Harsh Batra

Harsh Batra

Hello,

This week, Innomotics India agreed to acquire Siemens’ low-voltage and geared motors business, a significant industrial consolidation with global implications and strong M&A relevance, especially as multinationals rejig portfolios and shift production toward India.

Meanwhile, ICICI Prudential AMC is preparing an acquisition in the PE space. It is a rare move for a domestic asset manager to reckon with the riskier asset class. If this comes through, it could reshape the competitive landscape for homegrown managers, alter LP allocation options, and push India deeper into alternative assets.

And, Shriram Pistons has bought three companies for ₹1,670 crore ($185 million), a neat manufacturing roll-up.

Finally, climate-tech funding dipped as VCs figured they preferred exportable solutions, prioritising defensible IP and global markets over the government subsidy-linked domestic play.

I hope you enjoy this week’s roundup – please connect on LinkedIn to discuss how Ideals VDR can help with your next M&A deal.

Let’s dive in.

Deal Tracker

Our weekly roundup of confirmed M&A deals in India.

Market Trends

S&P’s happy upgrade and Parliament’s unhappy warnings

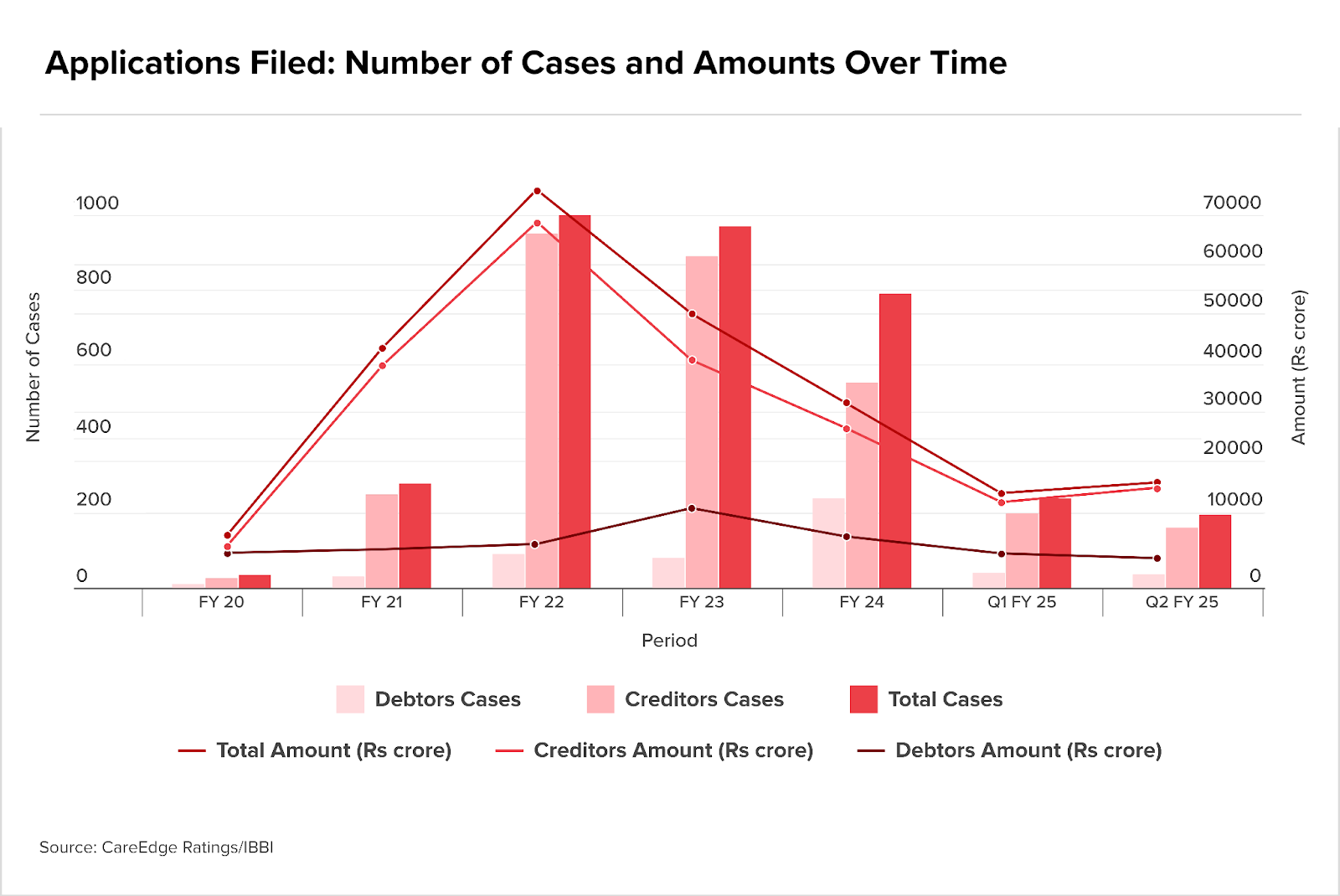

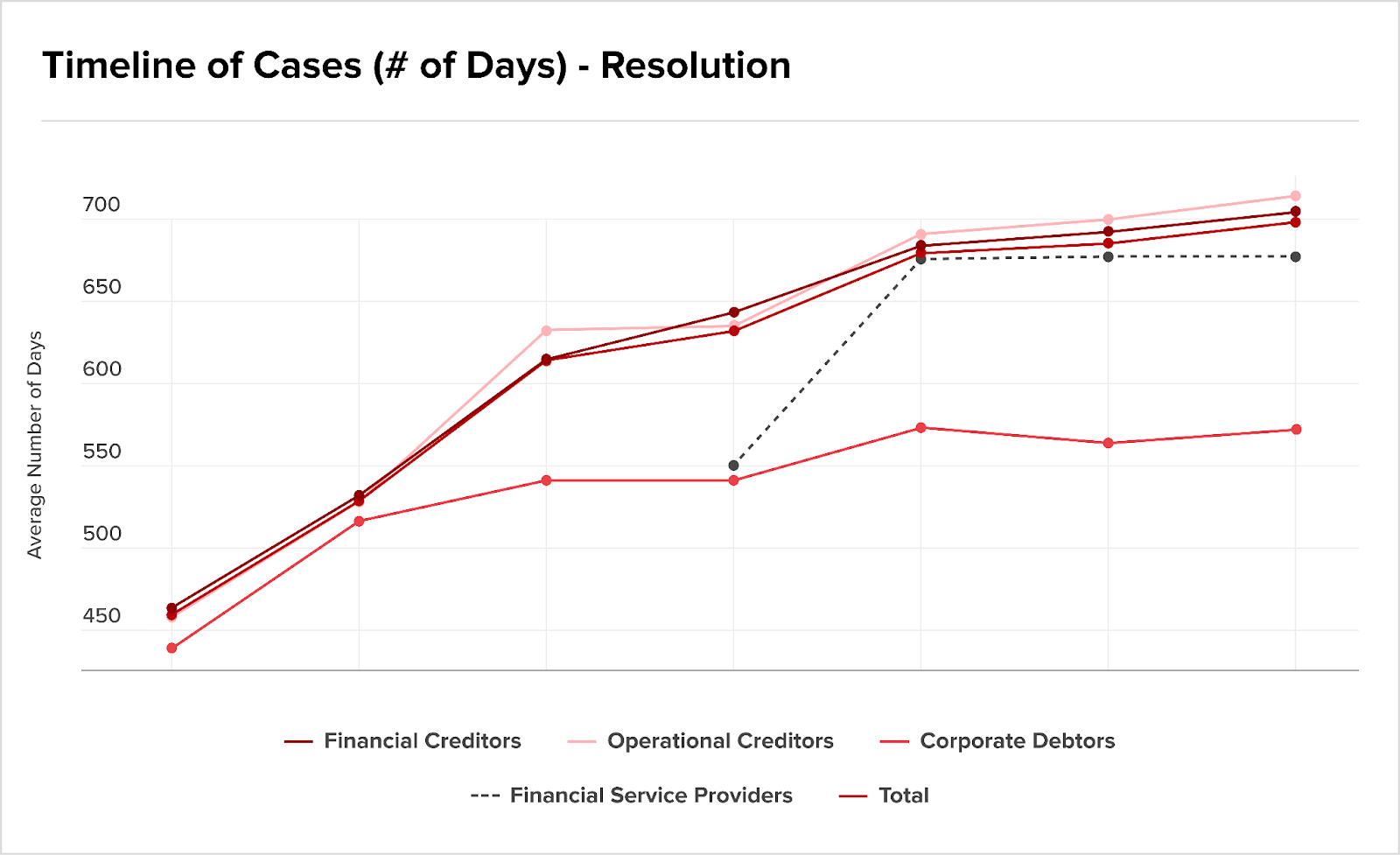

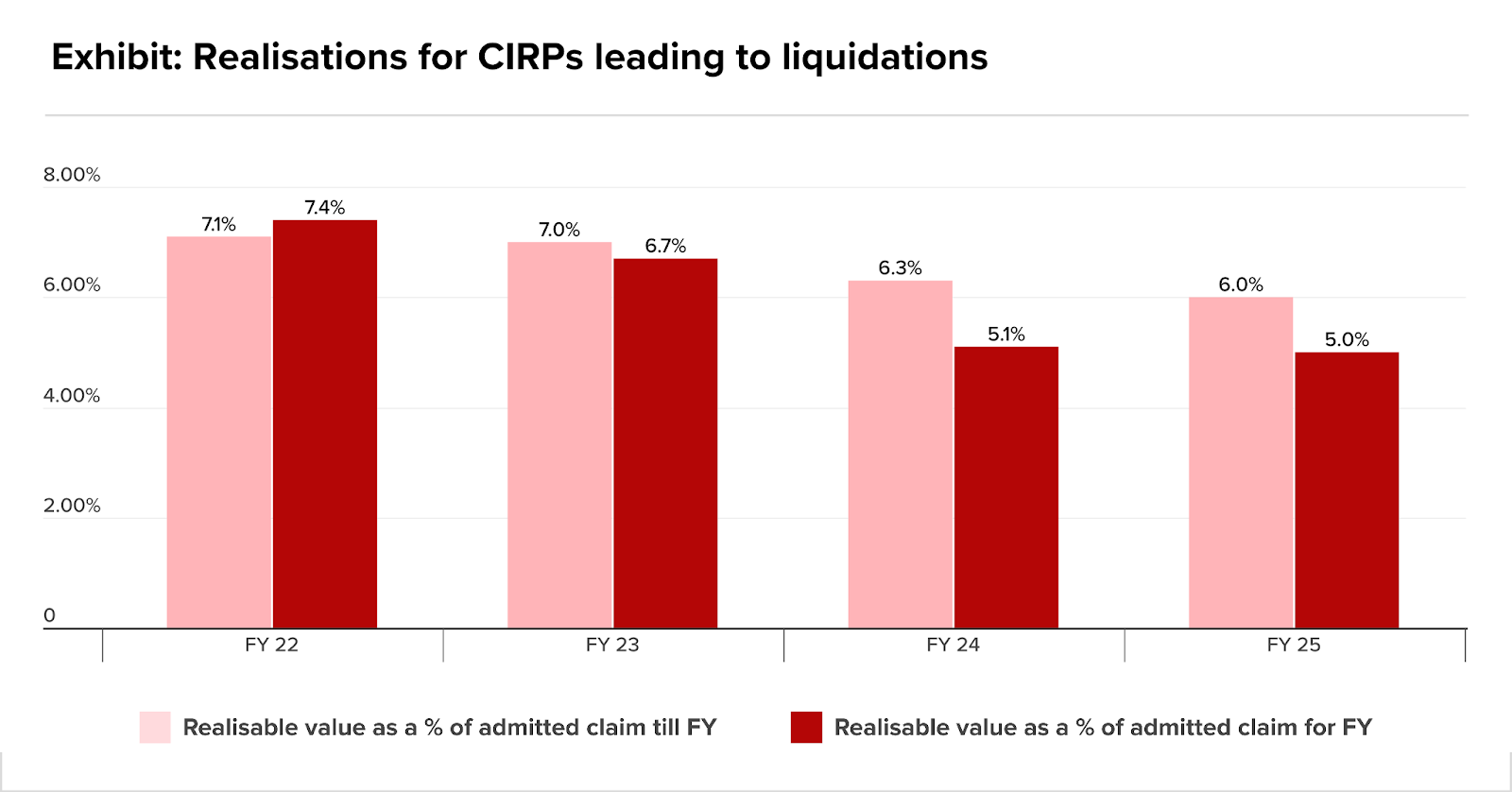

It seems schizophrenic – just as S&P upgraded India’s insolvency framework for becoming more creditor-friendly, policymakers in Delhi warned the system being celebrated was slow, costly, and prone to value erosion.

The ratings group thinks India’s laws governing restructuring of distressed assets – under the Insolvency and Bankruptcy Code (IBC) from Group C to Group B – are improving by offering better protection of creditor rights.

In other words, it seemed pleased that the balance of power was moving decisively toward creditors, including the real possibility that promoters (family-run business owners) could lose control if they failed to resolve dues, a departure from the era where promoters stayed in command.

The agency also noted materially stronger outcomes: average recovery rates had risen to 30%, compared with 15-20% earlier. Meanwhile, resolution timelines had shortened from 6-8, to roughly two years.

Yet, India trails S&P’s top-tier Group A jurisdictions, largely due to persistent delays, litigation overload, and procedural bottlenecks. Recent Supreme Court (SC) rulings reinforcing creditor rights were welcomed by lenders and investors.

So what for stressed asset dealmaking?

A higher jurisdiction ranking increases investor confidence in the enforceability of creditor rights and predictability of outcomes, supporting improved pricing for distressed deals.

Banks and financial investors may now feel more comfortable participating in resolution auctions or bidding for stressed assets, with global risk analysts viewing India more favourably, one hopes.

But even as the SC and the upgrade signal current improvement, a Parliamentary panel called for sweeping reforms to rescue and streamline the insolvency ecosystem. It said the system needed an overhaul of the rules setting out a number of recommendations to target speed to resolution, reducing litigation, and improving outcomes, which included the following suggestions:

- Advance ruling mechanism: Resolving key legal and factual issues before formal admission of a case, reducing avoidable litigation that stalls progress.

- Mediation and ADR: A structured mediation pathway to divert disputes away from tribunals and reduce caseload pressure.

- Digital ‘no dues’ system: A centralised digital platform to issue no-dues certificates and statutory clearances once a resolution plan is approved, enabling revived companies to restart operations without legacy frictions.

- Greater NCLT capacity, and more tech: More NCLT (National Company Law Tribunal, a quasi-judicial body) benches and rapid rollout of case-management tools such as the iPIE platform to improve handling efficiency.

- Deterrence against frivolous appeals: Upfront security deposits to discourage ‘vexatious’ appeals that delay the resolution process.

The panel aims to address structural chokepoints, litigation bottlenecks, unclear early-stage positions, and tribunal overload – all of which erode enterprise value and scare investors.

The S&P and the Parliamentary committee’s blueprint together suggest an insolvency framework that is not actively evolving toward global best practices, with major implications for M&A in stressed assets and turnaround and special situations investing.

In conclusion, India’s resolution regime is improving, but will the next wave of reforms unlock greater value?

The rumour mill

- The new Omnicom, post IPG acquisition: End of an era?

- The Byju’s money trail: How missing millions may have reached India from Singapore

- Swiggy’s Rs 10,000-crore QIP gets 4.5x subscription; most bids around Rs 375 per share, sources say

- Paramount’s hostile takeover bid filings for Warner Bros. reveals ‘hidden’ name involved in deal — Jared Kushner

- Multiplex Association of India fears Netflix’s acquisition of Warner Bros threatens India’s theatrical releases

- Innomotics India to acquire Siemens low voltage and geared motors business

- ILFS to initiate process before NCLT to recover Rs187 cr excess remuneration paid to ex-directors

- DCM Shriram Industries sets December 19 record date for major demerger scheme

- CCI Approves IHC’s Stake Purchase in Sammaan Capital

- Boat auditors flag mismatch in financial statements filed with lenders

- Bad boy billionaires: India’s biggest fugitive economic offenders and here’s how…

- Govt may seek bids for $7 billion IDBI Bank stake this month

M&A news

- Year in review: Late-stage deals hushed by loud IPO buzz

- What Every Company Can Learn from Private Equity

- United Hospitality Management expands into India with acquisition of Rosastays

- Moneycontrol Pro Market Outlook | Can Indian markets touch a new high before the year ends?

- India’s ICICI Prudential AMC plans acquisition in private equity space, CEO says

- Geopolitics reshapes LP allocations: Story of the year

- Despite FPI exodus, private equity bets big on India: $50 bn still flowing in: Amit Chandra

- Creador acquires 7% stake in La Renon healthcare from promoter, PeakXV

- Advent’s $1bn Whirlpool India deal collapses on valuation differences

- ‘Huge room to grow’: Why global investors are betting big on India, Christine Li of Knight Frank explains

- Indian Family Offices: A new investment force in private market

Job moves

- Who is Vikram Sahu? RBI approves appointment as Bank of America’s India CEO

- Viji Finance Limited Announces Resignation of Whole-Time Director Nitesh Gupta

- Veritas India Seeks Shareholder Approval for $130 Million Asset Sale and Director Appointment

- Twamev Construction And Infrastructure Ltd – Announcement under Regulation 30 (LODR)-Resignation of Director

- Timken India’s Non-Executive Director Douglas Smith to Step Down

- SBI Cards Appoints Smt. Parvathy Vairava Sundaram as Independent Director

- RBI Announces Appointment of Usha Janakiraman as Executive Director

- PTC India Seeks Shareholder Approval for Key Board Appointments

- Lexoraa Industries Appoints Two Independent Directors, Reshapes Board Committees

- InCred Capital ropes in Sanjay Singh as investment banking head

- AAA Technologies Board Meeting Approves Director Changes and Investment Plans

IPOs

- NephroPlus Raises Rs 260 Crore From Anchor Investors Ahead Of Rs 871-Crore IPO

- Nephrocare Health Services IPO subscribed 12%

- Meesho listing unlocks billions in wealth for founders, early investors Elevation, Peak XV

- India Digest: Blacksoil raises capital; Areion Asset launches fourth fund

- Blackrock fund to invest $225m in India’s Aditya Birla Renewables

- All eyes on ICICI Prudential AMC IPO as GMP suggests 13% listing pop. What investors should watch this week

- Ahead of IPO Nephrocare Health Services collects Rs 260 cr from anchor investors

Fundraising

- Centre Court Capital closes debut fund, to invest in sports, wellness firms

- Wakefit raises Rs 580 crore through anchor portion

- US, India-focused tech investor Nexus Venture Partners pulls in $700m for latest fundraise

- US-based Accel, Japan’s TDK Ventures eye funding in India spacetech firm

- Quick-fashion startup Knot ties up $5 million funding from 12 Flags, others

- Plant-based nutrition brand Earthful raises $2.8 million from Fireside Ventures, others

- India’s IBC wins global praise: Why S&P’s upgrade matters for industrial disputes and credit discipline

- India: DMI Alternatives closes $120m fundraising for private credit fund

- India deal review: Startup funding halves in November to $922m, mega deals dry up

- Fintech startup Fibe raises $35 million from IFC in series F round

- Edtech firm Uolo raises $7 million

- Climate-tech funding dips as VCs look for exportable solutions

- Chiratae Ventures launches Sonic Deeptech programme, offers cheques up to $2 million

Compliance/regulatory update

- Shriram Pistons shares jump 5% after acquiring three companies for ₹1,670 crore

- Sebi clears key hurdle for AIFs migrating to funds only for accredited investors

- S&P upgrades India’s insolvency regime to Group B on stronger creditor protection under IBC

- RBI’s interest cut supports growth, amid uncertainties

- RBI may need to inject further ‘2 lakh crore to let rates transmit

- RBI Governor Asks Banks For Transmission Of Rate Cut To Customers

- RBI cuts rates amid benign inflation and strong growth: The perfect hook shot

- Policy space may persist for emerging markets on 25 bps cut by Fed in Dec, followed by 50 bps cut in H2 FY26: S&P Global

- Parliamentary panel calls for sweeping reforms to rescue India’s insolvency & bankruptcy ecosystem

- India’s RBI to deliver up to $16 billion liquidity boost for bond markets

- Groww secures online bond distribution licence from Sebi

- Exceptional’: SBI hails RBI’s repo rate cut

- ET in the Valley: AngelList rethinks India play as new Sebi rules impact angel investing

- Electronics Inc asks govt to OK China JVs with 26% stake cap

- Budget 2026-27: Govt sets the stage for a frenzied Q4 push in disinvestment