Daniel Black

Daniel Black

The details of McCormick’s deal with Unilever were made public this week, with the merger valued at a rather spicy $44.8bn.

While Unilever will control 65% of the new spin-off, it will be called McCormick and will be led by the US firm’s executives. The deal is forecast to result in $600m in annual savings by the end of the third year.

And in other news this week:

- The AA has attracted interest from EQT as it prepares a £5bn sale

- BlackRock is considering HSBC’s Canary Wharf tower for its London HQ

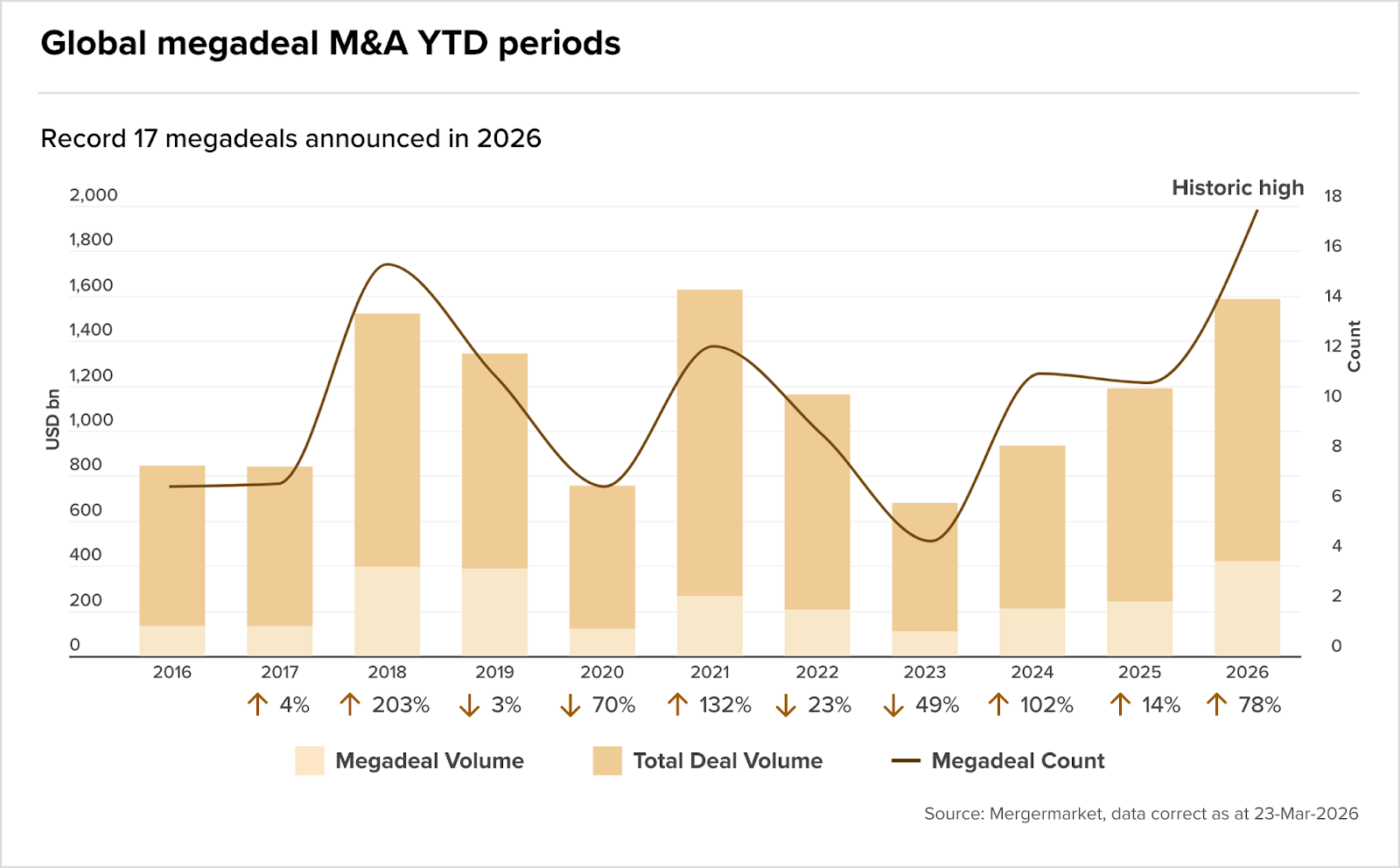

- It’s been a record Q1 for global megadeals

Thanks for reading, and connect with me on LinkedIn if you want to discuss how Ideals can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- McCormick agrees to acquire Unilever Food Arm in $44.8bn merger as Unilever’s stock wipeout deepens

- AA attracts interest from EQT as it prepares for £5bn sale

- UK watchdog probes $3.4bn Suzano and Kimberly-Clark deal

- Clarke enters agreement of $1.1bn to acquire Ravelin

- Blackstone in advanced talks for UK aerospace supplier Senior

- Apollo funds to acquire UK-based Gatehouse Living from Gatehouse Bank

- ABF’s Hovis takeover clears Britain review, flagged in Northern Ireland

- New BP CEO starts in fresh bid to revive embattled oil giant

- Apollo-Backed Athora to move to UK from Bermuda after buying PIC

- Howden launches IAL arm as acquisition announced

- Peel Hunt to top £140m in revenue despite UK IPO slump

- Algebris eyes UK growth: ‘We can do a lot more’

- UK investment bank Cavendish to post £56m revenue despite London IPO dearth

- BlackRock looks at HSBC’s Canary Wharf tower for new London HQ

- British neobank Zopa eyes acquisitions for European expansion

- Diageo Unit Investor Wants Asahi Kenya Offer Made to All Owners

Industry news

- Santander plans SRTs on UK, US loans amid acquisition spree

- Will the Iran War push the UK economy into a recession?

- UK firms plan to raise prices faster as Iran war hits costs; Trump sends European stock markets sliding

Salaries and bonuses

- Top investment bankers lose lucrative allowances as bonuses jump

- Maven Securities hikes average staff pay 46% after revenue jump

- Jefferies has more top bankers in London, but it’s paying them less

Job moves

- Cavendish looks to hire ‘good people’ as tough market frees up talent

- Alantra hires dealmaker Burton to bolster tech coverage in London

- Morgan Stanley shifts dealmaker Luehrs to lead European private credit

- Standard Chartered hires Citigroup’s Metzger as global head of coverage

- HSBC poaches BBVA executive to run Swiss private bank

- Linklaters promotes 37 partners in expanded round. Here are the names

- Aberdeen’s failure to find a chairman blamed on bad luck and competition

Market trends

Megadeals set a new benchmark

Global dealmaking opened 2026 at a register not seen in years. Seventeen megadeals announced in the year to date marks a historic high, with total deal volume up 78% on the same period in 2025, driven overwhelmingly by concentrated bets on artificial intelligence, as recorded by Mergermarket.

OpenAI’s $110bn raise, Anthropic’s $30bn round and xAI’s $20bn funding collectively anchored the quarter’s top 10, alongside power infrastructure plays reflecting the energy demands that AI computation now places on the grid.

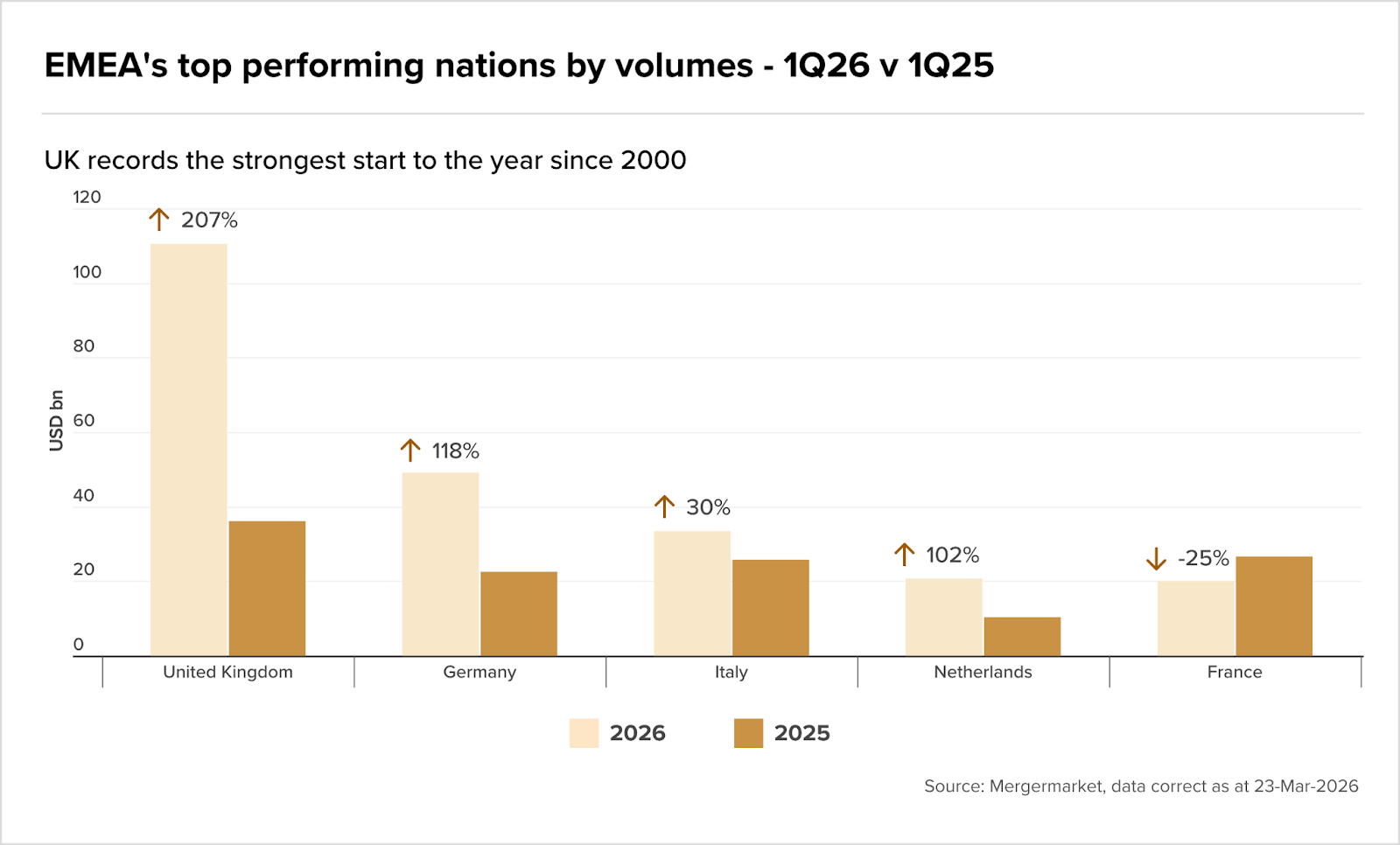

That strength carried into EMEA, where the UK recorded its strongest start to a year since 2000, with deal volume reaching $110bn in Q1, up 207% on the same period in 2025. Two blockbuster transactions account for the bulk of that figure, and stripping those out, volumes track broadly in line with the preceding two quarters.

Germany placed second at $49.2bn, largely on the back of UniCredit’s approach for Commerzbank, though rising energy costs continue to weigh on its Mittelstand industrial base. France was the only top-five EMEA market to record a year-on-year decline, down 25%, a reminder that volume leadership across the region remains concentrated rather than broad-based.

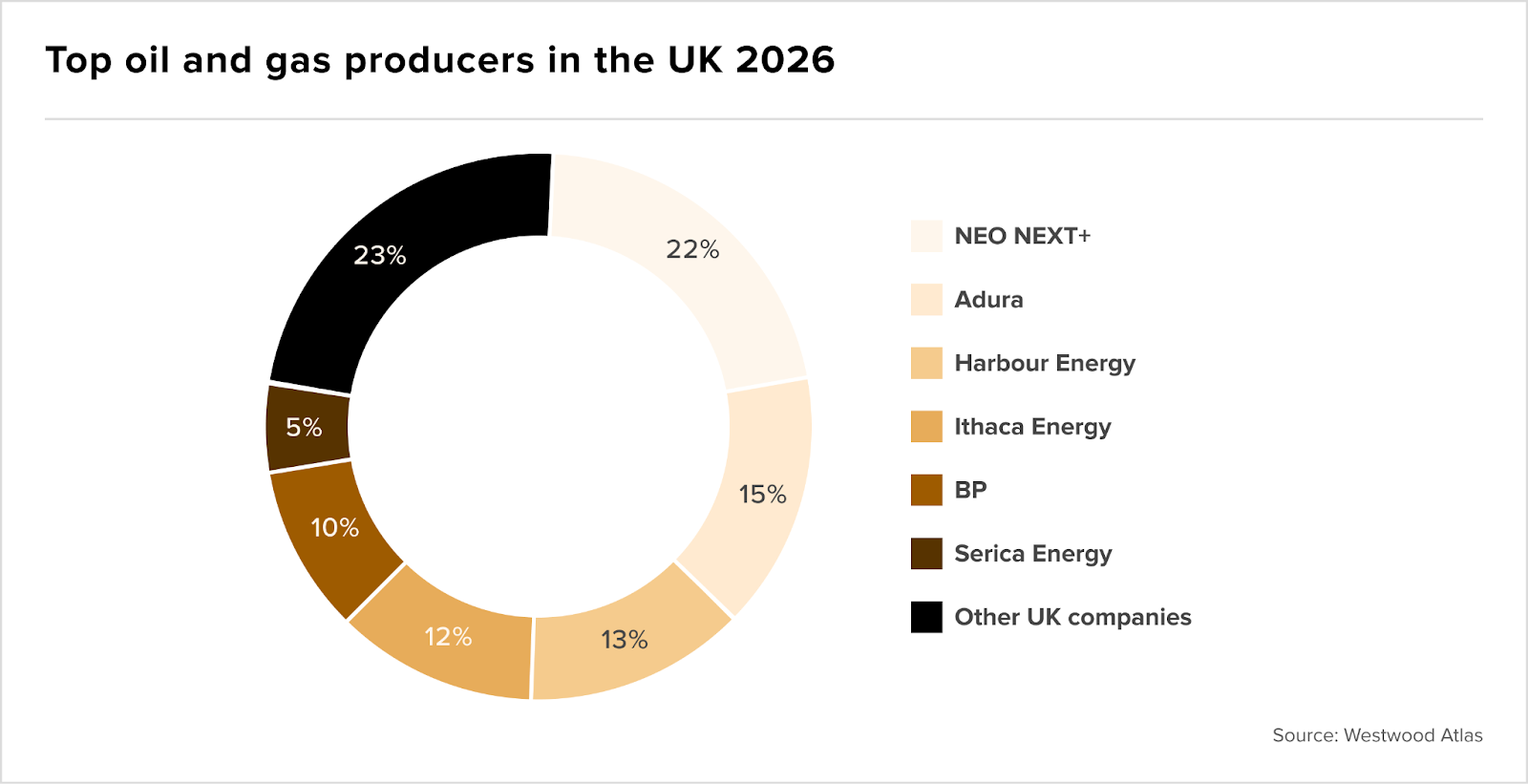

Independents inherit the basin

The North Sea’s ownership map has been redrawn almost entirely over the past decade. The completion of the NEO NEXT and TotalEnergies UK merger on 30 March, forming NEO NEXT+, leaves a UK-focused independent accounting for 22% of total 2026 basin production. In 2014, the five largest holders of UKCS reserves were all Majors. Today, only BP remains in the top six, its peers having retreated from 52% to 16% of reserves as the Energy Profits Levy and shifting capital priorities pushed investment elsewhere.

According to Westwood Energy, the number of companies holding UKCS reserves has fallen from 74 to 34 since 2014, with the top six now controlling 80% of what remains. BP, absent from recent deal activity despite holding a steady share of reserves, is the one constant in a basin thoroughly reshaped by private equity-backed independents moving in as the Majors moved out.

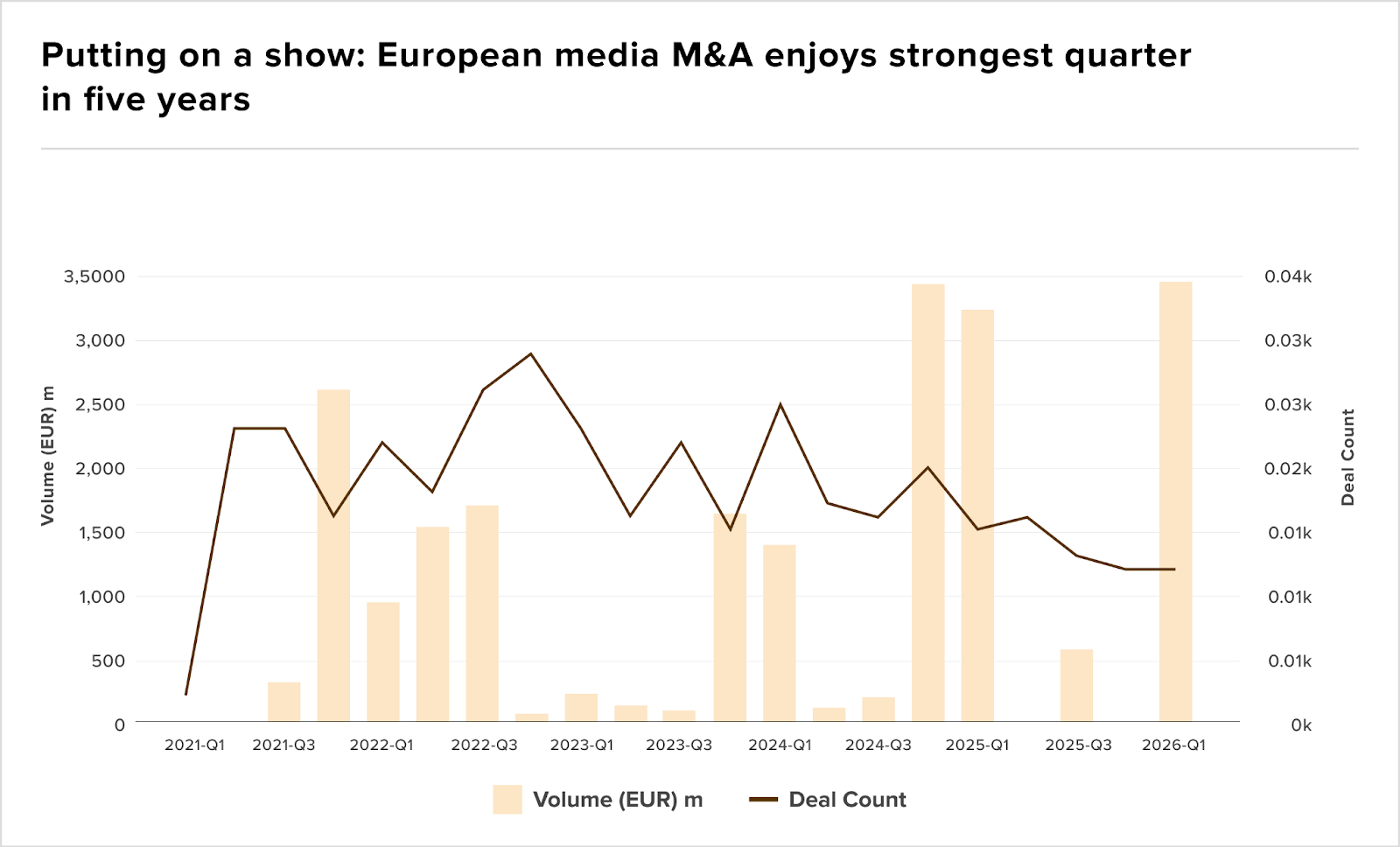

Content race heats up

European media M&A has found its footing in 2026, with Banijay’s tie-up with UK’s All3Media and Mediawan’s acquisition of North Road’s parent driving audiovisual deal volumes to EUR 3.44bn in Q1, the sector’s strongest quarter in five years, according to Mergermarket.

The consolidation now puts ITV Studios in sharper focus as an obvious next move. Subscale relative to its newly enlarged continental peers and attached to a linear broadcast business under pressure, the Studios arm looks like a natural acquisition target.

Comcast’s reported interest in ITV M&E may yet broaden into a full-group approach, with EUR 800m of firepower sitting on Banijay’s balance sheet as a reminder that the consolidation cycle is far from over.

Fundraising

- Hedge fund Kite Lake raises $700m and closes to new cash

- Inflexion raises €4.5bn for buyout fund in just six months

IPOs

.