Harsh Batra

Harsh Batra

Hello,

This week, Gujarat-based Torrent Pharma became India’s fifth largest drugmaker after acquiring JB Pharma. This high-impact deal may well reshape India’s pharma landscape in the medium term. It also reflects consolidation trends in the sector.

Meanwhile, there are rumours that India-driven PE and VC firms may cash in on a market rally to clock up $3bn via exits as soon as investor moods coincide with India-focused funds’ liquidity cycles.

And finally, our Market Trends story looks at India’s big time infra plans as Mazagon Dock looks to buy neighbouring Sri Lanka’s Colombo Shipyard for around $53m, a rare but significant cross-border purchase in the maritime sector pointing to the country’s growing regional footprint.

I hope you enjoy this week’s roundup, and please do connect with me on LinkedIn to find out how I can help with your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

Are India’s public sector assets finally in play?

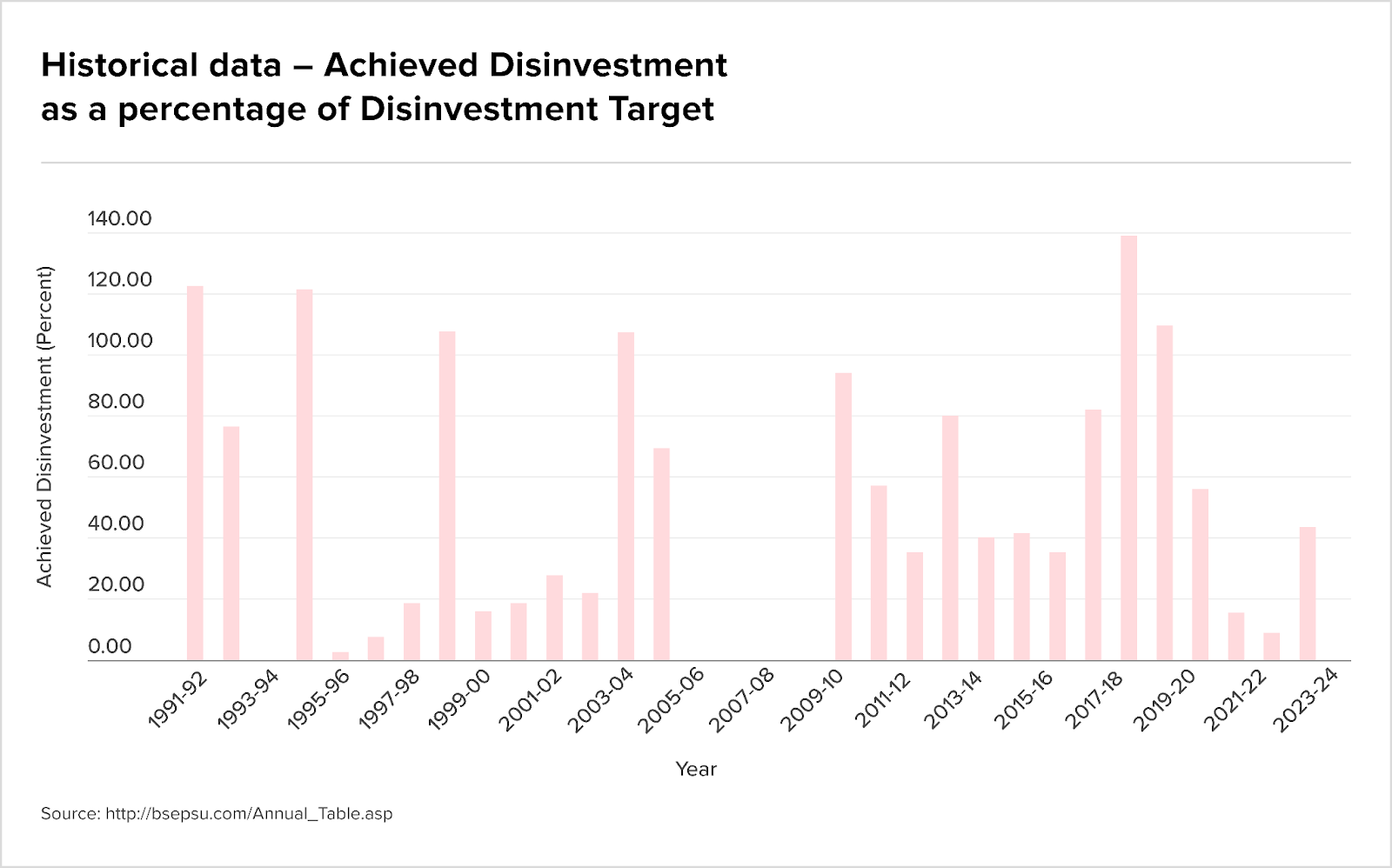

The Indian government is back on the disinvestment train after a few hiccoughs, but this time with assets that aren’t just loss-making ‘public sector units’ (PSUs) but also the country’s crown jewels, called ‘ratnas’ – all of differing size and heft.

These disinvestments – from LIC’s mega-IPO in 2022 to the ongoing sale of IDBI Bank, and asset monetisation in the national highways company, NHAI, and Indian Railways – are not only about offloading post-independence and post-Covid deadweight but reshaping the public sector to invite private sector participation where it matters.

Once stalled because of political pressures, they are now moving. In recent weeks, the government has accelerated key processes: the IDBI Bank sale is approaching the financial bidding stage; PSU banks have been asked to list subsidiaries; and stake sales in railway wifi firm RailTel and ticket booking app IRCTC have begun. Even the long-awaited sale of Concor (Container Corporation of India) has moved into its active stage.

And it’s creating fresh, lucrative M&A openings in infrastructure sectors such as transport, aviation, insurance, and railways (where land value is key).

Dealmakers may even look to greater private participation in PPP models across major cities, particularly in services like airport ground handling; maintenance, repair, and operations (MRO); and airspace operations.

So who’s buying?

Despite the renewed push, political sentiment around disinvestment is mixed, which might be reflected in the government’s repeated failure to meet its own targets. As a result, there is the pressure on them to lower valuation expectations.

Land usage and post-privatisation protections such as labour migration have been clouded by regulatory ambiguity, plus the array of small and large government departments involved are not the most conducive for ease of doing business. Authorities such as DIPAM and sectoral ministries have indicated that standard operating procedures for disinvestment will be updated to enable smoother transitions and make assets investor ready, including land titling, faster labour transition policies and simplified valuation forms.

Indeed, this outlook hasn’t stopped a cohort of smart Indian business houses such as the Tatas, Adani, L&T, Brookfield India, Cube Highways, Torrent, and the domestic sovereign fund NIIF, from actively bidding.

Global investors too, such as Canadian pension fund of funds, CPPIB, Aussie investment bank, Macquarie, and Emirati sovereign fund Mubadala are on the scene, especially for long term operating contracts. PE, too, is moving from financial bets to direct ownership, particularly in infrastructure.

What’s the hurry?

India’s post-Covid capex pressures have left no room for inefficiency. The finance ministry is operating with fiscal realism as there is the risk, some say, that a change in political leadership could stall or reverse the current disinvestment strategy. The window may not be open long, especially if public resistance gains traction.

This shift toward an asset-light state also aligns with G20-style infrastructure diplomacy which aims to crowd in private capital while the government focuses on governance and regulation.

While the LIC IPO may not have deepened institutional interest as much as expected, roads, railways, and logistics assets offer a different investor profile. Future stake sales in GIC, New India Assurance, and PSU banks (covered in a previous Teaser India) are likely, pending regulatory fixes.

More crossholding sales like those in UTI AMC and IFCI may also surface.

Deal and policy milestones

While true privatisation remains rare as bids often fall short of price expectations, several significant developments are underway:

- Sovereign wealth fund proposal will consolidate and reposition high value public sector units

- Indian Railways’ dedicated freight corridors that could reshape freight logistics economics.

- NHAI InvIT and TOT bundles: the FY25 pipeline was announced recently with Macquarie, NIIF, and Cube Highways already showing interest.

- IBC-driven infra M&A: Insolvency processes are opening up stressed infra assets, presenting new acquisition avenues

Looking at the big picture, it seems clear that meaningful monetisation, not fire sales, is on the agenda.

The rumour mill

- Bharat Forge completes Rs 746.46 cr acquisition of AAM India manufacturing

- Waaree Energies gets board nod to acquire Kamath Transformers for Rs 293 crore

- Saraswat seeks RBI approval to acquire New India Cooperative Bank

- IEA throws weight behind India’s digital energy stack

- Indian family offices now go beyond investing for HNIs and are involved in legacy planning, capital preservation for the future: Umang Papneja, CEO, Julius Baer India

- Reliance-Owned Campa Cola Faces Backlash Over Alleged Religious Insensitivity

- Adani Properties successfully bids for two HDIL projects

- Another startup — Zyngo EV Mobility — faces insolvency proceedings

- SBI classifies RCom loan account as fraud; reports Anil Ambani to RBI

- Torrent Pharma to Acquire Controlling Stake in J. B. Chemicals & Pharmaceuticals from KKR

- Edelweiss fund may pull out of Indian solar JV with Engie-report

- Jefferies warns heavy equity supply may cap India market upside amid rebound

- Cloud kitchen operator Curefoods’ investors rush for exits ahead of IPO

- Delay in the Timetable for the Acquisition of a Majority Stake in Vinpai and the Filing of a Simplified Tender Offer for Vinpai Shares by Camlin Fine Science Limited

- Zydus Wellness eyes M&A-driven growth, targets food, skincare and global expansion

- Bharat Value Fund mulls investment in Amnex Infotechnologies

- FMO proposes $7.5m investment in Indian MSME-focussed lender, NeoGrowth

- FMO weighs $40m debt investment in Indian NBFC Protium Finance

- IFC proposes $50m investment in India’a Grihum Housing Finance

- India’s Apollo Hospitals to list digital health and pharmacy arm in 18-21 months

- Stayvista raises $4.6m; KKR plans fund-to-fund transfer of Lighthouse Learning

- India’s TVS Capital tragets higher stakes, larger cheques from Fund IV

- Hindalco acquisition: Rs 1,074 cr deal! KM Birla firm to acquire THIS company

- Jaiprakash Associates Insolvency: Vedanta, Adani among others submit resolution plans for acquisition

- NMDC Steel disinvestment unlikely this fiscal, say govt sources | EXCLUSIVE

- IDBI Bank to go private: Govt, LIC likely to invite financial bids by Sep to offload 60.72% stake

- Billionaires Mukesh Ambani, Gautam Adani In Fuel Retailing Partnership Across India

- Upcoming IPO: Cloud Kitchen Operator Curefoods Filed DRHP With SEBI For Rs 800 Crore Public Issue

- Ayala, UPC Renewables JV to sell stake in 1 GW projects in $600 mn deal

- Reliance Defence eyes India’s ₹20,000-cr defence MRO mkt with new JV

- SSP Group Prices Indian Travel Food Services Joint-Venture IPO at Up to $1.7 Billion

- Triumph Composites, Quartz Fiber seek merger approval for Owens-Corning India

- Leapfrog considers alternative ways to exit following 3.3x sale

- India’s Dorf-Ketal in talks to raise $500 million private credit for European acquisition, sources say

- Proxy advisors urge shareholders to block Zee promoters’ Rs 2,237 cr stake hike

M&A news

- Cybersecurity Challenges in Mergers & Acquisitions: How Virtual Data Rooms Safeguard Confidential Transactions

- Japan’s SMBC seeks CCI nod to acquire 20 pc stake in Yes Bank

- Time to polish our public sector ratnas: Creating an Indian sovereign wealth fund to recast jewels

- Why are Indian corporates flocking to capital markets for funding?

- ImpactAlpha LP/GP: Can military technology be an impact investment?

- IPO-Bound Curefoods Faces Criminal Cases, Child Labour Allegations

- Rs 44-crore assets of Rajat Wires to be auctioned on July 3

- Rs 167-cr Nakoda assets go under the hammer; e-auction set for July 28

- CAM, TT&A guide historic Central Bank – Future Generali India JV

- India’s M&A deals hit Rs 3.53L cr in H1, driven by healthcare

- PE investments in Indian property slow to USD 1.73b amid global headwinds

- India’s Banks Will Lend. Will Tycoons Borrow?

- Indian Hotels Co announces divestments of Leanluxe Hospitality to Tata Sons

- FM says economic reforms to continue, refers to India’s ‘Goldilocks situation’: Report

- India’s Mazagon dock to buy controlling stake in Colombo Shipyard for up to $53m

- Interview: TR Capital prioritises asset quality, market nuances in India investment strategy

- TR Capital buys stakes in India’s MoEngage,Shadowfax, Whatfix from Eight Roads

- Taiwan-India JV powers breakthrough as MiPhi launches India’s first enterprise-grade SSDs

- Essar Ports at Logistics Outlook’s Multimodal Confluence 2025: Advocating Smarter, Integrated Logistics for India’s Future

- Manappuram Finance acquisition: Bain Capital gets CCI nod! Investment firm to acquire 18% stake

- Lupin spins off consumer healthcare business

- Sitharaman proposes 7-point strategy to mobilise private capital at UN meet in Spain

- Prestige Group inks JV with Arihant Group for ₹1,600 crore residential project in Chennai

- The Great VC Shakeout: Lessons for India from the U.S. Venture Landscape

- Central Bank of India forms joint venture tie-up with Generali

- India becoming a core pillar of our growth strategy Goldman Sachs Kim Thu Posnett

- Morgan Stanley’s Chief Asia Equity Strategist Jonathan Garner says Indian equities are most preferred in Asia

- IPOs Deliver the Best Exits in India, M&As Don’t Pay as Well: Info Edge’s Kitty Agarwal

- Meet the biggest investors in PE – the global 150

- Hamilton Lane Launches First Asia-Focused Private Markets Evergreen Offering to Enable Access to Targeted Opportunities Across the Region

- Finance Ministry asks public sector banks to monetise investments in subsidiaries via listing on bourses

- PEVC firms cash in on stock market rally to mint $3bn via exits within a month

Job moves

- Amitabh Kant Joins Fairfax as Senior Adviser After G20 Sherpa Role

- AU Small Finance Bank appoints two independent directors, senior executives

- Anant Ambani to get Rs 10-20 cr salary, profit commission as Executive Director of Reliance

- ITC CMD Sanjiv Puri draws ₹25.66 crore salary in FY25, slightly higher than last year

- Barry Litwin appointed as TestEquity CEO effective July 14

- NCLT appoints new liquidator for Uniply Industries amidst suspension of previous one

- ANM Global grows M&A practice with Mumbai partner hire

- Delhi paychecks still tiny compared to global cities like Geneva, Zurich, Deutsche Bank report show

- People Digest: IQ-EQ names senior leaers in SG, JPN; Rahul Agarwal joins Health

- Setu co-founder Sahil Kini appointed as CEO of Reserve Bank Innovation Hub

- From Wipro to Infosys, India’s IT giants see massive pay gap between CEOs and employees

IPOs

- PhysicsWallah files draft IPO papers with Sebi via confidential route

- Boat’s parent Imagine Marketing files for IPO; eyes valuation of over $1.5 billion

- Early Nykaa investor to offload $150-million stake via block deal

- Groww files draft papers for IPO, eyes $700 million to $1 billion listing

- Meesho gets shareholder nod to raise Rs 4,250 crore via IPO

- Pine Labs files for IPO with Rs 2,600 crore fresh issue; Peak XV, PayPal to pare stakes

- Startups aim to raise over Rs 18,000 crore via IPOs in major D-Street push

- Urban Company files DRHP for Rs 1,900-crore IPO

- Digital lending startups put off IPO plans amid muted growth

- Wakefit files DRHP for IPO; to raise Rs 468 crore via fresh issue

- Credila Financial Services files for $584m India IPO

- HDB Financials IPO gets $19b in bids as institutiona; buyers pile in

- Indian firms set to raise $2.4bn via IPOs this month on renewed confidence

- Walmart’s Phonepe loks to ris $1.5bn from India IPO

- Hero Motors refiles IPO papers with Sebi, ups issue size to ₹1,200 cr

Fundraising

- India’s Amicus Capital closes second PE fund at $214m

- Infra.Market raises another $50m from MARS; extends existing $100m facility by 5 years

- IORA raises India’s first carbon credit-backed loan from Caspian Debt

- Udaan raises funds from Lightspeed and others

- Indian telecom startup Wiom raises $40mb in Bertelsmann, Accel-led round

- Natixis Unit AEW’s $500 mn infra debt fund with India mandate taps key LP

Compliance/regulatory update

- SEBI approves Jio Blackrock JV for brokerage services in India

- Sitharaman presents India’s reform-led investment model

- IBC 2.0: India Greenlights Game-Changing Group Insolvency Framework

- RBI Governor Sanjay Malhotra to appear before House panel on July 10

- India Posts Current Account Surplus Of $13.5 Billion In Q4FY25: RBI Data