Daniel Black

Daniel Black

EQT raised its offer for British testing and inspection group Intertek to an equity value of £8.9bn this week, and approximately £10.3bn including debt.

However, the FTSE 100 firm is set to reject the sweetened bid, according to Reuters and Bloomberg.

It’s a striking moment in a market where UK assets are increasingly seen as undervalued, and underscores how difficult it has become to take quality British businesses private, even at a substantial premium.

And in other news this week:

- Vodafone is buying out CK Hutchison’s stake in their merged UK operator for $5.8bn, taking full control of Britain’s largest mobile network.

- Santander is preparing to remove the TSB brand from British high streets after 215 years, ending a storied chapter in UK retail banking.

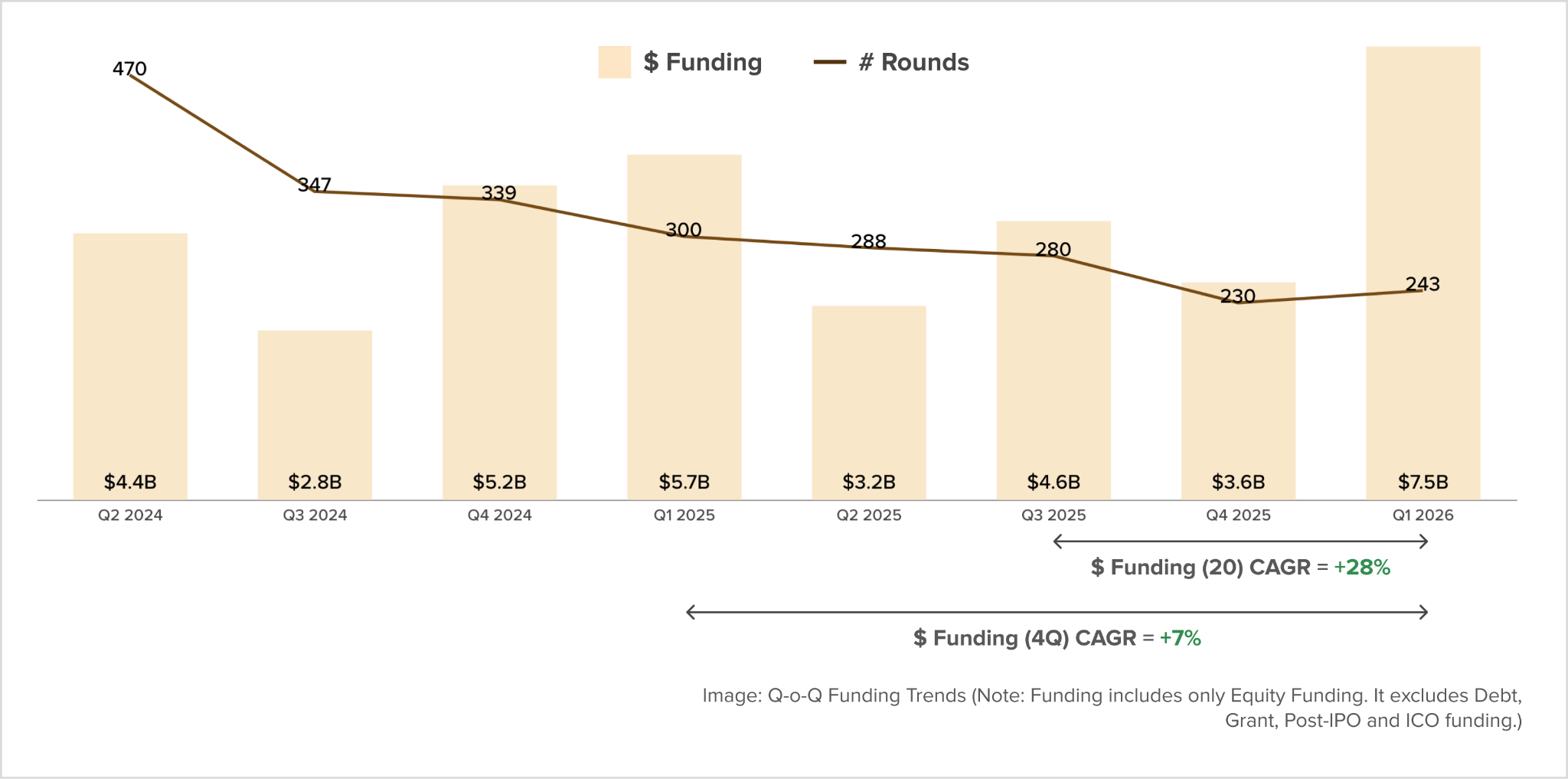

- UK tech funding hit $7.5bn in Q1, up 32% year-on-year and more than double Q4 2025, placing the UK second globally behind only the US.

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Bullish to acquire Equiniti for $4.2bn

- Workspace, pursued by Saba, weighs sale of prize London Office

- StanChart agrees to sell some card business to India lender Federal Bank ltd. in pullback

- Harbour’s tie-up with Waldorf cleared in court defeat for HMRC

- Intertek primed to reject EQT’s latest £10bn takeover bid

- Vodafone to buy out UK’s biggest operator for $5.8 Billion

- Standard Chartered to sell East African headquarters as footprint shrinks

- Aegon, Barclays Say Prepare for Market Pain

- Santander to remove TSB brand from British high streets after 215 years

- BP reviews UK North Sea assets as new CEO eyes disposals

- UK’s Capricorn Energy says deadline for takeover offer from Saudi’s Cafani unit extended

- HSBC’s corporate and institutional unit slips 12% as trading revenue declines

- Lazard to acquire private capital advisor and placement agent Campbell Lutyens for $575m

- York Space Systems to acquire ALL.SPACE

- Searchlight to invest in B2B events firm CloserStill Media

- Ansor-backed Complii to acquire Classic Lifts Scotland

Industry news

- Private equity firms face reckoning as £31bn broadband push turns sour

- A decade after Brexit, UK stocks are rebounding – but can it last? Bank of England holds interest rates but signals possible hikes as inflation rises

- UK long-term borrowing costs hit highest level since 1998

- Bank of England in stand-off with FCA over trading firms’ capital

Job moves

Market trends

Record capital, half the deals

KPMG’s Venture Pulse shows that venture capital financing into UK firms had a mixed start to the year. While $9.7 billion invested in Q1 eclipsed every quarter since early 2022, the deal count has contracted to fewer than 600 deals.

AI lifts the headline, but Europe’s funding pipeline is thinning

Crunchbase funding revealed that European venture funding reached $17.6bn in Q1 2026, up nearly 30% YoY and second consecutive quarter of growth, with AI accounting for more than half of total regional capital for the first time at $9.2bn.

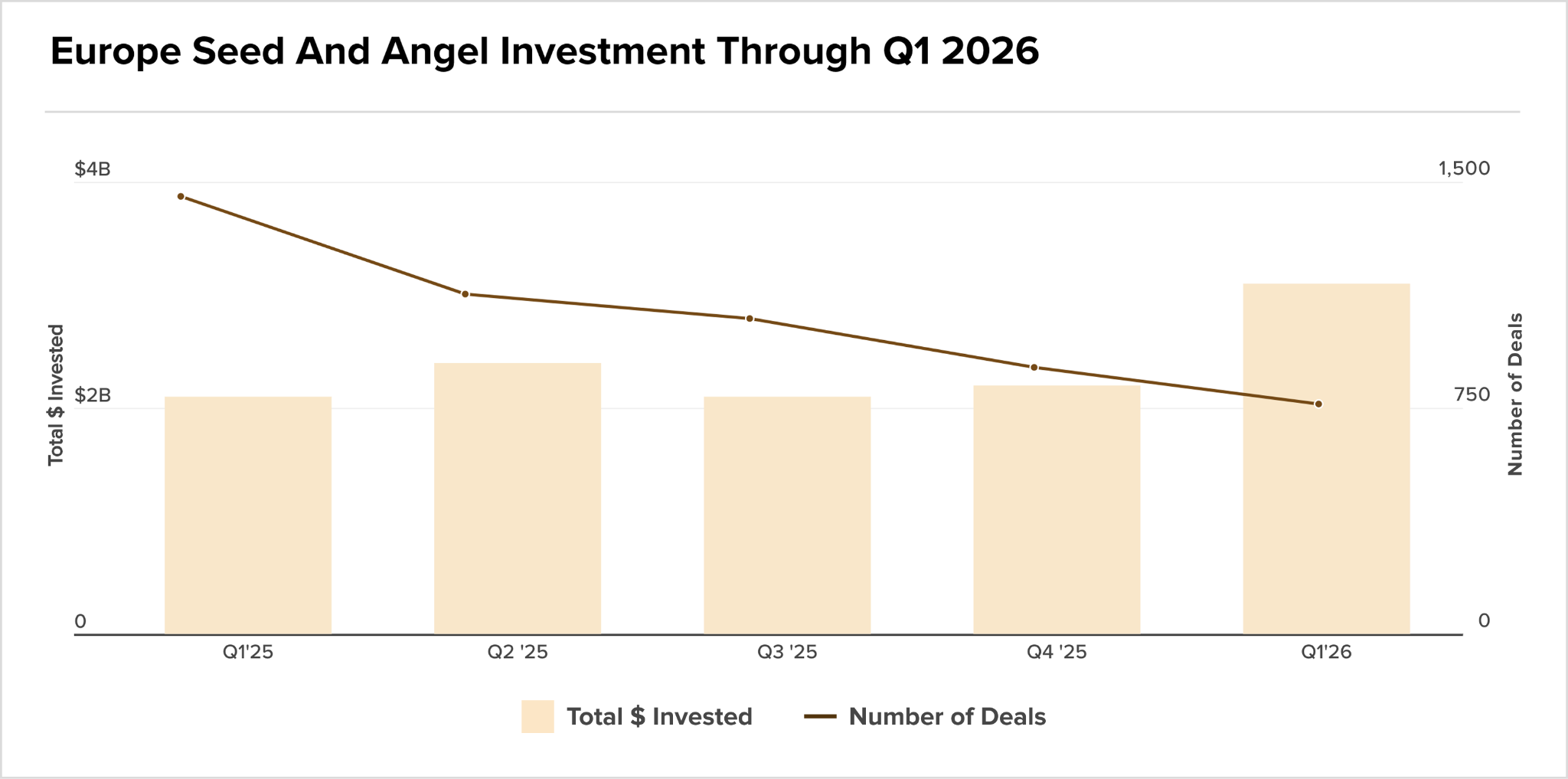

Seed and angel investment recorded $3.1bn in Q1 across around 790 deals. The 50% YoY increase in value is largely a function of Advanced Machine Intelligence’s $1bn round, the largest seed deal on European record.

The underlying trend is less constructive, since the deal count has shown a consistent decline in the past 12 months.

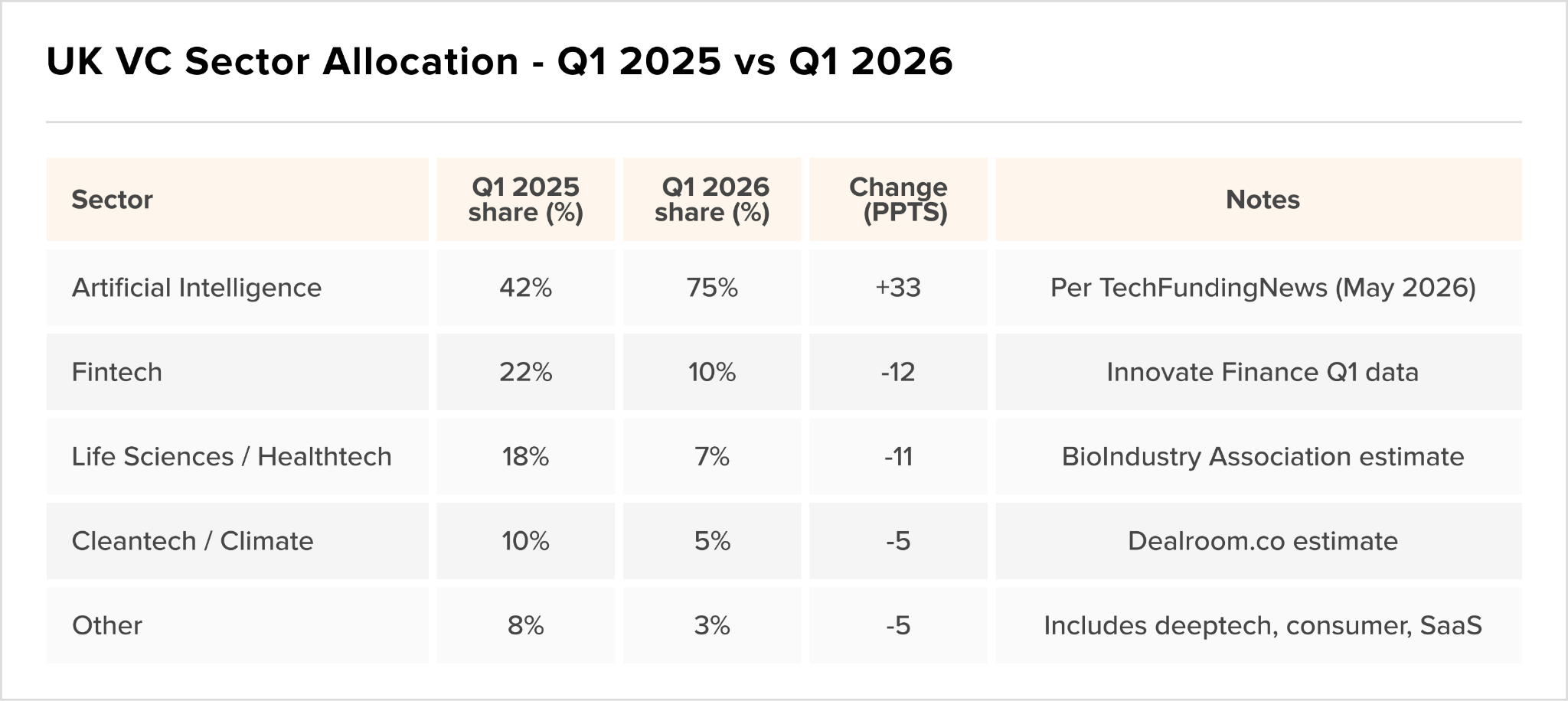

75% and climbing

The AI dominance visible at the European level is even more pronounced in the UK specifically. Three-quarters of all UK venture capital deployed in Q1 2026 went to AI startups. That 75% figure, up from 42% a year earlier, represents the highest single-sector concentration in UK VC in at least two decades.

Late-stage capital floods in as London tightens its grip

Tracxn’s UK Tech Q1 funding report puts the sector figure at $7.5bn, up 32% YoY and more than doubling Q4 2025’s $3.6bn, placing the UK second globally behind only the US. Meanwhile late-stage rounds absorbed $5.1bn, a 174% quarter-on-quarter surge, with 11 companies individually clearing $100m.

Capital is consolidating into a narrow set of proven platforms, predominantly in Enterprise Infrastructure and Auto Tech, where institutional investors are prioritising downside protection over optionality.

Exit activity contracted in volume but held on value, with total acquisitions falling 18% to 86 events against Mastercard’s $1.8bn acquisition of BVNK anchoring the quarter.

A single new unicorn, Allica Bank, reflects a valuation environment that remains disciplined rather than permissive. London’s 89% share of all inflows, at $6.7bn, confirms the structural gap between the capital and the rest of the UK tech ecosystem.