Daniel Black

Daniel Black

Hello,

Uncertainty seems to be the key theme of recent weeks. In response, UK interest rates were held at 4.5% on Thursday, with the Bank of England saying it was waiting to see the impact of US tariffs.

It’s making life difficult for dealmakers, with both M&A and IPOs on hold while people wait for something nearing clarity on economic policy and tariffs. One piece of good news though – Chancellor Rachel Reeves plans to restrict the CMA’s merger investigations as part of a bid to boost UK corporate confidence and ease regulations.

Also making the headlines this week:

- Apollo is to buy energy group OEG for $1bn

- Carlyle’s $945m Energean deal is facing collapse

- AstraZeneca will pay up to $1bn for cell therapy firm EsoBiotec

Thanks for reading, and do connect with me on LinkedIn.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Rachel Reeves to restrict UK competition watchdog’s merger investigations

- UK stocks kick off week higher as commodity-linked shares advance

- Gilt yields tick up after BoE holds rates and flags uncertainty

- Reeves is to announce the rebuilding of £9.9bn fiscal buffer

- UK Foreign Secretary David Lammy emphasizes the need for British diplomacy to foster business ties and economic growth, announcing new measures, such as Geopolitical Impact Unit

- Budget drives uptick in the UK PE deals, but outlook remains uncertain

- M&G blames ‘challenging market conditions’ for its £1.9bn net outflows in 2024, although its AUM rose to £345.9bn

- NatWest CEO Paul Thwaite says there is a ‘very high bar’ for potential M&A opportunities

- Britain is no longer largest investor in NatWest after fresh share sale

- Why the London Stock Exchange must go 24/5

- Warship maker Babcock is to join FTSE 100 after defense rally

- Thames Water aims to agree takeover by end of June as it mulls approaches from potential investors, including Castle Water, Covalis and KKR

- HSBC is in advanced talks to sell its German fund administration arm, Inka, with £308.3m in assets, to BlackFin

- UK Takeover Panel extends deadline for KKR-Stonepeak Assura bid

- Carlyle’s £728.3m Energean deal is at risk of collapsing amid regulatory hurdles, particularly in Italy and Egypt

- Apollo is to buy UK energy services group OEG at a valuation of more than $1bn

- BP seeks buyer for half of solar developer Lightsource bp

- Liberty Global approaches Vodafone about buying out Dutch JV stake

- London City Office is set to sell to SVP at 62% discount to offer price

- CityFibre targets 1mn customers as it seeks crucial £1.5bn financing

- Keysight acquisition of Spirent passes UK regulatory hurdle

- Partners Group agrees EUR 1bn sale of Greenlink Interconnector

- Miami International Holdings is to buy Guernsey stock exchange for £70m

- Indian billionaire and Bharti Airtel founder Sunil Bharti Mittal is reportedly exploring the possibility of increasing his 24.5% stake in BT

- Shuka Minerals’ planned buy of Leopard Exploration is hit by delay

- Bakkavor rejects a takeover bid by Greencore

- AstraZeneca is to pay up to $1bn for cell therapy firm, EsoBiotec

- ITV talks to merge with All3Media make progress

- Quinbrook closes £239m debt deal for Cleve Hill project in UK

- Maven Capital Partners invests in Digital Rewards Group

- Mubadala wraps up exit from UK smart metering firm Calisen

- Harmony Energy Income Trust “minded to accept” possible Foresight bid

- Battery firm Harmony Energy Income Trust gets £191m takeover offer

- Unilever CEO plans to sell underperforming food brands

- Dar Global invests £300.6m in Saudi Arabian real estate

- Harvest Minerals shares plunge as it considers selling divisions

- UK CMA agrees Capita One disposal worth £200m

- Crimson Tide shareholders vote down £6.5m merger with Checkit

- Afentra is in talks to buy Angola oil assets from Etu Energias

- Crispin Odey banned from City and handed £1.8m fine by FCA

Salaries and bonuses

- UK pay rises fall back in line with inflation for the first time since October 2023

- Klarna’s CEO got an 862% pay rise ahead of its IPO

- UBS bonuses were the highest for four years – for MDs

- Deutsche Bank’s bonus pool rose by 32%, leading to salaries of €6m salary for some top earners

Job moves

- Barclays hires BofA veteran to help lead healthcare bankers

- Hargreaves Lansdown CFO is set to depart

- Alter Domus appoints Mark Wiseman, former Head of Active Equities and Chairman of BlackRock’s Alternatives Business, as Chairman

- PayFuture names Praful Morar as new deputy CEO

- Hedge fund Schonfeld hires FX quant head in London from Millennium

- Artemis names ex-Man GLG boss Johnston as next CEO

- CVC hires ex-KKR dealmaker

- Citi’s London energy & power team keeps leaking people. JPMorgan may hire them

- Hedge fund Citadel hired a great wit, John Szatmary, from Google

- Tikehau Capital names Emmanuel Laillier as CIO of private equity

- Revolut is hiring founders for its fintech startup pod shop

Market trends

A gloomy economic outlook?

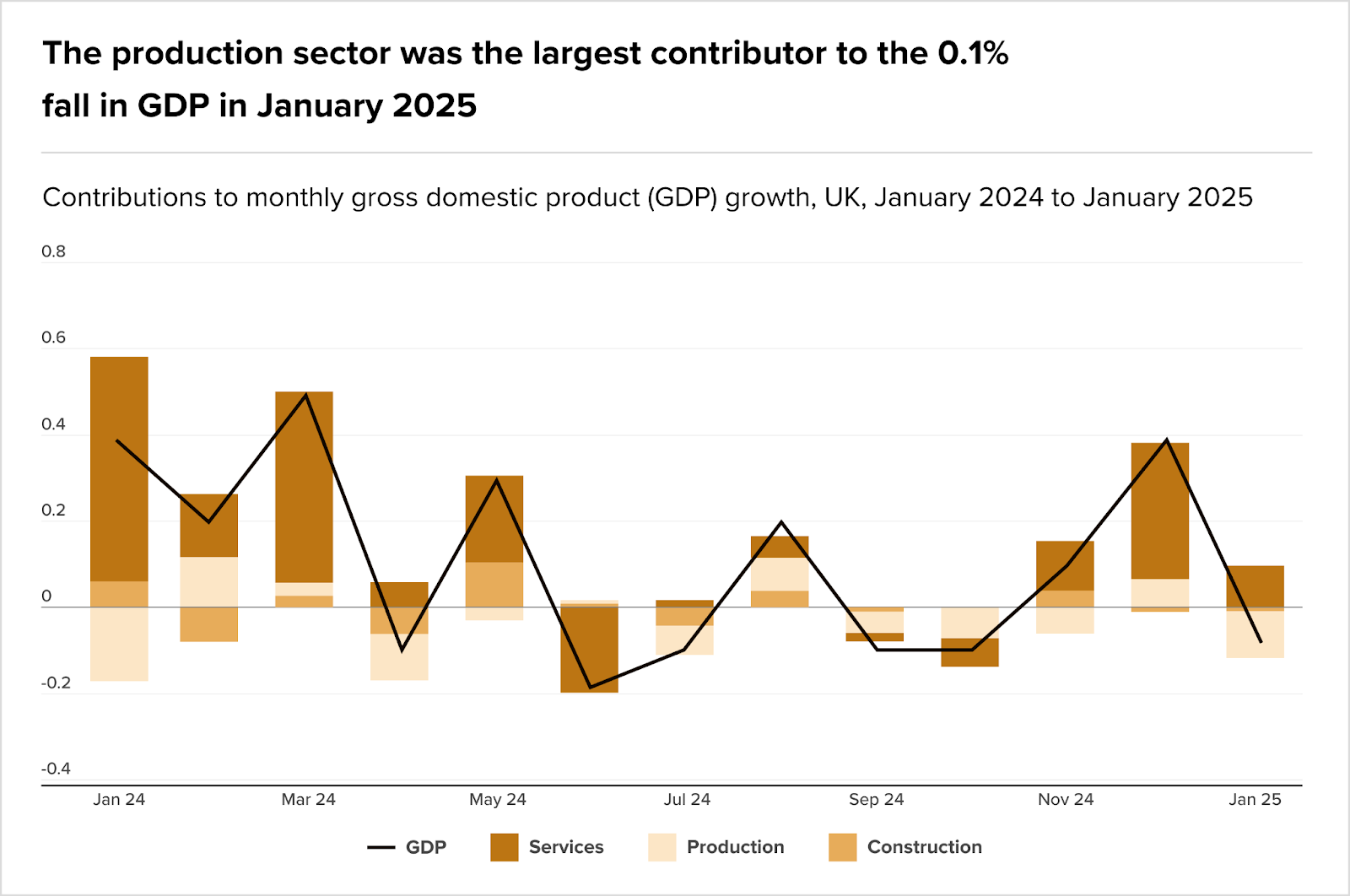

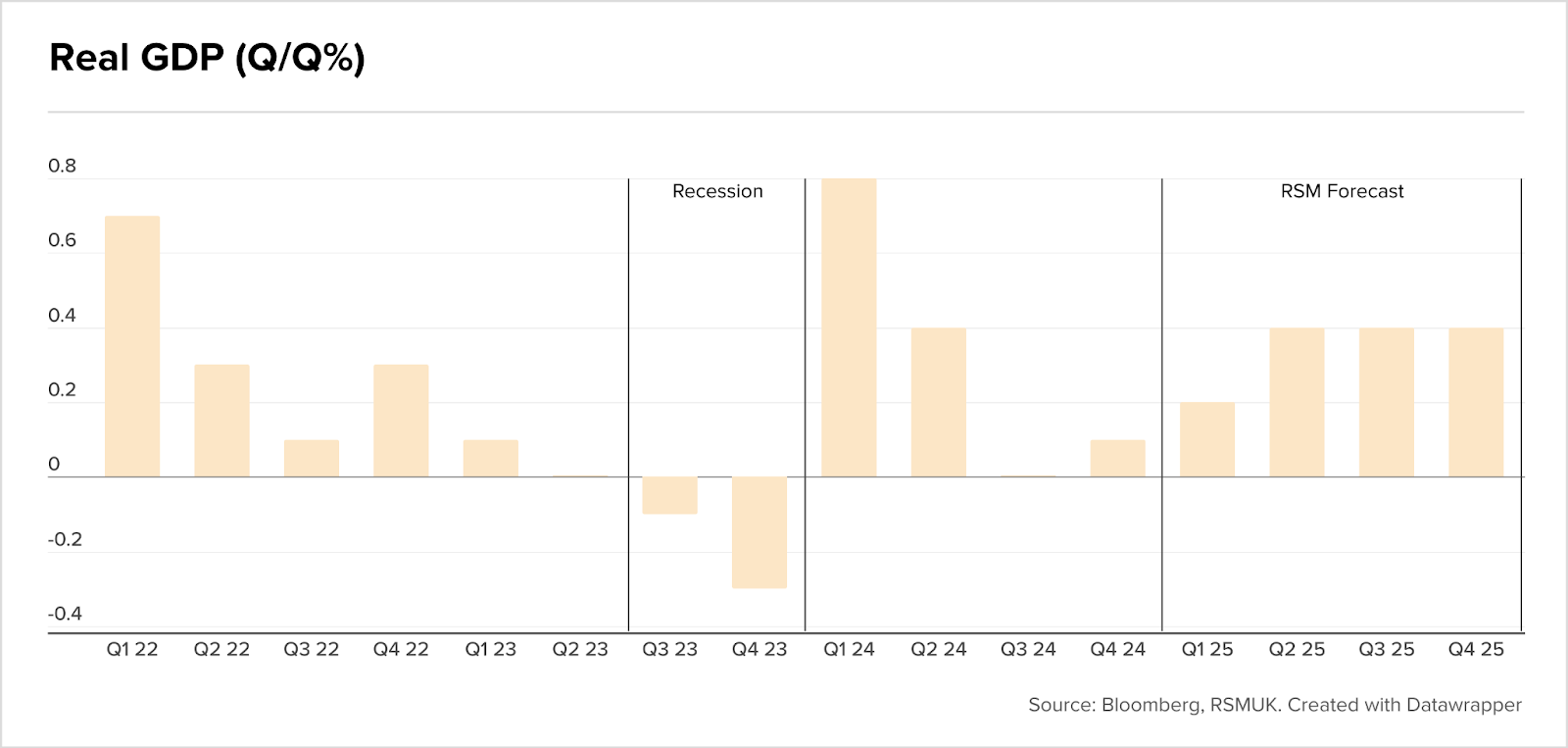

It’s not been the rebound many had hoped for. Analysis published this week by RSM UK shows UK economic growth is set to remain sluggish going further into mid 2025, with GDP expected to rise by a modest 1%, dampened by global trade uncertainty and weak external demand. Inflation is forecast to tick back up to nearly 4%, consequently raising concerns about a return to stagnation. While real household disposable incomes grew by 4% last year, consumer spending has barely moved.

Further adding to the concerns, UK production output took a hit in early 2025, with January’s figures showing 0.9% month-on-month decline to its lowest since May 2020. Manufacturing, which was down 1.1%, was one of the key contributors to the decline, alongside notable drops in basic metals and pharmaceuticals. Mining and quarrying saw an even larger drop of 3.3%.

The ONS data shows that production output for the three months to January 2025 was estimated to have decreased by 0.9% compared with the three months to October 2024; this is the ninth consecutive three-monthly decline in production output.

from GDP monthly estimate, UK: January 2025

All in all, not the best outlook for the UK. However, RSM’s analysts do conclude that “things aren’t as bad as they seem at first glance.”

“Growth should still improve throughout the year and the surge in inflation is likely to be temporary. But it now seems like we’ll have to wait until 2026 before a return to ‘normal’.”

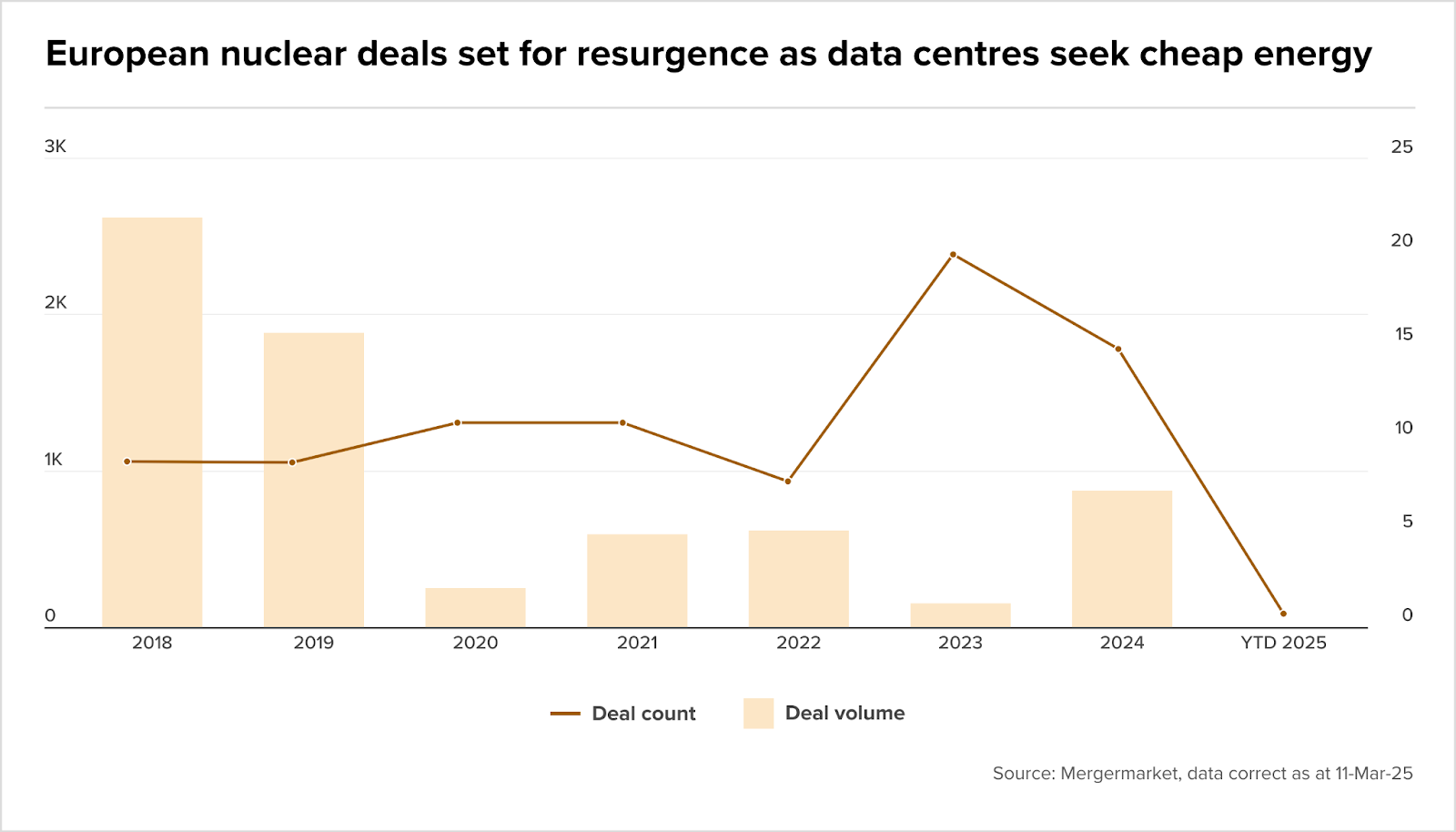

M&A goes nuclear

A nuclear renaissance is underway in Europe, which could be good news for dealmakers. With data centres consuming massive amounts of energy, the need for reliable, low-carbon energy solutions is pushing industries to look toward atomic energy.

France is leading the charge, with the overall momentum also extending to the UK where the Hinkley Point C project, one of Europe’s largest nuclear initiatives, is a major focus for investment.

According to MergerMarket, nuclear dealmaking is beginning to boom as a result. In 2024, deal value in Europe grew to EUR 886m across 15 deals, compared to EUR 160m over 20 transactions in 2023.

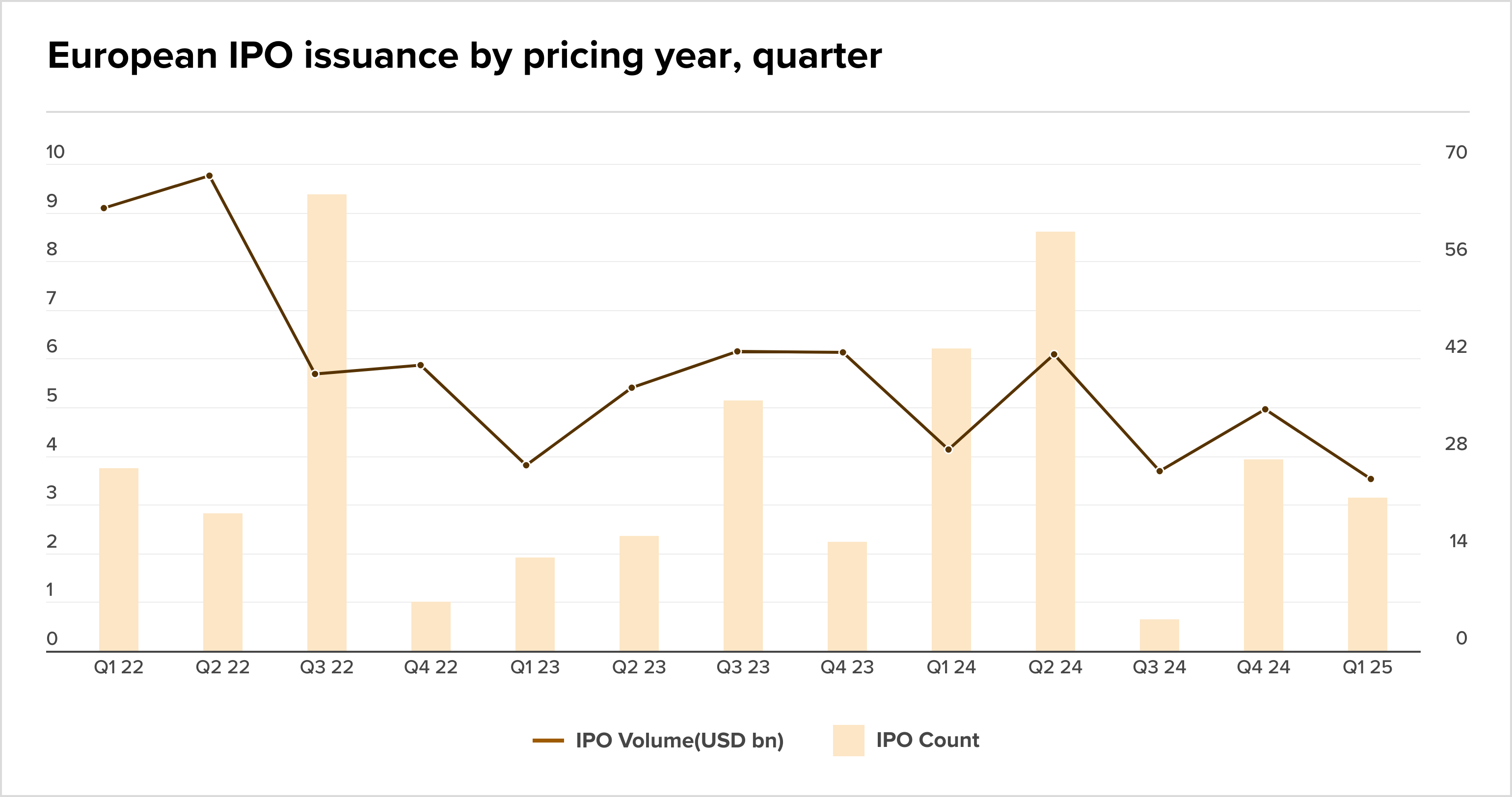

Cautious approach: IPOs hit pause

New data suggests that European IPO issuers are pausing as US market volatility and trade tensions create uncertainty. Expected deals, like Blackstone-backed Cirsa, are being delayed, with market conditions making it risky to launch new listings.

This comes off the back of last week’s update on Bain’s decision to shelve its IPO plans in favour of a £5bn sale of its Kantar assets.

Fundraising

- Vanguard ends new fund drought with active fixed income plans

- Ex-Millennium portfolio manager’s hedge fund gains 7% in debut year

- APG and TIAA back Arcmont’s £397.3m impact private credit strategy fundraise

- bd-capital raises £360m for second fund

- PBBE closes sixth European real estate PE fund at £418.2m