Harsh Batra

Harsh Batra

Hello,

This week, Carlyle group was reportedly in talks to buy a majority stake in Nido Home Finance, a PE control buyout in realty and home lending, after a period of caution.

Meanwhile, CarTrade’s $1.2-billion CarDekho acquisition talks failed, a story which may be just as instructive as closed transactions for the M&A community. The problem? A valuation mismatch between public and private markets.

And in another eye-catching moment: ‘We did not sign up for chaos’ is the headline quote as the Omnicom–IPG merger sparked client jitters.

I hope you enjoy this week’s roundup – please connect on LinkedIn to discuss how Ideals VDR can help with your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

Is India’s IPO class too cool for school?

This year the government changed MSP (minimum public shareholding) rules, covered in a previous Teaser, which loosened capital concentration but like much else, markets and clever accountancy found a new workaround. Here’s how.

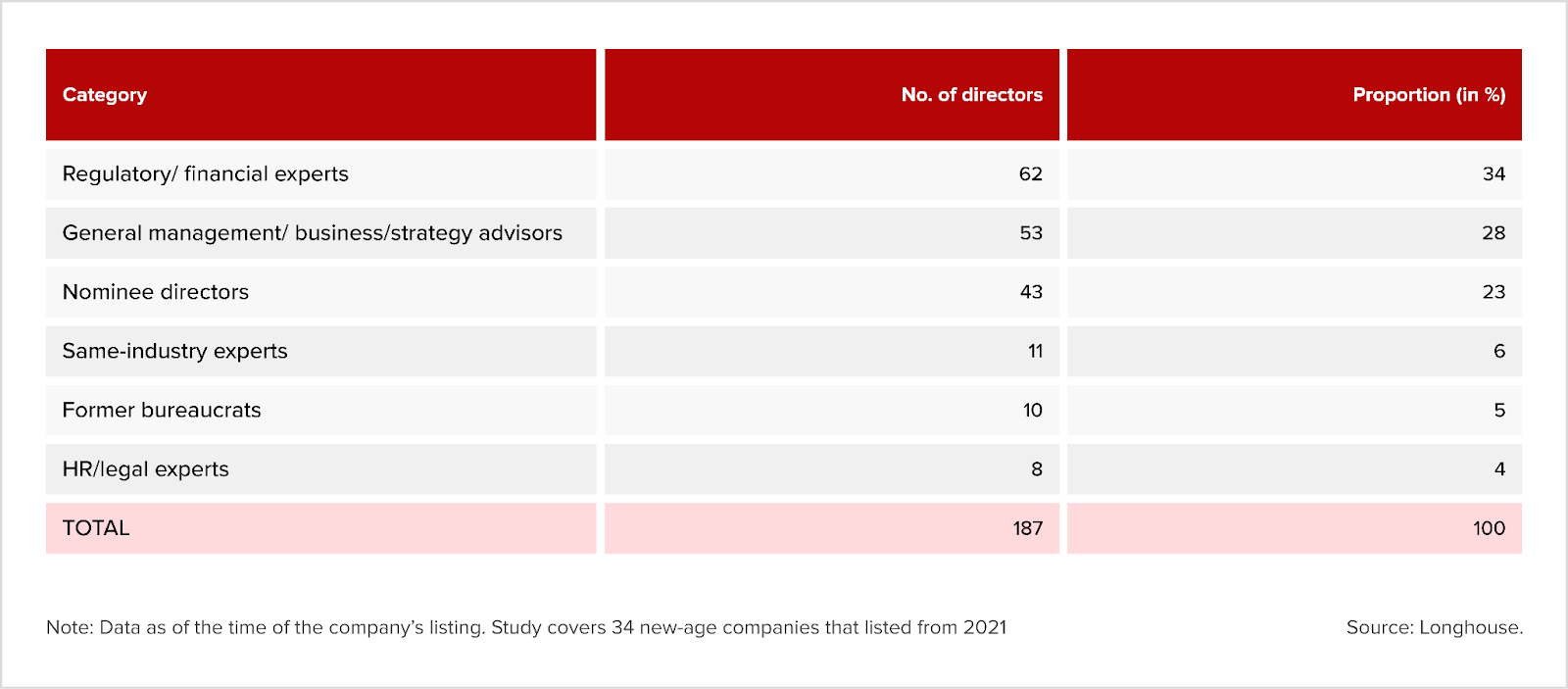

A recent Economic Times piece cited a Longhouse study of 34 venture-backed firms that have gone public since 2021 showed that nearly 90% of independent directors (ID) were appointed by them within six months of filing IPO papers.

The new kids seem too cool for succession planning, and have been caught making last-minute board makeovers intended to meet regulatory thresholds and polish governance optics just before listing. This is worrying.

The profile of directors says a lot. Just over a third (34%) were regulatory or financial specialists; 28% were general business and strategy advisors; and 23% were nominee directors representing investors. Only 6% were sector specialists drawn from the company’s own industry.

The focus is on gaining governance credibility rather than operational guidance or long-term mentorship.

These do not present as organic or evolutionary strategy/domain-wise. It is like teenagers scrambling to tidy up their bedrooms before authority figures show up (read: compliance-driven risk controls inserted at the eleventh hour).

Hired hands

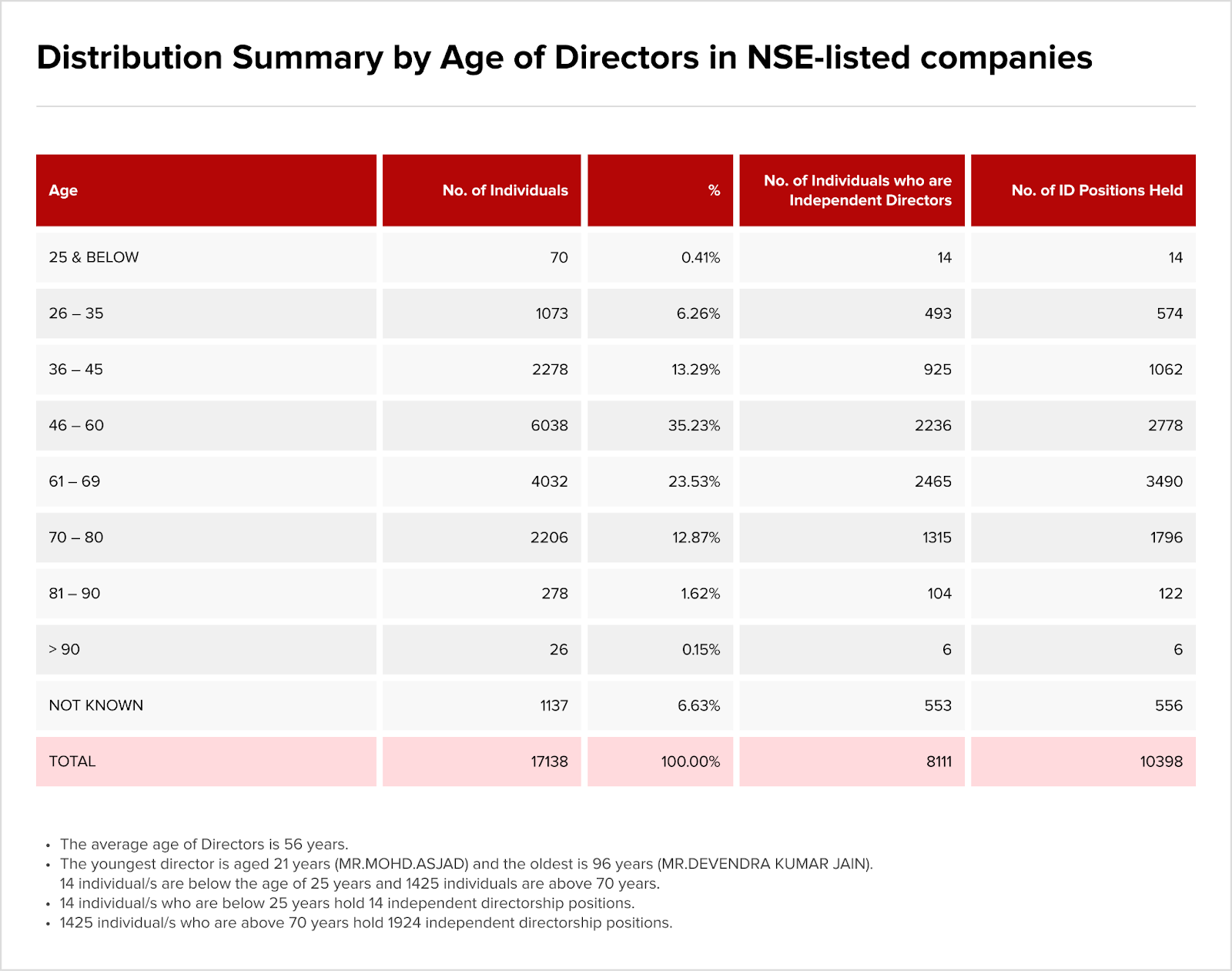

National Stock Exchange (NSE) data on director age provides the broader backdrop. The average director age is 56, with almost half (49%) clustered between 46 and 69 years old, and more than 1,400 individuals above 70 still occupying independent seats.

What’s missing? Younger, execution-oriented independent directors.

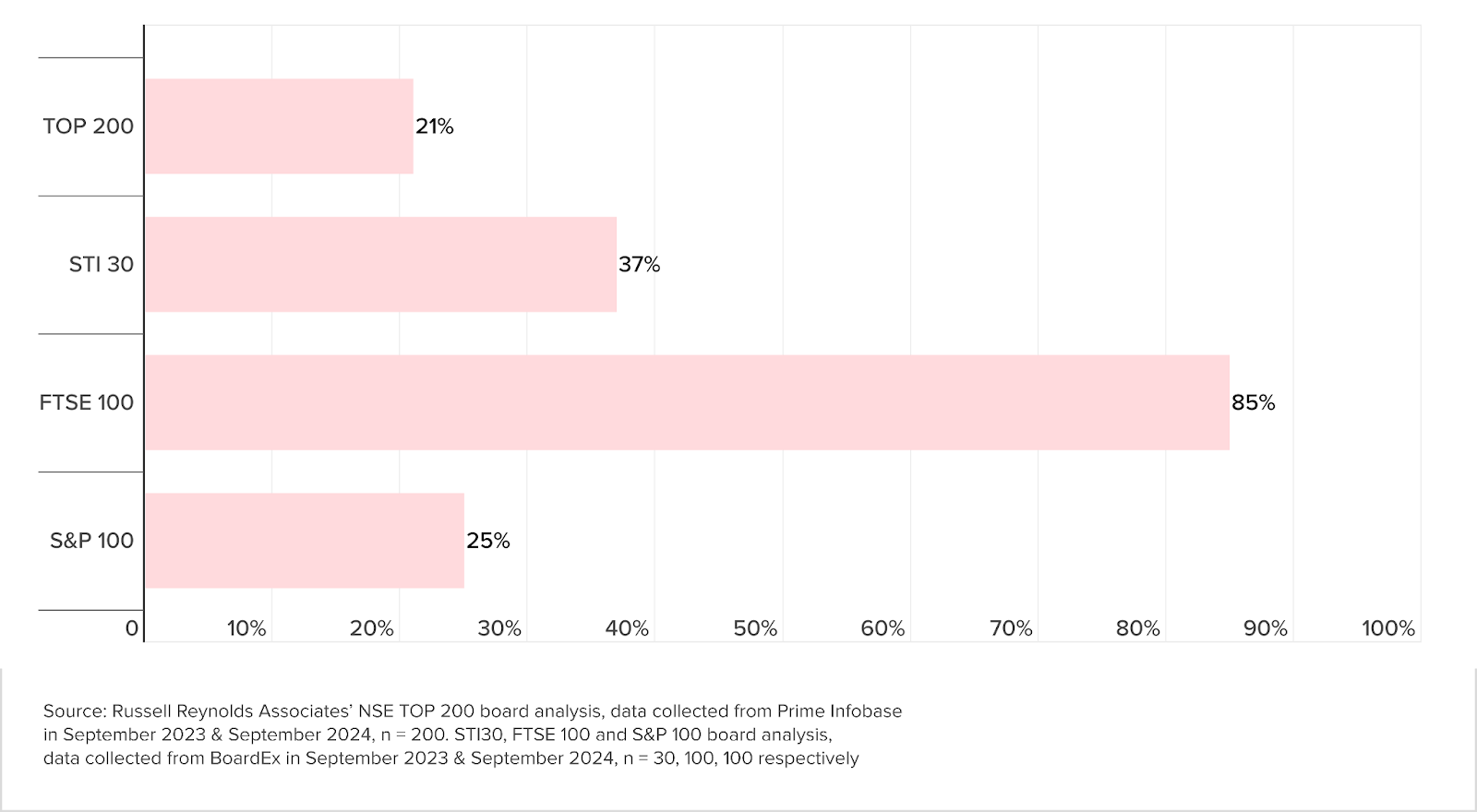

US consultancy, Russell Reynolds’ study Deciphering the Indian Boardroom 2024 takes a different compass bearing.

It finds that an average of 9.8 directors occupy boards across the Top 200 NSE-listed companies, with most directors holding around 2.1 seats across different boards, pointing to a tightly recycled pool of talent rather than renewal.

Leadership structure tells the deeper story. Only 21% of major Indian corporates have independent board chairs, compared with 85% in the UK’s FTSE 100 and about 25% in the S&P 100. Control still remains disproportionately concentrated with founders and promoter families.

All this goes some way to explain the tenure mismatch as well. Parachuted leaders are entering boards late, largely for IPO legitimacy, with little commitment toward building pre-listing mentorship relationships with founders. Their mandates skew toward monitoring, audit sign-off, and risk mitigation, not long-term strategy or CEO development.

Women have little meaningful participation in this onward journey, as boards remain male-dominated, with only 21% of female directors, the RR data reveals.

It’s control, not economics, stupid

Then there’s the chief executive churn adding to the instability. According to ET, 141 CEOs left listed Indian companies in FY25, the highest figure in recent years.

Meanwhile, Deloitte’s 2025 Executive Performance & Rewards Survey, cited by Mint, finds that the pay divide widened sharply between CEOs, C-suite leadership, and independent directors.

IDs at Nifty50 firms are paid nearly double of what they were five years ago, reaching close to ₹1 crore ($120,000) annually in many cases, but without a proportional increase in firms’ governance authority.

Besides, independent chairs remain rare, promoters retain veto power, and founders continue to dominate board agendas, whether in family-run enterprises or founder-led tech companies, it is the same control architecture playing out.

Reasons for leaving

Russell Reynolds’ list of the commonly stated reasons for board and executive resignations seems euphemistic:

- Pre-occupation

- Personal reasons

- Health or old age (not retirement — directors routinely serve well beyond 60–65 in India)

- Moves to join other boards

- Structural or regulatory transitions, including resolution plans or management changes

Off the record, however, the friction points are better understood as limited autonomy, promoter resistance to modern governance norms, slow reform cycles, and insufficient board mentorship.

While Sebi has encouragingly chipped away at family-run businesses to lower their guard, the newest tech cohort is hardly at its best behaviour. IPO-led director inflation often masks promoter/founder dominance, a scramble to tidy up governance just in time for listing.

Boards may look global on paper, but that illusion cannot stretch far and managements must change if they know what’s best for them, or seasoned India investors will move on, and regulators move in to make more rules, increasing compliance costs and bringing more headaches.

The rumour mill

- Carlyle said to eye stake in Indian housing finance firm

- No plans for public sector banks merger government issues clarification; here’s what MoS detailed on FDIs, IDBI offloading and more

- India warms to secondaries amid rising demand for DPI

- Multibagger penny stock surges 4000% in five years, Rs 1 lakh grows to Rs 41 lakh

- Kissht DRHP: Rs 1,000 crore fresh issue, Vertex and other investors to sell stake

- Meesho faces investor protest over anchor allotment to SBI Funds

- VC Lightspeed joins race for stake in cloud infra startup Neysa

- ETtech Exclusive: Public markets won’t bankroll qcomm cash burn for long: Blinkit CEO Albinder Dhindsa

- Mitsui, Sumitomo Lead Japan’s Push Into India’s $1 Trillion Realty Future

- Why are foreigners betting big on Indian real estate?

- Why global funds are rushing to build dedicated India strategies

- Indian e-commerce firm Meesho bets on AI, new business lines in growth push

- India’s Adani seeks up to $5 billion investment in Google data center to join AI boom

- NCLT approves ₹145.26 crore resolution plan for Indo Global Soft

- The Timing Factor – SEBI Gives Adani A Clean Chit

- Softbank all in on being OpenAI’s top supporter, won’t back rivals: CFO

- Jefferies initiates Kinetik Holdings stock with Buy rating on M&A outlook

- Barrick Considering Spinning Off North American Gold Assets

- Carlyle group in talks to buy majority stake in Nido Home Finance

- ‘We did not sign up for chaos’: Omnicom–IPG merger sparks client jitters

- The Omnicom-IPG merger – Why the acquired company always pays the higher price

- India aims to accelerate space technology investment as China races ahead

- Venture capital targets India space tech; US banks lend more to private equity

- PSU bank mergers: Do bigger banks mean happier employees?

- Reliance joint venture to build $11 billion AI data center in India

- Sridhar Vembu shares bizarre startup acquisition pitch leaking rival offer. AI takes the blame later

- What’s the reason behind Bandhan Bank selling over ₹6,900 crore in stressed assets

- Temasek’s Seviora to absorb Pavilion Capital, boosting AUM to $72bn

- CCI Clears Toyota Group Restructuring, Investment Arm To Acquire Toyota Industries

- CCI Clears ICICI AMC, Toyota, And Jindal Deal Approvals

- Juniper Hotels bids for distressed JW Marriott property in Bengaluru via insolvency process

- Canara Bank to raise ₹3,500 crore through ATI Bonds to strengthen its capital base

- CarTrade’s $1.2-billion CarDekho acquisition talks come unstuck

Fundraising

- SalarySe secures $11.3 million from Flourish Ventures, SIG Ventures

- HDFC Capital comes in as LP to Brigade and Gruha’s proptech fund

- Fireside Ventures closes fourth fund at Rs 2,265 crore, its largest so far

- Learning platform Yoodli raises $40 million in round led by WestBridge Capital

- Swiggy’s board approves Rs 10,000-crore fundraise via QIP

- LPs drill down into GPs’ long term resilience

- LPs’ are expanding into more diverse secondaries strategies

- India Digest: Mixx Technologies, Cloudextel raise funding

- Sheela Foam leads $13.9m funding in Furlenco and other India deals

- Info Edge invests $7.8M in subsidiary Startup Investments Holding Limited

- IFC extends $58.5m debt funding to Candi Solar

- India: Venture Soul Partners coses maiden debt fund at $33.5m

M&A news

- Omnicom restructures India leadership team after merger with IPG

- Why private credit is becoming corporate India’s new favourite

- Download Buyouts’ 2025 GP stakes report

- With $2.2 billion fund, ChrysCap has appetite for riskier bets

- India’s services growth accelerates in November but export engine sputters, PMI shows

- India’s M&A activity surges 37% to US$26 billion in Q3 2025, defying global volatility: EY India M&A Report

- Omnicom-IPG deal closed: Timelines, key agencies and what’s next?

- 3one4 Capital charts strategy for 5th fund as ecosystem evolves: Pranav Pai i’view

- Malaysian PE Creador enters India’s QSR sector with $73m investment in Sapphire Foods

Job moves

- LIC appoints Ramakrishnan Chander as Managing Director

- State Bank of India Appoints Anindya Sunder Paul as Deputy Managing Director (Finance)

- R Chander Assumes Charge As LIC Managing Director

- Jitendra Gohil Takes Charge as CIO at Bajaj Alternate Investment Management

- Tamasek appoints ex-DBS CEO Piyush Gupta as India Chairman

- Pramod Kumar Dwibedi appointed Executive Director of Bank of India

- Ramprasad Sridharan appointed as new PUMA India MD

IPOs

- Meesho IPO: Offer Size, Financial Report Card, Risk Factors & Other Takeaways

- Groww, Pine Labs IPOs spark fresh deal flow for fintech startups

- Meesho raises Rs 2,439 crore from anchor investors ahead of IPO

- Meesho IPO: There’s no slowdown, India among the least penetrated ecommerce markets globally: CEO Vidit Aatrey

- Wakefit IPO values company at Rs 6,373 crore, to unlock major gains for founders, investors

- Zepto may file draft IPO papers this month; eyes $450-500 million fundraise from public markets

- New-age firms rejig boards fast to plug IPO gaps: Longhouse

- Boardrooms’ pre-IPO makeover; The mule account MO

- Meesho’s $604m India IPO fully subscribed on retail investor demand

- Indian plane parts supplier Aequs’ IPO fully subscribed

- Indian data centre operator Sify infinit bets on AI, albeit with caution

- NephroPlus set to launch IPO open on Dec 10; eyes Rs 353-cr via fresh issue

- General Atlantic-backed ASG hospital eyes $391 million India IPO

Compliance/regulatory update

- LP scrutiny on the rise for CFOs

- Slumps on importers’ panic buys; RBI dlr sales cap fall

- Parliamentary panel moots advance ruling mechanism in IBC framework to tackle litigations

- RBI may cut interest rate by 25 bps on Friday

- India manufacturing PMI registers slowest improvement in operating conditions since February, S&P data shows

- IBC resolution process: House panel raises concerns over ‘haircuts’, asset valuation; encourage global bidding

- RBI’s MPC starts three-day meet; key rate decision on Friday

- S&P upgrades rating for India’s insolvency regime as IBC lifts recoveries

- Raghuram Rajan, ex-RBI governor, warns of rising risks in global private credit market

- The regulator’s gambit: Why SEBI took a stand against a business dynasty

- ‘Everybody is waiting for RBI’: Piyush Goyal hints at room for rate cut as inflation hits series low

- Facilitating PE/VC exits in India: Finding a way out