Harsh Batra

Harsh Batra

Hello,

This week, NTPC and Mahagenco signed an agreement to acquire STPL (Sinnar Thermal Power Ltd) for a believed ₹38,000 crore, a marquee public-sector transaction of scale signalling confidence in large-ticket strategic acquisitions using state-owned firms’ balance sheets for infrastructure and energy M&A.

Meanwhile, a source-led exclusive revealed Bain might delay its part-acquisition of gold lender Manappuram Finance because of rules introduced by Sebi on private ownership/control of banking/NBFC assets.

Also, a Supreme Court tax ruling this week on merger share-swaps may affect deal structuring, valuation, and choice between cash vs. share consideration.

And finally, Prudential Financial is said to be thinking of selling its India asset manager, pointing to global financial firms reassessing their exposure to the subcontinent.

I hope you enjoy this week’s roundup – please connect on LinkedIn to discuss how Ideals VDR can help with your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

India in 2026 looks like the best house in a shaky neighbourhood

It feels fair to start with a cricket metaphor given how much of it is about these past and coming weeks: the Indian markets are having a good innings fought on decent fundamentals. But how will the country fare as geopolitics and economics become ever more challenging?

A solid innings, but with macro risks

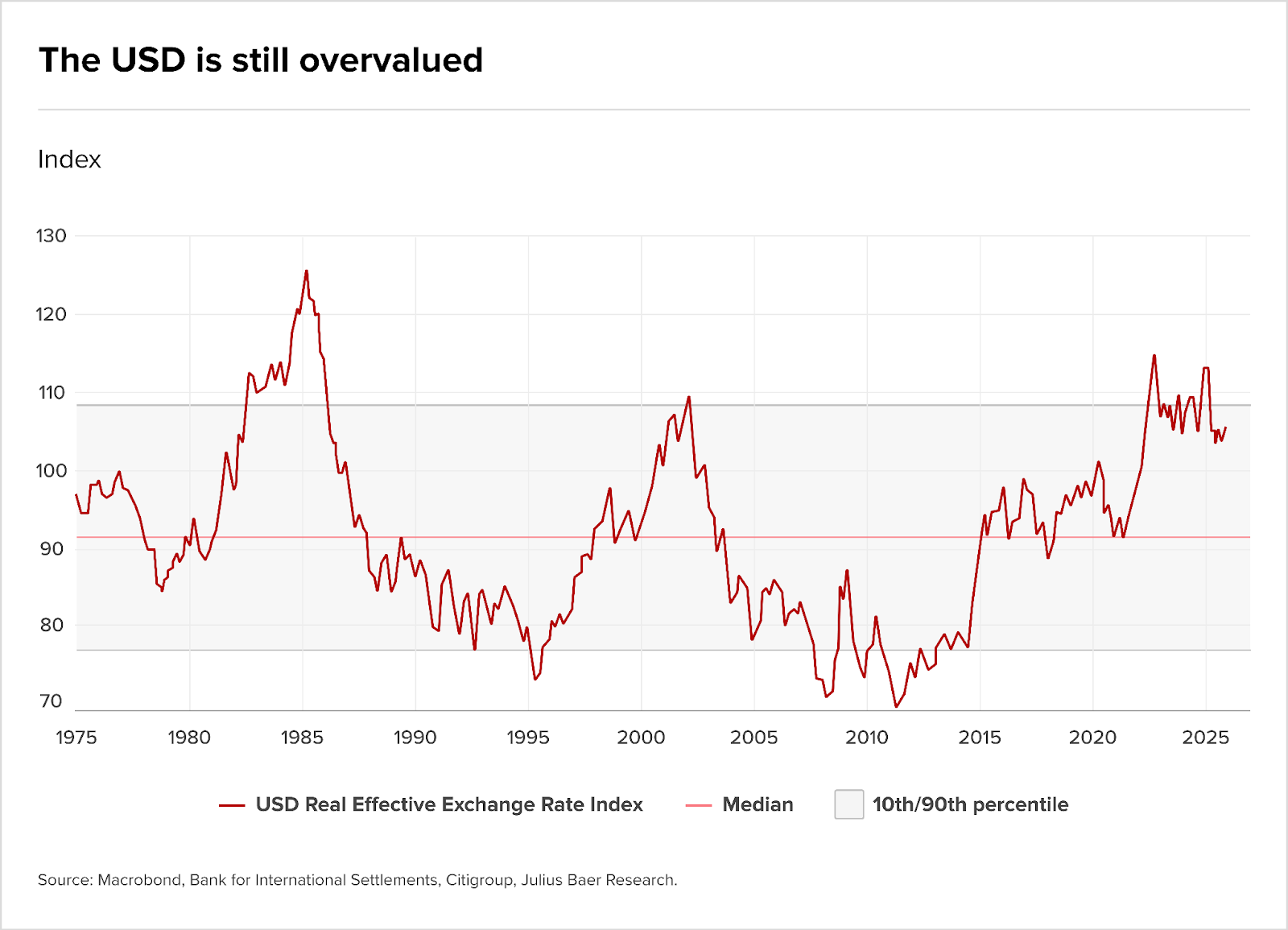

Let’s begin with the caveats in this macro picture: Starting with the greenback.

The world’s most favoured reserve currency (USD) remains overvalued versus its track record, says Julius Baer, and remains relatively strong. A strong dollar will reshape crossborder deals and the implications for India are clear: imports will be expensive; dollar debt will remain elevated; and margins in capex-intense businesses will be under pressure.

For dollar-based buyers (whether SWFs, US strategics, or PE), a stronger dollar implies greater purchasing power in local currency priced assets (including India) and therefore a tactical advantage when bidding for emerging market (EM) targets. But the flipside is that a persistently strong dollar can also weigh on EM earnings via weaker global demand and higher import costs, increasing currency risk for domestic sellers.

As a result, any cross-border deals must therefore scrutinise currency hedging, with sensitivity testing across export volumes and input price scenarios.

From expansion to consolidation: Exits and breakups

Against this backdrop, dealmaking is beginning to shift, and a gander at the week’s news suggests the dominant M&A signal in India is a consolidation plus unwind phase, marked by large strategic exits, and JV breakups – with more to come.

For instance: papers reported that Allianz completed its divestment from India’s Bajaj Finserv in a ₹21,390-crore ($4.6 billion) buyout; Prudential Financial is reportedly mulling a sale of its India asset manager; And chemicals firm SABIC is overhauling its portfolio.

Regulation no longer just background noise

Dealmakers will want to hedge against regulatory mood swings at the RBI, CCI and tax authorities, as these increasingly influence valuation, and even transaction viability.

Energy and renewables will see consolidation, with fewer buyouts, and more minority and structured asset-level deals backed by sovereign funds and infrastructure capital.

But consumption will slow, QSRs will consolidate; Fintechs will seek cost synergies, tech rationalisation, and IPO readiness over expansion.

Special situations will re-emerge if acquisition financing tightens. Stressed balance sheets and IBC-driven asset sales will create opportunities for PEs willing to underwrite complexity and long-winded resolutions.

BUT that’s it for the caveats

Happily, two reports from S&P Global and one by Julius Baer bear better tidings, and the graphs below aim to show it.

To begin with, Baer’s earnings per share (EPS) chart showed projected growth in EMs (and China) comfortably outpacing developed markets across 2025–27.

Baer suggested India will see acquisitions in profitable, especially export-oriented, manufacturing.

Financial services and larger consumer franchises which are (relatively) defensible will also remain attractive targets.

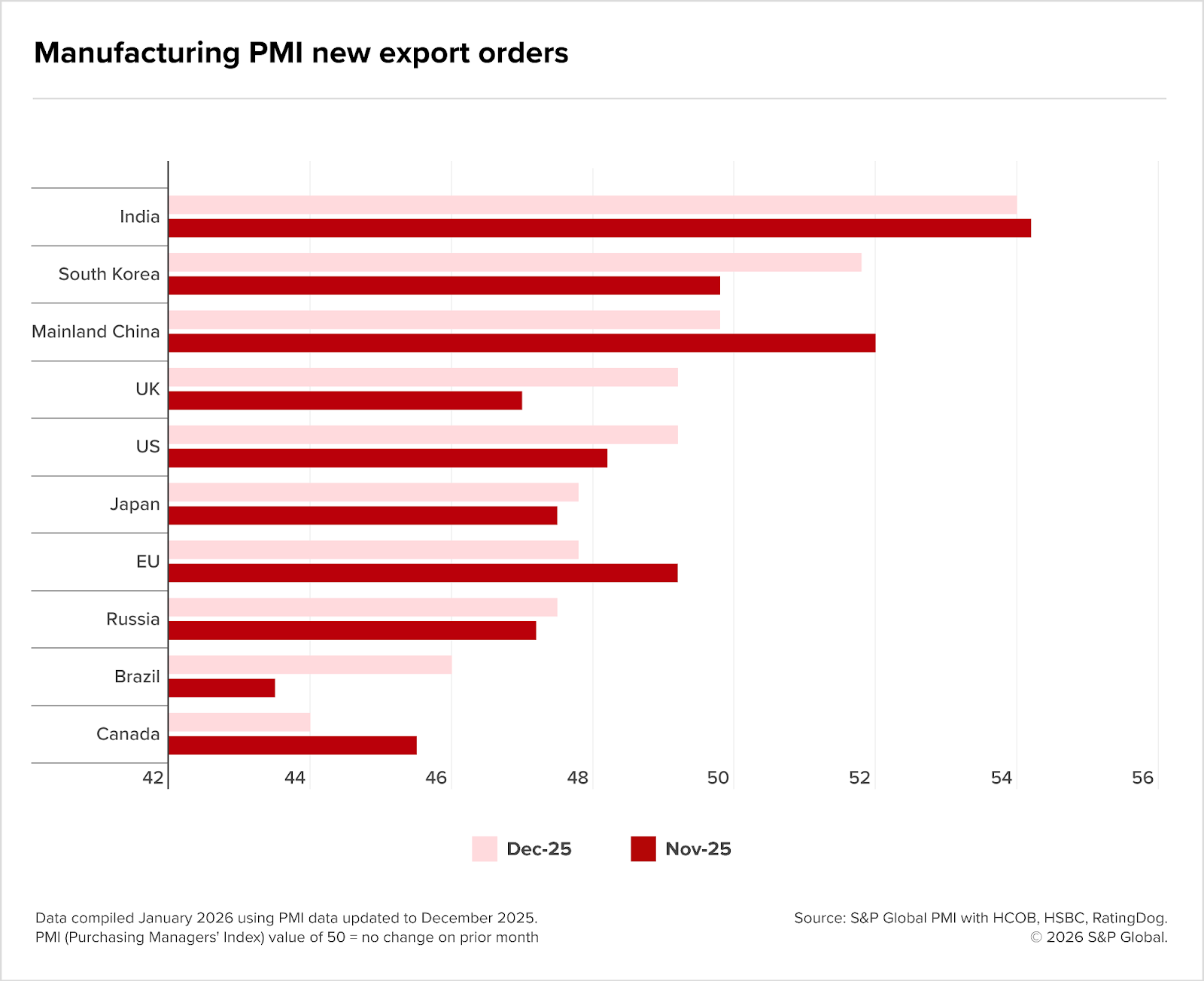

India’s export surprise in a shrinking global trade pie

An S&P Global analysis singled India out as one of the two large economies consistently recording growth in goods export orders at 2025’s end, even if overall growth moderated each consecutive month last year.

It seems likely India’s manufacturers are finding demand where many developed markets – and several EMs peers – are flailing, gaining share in a shrinking global exports pie.

This will strengthen M&A for India’s industrials, engineering, chemicals, and niche capital goods platforms that can scale exports.

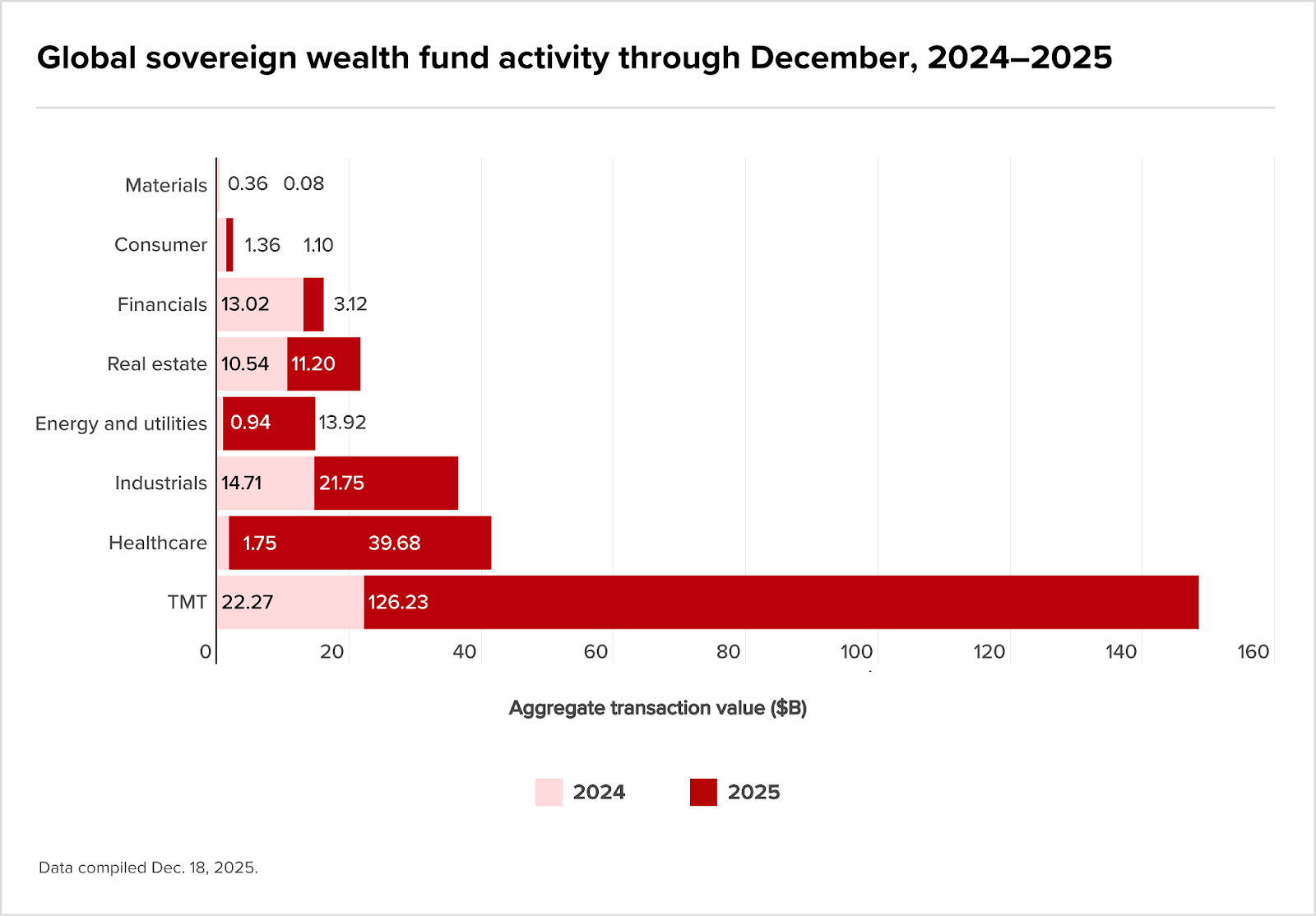

Serious capital is going long

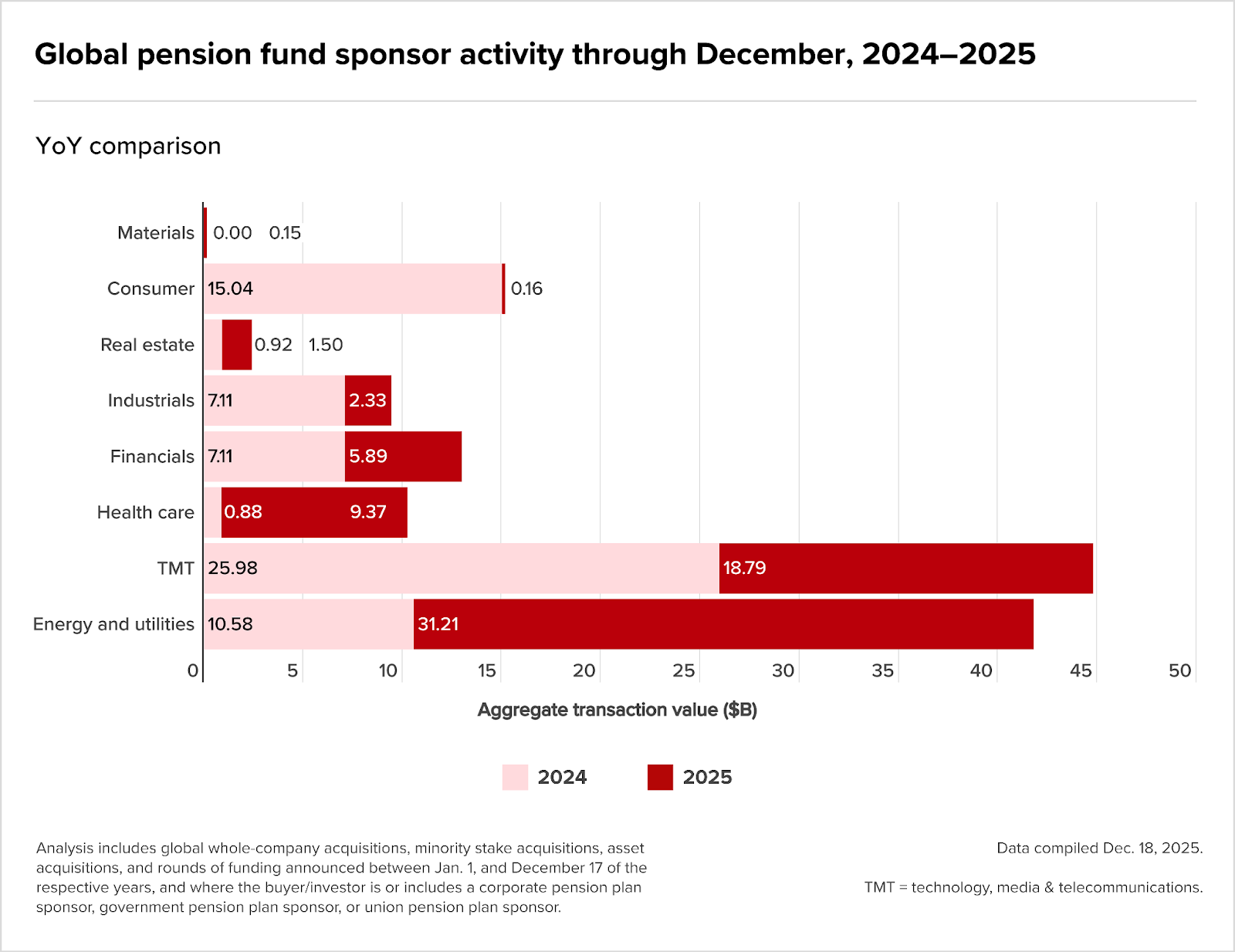

Next, an S&P Global note on sovereign wealth funds (SWFs, below) shows a near doubling in private market transaction value in 2025, with a clear thematic tilt toward TMT, large buyouts, and PE co-investment.

SWF interest may raise the floor on pricing for high-quality platforms, increase availability of long-dated capital for large platform deals, and make co-investment structures the default for very large transactions.

For India, S&P explicitly flags that newer allocators will ‘selectively engage in direct deals…particularly in India and Japan,’ picking out India’s attractiveness.

Another highlight of the report is that large global pension funds are pivoting to energy and utilities.

To conclude…

Taken together, the data suggest India enters 2026 not without risks but as a market where capital, consolidation and conviction seem in healthy alignment.

The rumour mill

- Acquisition financing by Indian banks to sanction risk, 2026 set to be a learning year for India Inc

- Blackrock seeks CCI clearance for investment in Aditya Birla Renewables

- Spandana Sphoorty evaluates merger of subsidiary Criss Financial

- THESE two public banks are set to merge, will become second largest after SBI; here’s what will happen to your money, chequebook, passbook

- Kotak Investment Banking Projects ₹6 Lakh Crore Equity Market Fundraise for CY26

- Mergers, money flow into India’s QSR industry as sales stall

- NTPC and Mahagenco Sign Agreement for STPL Acquisition Worth ₹38,000 Crores

- Lockers to demat: How gold ETFs are changing India’s ties with the yellow metal

- Org Chart: PayU India’s long game as fintech’s easy growth fades

- Offshore U.S. CPA Firms new reality: Talent crisis, attrition, skyrocketing salaries

- Prudential Financial Is Said to Mull India Asset Manager Sale

- Risks Remain Elevated for India Investors, Warns Former Adviser

- India Nifty Earnings May Fall Short of Expectations Yet Again

- Warburg Pincus to invest $106m in Lemon Tree’s hotel ownership arm Fleur

- CDR vows to eschew retail fund push

- Torrent Pharma eyes Rs 12,500-crore bond sale next week. Check details

- US PE firm Sirion Haveli Investments to buy majority stake in India-founded Sirion

- India’s Reliance open to buying Venezuelan crude if opportunity arises

- Razorpay Prepares for IPO, Plans to Raise Up to INR 4,500 Cr

- Trilegal represented Japan Post in securing an unconditional approval from the CCI for a USD ~932 million proposed investment in Logisteed Holdings

- Stocks Market Today: All You Need To Know Going Into Trade On Jan 12

- CCI Approves Prosus’ Stake Increase in Rapido Following Swiggy and TVS Exits

- Saks Poised for Bankruptcy Amid Restructuring Challenges

- SABIC accelerates portfolio overhaul with $950m divestment deals

- Devyani-Sapphire merger reshapes Taco Bell India tech and marketing roles

- Exclusive: Bain’s Manappuram deal delayed by Indian regulatory concerns, sources say

- Sidley Advises on Market-Defining Cross-Border India Matters in 2025

- IFC muls $25m investment in HDFC AMC’s structured credit fund

- Sovereign wealth fund private market deals soar, pension fund activity slows

- India regulator says Bank of America breached insider trading rules in 2024 deal

- IBC Route Unlocks Prime Indian Urban Land Amidst Scarcity

- Sical Logistics Lands ₹4,038 Crore SECL Coal Mining Contract

M&A news

- Bajaj Group completes 23% stake acquisition in insurance units from Allianz

- Cognizant Technology Solutions: Recent Acquisition And Proposed India Listing Draw Attention

- CII calls for value unlocking of PSUs through fast-tracking privatisation

- India has progressed on many fronts, it must avoid middle-income trap: PM’s eco advisory panel chief

- Download: PE fundraising in North America hits post pandemic low

- From mega M&A to aggressive expansion, 2025 was the year of Indian conglomerates. Will the momentum sustain in 2026?

- Data Vantage: Glance in focus and other updates

- Global trade declines at end of 2025

- Citi, JPMorgan Opt Out of $1.4 Billion SBI Funds IPO on Fees

- India: Regulatory expectations impacting banking and capital markets

- India Deal Review: Startup funding slips in Dec as deal activity slows

- NLC India board greenlights listing of renewables unit

- Demand for bunkers mixed at Indian ports in Dec

Job moves

- Nirvana Kumar Chaudhary appointed as chairman of Nabil Bank, former CEO Anil Keshari Shah

- AKI India Limited Restructures Board with New Independent Director Appointments

- Shreeyam National TMT Strengthens Board with Industry Veterans Atul Bhatt and Ashok Garg as Independent Directors

- NCLT approves Rs 420.86 crore resolution plan for Supertech ORB, offers relief to homebuyers

- Coller Capital Expands Asia Pacific Footprint with New Tokyo Office and Japan Private Wealth Team

- Elegant Floriculture & Agrotech Appoints Two Independent Directors to Strengthen Board

- Avenue Supermarts Leadership Transition Announced for 2026

- SBI Card Announces Postal Ballot for Appointment of Two Independent Directors

- People movement news: Girish Srikrishna Paranjpe appointed as chairperson of Mphasis

- Nippon Paint India Unveils Strategic Roadmap Under New Leadership

Fundraising

- India Digest: Betterinvest floats credit fund; Bluecopa raises $7.5m led by Analog

- Bessemer leads $4.6 funding in Aivar and other India deals worth $156m

- India Digest: Spector.ai bags funding; Amagi IPO opens next week

- Dharana Capital raises second growth fund with $250mn corpus to invest in Indian startups

- Inox Clean Energy raises Rs 3,100 crore through 6 pc equity sale

Compliance/regulatory update

- RBI To Conduct Auction Of State Government Securities Worth Rs 26,815 Crore On January 13

- Growth paradox: Why India’s 8% growth isn’t translating into higher incomes or investor confidence

- India’s inflation ticks up in December but remains well below RBI target

- India’s forex reserves drop 98b in sharp weekly decline

- Rupee’s spectacular fall why RBI isn’t targeting a price band but inflation the impossible trilemma explained

- India’s inflation stays low, leaves room for interest rate cut

- A massive tax shortfall and slower growth loom, but the Centre’s budget math still works

- RBI wants to cap banks’ dividend pay-out at 75% of net income

- SC ruling casts a tax shadow on merger share-swap deals

- India’s forex reserves fall by nearly 10 bln USD

- USD/INR bounces back as Indian importers pick RBI’s intervention-led decline

- RBI MPC 2026: No need to waste bullet when growth high, inflation low, says PwC on central banks’s rate cut

- India Budget 2026: Tax reforms to help India win the new industrial power game

- India’s inflation edges higher but stays below central bank target range

- Faster, demand-led approach needed for PSE privatisation: CII

- RBI’s new upper layer list could include NBFCs promoted by banks, strong promoters