Daniel Black

Daniel Black

The UK is on sale. US ingredients giant Ingredion made a £2.7bn bid for Tate & Lyle this week, adding another iconic UK name to a foreign M&A pipeline that has now hit $192bn in announced deals – more than triple this point last year, according to LSEG data.

US acquirers alone are driving over half of inbound volume, drawn by FTSE valuations that have looked cheap for the better part of a decade. Britain’s discount, in other words, is finally being arbitraged at scale.

And in other news this week:

- Spire Healthcare received a £1bn takeover proposal from Toscafund, adding another listed UK target to the take-private pipeline.

- Anglo American agreed a $3.9bn sale of its Australia coal business as the group continues its strategic reshape.

- Standard Chartered is set to cut thousands of back-office jobs as part of a wider AI-driven restructuring.

Thanks for reading, and connect with me on LinkedIn if you want to discuss how Ideals VDR can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- London’s Global Healthcare Opportunities and Asia’s CBC Group to merge creating investment giant

- Revolut has big plans for its ex-HSBC private bankers

- Revolut develops private bank as more euro firms pursue wealth management

- British theatre group ATG Entertainment readied for sale

- Medtronic announces intent to acquire SPR Therapeutics

- Citi strikes €15bn partnership with BlackRock for private European lending

- Space stock craze comes to Europe as one UK Fund Quadruples

- Anglo American strikes $3.9bn deal to sell Australia coal business

- Tate & Lyle shares leap after £2.7bn Ingredion takeover bid

- Spire Healthcare shares soar on £1bn takeover offer

- London’s Spire Healthcare gets $1.35bn buyout proposal from Toscafund

- Impax sees revenue drop as ESG investor keeps focus on costs

- Fenchurch, Ardea score roles as private equity-backed wealth firm AFH explores sale

- Triton to exit healthcare provider Aleris in strategic sale

- Ansor-backed Complii to acquire the Escalator Company

Industry news

- UK Inflation Falls Unexpectedly, Lowering Chances of a BoE Rate Hike

- Why London’s private and public sectors need to work together to unlock investment

- Macro hedge fund Caxton opens India office

- US trading firm Susquehanna more than triples London office space

- Years after LSEG drama, Chris Hohn’s TCI makes a new exchange bet

Salaries and bonuses

- Pay for hedge fund portfolio managers vs. long-only PMs in London

- Ex-Goldman Sachs bankers’ boutique Ardea hikes UK pay after hiring spree

Job moves

- HSBC hired a new cloud CTO from Citi as AI layoffs loom

- HSBC’s private bank names Werner to senior UK role

- One London hedge fund cut jobs after March. The rest are wary of making big UK government bond bets

- Citigroup hires JPMorgan’s Chuka Umunna in UK dealmaking push

- Moelis hires Lazard’s Knott to bolster London chemicals coverage

- Standard Chartered chooses Costello as new CFO

- Standard Chartered to cut thousands of back office jobs in AI push

- Rothschild & Co hires UBS’s Hall in investor advisory push

- Deloitte UK aims to move hundreds of juniors into AI audits

- Freshfields names London private capital co-head as new UK boss

- Investment Association names EY’s John Owen as next CEO

- Standard Chartered already cut 88% of one team, but these jobs look safe

Market trends

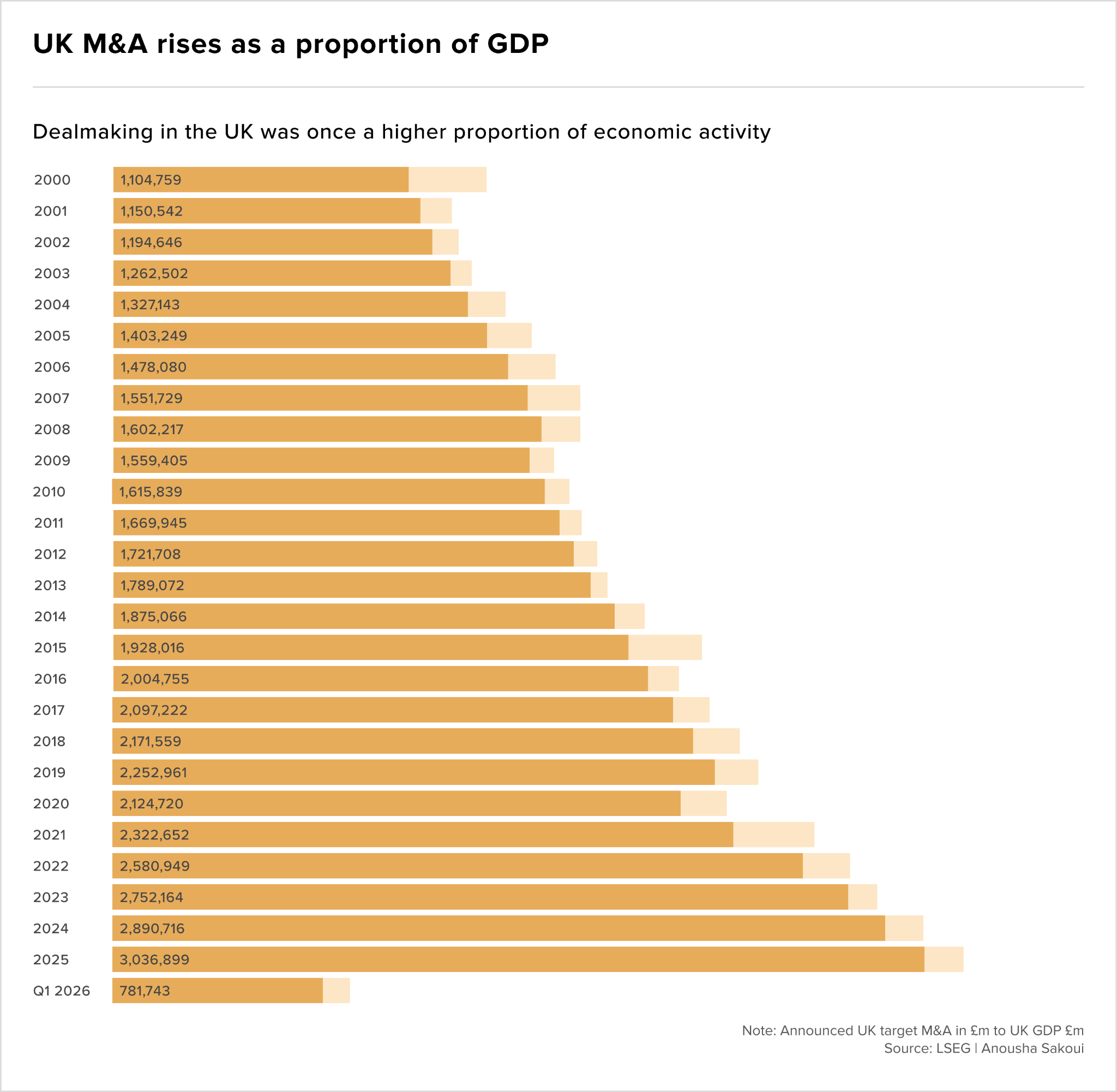

UK on sale

The UK is the world’s most haunted market right now, and foreign buyers aren’t done yet. $192 billion in announced deals by mid-May, more than triple the figure from this point last year, with US acquirers alone driving more than half of inbound volume.

According to LSEG data reported by Reuters, UK M&A accounted for 14% of UK GDP in Q1 2026 alone, up from just 5% across all of 2025. The FTSE 100’s persistent discount to US and European peers has turned Britain into a clearance aisle for global strategics and private equity alike.

Intertek, Schroders, Tate & Lyle: these aren’t distressed assets. They’re well-run, globally relevant businesses trading at prices that would have looked impossible five years ago.

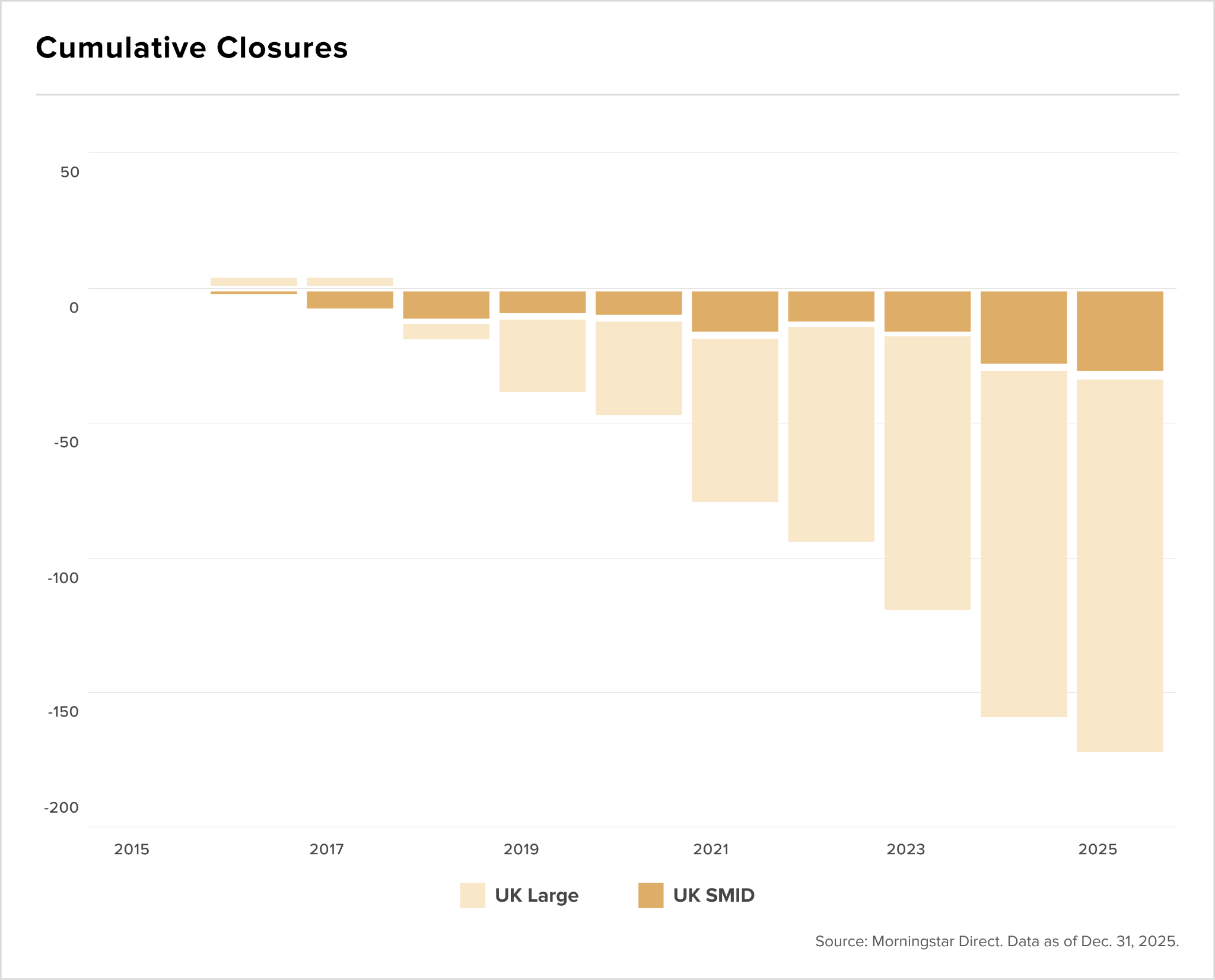

The exodus that built opportunity

To understand why the UK got here, you have to follow the money backwards. Since 2016, UK equity funds have bled over $160 billion in cumulative net outflows, and around 380 UK equity strategies have closed against just over 200 new launches, according to Morningstar Direct.

Active managers at Columbia Threadneedle, Jupiter, Liontrust, and Schroders bore the brunt. The winners were passive providers: iShares and Vanguard now control nearly half of all UK equity index money, up from 22% a decade ago.

That capital flight compressed valuations to levels that now look anomalous relative to global peers, particularly in large caps. The irony is sharp. The same outflows that battered domestic confidence are precisely what made UK assets irresistible to foreign buyers.

The SMID segment, meanwhile, remains largely ignored, delivering near-zero total return over five years while large caps outperformed. That gap hasn’t closed, and it’s quietly becoming a dealmaking conversation of its own.

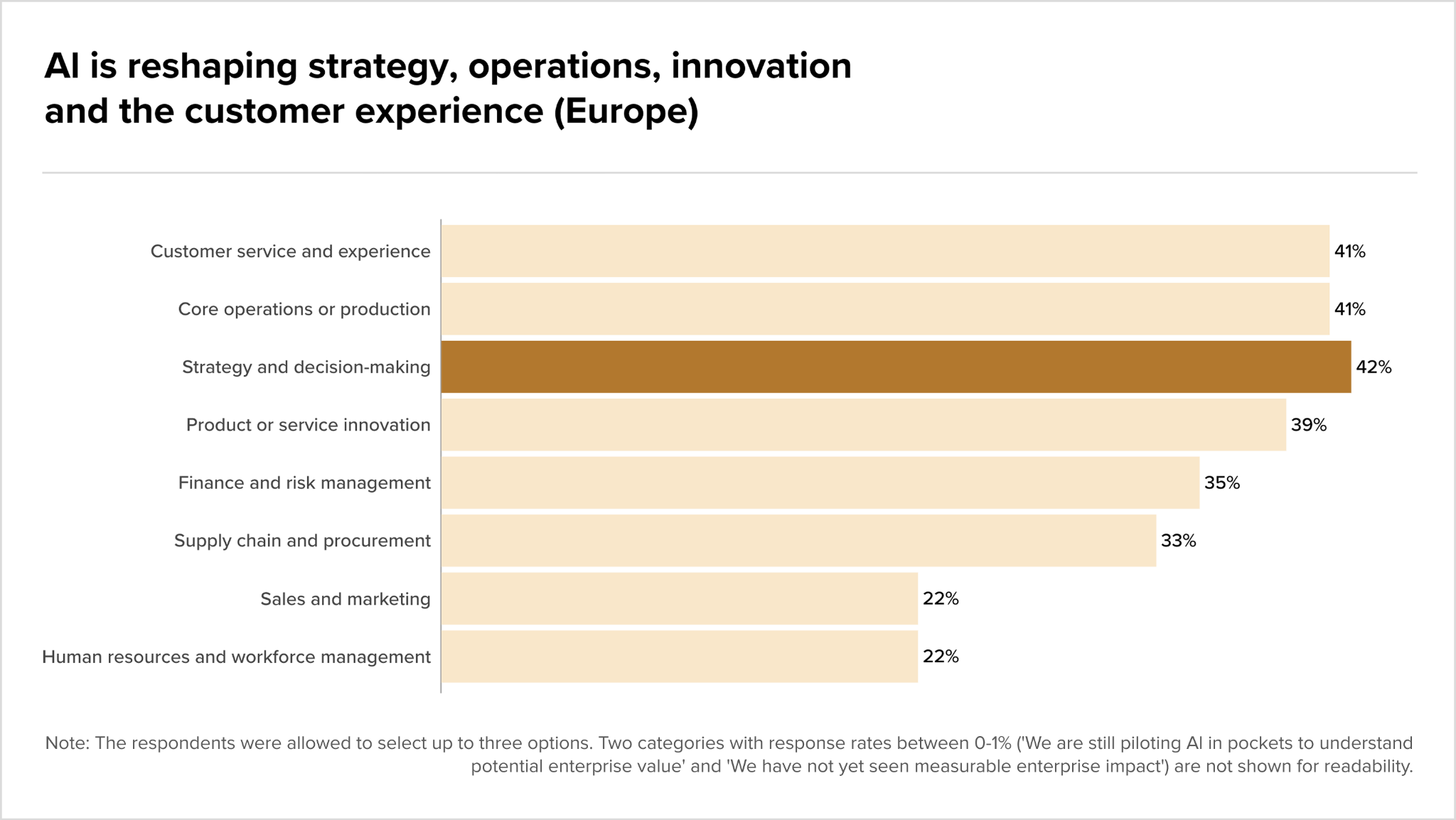

Buying the Machine: AI as the new M&A thesis

Foreign acquirers aren’t only buying cheap assets. Increasingly, they’re buying transformation capacity. EY’s latest pulse check on global CEO sentiment found AI already registering measurable impact across European enterprises in strategy and decision-making (42%), core operations (41%), and customer experience (41%).

These aren’t pilot programmes sitting in an innovation lab. They’re live capabilities embedded in how businesses actually run. For US strategics in particular, acquiring a UK company that has already built AI into its operational core compresses years of internal development into a single transaction.

That fundamentally shifts the acquisition thesis. You’re not just buying revenue or market share, you’re buying a functioning AI-enabled operating model at a FTSE discount. That’s a compelling pitch to any deal committee.

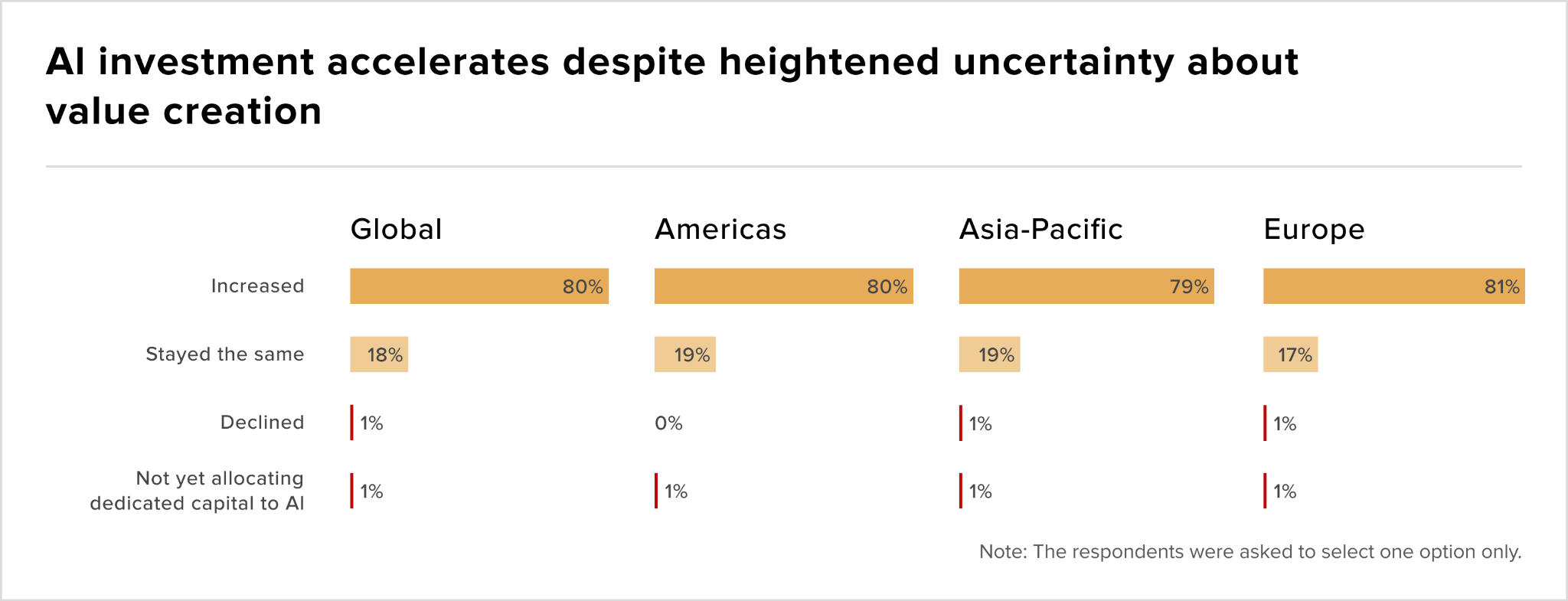

The capital behind this isn’t slowing. Across Europe, 81% of CEOs increased planned AI investment for 2026 versus 2025, the highest regional figure globally. What’s striking is that this acceleration is happening despite widespread uncertainty about whether the returns will actually materialise.

CEOs aren’t waiting for proof of ROI before writing the cheques. They’re treating AI as a structural lever, not a discretionary line item.

For the M&A market, that creates a specific dynamic: companies that can demonstrate measurable AI-driven improvements in margins, operations, or customer metrics will command premiums in any sale process. Those that can’t are increasingly vulnerable to acquirers who believe they can extract that value themselves post-close.

Expect AI diligence to become as standard as a financial audit in UK deal processes over the next 12 months.

IPOs