Daniel Black

Daniel Black

UK inflation and interest rates both dropped this week, bringing some welcome news just before the Christmas break. It’s the sixth rate cut in the past year, though it might be a while until we see the next one, according to reports.

In other notable news:

- The Daily Mail secured funding for its Telegraph buyout

- Coca-Cola’s sale of Costa Coffee has hit the rocks

- Shell’s M&A chief left after the CEO blocked a bid for BP

We’re now taking a break until the New Year. Many thanks for subscribing to Teaser UK and I hope you enjoy a restful holiday period.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Rothermere’s DMGT secures funding for Telegraph takeover

- Coca-Cola holds last-ditch talks in bid to salvage Costa Coffee sale

- AA and RAC private capital owners set to exit roadside recovery businesses

- KKR nears Viridor stake sale to Equitix

- Diageo to sell Kenyan drinks business to Japan’s Asahi in $2.3bn deal

- Insurers line up in £3bn sale of Aegon’s UK arm

- UK’s Aberdeen to acquire $2 billion of US closed-end assets

- UK’s Inocea Group eyes acquisition of Germany warship builder GNYK, source says

- UK’s Serica Energy to buy Southern North Sea assets for $76 million

- BC Partners to buy logistics platform Fortidia

- Doncasters said to pick banks for US IPO

- Spain’s Qualitas Energy nears deal for Cubico

- Shell mergers chief departed after CEO blocked bid for BP

Industry news

- Bank of England cuts interest rates to 3.75% in pre-Christmas boost for struggling economy

- UK inflation falls more than expected to 3.2% in November

- How UK real estate companies can repel private equity bargain hunters

- Recently appointed Esure chief executive decides to leave business

Salaries and bonuses

Job moves

- BP appoints first outsider as CEO after ousting Auchincloss

- Lloyd’s broker enters speciality market with senior appointment

Market trends

The bear awakens

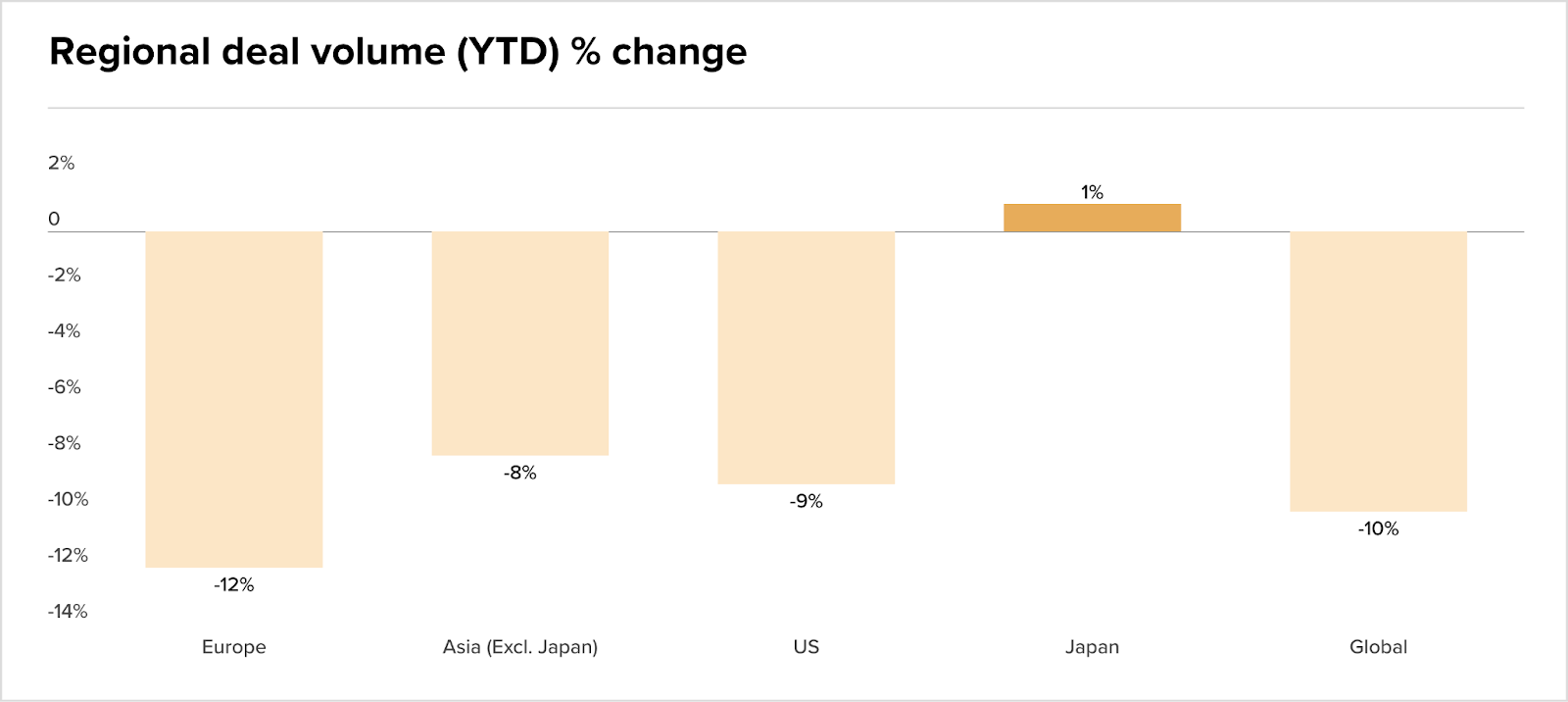

The M&A market continues searching for equilibrium in 2025, with YTD deal volumes down 10% on 2024 after Liberation Day volatility derailed initial momentum. While public markets remain bullish, this hasn’t translated into deal activity, with consistent declines across the US, Europe, and Asia.

However, DC Advisory notes that pressure on private equity to divest assets and deliver liquidity is creating an inevitable backlog, a dynamic expected to drive a predicted 15% increase in deal activity for 2026, finally coaxing the long-hibernating ‘M&A Bear’ from its cave.

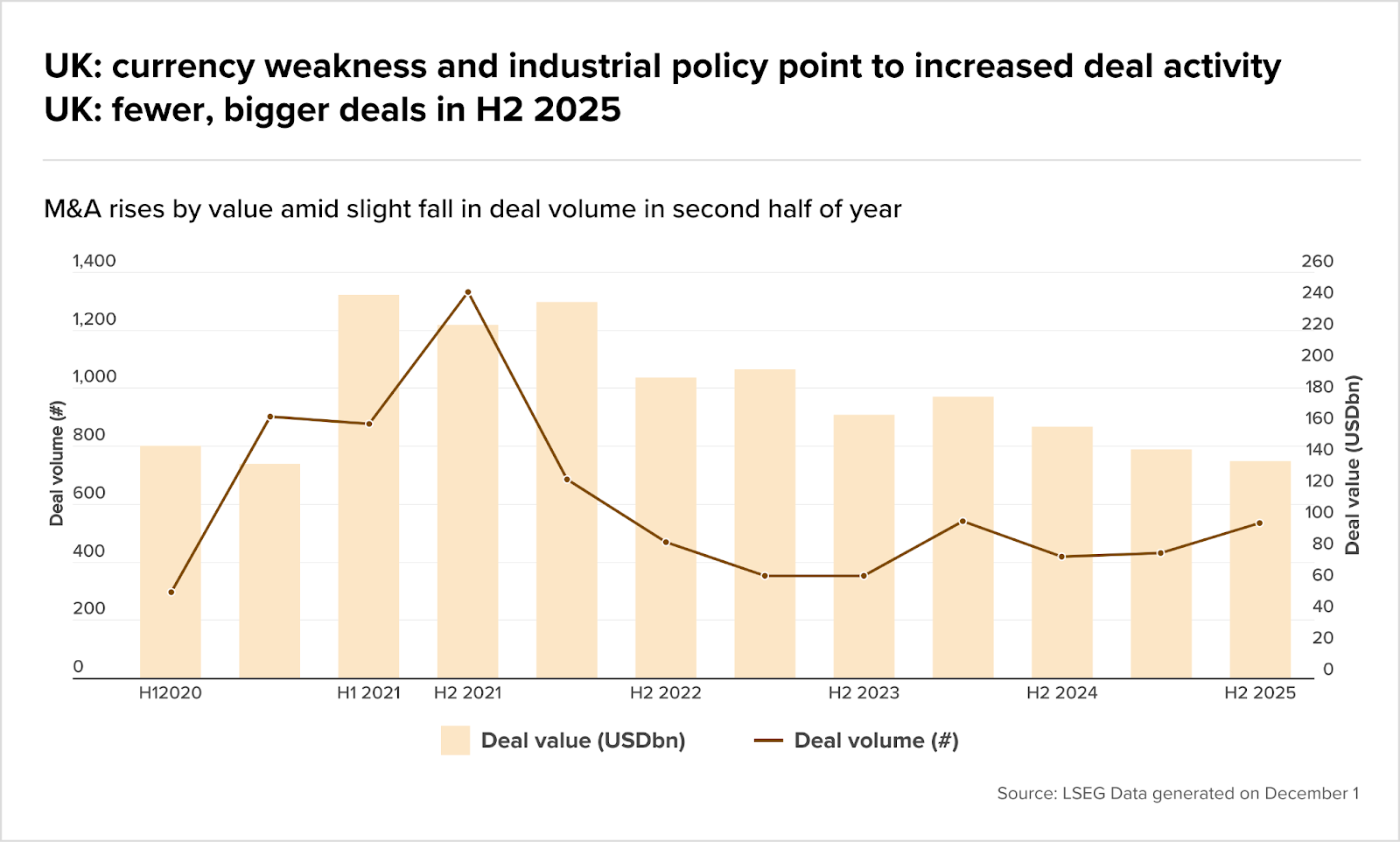

UK M&A has strong H2

UK M&A activity showed resilience in H2 2025, with deal value rising 38% in Q3 vs. Q2 despite a 16% drop in volume, creating 63% larger average transactions as financing conditions improved.

According to A&O Shearman, sterling’s weakness against the dollar, combined with strong FTSE 100 performance, attracted increased foreign buyer interest from the US, Middle East, and APAC, particularly in financial services, tech, and life sciences.

Activist investment surged dramatically, with the UK seeing a 44% YoY increase in targeted companies (from 36 to 52) led by US firms like Elliott Management and Trian Partners, focusing on board changes and break-up plays. Notable H2 IPOs, including Princes’ £1.16bn listing, signaled improving exit conditions for private equity sponsors heading into 2026.

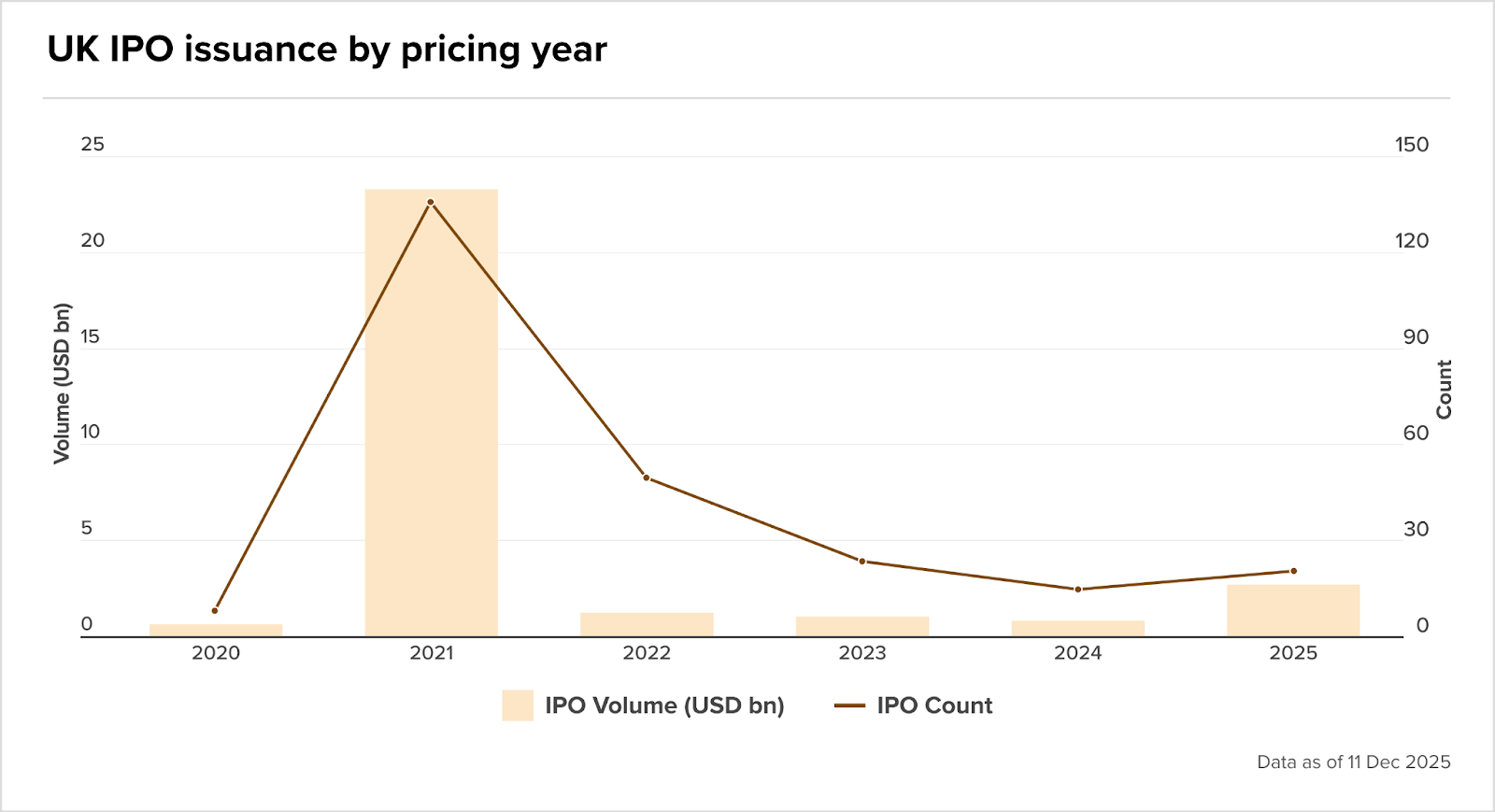

A smoother path for IPOs?

Building on these IPO developments, IonAnalytics reports that the UK’s new prospectus regime (effective 19 January 2026) allows companies to raise up to 75% of share capital via market announcements rather than full prospectuses.

While reforms aim to mirror US-style rapid capital-raising, dealmakers remain skeptical as pre-emption rights still require shareholder approvals beyond standard non-pre-emptive authority, leaving governance constraints largely unchanged.

Despite October 2025’s sizeable IPOs from Princes Group and Shawbrook boosting volumes to $2.8bn (up from $950m in 2024), participants note that reputational risk and transparency demands will likely offset time saved, with market conditions, not regulatory changes, ultimately determining whether London’s 2026 pipeline delivers sustained recovery.

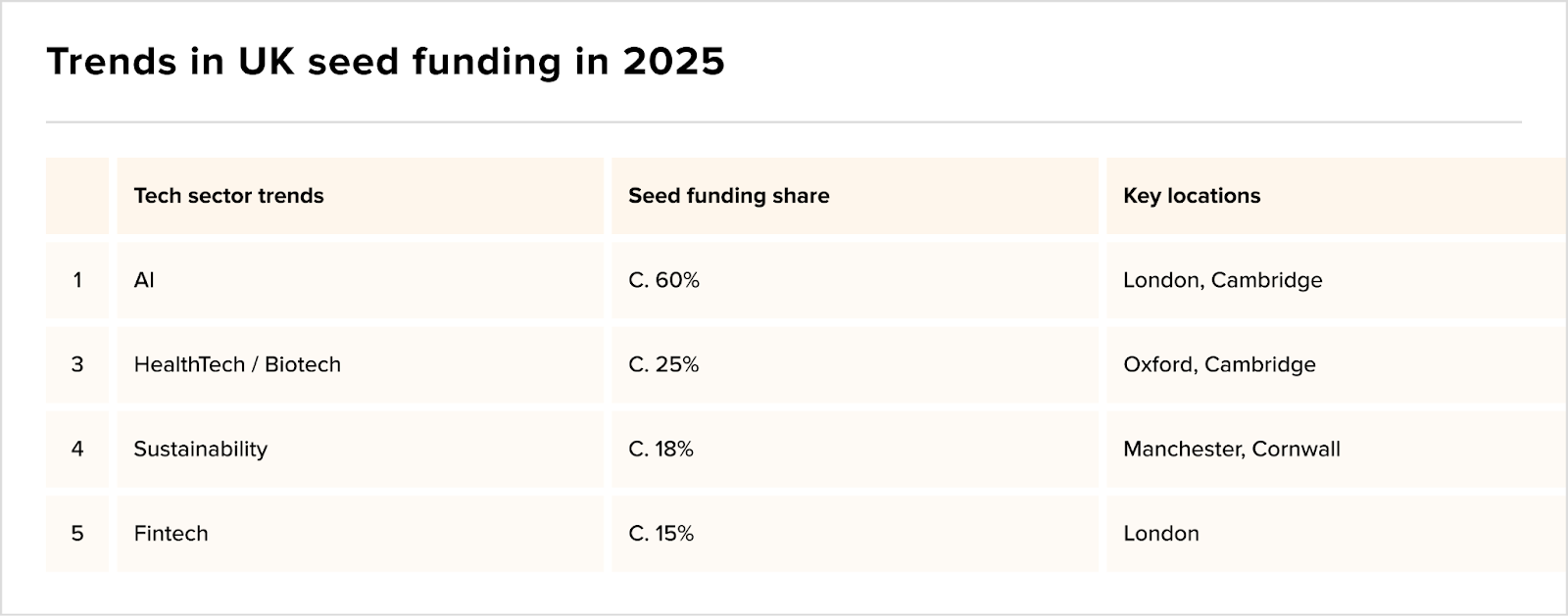

AI takes lion’s share of UK fundraising

UK seed funding demonstrated robust activity in 2025, with 1,604 early-stage companies securing £1.8bn in inaugural investments. Beauhurst’s 2026 Predictions highlight that AI dominated over 60% of deals, evolving from hype to practical deployment across fertility therapeutics (OvartiX), surgical software (VitVio), and freight optimization (Nexcade AI), with London and Cambridge’s “Silicon Fen” leading integration.

Health tech captured nearly 25% of funding, positioning the UK as Europe’s biotech epicenter through innovations in RNA platforms and AI-driven diagnostics.

IPOs

- Will 2026 see swathe of IPOs as the consolidation of consolidators well runs dry?

- Revolut chief casts more doubt on London IPO