Daniel Black

Daniel Black

Hello,

Have we heard the starting gun for a wave of consolidation in the UK’s home fibre market? Reports suggest that Virgin Media O2 is in talks to acquire Netomania for around £2bn, which would cement its status as BT’s biggest competitor.

The FT reports that dozens of smaller broadband providers are struggling with high debt and low customer numbers, making consolidation a likely outcome.

And in other news:

- Battersea Power Station is up for sale

- Thames Water paid KKR’s £20m due diligence fees

- EY’s partners saw pay increase to £78k on average

Thanks for reading, and connect with me on LinkedIn if you want to discuss how Ideals VDR can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Nelson Peltz says $7bn take-private bid would let Janus Henderson ‘de-risk’

- UK Broadband challenger Netomnia courts CityFibre, Nexfibre for £2bn sale

- AIG to buy stakes in Convex, Onex for more than $2.7bn

- Vodafone to buy German cloud specialist Skaylink for $204m

- UK’s Virgin Media O2 signs deal with Musk’s Starlink for rural coverage

- Virgin Media O2 in talks for £2bn takeover of broadband rival

- London’s rejuvenated Battersea power station is put up for sale

- Angola submits bid for Anglo American’s entire De Beers stake

- EU to probe sale of Anglo’s nickel business to China-backed MMG

- Thames Water paid £20m to cover KKR’s due diligence for abortive bid

- Cinven weighs up Think-cell sale

- Drax agrees to acquire 260-MW battery project portfolio from Apatura

- Long Path to buy UK’s Idox for $438m

- CVC, Jersey Telecom to buy Manx Telecom Group

- BlueCrest Capital’s UK revenue surges 149%

- Coutts assets rise as markets boost wealth managers

- Global equity issuance jumps to $687bn despite economic headwinds

- Barclays to buy Best Egg for $800m and expand US footprint

- English football investor accused of ‘egregious’ governance in proxy fight

- LSEG teams up with Anthropic in latest AI deal

- Main Capital invests in logistics platform Shippingbo

- Blackstone among suitors for UnitedHealth-owned Optum UK

- Welltower may be near £4bn deal to buy Barchester Healthcare

- Legal & General agrees £4.6bn UK pensions buyout deal with Ford

- Major banks take £170m stake in LSEG Post Trade Solutions

Industry news

- Sustainable finance is a growth opportunity for the UK

- FCA targets 2027 launch for UK equities consolidated tape

- BlackRock and LSEG extend partnership with addition of Preqin private markets data

- HSBC’s dealmaking fees slip 6% after investment bank pullback

- Why the Bank of England has freed small lenders from Brexit’s shackles

- Revolut wins banking licences in new markets as it continues to face UK delays

- Robinhood to launch UK futures trading with CME

Salaries and bonuses

- EY’s UK partner pay rises to average of £787,000

- BlueCrest pay in London: Up 92% for partners, 14% for the rest

- Morning Coffee: Barclays’ biggest bonus goes to retail bankers who left 18 years ago

Job moves

- Electronic trader Optiver hires Barclays and Morgan Stanley salespeople in equities push

- HSBC Asset Management COO steps down after six years in role

- HSBC has completed planned job reductions, CFO says

- London Metal Exchange CEO says no plans to step down ahead of 10th year in charge

- London credit hedge fund run by trading prodigy hired an equity derivatives PM

- Blackstone appoints Michele Rabà as head of European Private Equity

Market trends

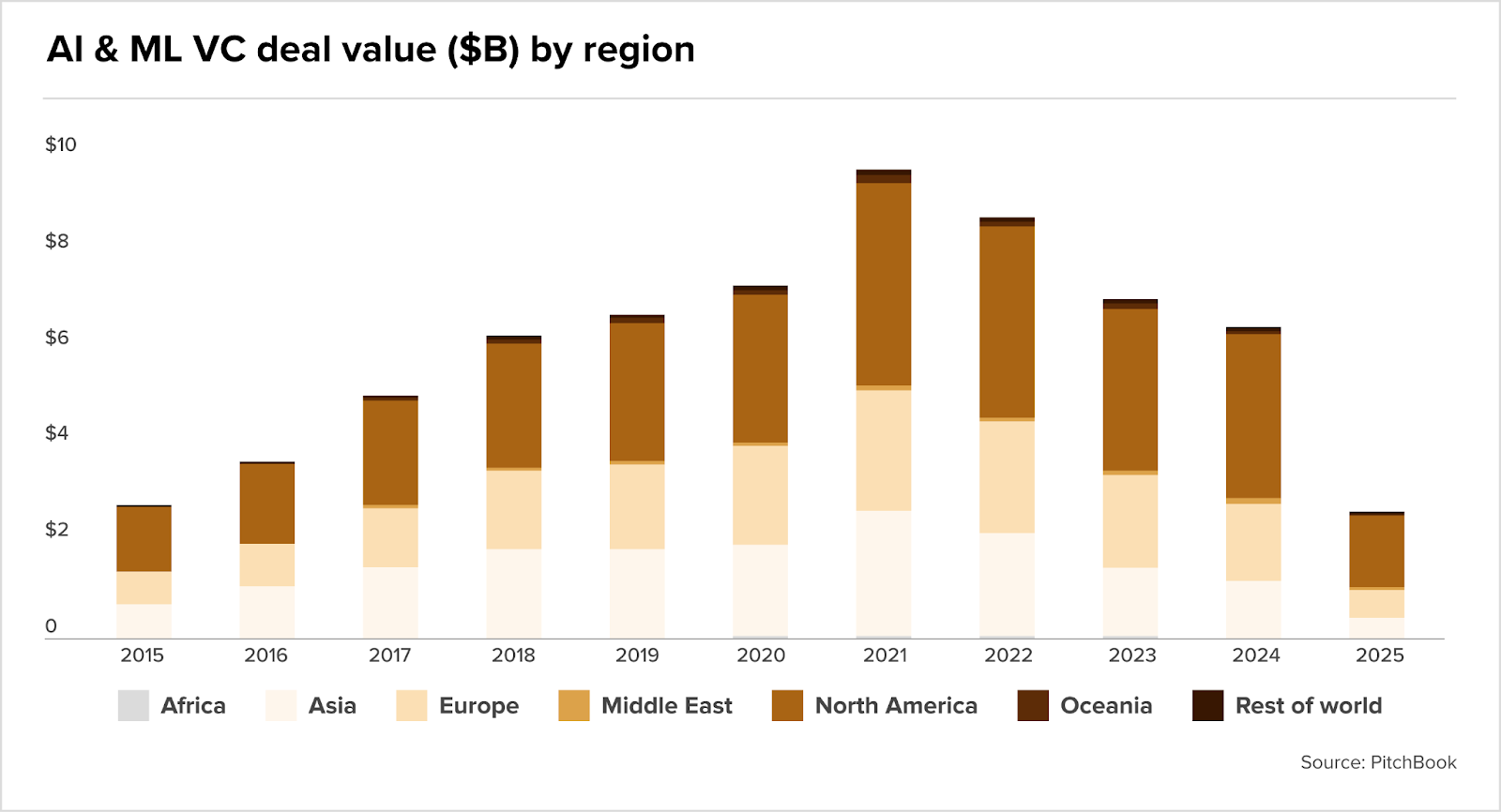

Europe lags behind in AI funding

In the great AI goldrush, North America is hoovering up the lion’s share of investment. The region’s startups captured around 60–70% of AI/ML VC deal value in 2024 and H1 2025, far above Europe and Asia, reported PitchBook.

Europe’s modest share reflects tighter capital and risk aversion, with the continent’s AI sector constrained by new regulations and record levels of “down rounds” and valuation resets. Median deal sizes in Europe have stagnated, with late-stage (Series E) valuations notably below US levels, and many scaling companies relying on US investors to fill capital gaps.

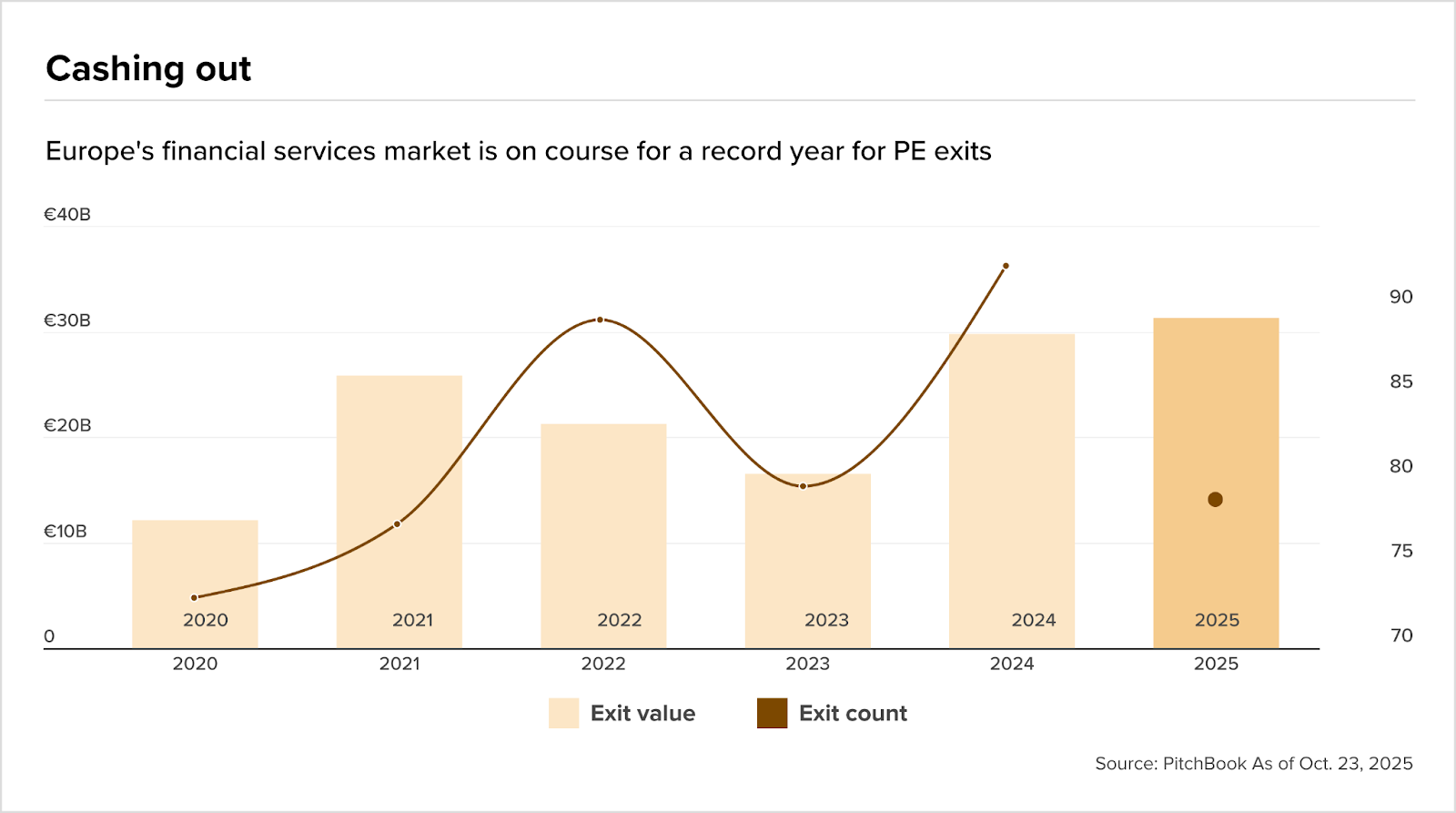

Record PE exits in Europe

Private equity exits in Europe’s financial services sector have surged to record levels in 2025, with €31.3bn deployed across 77 transactions year-to-date. This momentum reflects both liquidity pressures as LPs demand capital returns before committing to new funds and improving market dynamics, including regulatory tailwinds such as the EU’s CRR3 framework and the UK’s streamlined Solvency II regime catalysing consolidation activity.

Marquee deals underscore the sector’s vitality, led by CVC’s €6.7bn exit of Pension Insurance Corporation and Cinven’s €3.5bn Viridium Gruppe sale.

With valuations normalizing and strategic buyers actively pursuing fintech, payments, and insurance assets, PitchBook predicts 2025 will close with approximately €37bn in total exit value across the financial services vertical.

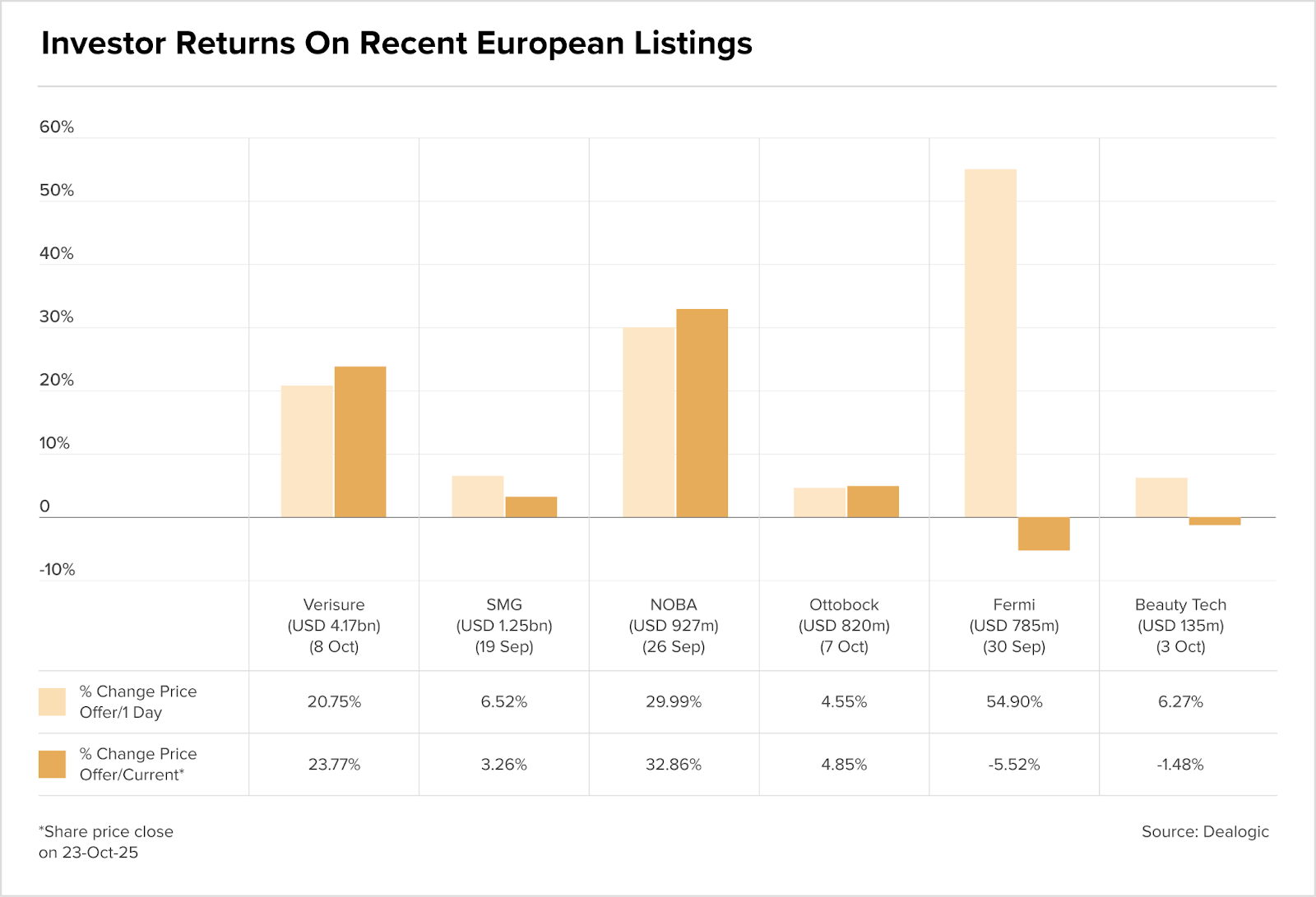

Seller pricing strategy tests investor confidence

According to Dealogic, Europe’s IPO market is showing signs of strain as sponsors adopt increasingly aggressive pricing strategies that prioritise immediate seller returns over aftermarket performance.

While Hellman & Friedman’s €3.6bn Verisure Stockholm listing has delivered strong 24% gains, recent deals including SMG and Ottobock have traded flat after syndicates stretched peer group comparisons to justify premium valuations.

Investors report growing frustration with sellside efforts to benchmark against distant, high-multiple peers rather than natural comparables, a dynamic now emerging in Shawbrook’s London IPO where the discount to closest peer Paragon appears negligible.

Fundraising

- BC Partners raises $1.8bn ahead of first close of flagship buyout fund

- Columbia Threadneedle launches US asset-backed securities fund

- GHO Capital raises over €2.5bn for largest fund

IPOs

- BC and Pollen Street take Shawbrook public in £1.9bn London IPO, with the specialist lender pricing its £348 million offering in the middle of the range.

- Food supplier Princes is set to price London IPO at bottom of range

- UK Boeing supplier Doncasters prepares IPO in New York