Daniel Black

Daniel Black

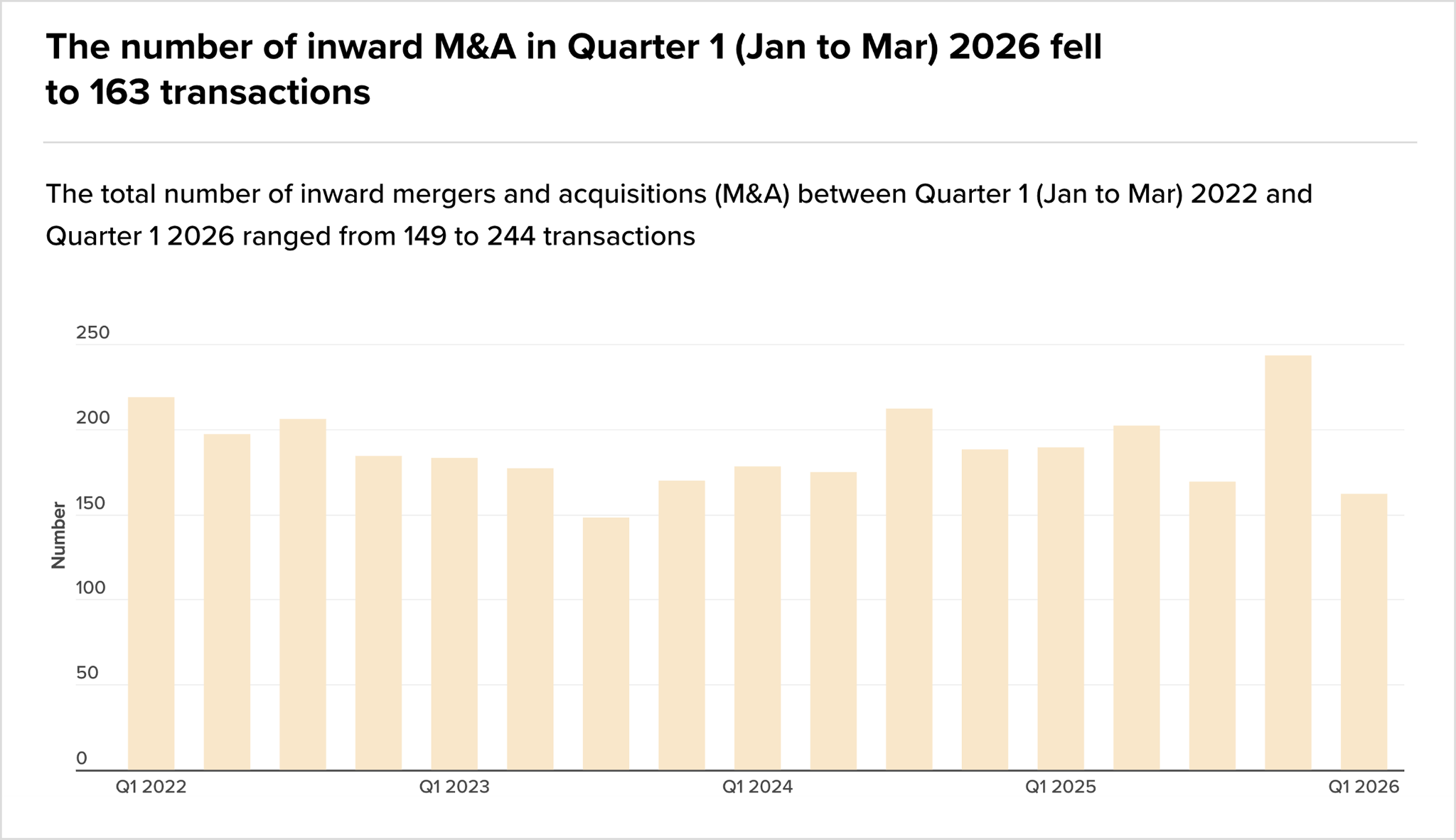

For all the foreign-buyer headlines of recent weeks, the official numbers tell a different story. UK inward M&A value fell from £33bn in Q4 2025 to just £14.2bn in Q1 2026 – the sharpest quarterly drop in the ONS dataset. Deal count slid from 244 to 163 over the same period.

The take-private wave hasn’t ended, but it’s running against a backdrop of overall foreign activity that quietly contracted in Q1, and RSM UK warns Q2 could be worse if Middle East tensions don’t resolve.

And in other news this week:

- BP held talks about selling £2bn of UK North Sea assets to Ithaca, in a major reshape of the oil major’s domestic portfolio.

- Top UK building societies are plotting bids for digital bank Atom, the latest sign of consolidation pressure in UK fintech.

- Milbank pushed new lawyer pay to $235k, intensifying the City legal pay war.

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of confirmed M&A deals in the UK.

The rumour mill

- Siemens Energy agrees deal for digital grid outfit Camlin Group

- Drax agrees £548m acquisition of Bluefield Solar Income Fund

- BP held talks about selling £2bn of UK North Sea assets to Ithaca

- EasyJet’s summer sale reaches Wall Street

- Castlelake: the private credit lender taking a run at EasyJet

- Triton is said to near €3bn deal for Carlyle’s Flender

- Top UK building societies plot bids for digital bank Atom

- CVC buys IFF’s food ingredients division for $4.3bn

- Waldencast to sell its skincare line Obagi Medical to Bridgepoint for $460m

- H&F agrees to acquire B2B events platform Hyve from Providence

Industry news

- UK government urges companies to share data about AI effects on workforce

- Sterling struggles for direction as Iran talks at impasse

- Bank of England’s Bailey says public must be given confidence in 2% inflation target

- UK public inflation expectations ease further in May from March’s Iran shock, survey shows

- Bank of England is watching public-sector pay for inflation risk, governor says

Salaries and bonuses

- Milbank pushes NQ lawyer pay to $235k

- BCLP confirms it boosted NQ lawyer pay to £125k earlier this year

- In-house lawyers call for a ‘cease fire’ in the City pay war

Job moves

Market trends

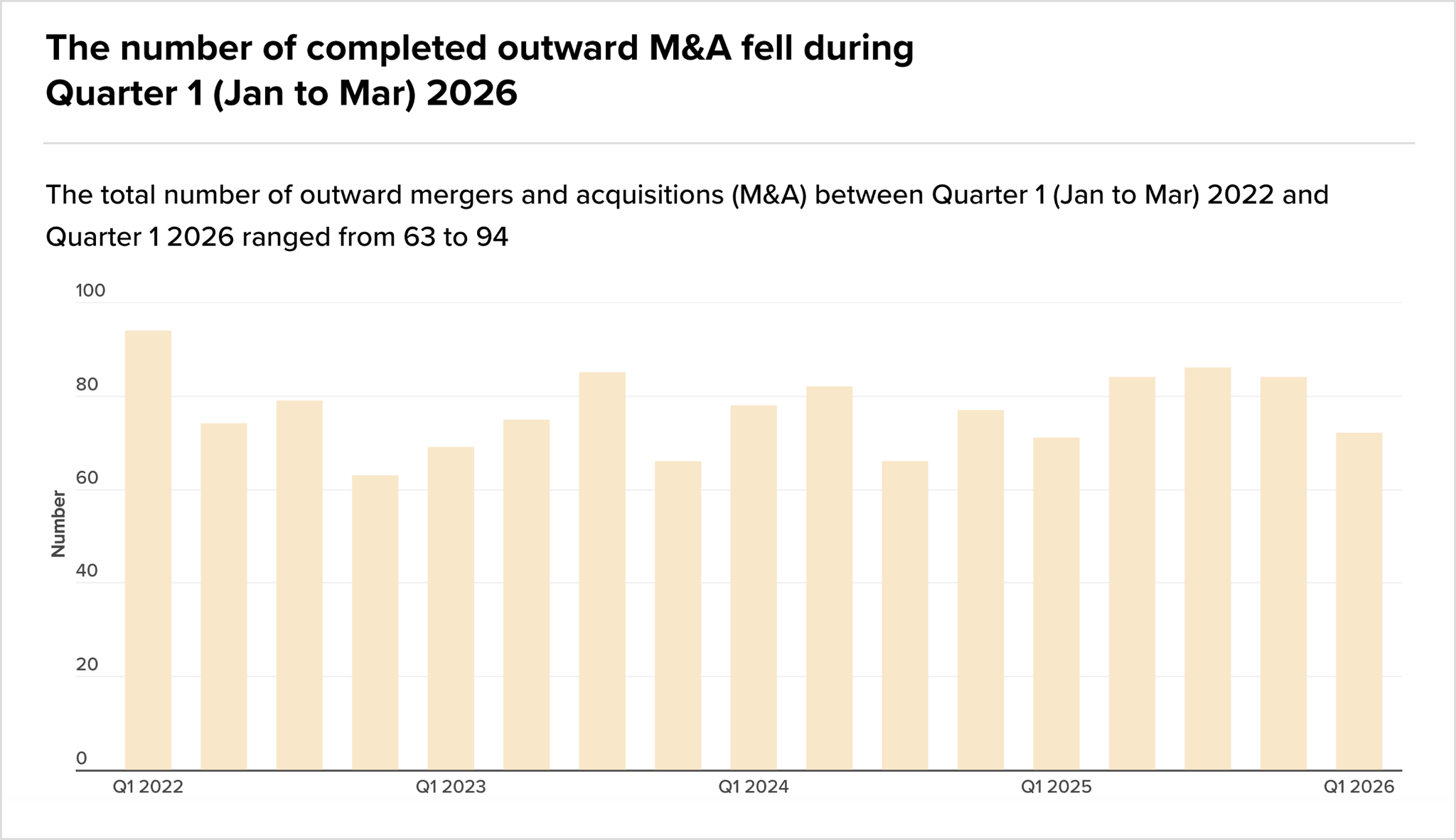

UK outbound deal activity is cooling

The ONS doesn’t dress it up: completed outward M&A dropped to 72 completed transactions in Q1 2026, down from 84 the previous quarter. UK acquirers have grown more deliberate, mandates are running leaner, and boards are taking longer to sign off on cross-border moves when financing costs still haven’t fully unwound.

That said, Browne Jacobson reads the same data differently: UK businesses are increasingly looking abroad for growth, tapping into new markets and technologies even as domestic conditions stay uncertain. Four years of data shows a market stuck between 63 and 94 deals per quarter. There’s a floor, but there’s also a ceiling, and nobody’s breaking through it yet.

On the other hand, 163 inward transactions in Q1 2026 marks the sharpest quarterly fall in the dataset, down from 244 just three months prior. Even accounting for Q4’s historically elevated activity, that’s a meaningful reset. Foreign buyers haven’t walked away from the UK story, but they’re reassessing it.

Value-wise inward M&A fell from £33bn to £14.2bn in a single quarter. Some of that is deal timing, but RSM UK is more direct about the rest: unless the Middle East conflict finds a resolution soon, deal activity could be severely hit in Q2 as companies pull back on major decisions.

Buyers are watching energy costs, consumer confidence and supply chain resilience before committing. The UK remains one of Europe’s most liquid deal markets. It just needs a reason to bring foreign conviction back off the sidelines.

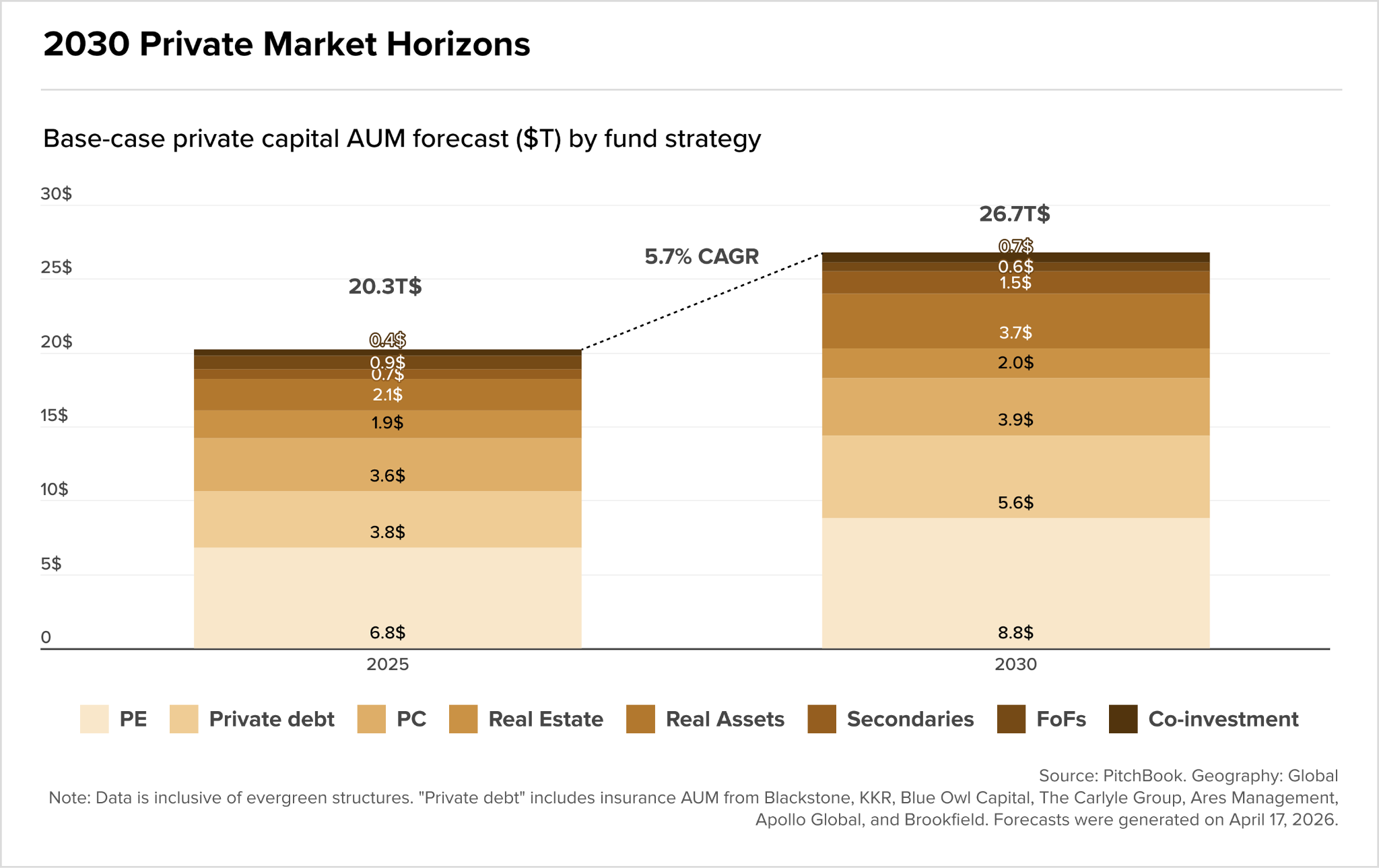

Capital is piling up in private markets, and it has to move eventually

According to PitchBook’s 2030 Private Market Horizons forecast, global private market AUM is on course to hit $26.7 trillion by 2030, growing at a 5.7% CAGR from $20.3 trillion today.

While the headline sounds bullish, the reality underneath it is more complicated. A growing share of that AUM isn’t fresh dry powder ready to deploy. It’s aging portfolio assets sitting in funds well beyond their expected hold periods, managers waiting for the exit window to reopen while LPs grow impatient.

For UK dealmaking, the pressure is building on both sides. GPs need exits, and private debt is forecast to nearly double to $5.6 trillion by 2030. That capital needs a home. When the window reopens, motivated sellers and deep credit markets is a combination the UK is well placed to absorb.

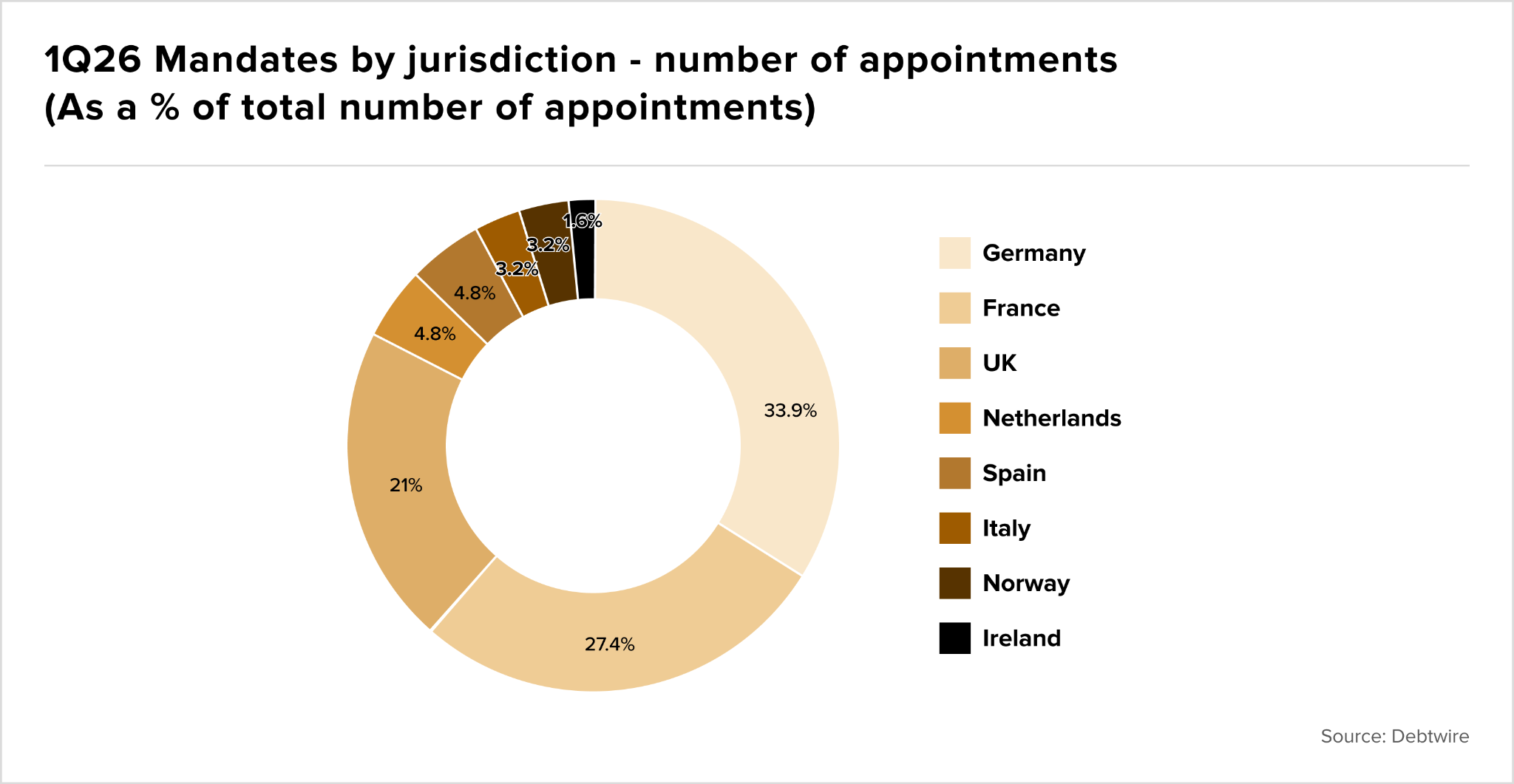

The UK’s restructuring pipeline is quieter than it looks

Debtwire’s Europe Restructuring Advisory Mandates report shows the UK saw just 13 mandates across six situations in Q1 2026, placing it third behind Germany and France with 21% of regional mandate activity. That share looks respectable until you notice in-court activity essentially stalled.

The chill traces back to a credibility problem with the UK’s flagship restructuring tool. A string of contested cases, failed plans and rising legal costs have pushed companies toward out-of-court workouts instead. Distressed situations don’t disappear when they leave the courtroom. They just become harder to track, and that’s when it matters most to be paying attention.

Fundraising

IPOs