Daniel Black

Daniel Black

Apollo made a £1.5bn bid for London-listed Bodycote this week, taking another well-known UK industrial name into US private equity’s crosshairs, according to the FT.

But the inbound wave is hitting friction – US activist Ancora is urging H.B. Fuller to drop its £600m-plus bid for UK medical adhesives group AMS, the first notable pushback to come from a US shareholder rather than a UK board.

Britain is still on sale, but for the first time this year, the question of whether US firms can afford to keep buying is being asked back home.

And in other news this week:

- BP ousted its long-serving chair Albert Manifold over governance and conduct issues, throwing fresh uncertainty into the major’s strategic reset

- Belgian gunmaker FN Browning agreed to buy a UK sniper-rifle manufacturer in a rare cross-border defence deal

- A.S. Watson, owner of Superdrug, is pressing ahead with a $30bn dual listing despite the volatile equity backdrop

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Your favorite AI meets Ideals VDR

Ideals VDR has launched its new MCP – a secure bridge that connects Claude, ChatGPT and Microsoft Copilot directly to the data room.

Dealmakers can now run an entire project, from due diligence to signing, through whichever AI tool their team already uses. Folder setup, document review, Q&A and bidder activity tracking all happen via natural-language prompts.

Every action stays within existing permissions and is captured in a full audit trail – the deal moves at the speed of conversation, while sensitive data stays exactly where it belongs.

Visit the Ideals website to see how it works.

Deal Tracker

Our weekly roundup of confirmed M&A deals in the UK.

The rumour mill

- UK software investor Hg strikes first buyout deal since SaaSpocalypse

- Activist Ancora pushes H.B. Fuller to drop bid for UK’s AMS

- H.B. Fuller said to bid over £600m for UK’s AMS

- Belgian gunmaker FN Browning to buy UK sniper producer

- Canadian firm weighs bid for U.K. broadband company KCom

- UK would block Indian billionaire raising BT stake

- Italian bank CDP to raise stake in payments group Nexi after CVC weighs bid

- Apollo makes £1.5bn bid for London-listed Bodycote

- Gresham House inks conditional deal to buy 480-MW BESS project in UK

- CVC consortium launches €10.9bn offer for Italian drugmaker Recordati

- Morrisons blames UK government policy for shutting 100 lossmaking stores

- Hg invests $500m in Rightsline

- AtlasEdge gets €1.2bn in loans for European data centers

- Permira agrees to A$3.4bn exit from I-MED Radiology

- Bowmark, Bridgepoint to sell Helio Intelligence to ECl

- BP Share Price: What’s Next After the Chairman’s Shock Exit?

- BP ousts Chair Albert Manifold citing governance and conduct issues

- Halifax and TSB have outlived their brand-name usefulness

- Hedge fund Brevan Howard’s equities business is thriving despite something unusual

Industry news

- UK Corporate bonds are opening up to retail investors – But are the risks worth It?

- UK’s ex-PM Blair calls on Labour to focus on policy, not personality

- Reeves urges ministers to ‘buy British’ in critical sectors

- Financial reforms set to give £1.6bn boost to City of London

- UK borrowing rises and retail sales slide in April

- UK retail sales drop by most in nearly a year as drivers buy less fuel

- UK inflation falls unexpectedly, lowering chances of a BoE rate hike

- Badly behaving London bankers can no longer resign immediately and get a new job

- Julius Baer UK CEO: AI is not a threat to wealth management

- London currency broker Halo Financial files for administration

Salaries and bonuses

Job moves

Market trends

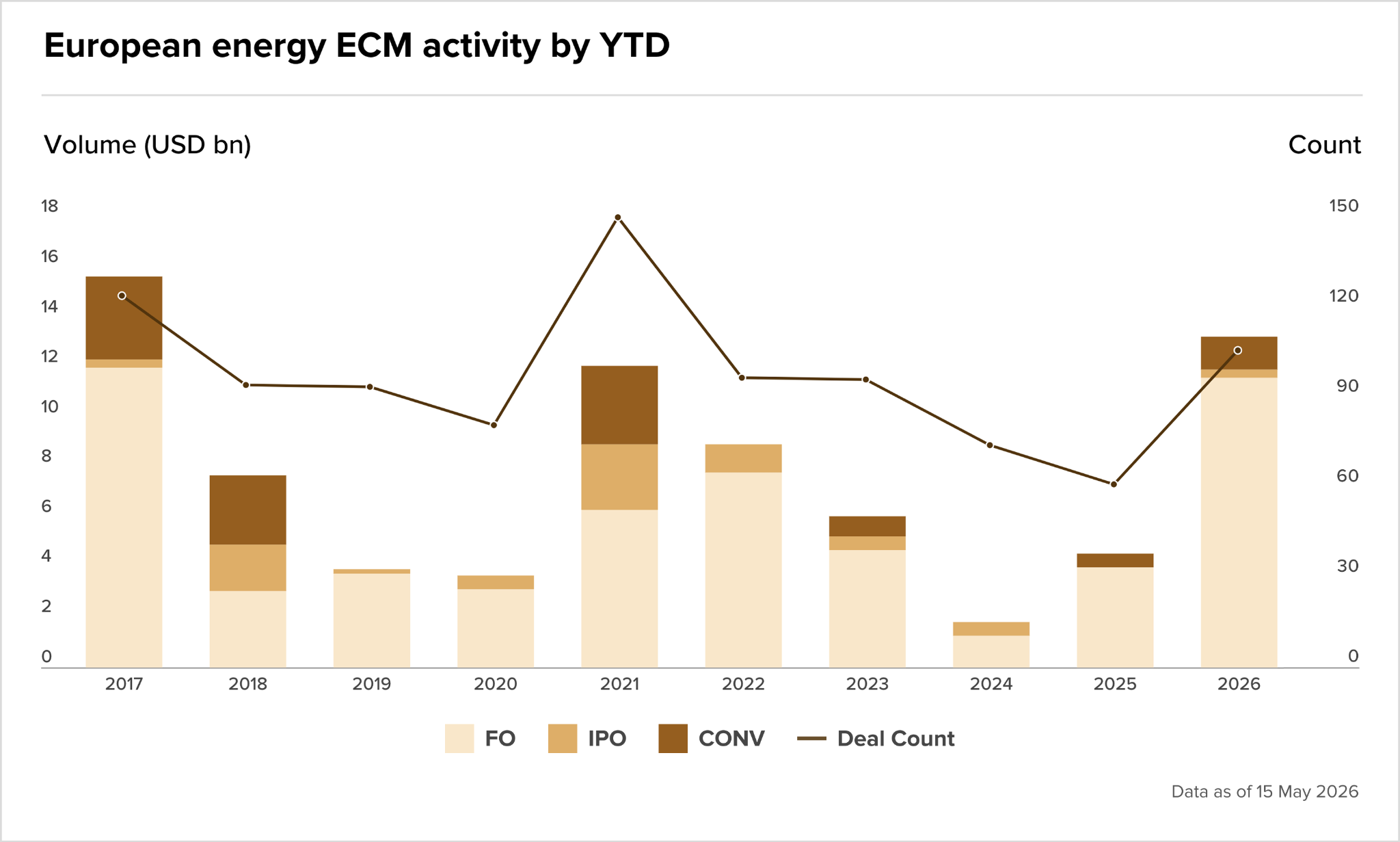

Conviction over volume

According to Dealogic data, European energy ECM issuance has already hit $12.9bn across 104 transactions year-to-date, the strongest start since 2017, pulling sharply away from a broader market that’s spent most of the year absorbing geopolitical shocks.

Two forces are compressing into one trade: AI infrastructure demands enormous and reliable power, turning European utilities into growth stories; and a second energy supply shock in four years has hardened security of supply from a policy talking point into a capital allocation priority.

Those two narratives used to be separate. In 2026, they’re the same deal.

IFR’s ECM Pulse reported that CVC’s EUR 1.2bn anchor into PPC’s capital raise needed less than an hour to be covered across its full size. When a sponsor of that scale moves that aggressively, institutional money follows, and that dynamic is now repeating itself across European energy equity.

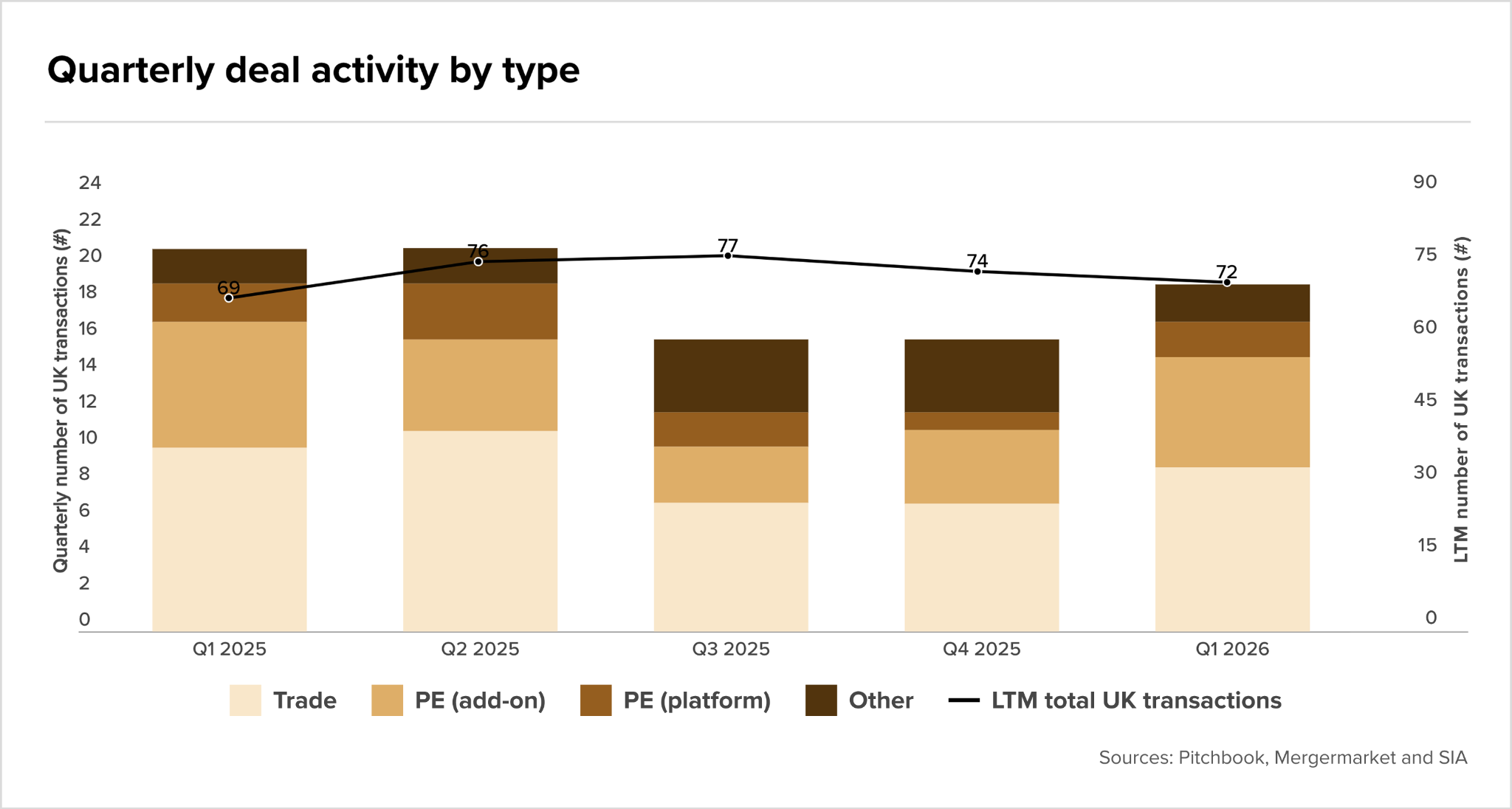

Stability in UK recruitment M&A

RSM’s Q1 2026 sector update, drawing on Pitchbook and Mergermarket data, puts 19 deals in the quarter, exactly in line with the 2025 quarterly average.

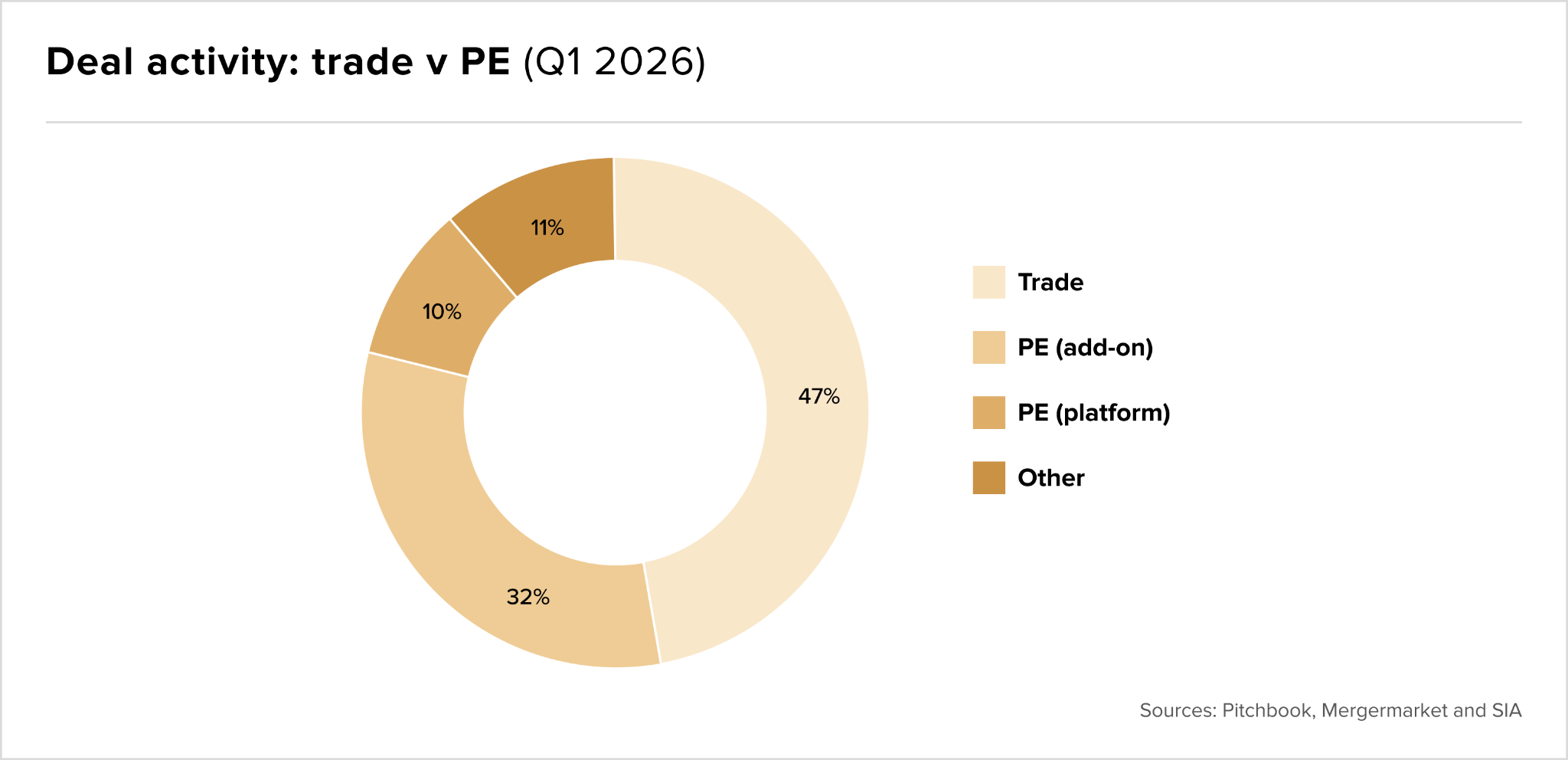

What this number doesn’t show is how sharply the composition of activity has shifted. Trade buyers have re-emerged as the dominant force. PE platform creation is nearly absent. Add-on acquisitions are now carrying the bulk of whatever private equity activity there is.

The market isn’t slowing, it’s sorting itself. Buyers are far more deliberate about which assets they pursue, and the deals clearing are the ones where quality, specialism, and growth trajectory are genuinely hard to argue with.

Trade buyers took 47% of Q1 deals; PE, in all its forms, accounted for 42%. That near-parity sounds balanced. It isn’t. Three-quarters of PE’s Q1 activity came through bolt-ons to existing platforms rather than fresh capital going into new businesses. PE isn’t hunting right now. It’s consolidating.

For sellers, that distinction matters more than the headline split. New platform deals are still happening, with Southfield Capital’s $100m acquisition of Metric Search being the standout, but they require a specific profile: US-market exposure, a senior-hire or specialist consulting model, and the kind of growth trajectory that justifies a premium in a cautious environment.

IPOs