Daniel Black

Daniel Black

Hello,

Well, that was quite the week. The good news is the global trade war seems to have been averted for the time being, though the constant turmoil and cliff-edge negotiations aren’t creating a fruitful environment for M&A.

If we look beyond tariffs, the news this week includes:

- Goldman topping the UK dealmaking charts in Q1

- KKR agreeing a £1.6bn Assura takeover

- Barclays hiring Andrew Woeber as its global head of M&A

Thanks for reading, and connect with me on LinkedIn if you want to discuss how Ideals can help streamline your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Starmer shifts focus in US trade talks to cutting 25% tariff on UK cars

- Trade war makes improved UK-EU relations ‘imperative’, says Reeves

- Trump tariffs will hit UK economic growth, BoE official warns

- UK pushes back on Trump’s claim Britain is ‘happy’ with 10% tariff

- UK considers nationalising British Steel

- M&A and IPO activity have paused due to market uncertainty, says Barclays’ Kristin Roth DeClark

- UK looks to ease regulation for smaller PE firms

- Cavendish says Trump tariffs could boost UK equities after ‘challenging period’

- Goldman Sachs leapfrogs rivals to top UK dealmaking in first quarter

- Assura rejects revised takeover offer from Primary Health Properties

- NHS landlord Assura agrees £1.6bn takeover by KKR consortium

- UK watchdog says it might accept remedial measures offered by SLB, ChampionX

- Ripple is set to acquire prime broker Hidden Road for £0.97bn

- Court approves takeover of TI Fluid by ABC Technologies

- Peabody Energy reviews Anglo coal deal after mine explosion

- Baker Tilly in talks to buy its US rival, Moss Adams, as accounting dealmaking heats up

- Janus Henderson strikes a deal to manage £35bn of Insurer’s assets

- Bowmark considers £500m Totalmobile sale

- Coats Group plans to fully exit from the Performance Materials division’s US Yarns business

- McLaren plans to merge with British EV start-up Forseven

- Shell will sell its interest in Colonial Enterprises to Brookfield Infrastructure Partners for £1.12bn

- Good Energy takeover by Esyasoft is sanctioned by court

- Canal+ and MultiChoice extend offer deadline to October 2025

- De La Rue bid talks continue as agrees sale of its Authentication unit

- 3i Group pauses MPM sale amid US tariff turmoil

- Bridgepoint, Cinven, and Triton make MyDentist bid

- Standard Chartered considers african expansion after divestures

- Fusion Fuel signs LoI to acquire a British fuel distribution company for £50m

Salaries and bonuses

- Gender pay gap widens at Lloyds Bank and Nationwide, despite a record low in the overall gap across major UK employers, with Lloyds’ gap rising to 35.5% and Nationwide’s to 29.2%

Job moves

- Standard Chartered hires David Hardoon as global head of AI enablement

- BP Chair plans to exit as oil major faces pressure from Elliott

- UK paytech Judopay names Anant Patel as new CEO

- Paymentology hires former GSG exec Jim Hart as new CISO

- BNP Paribas flies in Lynagh from New York to head UK global banking

- HSBC UK asset management boss Stuart White is to exit

- FCA chief executive Nikhil Rathi reappointed for second term

- Bank of England governor Andrew Bailey is to lead global banking watchdog

- Pemberton appoints Jürgen Breuer as Head of European Origination

- Investec strengthens European team with private credit appointment

- Gresham House Ventures appoints Investment Partner amid hiring push

- Barclays capital markets veteran Ken Brown to retire from investment banking

- Goldman Sachs names Weber and Wilkins to head of real estate dealmaking in Europe

- Credit Agricole eyes dealmaker hires in push for more European M&A

- Barclays hires Centerview dealmaker Woeber to lead global M&A

Market trends

UK’s knowledge hubs redraw the VC map

Cambridge and Oxford aren’t just academic heavyweights – they’ve also become VC magnets, pulling in £1.4bn of capital in 2024. Together, they made up over a quarter of VC funding beyond London, riding a wave of university-backed spinouts and deep tech breakthroughs. With a legacy of unicorns like ARM and Darktrace, both cities continue to prove that global innovation doesn’t need a London postcode.

The UK government is keen to increase this momentum through its recently announced £13bn in infrastructure funding, which aims to turn the so-called Oxford-Cambridge Growth corridor into Europe’s Silicon Valley. Meanwhile, major cities like Edinburgh and Birmingham are quietly making moves of their own, clocking record-breaking VC totals in 2024, according to PitchBook.

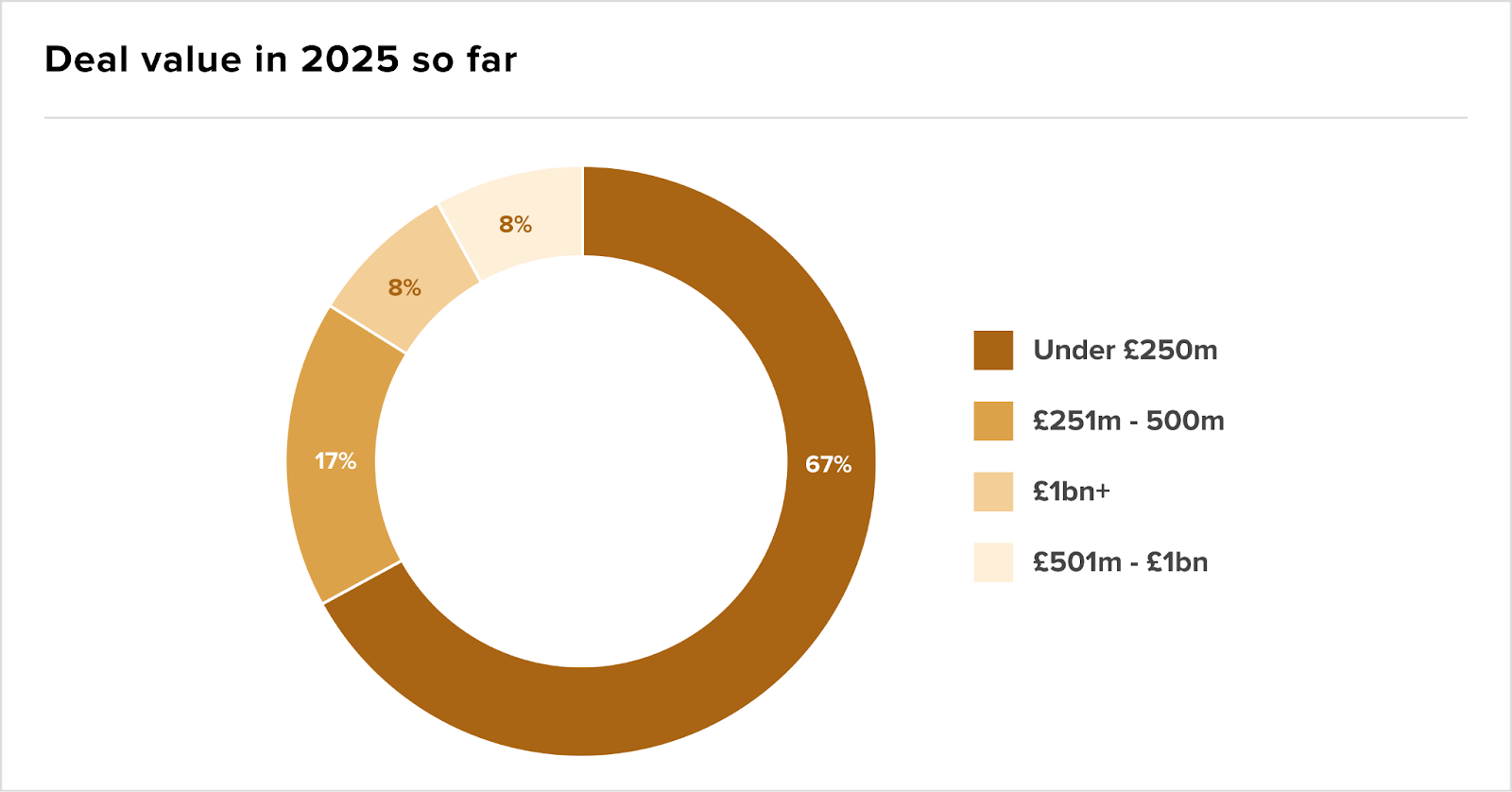

Strongest month yet, though values remain low

March delivered a steady level of public M&A activity in the UK, matching the seven firm offers announced in the same month last year. However, deal size remained modest. Six of the seven confirmed deals were valued below £250m, including Xtellus Capital Partners’ £5.1m bid for Sirenus Energy and Kondor AI’s £20.5m share offer for Ora Technology.

According to Herbert Smith’s data, the average deal value for 2025 so far stands at £263m – considerably lower than 2024’s £977m and 2023’s £362m. Despite relatively subdued valuations, interest in the market is building.

The month brought 12 possible offers, double the number seen in March last year. Larger potential deals, such as Greencore’s interest in Bakkavor Group (£1.14bn), could shift the tone of activity later in the year.

UK’s exporter face a rough ride

Though President Trump has paused a majority of import tariffs, the 25% levy on the automotive sector is still in place. He has also threatened to introduce “major” pharmaceutical tariffs.

This is bad news for the UK, which has cars and pharma products at the top of its list of exports to the US. Jaguar Land Rover has already paused shipments to the US, while GSK and AstraZeneca are potentially deeply exposed.

At the same time, UK interest rates are expected to fall to 3.75% by year-end, potentially fuelling deal appetite. Yet with transatlantic trade friction rising, buyers will be more cautious – scrutinising US-linked revenues, repricing risk, and sharpening diligence on cross-border deals.

Have you got insurance for that deal?

The uncertain deal market seems to be good news for insurers. W&I (Warranty & Indemnity) insurance is becoming a staple in modern M&A, helping buyers and sellers shift risk and close deals faster. And new data shows it’s particularly popular in the UK.

W&I usage in the UK hit 43% last year – the highest across Europe and a sharp rise from 30% in 2023. This reflects a busy H2, apparently driven by CGT changes and a rush to deploy long-held capital. Across Europe, W&I saw an 8% uptick, particularly in mid-sized and large transactions.

From CMS European M&A Study 2025

Fundraising

- Investindustrial closes oversubscribed £3.4bn fund

- Pantheon closes £4bn private credit secondaries fund

- L&G, NTR’s clean power-focused fund raises £520m at final close

IPOs