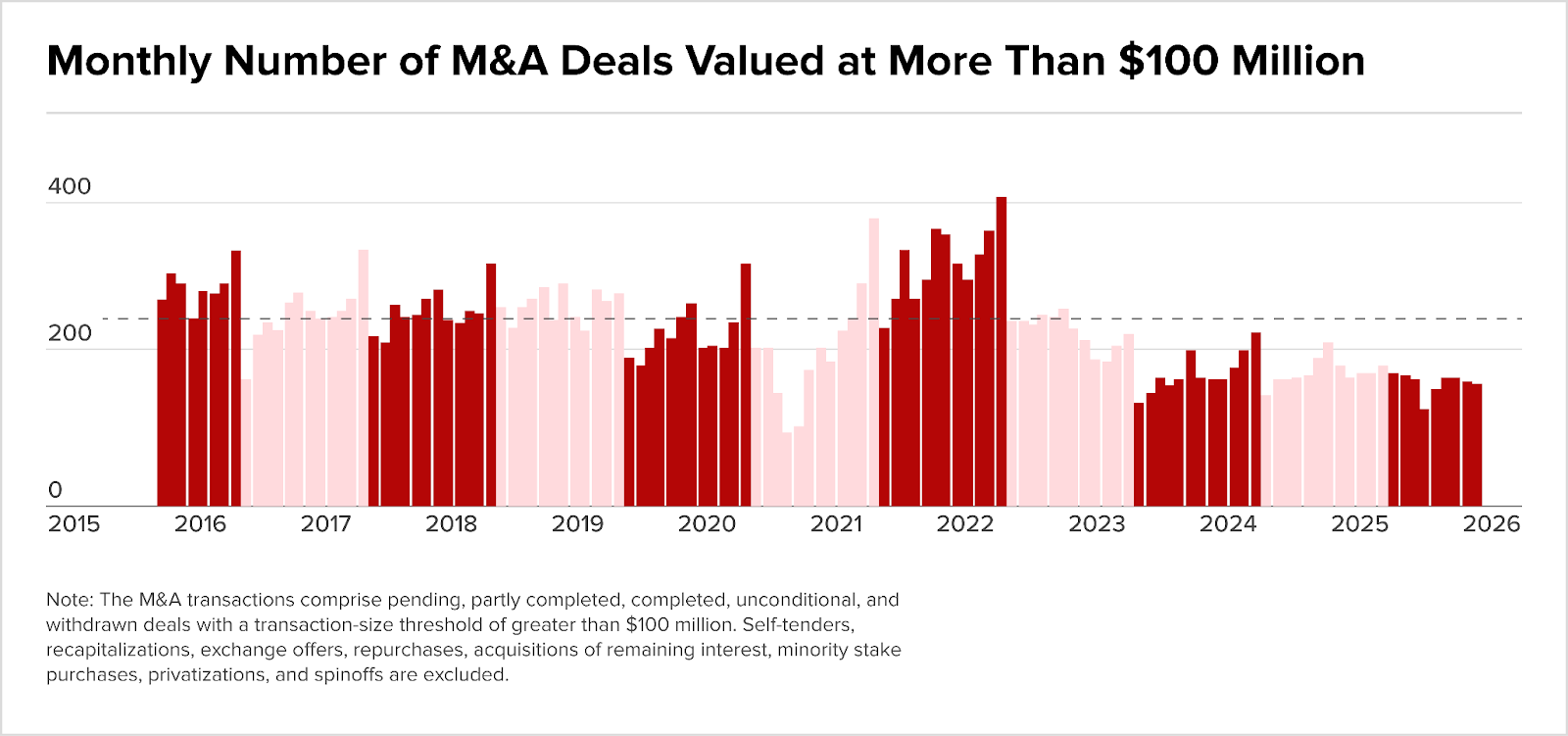

BCG also looked into trends in deal volumes and values. It found that ‘financials and real estate’ dominate in deal value, and TMT is next at $115bn. Consumer is at $107bn, and industrials at $69bn; the report revealed volume peaked in 2021 (20,180 deals) during the Covid pandemic.

Deals worth upwards of $100m peaked in 2021-22 (around 400/month). The years 2023-25 showed a slowdown but sustained mid-tier activity – fewer mega- more midmarket-deals.

BCG urged companies to play offense smartly, focussing on near-core roll-ups and good due diligence in times of uncertainty.

CSEP’s take on India’s private investment paradox

In a separate article published by CSEP, the economists assert that India’s private companies are investing less in tangible productive assets like plants and machinery.

This implies weak expansion and capacity building, even though optimism and stock valuations are sky high. Great expectations don’t result in actual private capex, creating bullish sentiment where execution is weak.

The authors say that policymakers and markets expect private investment to drive the next growth phase, but data show muted capex recovery. Corporate profits and capacity utilisation are improving, yet fresh project announcements lag.

Investment hasn’t picked up, the authors say maybe because of global uncertainty with high interest rates, supply shocks, and geopolitical tensions. No one knows what is to come. There are domestic headwinds such as weak consumption, slow rural demand, and financial tightening in India.

The researchers also say that government spending on infra ‘crowds in sentiment but crowds out private balance sheet appetite’.

Corporate behaviour is governed by these signals. Firms use profits for deleveraging, dividends, and buybacks rather than new capacity, and prefer asset-light, digital, or M&A-based growth, instead of greenfield projects.

Capital markets and policy gaps don’t help, either.

While FDI and private credit inflows have grown, these favour financial and services sectors over manufacturing. Incentive schemes (PLI, Make in India, etc) haven’t yet converted to dollars on the ground.

How do these very different takes connect?

BCG asserts that uncertainty creates opportunity for experienced dealmakers, while the Indian economists say all India is really seeing is many promises but little desirable outcome.

Risk taking in India remains suppressed as firms avoid new capex and prefer financial or M&A-led expansion. Money has also migrated from manufacturing to services, especially financial services. Policy clarity is needed to turn optimism into tangible investment.

Easier said than done.

The paradox is that India expects private‐sector investment to drive growth and job creation, but actual private investment seems weak and declining, especially in manufacturing and equipment. A cycle of what the think tank calls ‘paper optimism’ (big announcements, little execution). Approved projects have fallen as a share of GDP from 1% to 0.7% of GDP.

Despite India’s abundant reform impetus and investment announcements, private-sector investment is languishing. Firms are optimistic on paper, but lack the demand, return prospects and execution confidence to follow through, creating a private investment paradox.

The rumour mill

- KKR plans investment expansion for insurance unit in India

- Honeywell taps insiders to helm new aerospace company ahead of 2026 split

- India’s Groww bets big on wealth, commodities as broking’s share falls

- RBI’s Dollar Short Positions Rise as Rupee Defense Intensifies

- US PE Firm TGH Eyes $6 Billion Investment in Vodafone Idea, Contingent on Government Package

- Bank of Baroda, Bank of India other PSU banks rally up to 3% amid reports of merger, privatisation of smaller lenders

- ED attaches ₹4,462 crore prime Navi Mum land in Reliance Communications fraud case

- E-Auction set for Jammu assets of Surya Pharmaceutical with reserve price of ₹92 crore

- IDBI Bank hits 52-week high; stock rallies 9% on heavy volumes

- TCS $6.5 billion AI infra play signals private capital surge

- S.A.L. Steel Ltd. Announces Major Share Acquisition by Sree Metaliks

- Auction alert: Rs 37-cr assets of Venus Garments to go under the hammer

- Beyond the Buyout: Will India’s $12b bet unlock India deep tech potential?

- SC dismisses GLAS, BYJU’S RP plea; clears rights issue of Aakash

- Green Climate Fund to invest $20m in Kshema General Insurance

- From a sprawling HQ to a mailbox: Inside the Great Byju’s sale

- Netflix taps bank to explore bid for Warner Bros Discovery

- Indian Auto Giant Mahindra Officially Closed Its $175 Million Australian Aircraft Business — Here’s Why

- India: BII commits $75m to Blueleaf Energy to boost renewable energy production

- LIC stake sale: Centre mulls up to $1.5 bn divestment by year-end; Sebi float rule drives move

- India: Affirma, 360 One Asset to invest $56m in engineering service RMSI

- MTR & Eastern owner Orkla readying Rs 700 crore to acquire new brands, says MD-CEO Sanjay Sharma

M&A news

- India deal market surge: Q3 hits 999 deals worth $44.3bn

- Allied Blenders and Distillers Approves Merger of Two Wholly-Owned Subsidiaries

- KKR’s Bae: Apac will generate half our PE distributions this year

- From lab to launchpad: Bluehill’s $45m bet on India’s deep tech

- Tax cuts, rate cuts consumption boom; SBI dials up credit growth outlook

- India’s M&A market stays steady amid global uncertainty: Report

- Corporate deals in country hit six-quarter high in Q3 CY25, recording USD 44.3 bn in transactions: PwC

- ‘India needs large, resilient banks to compete globally,’ Debadatta Chand CEO Bank of Baroda

- IDEX Q2 2025 slides: modest growth amid market uncertainty, maintains cautious outlook

- India is one of the most active markets in Asia for KKR: Scott Nuttall, co-CEO

- India Sees Slump in Greenfield Projects in Manufacturing: UNCTAD Business

- Global mergers and acquisitions rise 10% to USD 1.9 trillion in 2025: BCG report

- Deal value of private equity and venture capital reaches $11.7 billion in Q3

- Pharma and Healthcare Deals Jump 166 Percent to $3.5 Billion in Q3

- Indian regulator blocks SBI’s bid to increase stake in Investec JV-report

- India: how the CCI shapes merger remedies for market integrity

- Between Expectation and Realisation: India’s Private Investment Paradox

- Does Your M&A Deal Need An AI Strategy?

- Canara Bank-led consortium sells Rs 520-cr debt of Karanja Terminal to Prudent ARC

- From the Opinions Editor: On interest rates, is RBI joining the right dots?

- India set to be Apac’s private credit engine

- Welspun Corp approves acquisition of further 4.11% stake in Welspun Specialty Solutions

- Nippon Steel seeks Indian approval for global acquisition of Krosaki Harima

- RBL and Yes Bank: How India’s two largest banking sector deals happened

- Viewpoint: The coming of age of the Indian banking landscape

Job moves

IPOs

- Groww raises Rs 2,985 crore from investors ahead of IPO, sovereign funds, SBI MF join anchor book

- Shiprocket gets Sebi nod for Rs 2,500-crore IPO: sources

- Our scale & financials justify an IPO: Pine Labs CEO Amrish Rau

- An IPO’s on the table for near future: Equirus Group MD Ajay Garg

- Highlights: Will Orkla India IPO list with a hefty premium on November 6? Check what the GMP indicates

- Norway’s NBIM, ADIA and SG’sGIC to invest in India’s Groww IPO

- Lenskart IPO: A Critical Analysis of Valuation, Greed, and Red Flags

Fundraising

- India’s Chryscapital raises its largest fund with $2.2-billion

- Solar module recycling firm Beyond Renewables secures $50 million

- Equirus Partners with Industry Veteran Srinath Srinivasan to Launch INR 1,500 Cr Private Equity Fund

- Goyaz raises $14,6bn funding led by Norwest and other India deals

- India: IFC commits $150m each to Signature Global, DCM Shriram

- Tata Capital ties up with Green Climate Fund to back climate-tech startups

- India: SalarySe raises $11m in Series A round led by Flourish Ventures

- India Deals Barometer Report: Startup funding rebounds slightly in Sept

- Indian digital trade financing firm Drip Capital secures $50mn credit line from TD Bank

- India: A91 Partners leads $28m funding in Intrcity Smartbus

- RPSG Capital leads $2.3m funding in BabyOrgano and other India deals

- India: SaaS startup MoEngage raises $100m led by Goldman Sachs, A91 partners

Compliance/regulatory update

- Default Is Default—Even On A Half-Disbursed Loan: NCLAT Clears Axis Bank’s CIRP Trigger

- USD/INR recovers possible RBI’s intervention-driven early losses

- Gold rally has reserves jumping by $31 billion this fiscal so far: RBI

- Car sales hit record high in Oct, driven by GST rate cut: FM

- RBI’s hard line on 2032 paper draws swift reaction from investors

- Nvidia joins in as India Deep Tech Alliance garners $850m commitments