Harsh Batra

Harsh Batra

Hello,

This week, public sector lenders SBI and PNB drafted a playbook to tap the country’s Rs 1.2 lakh cr ($14.3 billion) M&A market. This hints at large domestic banks actively structuring for a wave of buyouts and consolidations, while assessing financing and competitive appetite across sectors.

Meanwhile, the Indian central bank proposed a 70% cap on financing for acquisitions which would change transaction/sponsor economics. Let’s watch how this develops.

Also, KKR and ChrysCapital dominated the news: KKR is returning $350 million in carry after its Asia fund underperformed, spotlighting tighter LP scrutiny across the region. In contrast, ChrysCapital surged ahead, leading a ₹6,000 crore-plus bid for Nash Industries and closing a record $2.2 billion.

Finally, Blackstone might acquire 80.15% of Aadhar Housing Finance with regulatory approval.

I hope you enjoy this week’s roundup – please connect on LinkedIn to discuss your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

India’s edtech learns a lesson

When India’s edtech boom peaked circa 2021, the sector seemed unstoppable. The pandemic had forced 250 million students online, venture funding poured in, and valuations ballooned on the promise that digital learning would forever change education delivery.

But like most pandemic darlings, the sector’s growth story is now undergoing a painful correction.

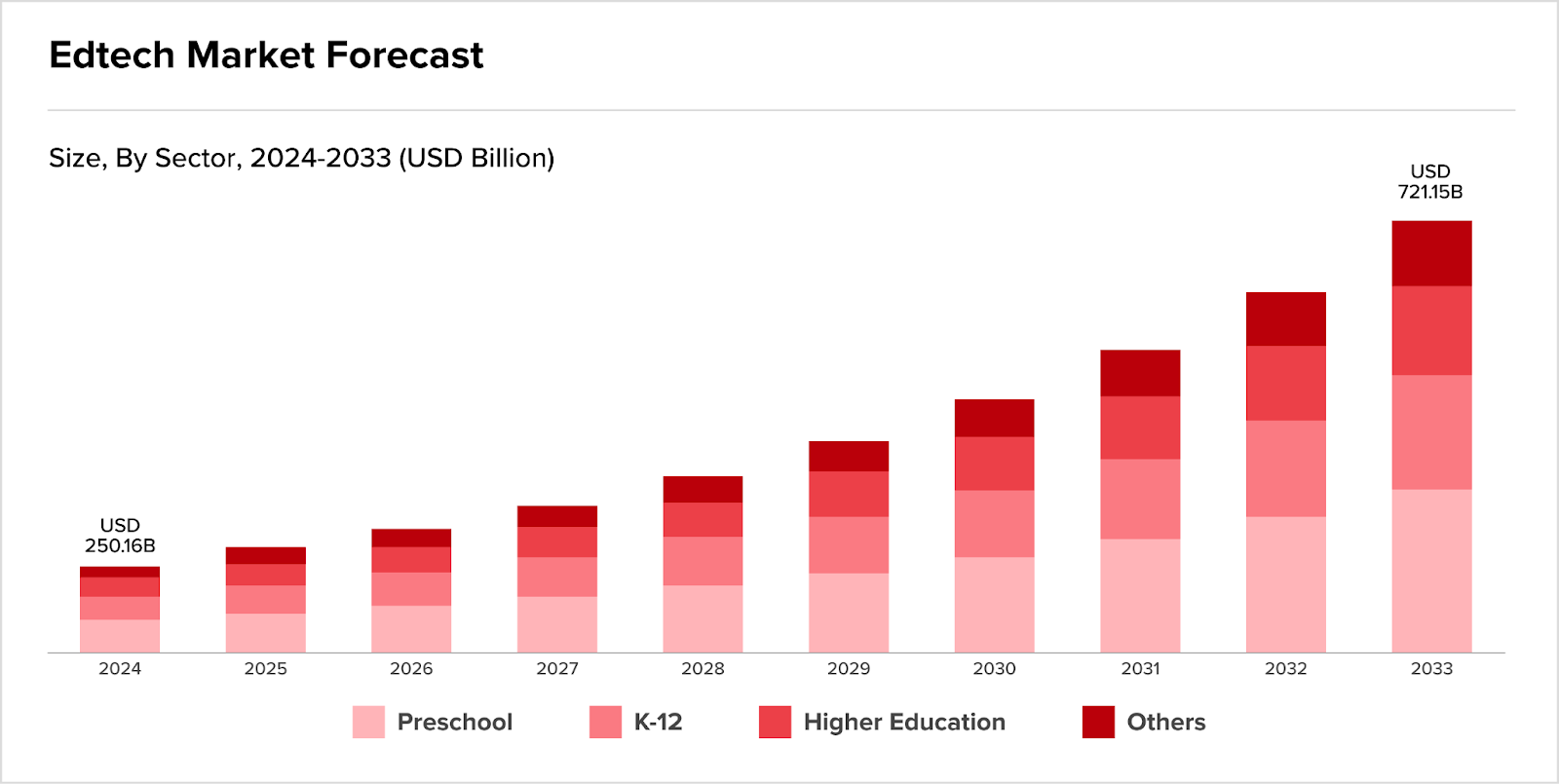

Globally, the market remains on a long-term growth curve. According to optimists, it might expand from $250.16 billion in 2024 to $721.15 billion by 2033, nearly triple its size as adoption deepens across preschool, K–12, higher education, and upskilling.

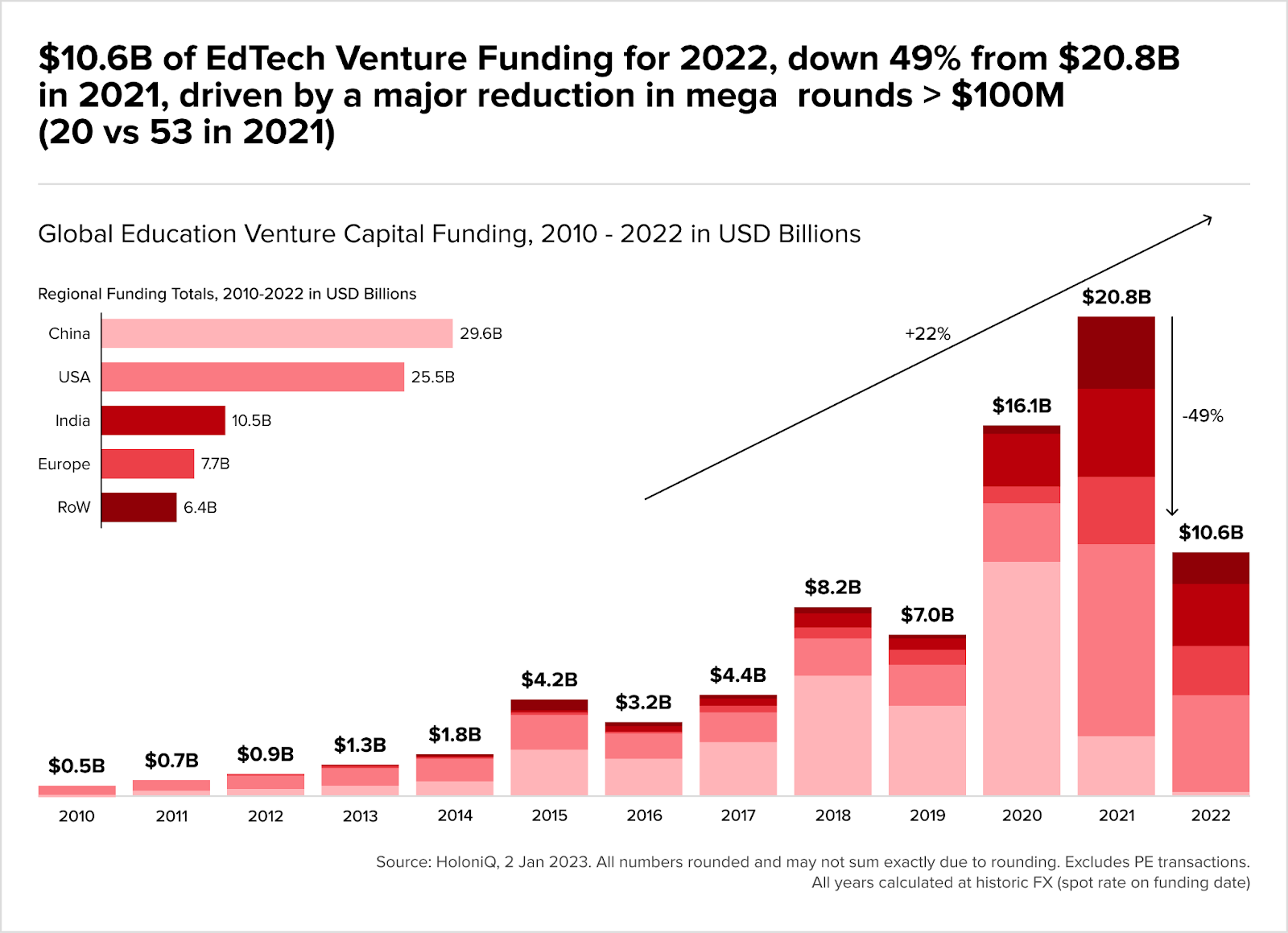

Yet HolonIQ, in 2022, said global edtech VC funding had halved (49%) year-on-year to $10.6 billion, down from $20.8 billion in 2021. This was caused by the collapse of the mega-rounds of $100 million+ from 53 in 2021 to just 20 in 2022.

India, which had been the third-largest recipient of global edtech capital after China and America, felt this correction deeply. It has attracted around $10.5 billion since 2021, but only around one billion in the past two years.

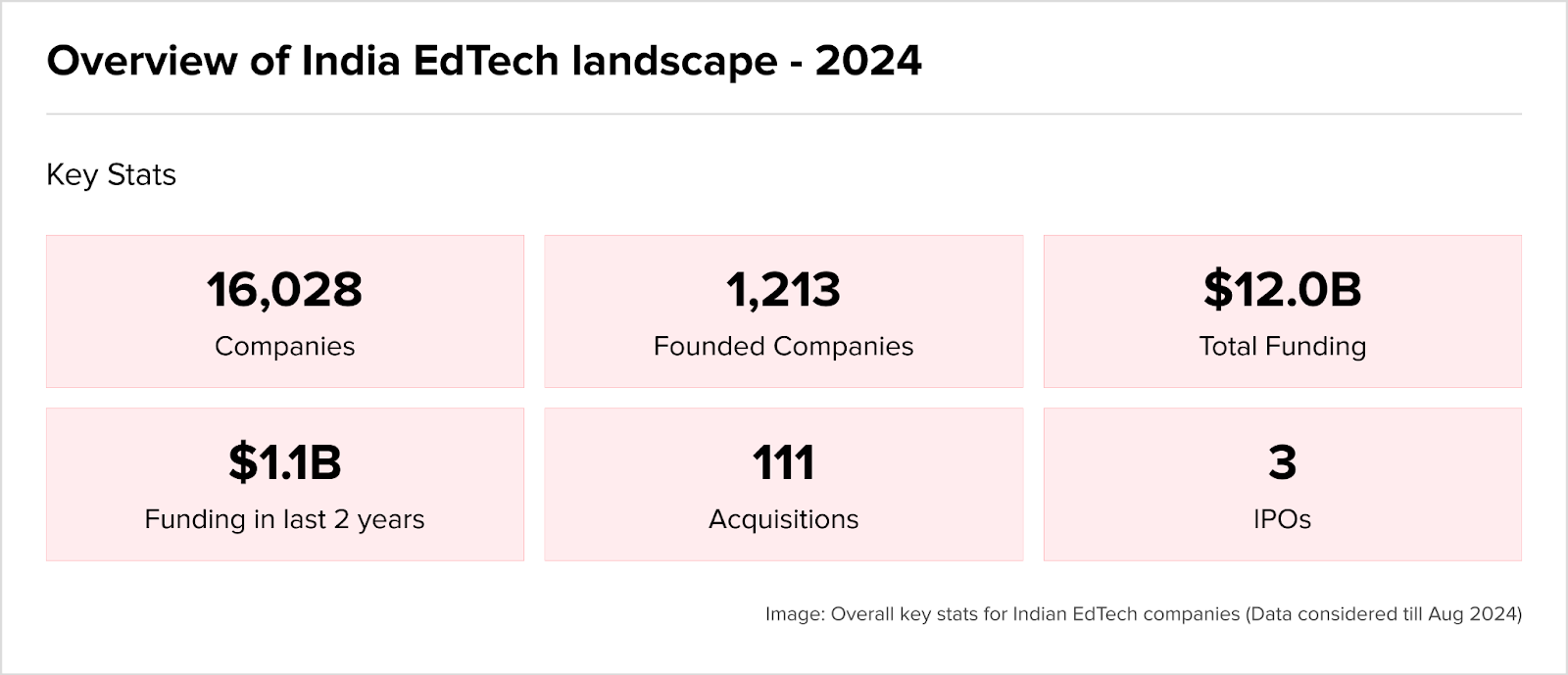

Still, India counts over 16,000 budding and growing edtech companies, of which more than a thousand are venture-funded, with cumulative funding at $12 billion.

There have been three IPOs showing the ecosystem hasn’t gone to seed completely and what’s emerging are cash-efficient firms which might just outlast the overfunded giants.

Byju’s bubble

No story captures overreach better than Indian edtech firm, Byju’s. Once valued at $22 billion, the company’s collapse has become a Harvard study in hyper growth gone wrong.

Its downfall stemmed from opaque governance and reckless acquisitions, such as WhiteHat Jr. and Aakash Educational Services, financed through debt. As post-pandemic demand waned, Byju’s failed to manage cash flow, delayed financial filings, and alienated investors.

Layoffs, board exits, and lawsuits followed, a dramatic reversal for a company that once shone with startup ambition.

Byju’s also misread the market’s cultural shift: parents and students, fatigued by screens, began returning to offline coaching, exposing the fragility of edtech models that were purely digital and aggressively priced.

Regard PhysicsWallah: Founded by Alakh Pandey, PhysicsWallah represents the opposite end of business. Built on affordability and teacher-driven trust, PW reached profitability early by combining low-cost digital courses with offline study centres across Tier-II and Tier-III Indian cities.

While the $100-million it raised at a $1.1bn valuation (when it became a ‘unicorn’) in 2022 was modest, its fundamentals were stronger than Byju’s: positive cash flow, measured expansion, and deep student engagement.

Comparatively, Byju’s raised over $5bn from investors including Tiger Global, General Atlantic, Sequoia, and Qatar Investment Authority deploying much of it for expensive acquisitions such as of Aakash, WhiteHat Jr., etc – before filing for bankruptcy.

PW’s has planned its IPO for about a year from now. It could restore investor confidence in India’s edtech narrative.

From form to content (or scale to substance)

Vanity valuations are giving way to sustainable business models anchored in meaningful, tangible values like pedagogy and teacher credibility, enabled by tech. With AI, adaptive learning, and varied Indian languages content, opportunity remains vast. Hybrid classrooms will remain indispensable. The edtech players that balance ambition with accountability will define the sector’s second act.

In other words, India’s edtech story may be shifting from scale to substance or from less heat to more light.

The rumour mill

- Akzo Nobel India Announces Strategic Agreements Post Acquisition Deal

- Brookfield India Reit plans to acquire business park for over ₹13,000 cr

- CarTrade set to acquire CarDekho in deal valued at over $1.2 billion

- ChrysCapital leads race for stake buy in Nash Industries valuing firm between Rs 6,000 cr-Rs 6,300 cr

- ChrysCapital, InCred Capital get CCI’s nod to acquire stake in ILJIN Electronics

- Creditors asked to submit claims as of Neptune Ventures liquidation process begins

- Delhivery Q2 Results: Co turns to red, suffers net loss of Rs 50 crore despite 17% rise in revenue

- Exclusive: Manipal group’s Ranjan Pai expresses interest in bidding for bankrupt Byju’s parent

- FMO proposes $22m Sunsure Energy solar PV project in India

- FMO weighs investment in Indian NBFC Ecofy Finance

- Glitter with risks: SEBI’s warning and India’s digital gold dilemma

- Global credit guarantor bets big on India with $500 million plan, exec says

- Goldman Sachs sells 0.1% stake in Kaynes Technology for Rs 44 crore

- Goldman Sachs upgrades Indian stocks to ‘overweight’ on growth momentum

- Heubach Colorants India Proposes Name Change to Sudarshan Colorants India, Seeks Shareholder Approval for Key Resolutions

- India’s RBL Bank says Emirates NBD to launch open offer on December 12

- Inside Unacademy’s potential sale to upGrad and the end of edtech’s golden age

- JSW in talks with Japan, South Korea firms for India battery JV to cut China reliance

- LGT Capital Partners eyes Asia PE secondaries, leans into China

- Maritime Development Fund set to take 10% stake in oil firms JV

- Market size of India’s hospital sector projected to reach USD 202.5 billion by 2030: Brickwork Ratings

- NCLAT sets aside private sale of Corporate Power Ltd, orders fresh bidding

- NCLT admits twin insolvency pleas by NARCL against Era Infra Group cos

- Perpetuus Secures Indian Joint Venture to Scale production of Graphene Masterbatch for Tyre Industry

- PIDG’s credit guarantee unit to increase India exposure with $500m plan

- Saudi Arabia’s PIF seeks CCI nod to acquire additional 64.57% stake in Olam Agri

- SG’s Wilmar to buy 13% stake in India’s AWL Agri for $529m

- Spinny to acquire GoMechanic in Rs 450 crore cash-plus-stock deal

- State Street to Enter Indian Mutual Fund Market via Joint Venture in GIFT City

- STT in Talks for India Mutual Fund Stake: Aligns With Growth Strategy?

- Surprise! Air India is now a smaller airline, a year after Vistara merger

- Temasek in advanced talks to back Indian healthcare fund manager

- Thaw in India-China ties: Quicker PN3 nod for China JVs in works

- With merger in the books, Mallinckrodt and Endo rebrand as Keenova and spin off Par Health

Salaries and bonuses

M&A news

- Blackstone to acquire 80.15% of Aadhar Housing Finance after CCI approval

- AI to augment ideas, help firms move up the creative stack: Figma global CTO

- Ancient roots, modern vision can build India’s financial sector

- Bain Capital sees Asia as private credit’s ‘clear winner’ amid global growth surge

- Beyond the Buyout: Asia distributions to drive next series of PE mega funds

- Broad-based deterioration in trade in October

- Co-Diagnostics Engages Maxim Group to Pursue SPAC Transaction for its Indian Joint Venture, CoSara Diagnostics Pvt. Ltd

- From $64m to $2.2b: ChrysCapital’s journey mirrors India’s PE revolution

- GIC-backed Asia Healthcare’s entry into India’s diagnostics stalls

- Greenberg Taurig Continues to Intensely Execute Its Global Strategies, Again Bolstering Its Singapore Office

- Hamilton Lane partners with Figure to launch blockchain-native registered investment fund

- Indian retailer Trent posts profit rise on store expansion; cuts Zara joint venture stake

- Kesar Reports H1 FY26 Results, Acquires Stake in Nexa Infraspace, and Announces Director Resignation

- Modelling public-private exposure

- Moneycontrol Pro Panorama | Is India an AI hedge trade?

- Not rushing our firms to public markets; no pressure to exit: SoftBank’s Sumer Juneja

- Ripple Announces $500 Million Strategic Investment Led by Fortress and Citadel Securities, Valuing the Company at $40 Billion Following Record Growth

- SBI, PNB draft joint playbook to tap country’s Rs 1.2 lakh-cr M&A market

- Singtel offloads about $1.2bn stake in Bharti Airtel

- SoftBank posts first annual profit in four years, but Ola and Swiggy weigh on Vision Fund 2 in Q4

- Stronger earnings and urban demand could revive FII confidence in India: Gautam Trivedi

- TVS Motor divests $33m stake in Rapido to Accel India, Prosus

- Warburg’s Perlman: Apac likely to benefit most as LPs rethink US exposure

- WeWork India’s quarterly profit tumbles despite record revenue

- Zydus Wellness posts ₹53 cr Q2 loss, despite robust sales

- Owl Ventures, BII co-lead $18m funding in Tetr College and other India deals

Job moves

- Delhivery CFO Amit Agarwal to step down; Vivek Pabari will take over

- Gaurav Sharma Appointed Head of Hotels & Hospitality Group at JLL India and Senior Director, Hotel Capital Markets, Asia

- Greenberg grows Singapore bench in cross-border boost

- HDFC Bank’s MFI chief K Venkatesh set to join Spandana Sphoorty as CEO

- HMT Limited Appoints M&A Associates as Secretarial Auditor for Five-Year Term

- Private lender IndusInd Bank appoints Amitabh Kumar Singh as new CHRO

- Sharad Malhotra appointed as MD of Nippon Paint India

- Trilegal strengthens Corporate practice with the appointment of Raya Hazarika as Partner, bringing its equity partnership to 150

- TVS’ Venu Srinivasan appointed vice chairman of flagship Tata Trust

IPOs

- After a sellout IPO, Lenskart makes weak debut on bourses amid valuation concerns

- Global beer giant Carlsberg picks Citi, JPMorgan as advisors for India IPO: Sources

- Groww IPO: Check day 3 subscription status as GMP falls sharply after muted listings

- Hyderabad-based Nephroplus IPO gets Sebi nod

- India Digest: Tiger Global exits Ather Energy; InCred plans IPO

- Indian edtech firm Physicswallah sets IPO price band at $3b valuation

- Indian eyewear retailer Lenskart valued at $7.7n in tepid market debut

- Indian Pine Lab’s $440m IPO fully subscribed despite valuation concerns

- LG arm, Tata Capital power India’s record IPO haul in October

- Orkla India’s INR16.6 billion IPO marks latest milestone in India’s ECM boom

- State Bank of India to sell 6.3% stake in asset mgmt arm via IPO

- State Bank of India, Amundi to jointly sell 10% stake in SBI Funds Management via IPO

Fundraising

- IFC commits $60m to PE firm Everstone Capital Fund V

- Fund Friday: Top fundraising news in private equity

- Funding and acquisitions in Indian startup this week [Nov 03- Nov 08]

- AI investor Glasswing Ventures seals $200m to close biggest fund yet

- Allianz’s $500 mn infra credit fund with India mandate ropes in key LP

- Ex-Wall Street banker Dhruv Jhunjhunwala launches Novastar Partners to back India’s private market opportunities

- Fund X represents a 60% increase over previous $1.35 billion Fund IX closed in 2022

- India: Digital lender Finnable secures $57m funding from Z47 , TVS Capital

- Indian food delivery platform Swiggy okays up to 1b fundraise via QIP

- Khaitan guides ChrysCapital’s $2.2bn record India fundraise

- Partners Group-owned Sunsure raising offshore financing for solar project

- Private credit’s Perpetual Motion machine

- Wilmar unit to acquire 13% of Mumbai-listed joint venture with Adani

Compliance/regulatory update

- At 0.3% retail inflation hits record low in October

- CCI Approves Lence Pte. Ltd.’s Plan to Raise Stake in AWL Agri Business Ltd

- Editorial. RBI’s calibrated opening up of acquisition loans is correct

- FMO weighs investment in India’s AMPIN Energy

- From Sealing the Deal to Breaking It Apart: Legal & Tax Considerations for Unwinding M&A Transactions in India

- Fuelling domestic capital formation via acquisition finance

- How a central bank move to slap down fund diversion split private, public sector banks

- India’s inflation cools to record 0.25% in October, strengthening rate-cut hopes

- India’s Ranking in Major Global Indexes 2025

- Lifting of curbs on bank acquisition financing to aid economy, says RBI chief

- Loan against silver: Not just gold, you can take loan against white metal; but what’s the maximum limit for such loan?

- Merger Control Comparative Guide

- RBI proposes 70% cap on financing for acquisitions and limits on CME

- RBI ramps up defence of rupee near record lows, curbs excess volatility

- RERA over IBC: The Supreme Court’s course-correction in real estate Insolvency

- Rupee Holds Steady As RBI Intervenes To Contain Excessive Market Volatility