Daniel Black

Daniel Black

The UK take-private wave just found its biggest target yet. US warehouse giant Prologis took its £12.6bn bid for UK logistics group Segro public this week after the FTSE 100 board rejected it, according to Reuters and the FT.

It’s the biggest single attempt on a UK-listed company so far this year and it fits a striking pattern: PwC’s mid-year outlook shows megadeals above $5bn now account for nearly half of all global M&A value, double their share from two years ago. The mid-market is shrinking; the giants are eating each other.

And in other news this week:

- H.B. Fuller is nearing a £628m deal for UK medtech AMS, despite months of activist pushback from US shareholder Ancora

- Ari Emanuel’s Mari is in talks to acquire UK theatre group ATG for $6bn

- Citigroup hiked bonuses for its top UK investment bankers by 24%, with London MDs averaging $1.5m and three breaking $11m

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of confirmed M&A deals in the UK.

The rumour mill

- H.B. Fuller nears £628m deal for UK medtech AMS

- EasyJet shows willingness to talk, after its investors hold out for £600m more from Castlelake

- Warehouse giant Prologis takes $16.6bn bid for UK’s Segro public after rejection

- ContourGlobal acquired 500-MW/2-GWh BESS project in Scotland in UK debut

- Segro rejects £12.6bn takeover bid from US data centre rival Prologis

- FirstCash to acquire UK pawn operator Ramsdens in £206m all-cash deal

- Ladbrokes-owner Entain explores options for CEE unit, sources say

- Ballard Power to buy UK hydrogen power firm GeoPura in $400m cash and stock deal

- Standard Chartered explores sale of Bahrain wealth and retail banking business

- Ari Emanuel’s Mari in talks to buy theater group ATG for $6bn

- Aviva to rebrand acquired Lloyd’s syndicate

- egg Power secures 90-MW UK wind PPA with Amazon

- Investcorp to take majority stake in Smart Managed Solutions

- Private equity-owned vet group IVC spends £34m on UK competition probe

- Southern Water Gets £300m Equity as Asterion Joins Macquarie

- EQT to acquire satellite deployment biz

- Peel Hunt’s dealmaking fees more than double on UK M&A boom

- XTX Markets looks for AI gems after striking gold with Anthropic

Industry news

- UK tax gap widens despite government crackdown

- UK fiscal watchdog picks former BoE rate setter as its new chair

- UK private equity braces itself for an Andy Burnham premiership

- UK bond consolidated tape launches to unify trading data

- A 35% FTSE fall and 7% interest rates: Bank of England to test private markets against severe shock

- Bank of England proposes trading capital changes as global regulators line up on Basel 3.1

Salaries and bonuses

- Citi paid its average London investment bank MD $1.5m last year. Three people there got $11m+

- Citigroup hikes bonuses for top UK investment bank staff by 24%

Job moves

- Standard Chartered hires O’Neill to lead infrastructure team

- Barclays hires senior Citigroup dealmaker Dalle to co-lead industrials in Europe

- Citi hires Deutsche’s Mansfield to lead EMEA M&A -memo

- Fried Frank loses real estate duo to Greenberg Traurig

Market trends

Global M&A gets its groove back?

Global M&A is on track for $4 trillion in 2026, the strongest year since 2021, but the headline flatters the reality underneath. PwC’s mid-year outlook shows megadeals above $5bn now account for nearly half of all deal value, double their share from two years ago. Strip them out, and the market is actually shrinking. Volume is falling while value climbs. Fewer people are at the table, and the ones who are arrived with very large cheques.

The mid-market is still grinding through valuation gaps, stubborn exit backlogs, and buyer caution on anything exposed to AI disruption. Software M&A has cooled, while infrastructure, power, data centres, and grid are pulling the capital that used to flow into enterprise tech. The recovery looks highly selective, and the selectivity is only tightening.

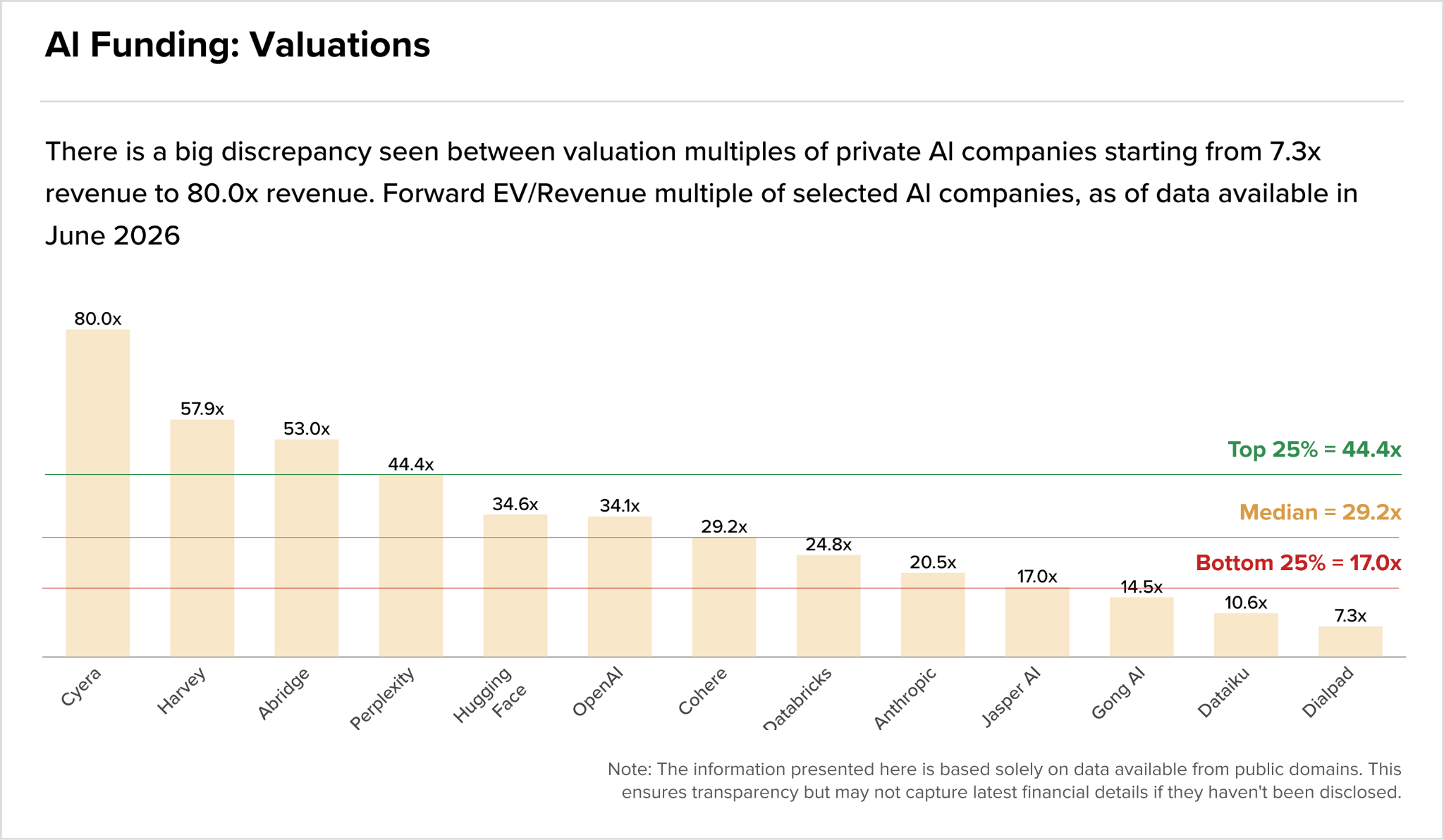

What’s your tech worth?

Aventis Advisors spent June mapping private market AI multiples and found them running from 7x to 80x forward revenue, with a median around 29x. This suggests a market where narrative still sets the price more than fundamentals do.

The companies at the top are being valued on the assumption that their momentum holds and that no frontier lab ships a competing product tomorrow. Both assumptions are fragile.

The fault line runs through private credit too. Pitchbook’s direct lending desk spoke to a number of European lenders this month and found the software conversation is less about panic and more about price discovery. Speaking at SuperReturn in Berlin, Bridgepoint Credit’s Andrew Cleland-Bogle was direct: some managers are going to zero on software right now, and he thinks that’s a mistake.

Arcmont’s Mattis Poetter sees a distinction between deeply embedded systems of record that clients won’t rip out for a modest cost saving and point solutions sitting on top of those systems, which AI-native challengers can already rebuild faster and cheaper. Lenders aren’t necessarily fleeing the sector, but they’re asking whether the right multiple is 15-18x or 10-12x, and taking longer to answer.

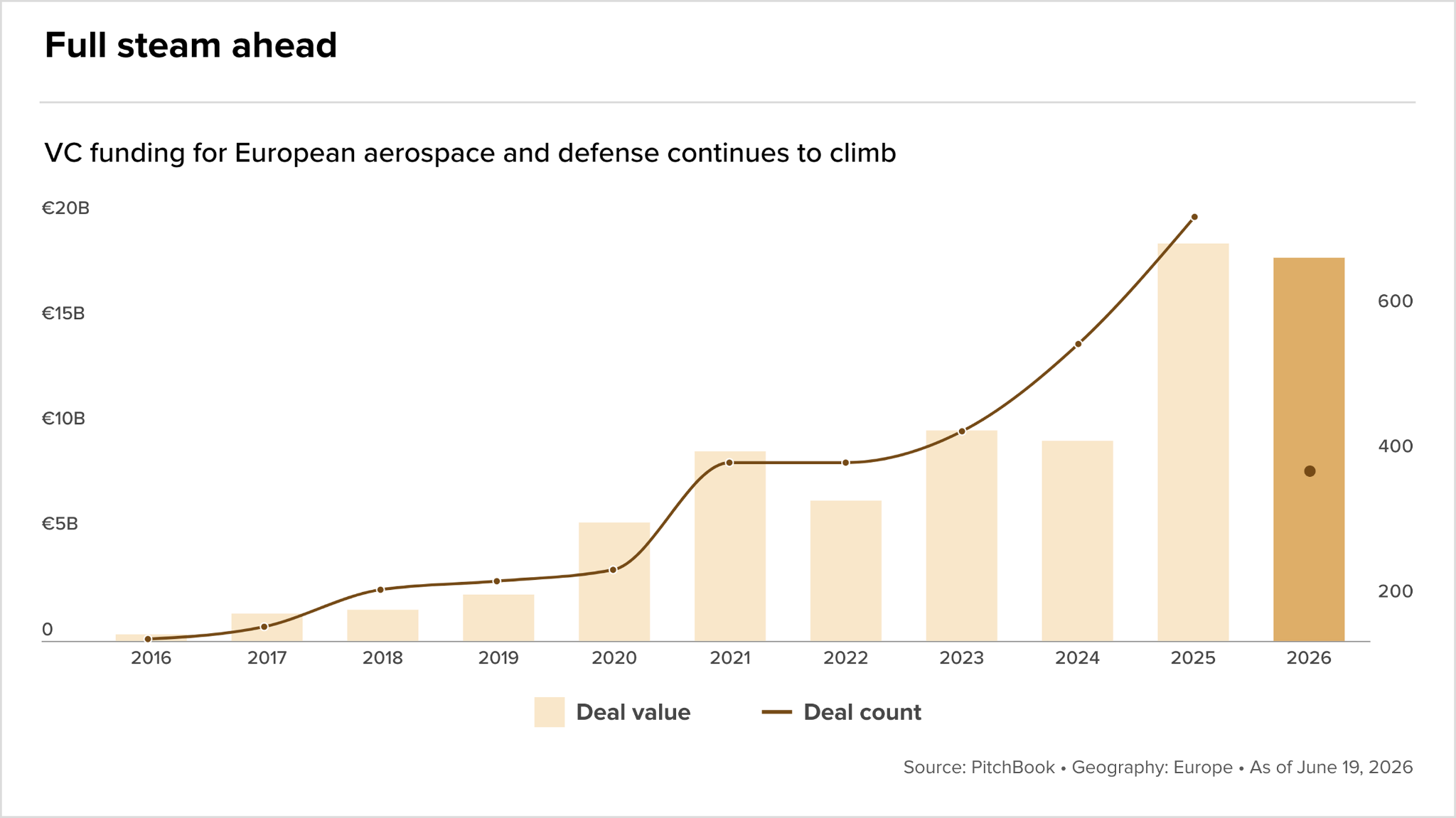

Europe is rearming

PitchBook’s latest data shows VC funding into European aerospace and defence approaching €19bn in 2025, with 2026 already tracking at pace and deal count at record highs.

The growth curve stopped looking like a venture trend some time ago. It looks like a rearmament programme expressed in term sheets.

The US-Iran conflict, the Russian invasion of Ukraine, and a security architecture fracturing in real time have given European governments a spending urgency they hadn’t felt in a generation. Germany, France, and the EU’s ReArm Europe programme together put well over €1 trillion of committed defence expenditure on the table through 2030.

The irony is that 98% of deal value in European defence VC rounds still involves foreign investors, up from 96.5% last year. Helsing and Stark, two of the continent’s most prominent defence tech names, were backed by General Catalyst and Sequoia. New vehicles like the €500 million E2D fund from AVP and Earlybird are pushing back, and BAE Systems’ direct LP commitments signal domestic primes are waking up.

But the dependency won’t shift quickly. For UK dealmakers, the window is in spotting where homegrown institutional capital is quietly building conviction before the American funds get there.

IPOs

- EG Group files plan for US listing that could raise $1bn

- Cavendish chief executive: UK IPO backlog is highest in six years