Daniel Black

Daniel Black

Hello,

It’s been a week of U-turns in the UK. Not only did the government put more pressure on public finances by caving on its proposed welfare reforms, but Spectris switched suitors to KKR only a week after announcing a takeover deal with Advent.

KKR’s £4.7bn offer is a 96% premium on the company’s share price before takeover interest became public.

And in other news:

- The bidding war for BP’s Castrol unit is heating up

- The CMA signed off Aviva’s £3.7bn Direct Line takeover

- Santander is buying TSB for £2.65bn

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Dealmaker spotlight

This week we spoke with Bethany Winsby, a Senior M&A Consultant at Deloitte.

Bethany shared her unique career journey, insights into mid-market deal origination, and why soft skills matter in M&A.

Read the article to find out more, and get in touch if you’d like to be profiled in our newsletter.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

Industry news

The rumour mill

- Foresight Group to invest £1bn+ across UK and Ireland

- TSB gets its moment in the Spanish sun

- BP’s $8bn Castrol unit attracting more bidders

- Chesnara is to buy HSBC’s UK Life Insurance Arm for £260 million

- HSBC to sell German custody business to BNP Paribas Securities Services

- Revolut set to enter Argentina via Banco Cetelem acquisition

- Nigeria’s GTBank to Raise $100 million Selling Shares in UK

- UK clears $5 billion Aviva-Direct Line deal, forming Britain’s top home and motor insurer

- Santander to expand UK footprint with £2.65bn TSB acquisition

- Apollo-backed Athora nearing takeover of UK’s Pension Insurance Corporation

- KKR pips Advent with £4.7bn offer for UK industrial company Spectris

- Santander to buy UK high street lender TSB for £2.65bn

- UK competition watchdog begins initial probe into Boeing-Spirit Aero deal

- Boeing set to take over Spirit in Northern Ireland as buyer talks fail

- Private equity firm HIG targets £800mn for sale of ex-KPMG restructuring unit

- Unilever pays $1.5bn for men’s grooming brand Dr Squatch

- Private equity-backed Valsoft acquires UK-based collectionHQ

- Iberdrola’s Scottish Power and Ovo Energy are in merger talks

- RTL to buy Sky’s German unit as it bids to challenge US streaming giants

- Oakley Capital to sell legaltech platform vLex to Clio

- UK Mobile Bank Starling Looking to Buy a US Lender in Expansion

- Gibraltar Industries seeks renewables exit to focus on building ops

- ICG sells Kee Safety stake to Inflexion and 65 Equity

- Battery Ventures-backed Forterro buys software company Targit

- Graphite sells education services provider Empowering Learning Group

- Maven exits employee engagement platform Oak Engage

Salaries and bonuses

- Goldman Sachs always pays a group of London MDs $9.5m+ each

- Good luck earning more than £860k at Rothschild

- Goldman Sachs ups bonuses for top UK bankers by almost 40%

- ING to cut 230 senior wholesale banking roles, focus on junior hiring

Job moves

- JPMorgan UK private banker exits as senior reshuffle continues

- Barclays revamps Asia-Pacific investment banking leadership team

- Alantra hires Matthes to lead investment banking in Germany

- Partners Group hires Stéphane Tetot as managing director

- UBS transfers 544 more UK Credit Suisse staff across as integration continues

Market trends

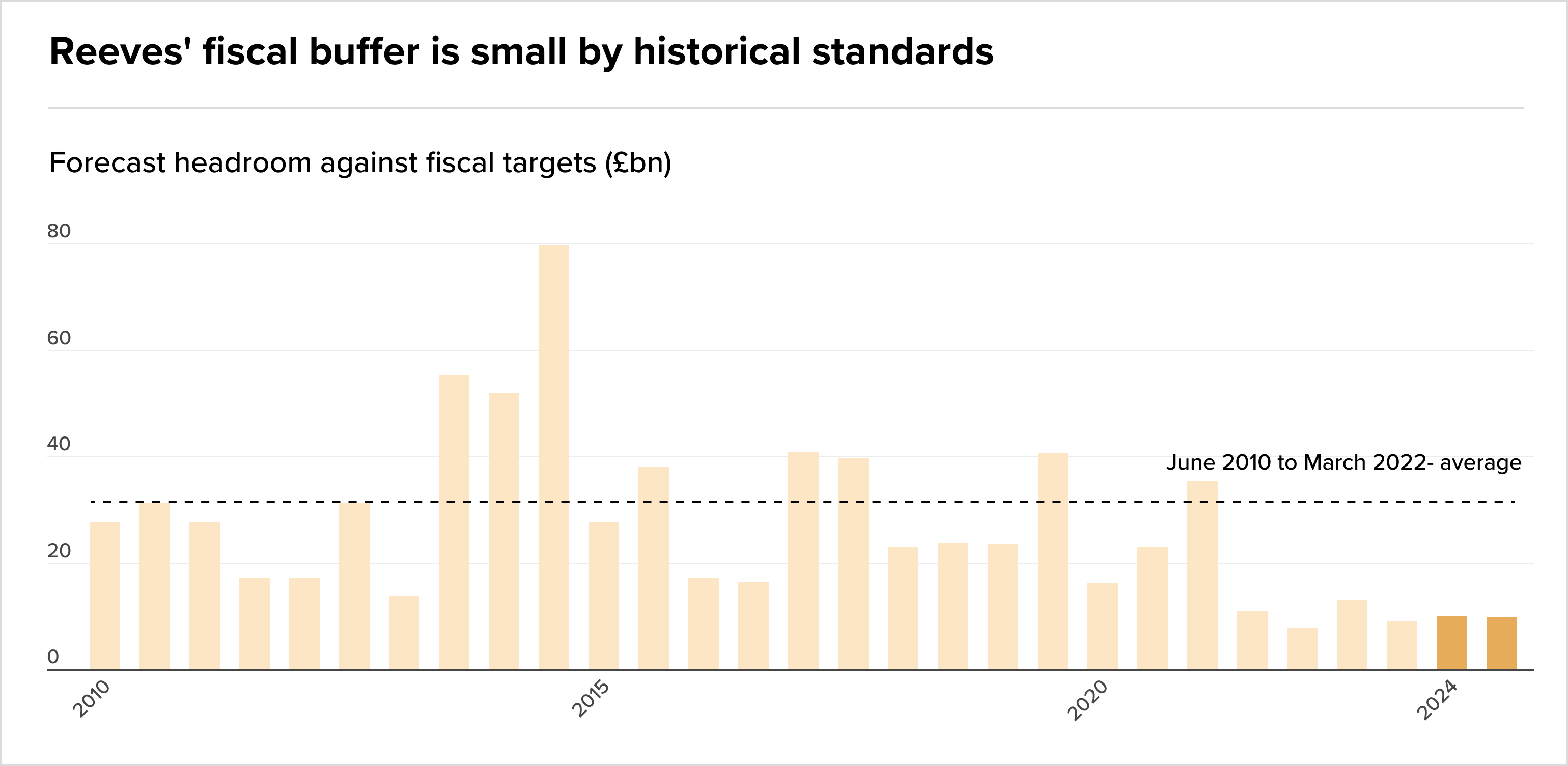

No headroom for Chancellor Reeves

In a fairly dramatic week for the Labour government, the Financial Times reports that the UK’s fiscal landscape has reached a critical juncture. Chancellor Rachel Reeves faces a potential £25bn shortfall following welfare reform U-turns and weakening growth forecasts.

Where previous chancellors maintained robust safety buffers, Reeves now has to operate with minimal headroom that renders public finances vulnerable to minor economic shocks.

With major revenue raisers now off the table due to manifesto commitments, Reeves faces what one ally describes as “no palatable options”. As a result the government is eyeing stealth taxes, from frozen thresholds that could raise £9.2bn to targeting businesses and the wealthy with precision strikes.

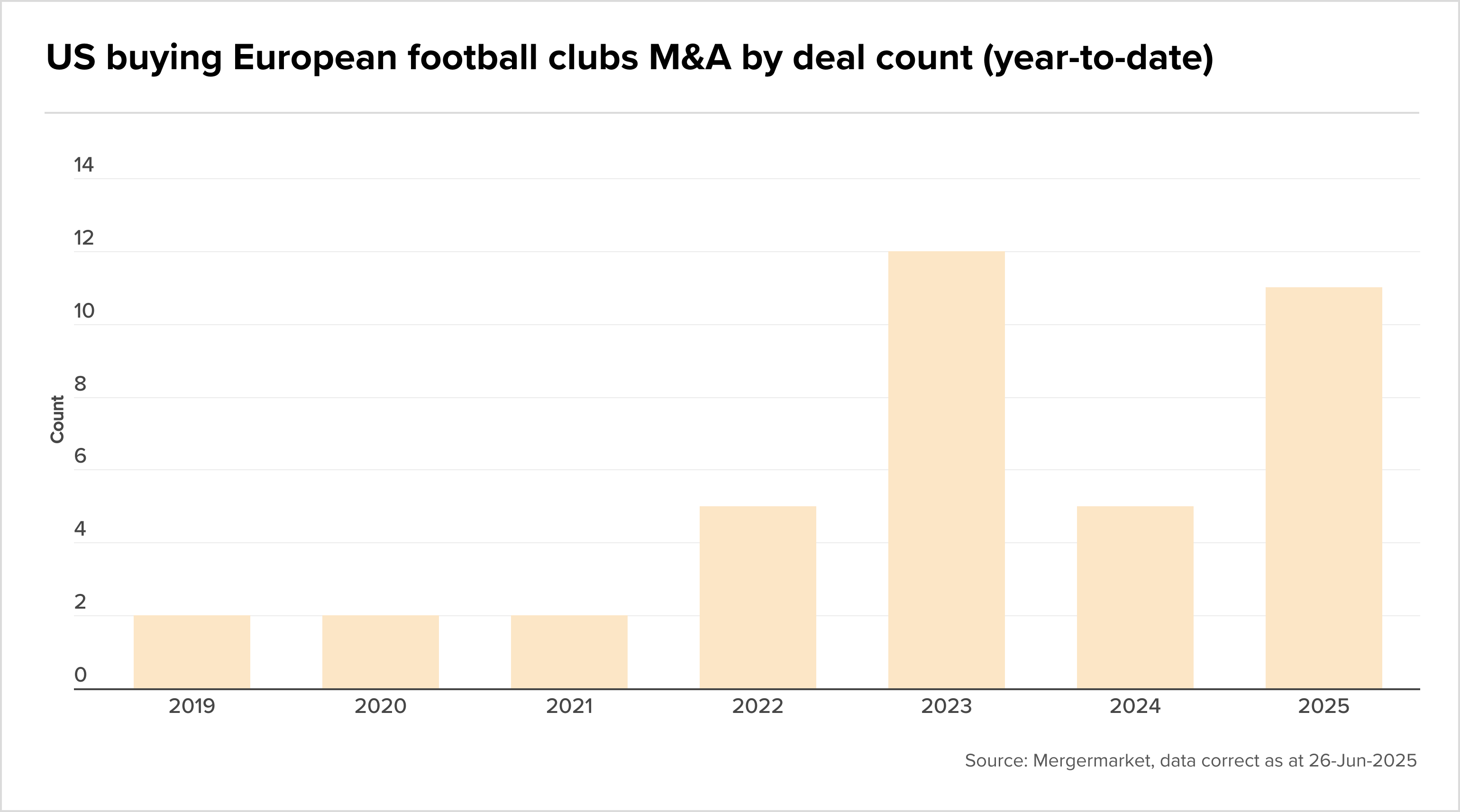

US buyers aiming to “do a Wrexham”

US investors are treating European football clubs like sleeping giants waiting to be awakened, completing 11 deals so far in 2025 and targeting legacy clubs with untapped commercial potential.

According to Mergermarket, American capital is flowing into strategic acquisitions, from Rangers FC’s £20m injection by 49ers Enterprises to multi-club ownership models. While UEFA’s financial fair-play rules create regulatory hurdles, US investors are adapting by pivoting toward women’s clubs and undercapitalized assets where valuations remain modest but growth potential is substantial.

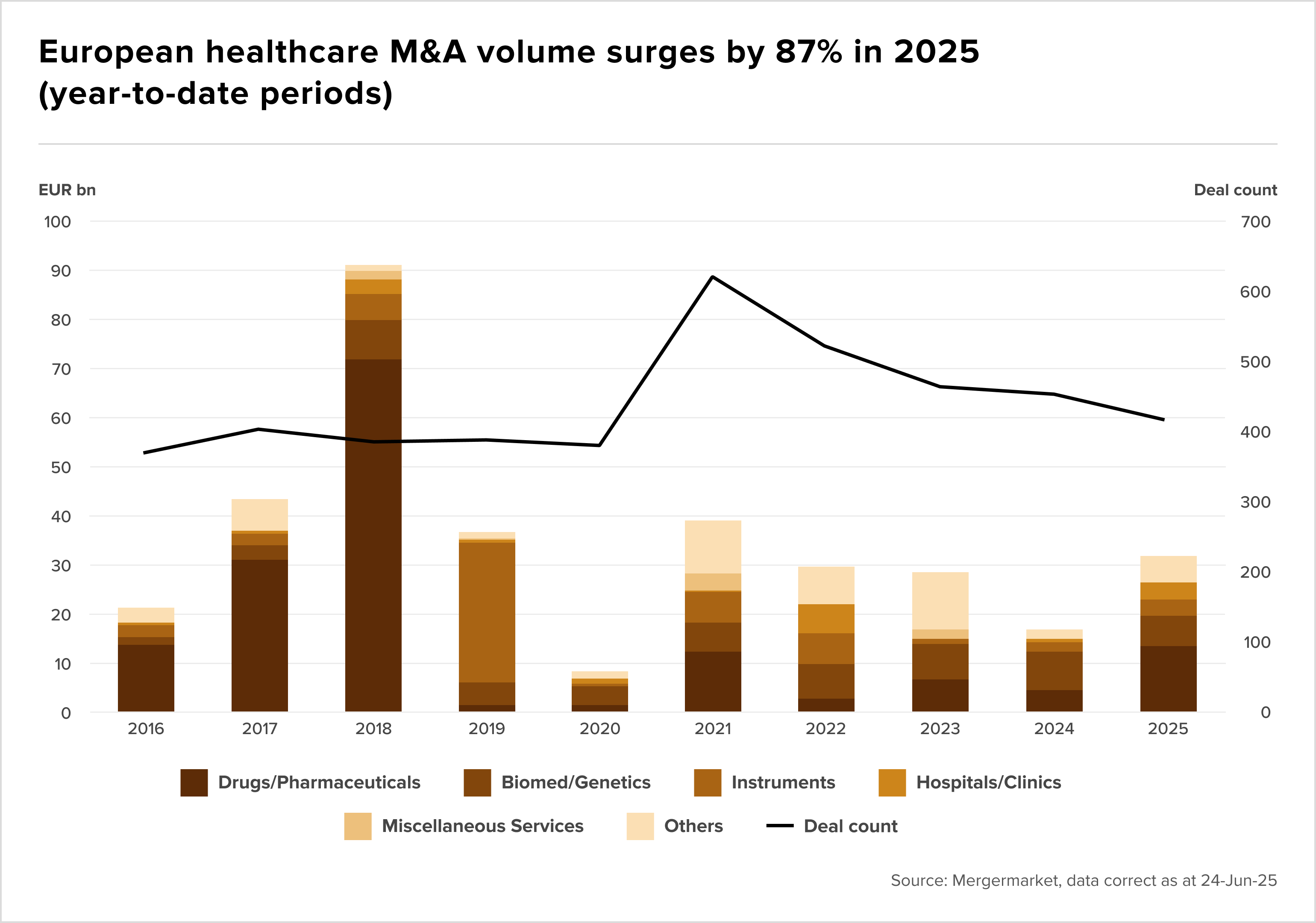

Uncertainty ahead for European healthcare M&A

European healthcare dealmakers are navigating a tale of two halves in 2025. The industry has seen an impressive 87% surge in deal volume, reaching €31.8bn year to date, however it faces cooling momentum as Trump’s tariff uncertainties cast shadows over the sector.

Mergermarket reports the pharmaceuticals segment continues to dominate, accounting for 42% of total healthcare volume and posting its highest activity levels since the pandemic.

Private equity firms are adapting to uncertainty with longer lead times and more strategic positioning, evidenced by sponsor buyout deals jumping 276% to €29.6bn this year.

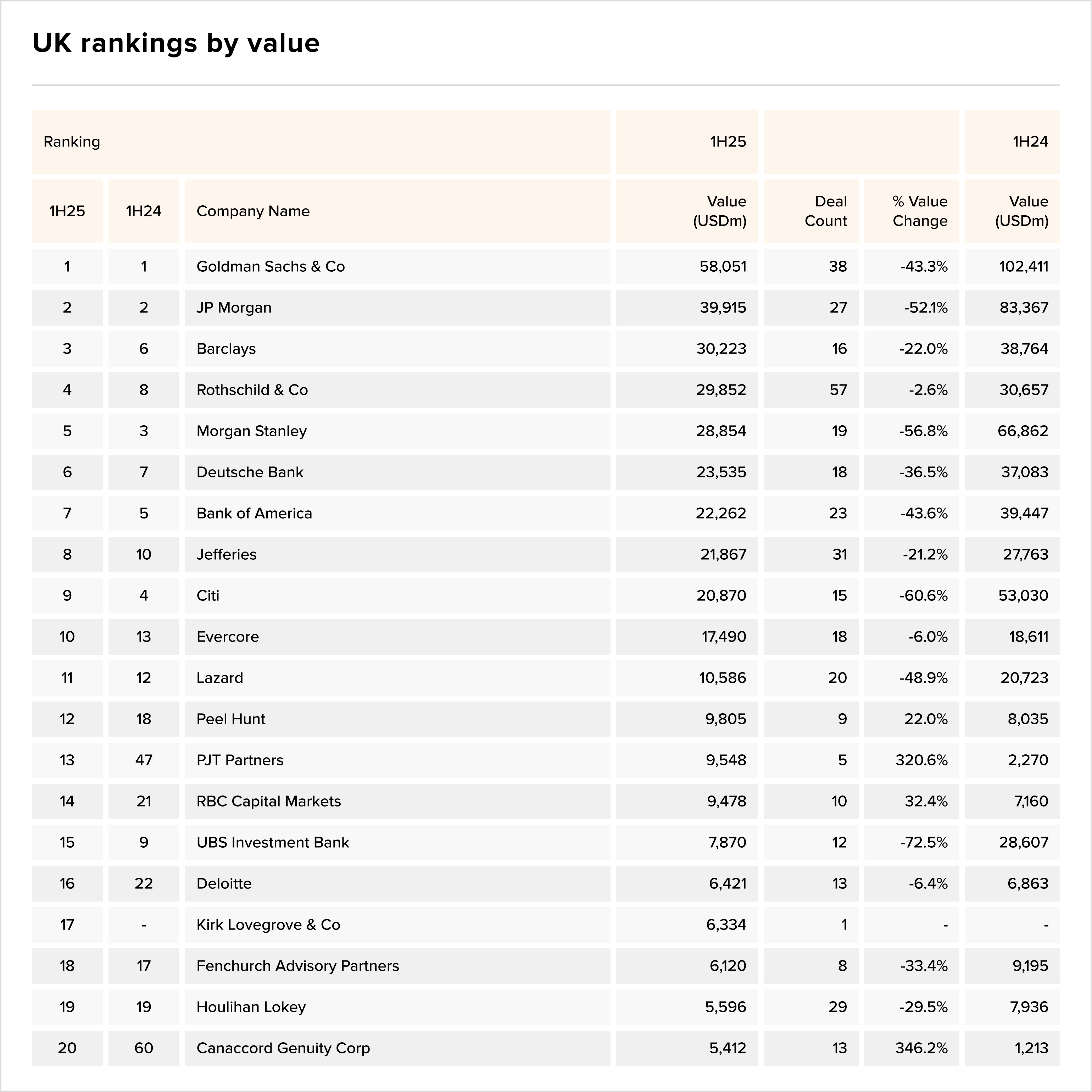

Goldman retain its crown

And finally, congratulations to Goldman Sachs for maintaining its dominance in the UK M&A advisory market during the first half of 2025, securing $58bn in deal volumes despite a 43.3% YoY decrease.

The Mergermarket ranking also saw Barclays climbing from sixth to third position and PJT Partners surging from 47th to 13th place.

Fundraising

IPOs