Daniel Black

Daniel Black

The latest H1 data shows foreign investment continuing to drive UK M&A, with LSEG reporting USD 202 billion in inbound investment during the period, more than double the total recorded in the previous six months.

That momentum continued this week, as French telecoms billionaire Xavier Niel agreed to acquire e&’s 16.2% stake in Vodafone for approximately £4.4 billion. Reuters reported that the transaction was agreed within days and valued the stake at a 13% premium to Vodafone’s previous closing share price.

The deal brings one of Europe’s most active telecoms investors into Vodafone following the group’s extensive restructuring, including its exits from Spain and Italy and the completion of its merger with Three UK. It also adds another major cross-border transaction to an active week for UK-listed businesses.

And in other news this week:

- ABB agreed a £4.1 billion recommended cash acquisition of engineering group Rotork, marking the Swiss company’s largest-ever takeover.

- Arlington Capital Partners offered £345.6 million for Gooch & Housego, representing a 40.7% premium to the photonics company’s previous closing share price.

- Supermarket Income REIT agreed to acquire three UK supermarket properties for a combined £118 million.

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Week Summary | From July 9 to 16, 2026

The UK recorded 25 announced deals between 9 and 16 July, with business services, industrials and consumer the most active sectors, accounting for eight, four and three transactions respectively.

Domestic consolidation dominated overall activity, although inbound buyers were behind several of the week’s headline transactions, including ABB’s proposed acquisition of Rotork and Arlington Capital Partners’ bid for Gooch & Housego.

Bigger deals, fewer transactions: UK M&A in H1 2026

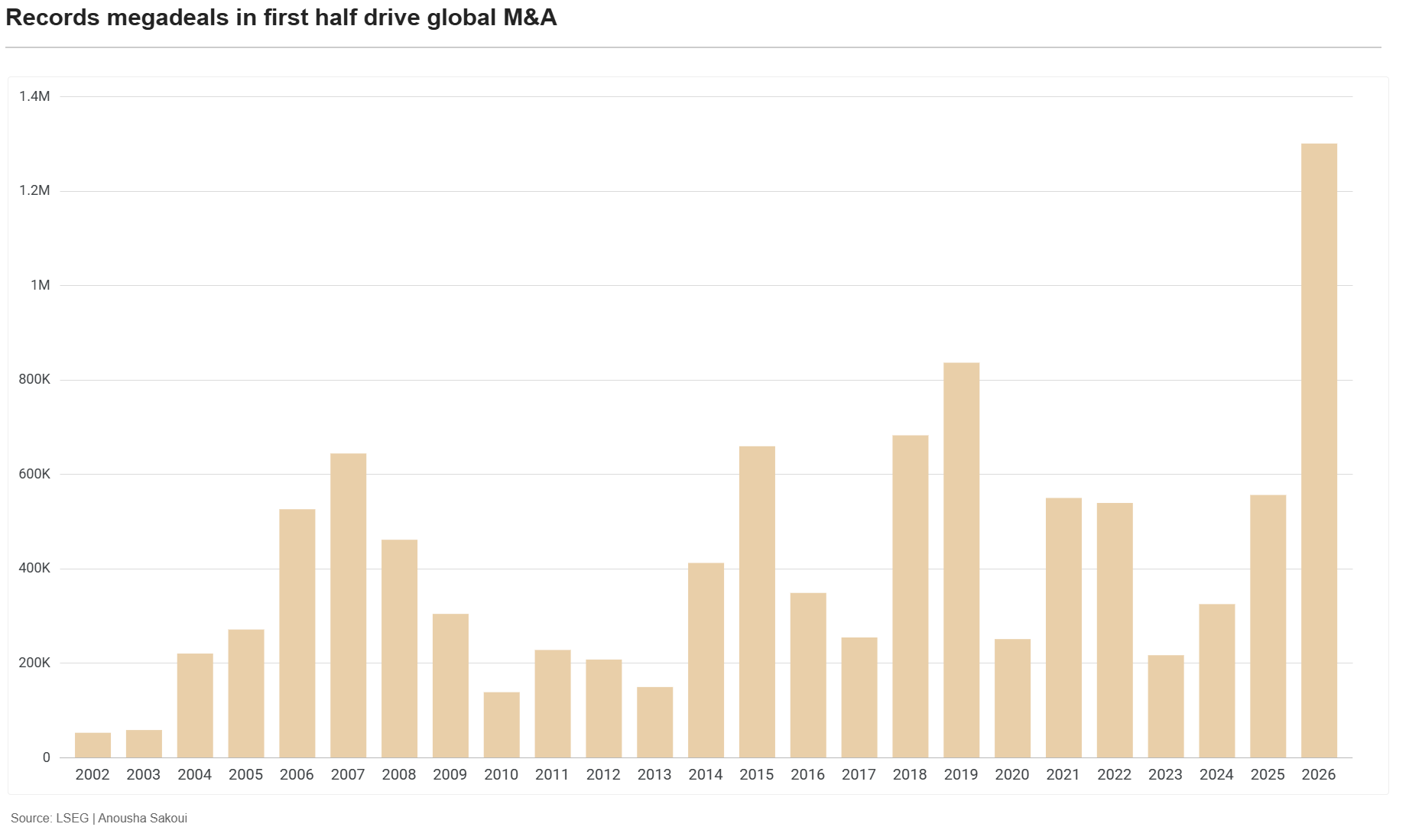

Global M&A saw dream deals take over H1 2026. LSEG data revealed a surge in $10 billion-plus mega-deals that pushed worldwide M&A value to a new record. Announced deals totalled $2.8 trillion, up 48% year on year, despite a 9% drop in deal volume.

Good news, indeed. Despite uncertainty, war and volatility, dealmakers still have that hunger for strategy and growth. It was no different in the UK M&A market.

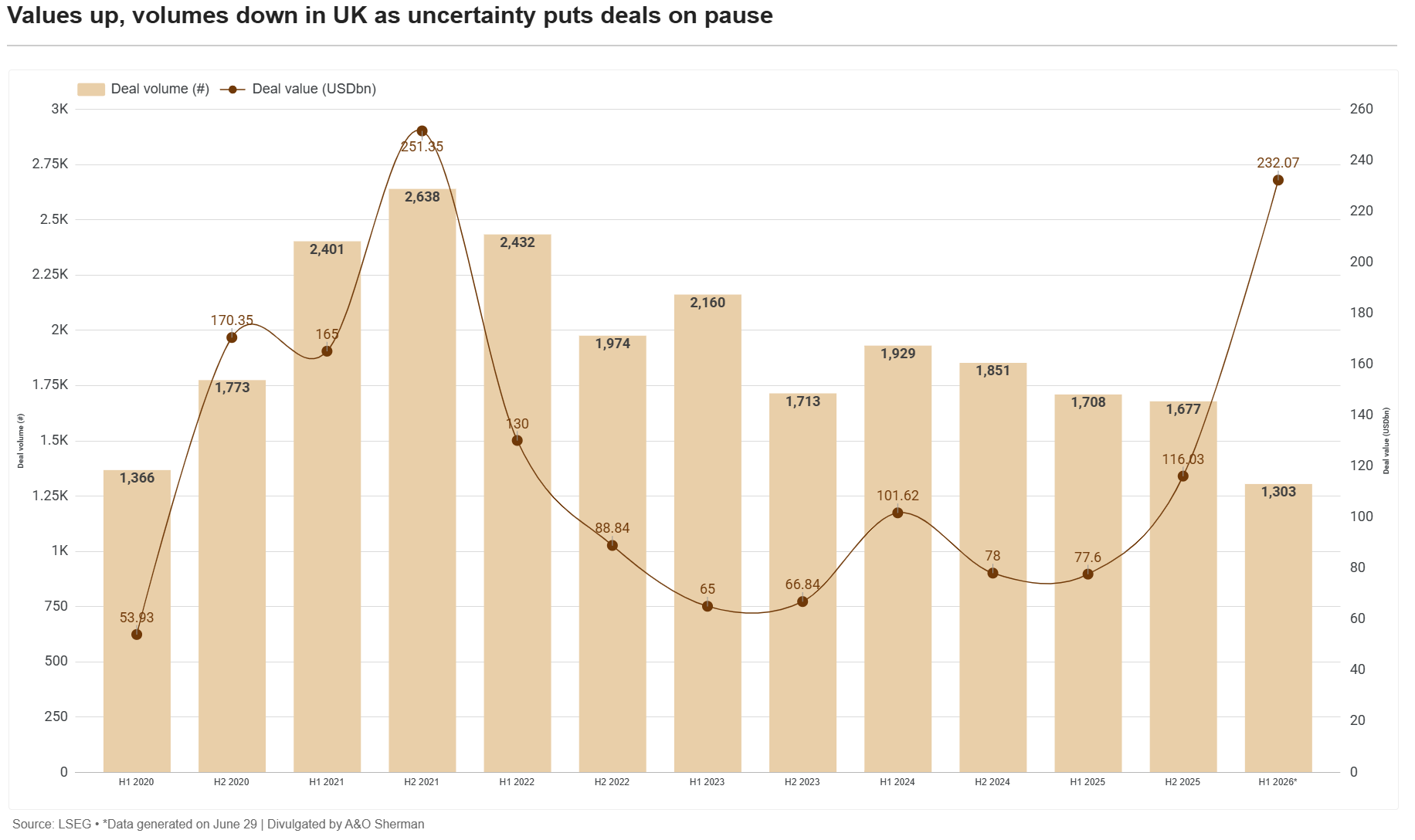

Here, deal value in H1 more than doubled compared with the previous six months, reaching $237 billion, while volume fell 22% from H2 2025 to 1,303 transactions. An analysis by A&O Shearman also revealed AI and carve-outs as boosters to the numbers. But volatility was also everywhere, with a sharp drop in Q2 amid tensions in the Middle East.

From a global perspective, executives interviewed by Reuters pointed to several reasons for the surge in value. There is a change in mindset that makes investors see large deals as requiring as much work as smaller ones, but offering more attractive premiums and synergies. For buyers, large companies also seem more established and competitive than smaller ones, making their multiples far more compelling.

But, of course, we can see the US impact in those numbers. And when we look at the UK in isolation, there are market signals that revive familiar dangers and risks.

AI and foreign investors: How H1 2026 reshaped UK M&A

The same market drivers that pushed M&A indicators higher are also shaping IPOs: technology and geopolitics. EY-Parthenon’s latest analysis points to global initial public offerings linked to AI and related infrastructure as a pivotal factor in IPO results. In M&A, technology was also the largest sector globally, with $649 billion in announced transactions.

But all of this lands differently in the UK. EY’s data also revealed a revival in listings on the London Stock Exchange. There were seven new listings, raising £577 million in the first half of 2026. This represented a 215% increase in proceeds compared with the £183 million raised in H1 2025. But these figures do not stand alone.

At the same time, companies are leaving the London Stock Exchange faster than new ones are arriving. There is a clear example this fortnight: Rotork, which is set to become the latest company to leave the LSE after Swiss group ABB agreed to acquire it in a £4.1 billion deal. We have discussed in previous editions how Britain seemed to be for sale, and that momentum appears to be continuing.

The problem is serious enough for Downing Street to turn to private equity heavyweights and ask why they are not listing British portfolio companies in London, according to the Financial Times. General Atlantic, Elliott Management and EQT are among the firms that have already met with ministers and aides.

The concern is understandable, and data from investment bank Peel Hunt reinforces the scale of the problem: takeover bids for London-listed companies have reached nearly £60 billion this year. Meanwhile, the combined market value of new entrants to the exchange stands at a comparatively microscopic £2.2 billion. Those seven new listings start to feel small by comparison.

The same signals are visible in M&A. Inbound investment dominated the UK’s deal flow, reaching $202 billion, more than double the previous six-month total and the highest half-year figure since H2 2021.

What the UK M&A outlook means for H2 2026

Growth in value, a drop in volume, tech dominance and the impact of geopolitics. The UK remains a market where stability and a positive business environment create opportunities. That is good: it attracts capital. But, at the same time, uncertainty is still raging.

Dealmaking in H2 will require the ability to manage risks ranging from limited diversification and the UK capital market’s dependence on foreign investors to AI valuations and geopolitical tensions.

Not an easy task.

Rumour mill

- DCC founder Jim Flavin has intensified his campaign against the proposed sale of the group to two US private equity firms, arguing that the offer undervalues the company. He urged the board to reject the proposal, focus on its growth plan and aim to build a “world-leading multi-energy solutions company”

- Prologis has renewed its push for a merger with UK warehouse owner SEGRO, publishing an updated investor presentation urging SEGRO shareholders to press the board to enter talks

- Hugo Boss has rejected a €3 billion takeover offer from Mike Ashley’s Frasers Group, calling it financially inadequate and saying it undervalues the German fashion group

- Barclays is preparing to sell approximately $875 million of debt financing used to fund a takeover of UK aerospace supplier Senior PLC

- Qiagen has drawn early takeover interest from KKR and other private equity firms, with potential offers from some suitors reportedly worth at least $50 per share

- Spire Healthcare has extended the deadline for Toscafund Asset Management to submit a formal takeover offer until 6 August

- LondonMetric Property said discussions on its proposed takeover of Picton Property Income were progressing

- BC Partners and CVC are among the private equity firms considering a bid for Italian coffee producer Segafredo Zanetti, as QuattroR weighs the sale of its majority stake in the company

- Safestay is in talks with Infill Capital Partners about a possible takeover after the investment firm’s website referred to a potential £40.9 million take-private deal

- GRIT Investment Trust is in discussions with a mining resources company about a reverse takeover and said non-binding terms were being signed

- Brave Bison is preparing a £45 million takeover bid for marketing effectiveness company System1. The proposed deal would represent a 16% premium to System1’s recent market value of £38.7 million, according to The Times

- Luke Johnson is in talks to acquire Mexican restaurant chain Wahaca following an auction of the business. Several companies are reportedly interested, but Johnson remains the frontrunner

- Mastercard is exploring the sale of a majority stake in its UK payments subsidiary Vocalink back to British banks amid concerns over US ownership of a critical UK payments asset

- Morrisons is in talks with several parties, including US-based Realty Income, over a £600 million real estate deal

- Watches of Switzerland Group has held talks in recent months about potential offers to take the London-listed luxury watch retailer private

- BrewDog co-founder James Watt said he had made an offer to buy back the craft beer business, months after it was sold to a US company

- NextEnergy Solar Fund has launched a formal sale process, citing its persistent share-price discount to reported net asset value and the challenges of raising equity capital

- Workspace said it had more than £200 million of assets for sale and was considering a further £100 million in disposals amid pressure from activist investor Saba Capital Management

Job moves

- SCP Standard Capital Partners appoints Fabian Becker as chairman of the management board and chief executive officer

- Jefferies financial institutions dealmaker Graham Davidson is set to join Continuum Advisory Partners

- PIB Group appoints Alastair Hay as chief financial officer

- Interpath appoints Suwin Lee as managing director and global head of tax

- DSW Transaction Services expands into Southampton with the appointment of Alex Milne

- Barclays appoints Peter Luck as chairman of UK investment banking

- Alvarez & Marsal appoints Bernd Oehring to strengthen its carve-out and merger integration capabilities

- FRP Advisory appoints Rick Thompson and Philip Davies to launch its UK Public Company Advisory service

- Cornerstone Research appoints Ryan Williams as a principal in London

- Saffery appoints Emma Siegel as corporate tax director in Edinburgh

- EY-Parthenon promotes Caroline Pover to equity partner in its UK and Ireland financial restructuring practice

Fundraising

- The British Business Bank has invested £27 million in maritime defence technology company Kraken Technology as part of its £130 million Series B funding round

- Clinical-stage biotechnology company Alchemab Therapeutics has raised £25 million in a Series A funding round

- Marker has raised $13 million in a seed round led by Index Ventures, with participation from LocalGlobe, betaworks, Radical Ventures, Tiny Supercomputer Investment Company, Otherwise Fund and angel investors Steve Newman, Cal Henderson and Thomas Wolf

- Pixel-Flo has raised £5.25 million in seed funding

- Leo Cancer Care has raised £48.6 million in a growth funding round led by Yu Galaxy, with new investment from Eventide Asset Management and continued backing from existing shareholders

- BGF has made an undisclosed multimillion-pound growth investment in engineering consultancy Rappor

- Foresight Group has invested £5 million in Regenerus Laboratories, which was also awarded a £3 million grant by Scottish Enterprise

- Reformed has closed an oversubscribed $22 million Series A round led by IRIS Ventures, with participation from JamJar Investments, V3 Ventures and FoodLabs

- The British Business Bank has committed £17.5 million to SFC Capital as it continues its investment programme

- Everflow has received a £22 million investment from BGF alongside a separate £22 million funding package from OakNorth

- Prolo has secured £4.2 million in an oversubscribed seed round led by Triple Point Ventures, with participation from Anamcara Capital, Concrete VC, Foundation Ventures, Haatch, Koro Capital, Love Ventures, Portfolio Ventures and the a16z Scout Fund

- Gridcog has raised £7 million in a Series A round led by ABB, with participation from Axpo, DNV Ventures, VERBUND X Ventures, AlbionVC and the Clean Energy Finance Corporation

- The British Business Bank has invested $65 million in Draig Therapeutics’ Series B funding round

- Valarian has raised $50 million in a Series A round led by New Enterprise Associates, bringing its total funding to $70 million

- Velocity has raised $38 million in a Series A round led by Dragonfly and FirstMark, with participation from Activant Capital, Capital One Ventures, QED Investors, Coinbase Ventures, Wintermute Ventures and Ripple

- Risk Ledger has raised £24 million in a Series B round led by Axiom Equity, alongside Mercia Ventures, which previously invested in the company’s Series A round

- Saible has raised a total of £2.9 million from angel investors, comprising £2.1 million already secured and a further £800,000 angel round

- The British Business Bank has made a £50 million cornerstone commitment to Soho Square Partnership Capital Fund II, with several US institutional investors also participating

- Supermarket Income REIT has launched an equity fundraising targeting approximately £100 million in gross proceeds

- BGF has invested £20 million in sports technology company Urban Zoo

- LDC, the private equity arm of Lloyds Banking Group, has made an undisclosed investment in Brady Solicitors

- Applied Computing has closed a $20 million funding round led by KBR, with participation from Databricks Ventures

- Tyred has raised £2.5 million from Raw Ventures, Ada Ventures and angel investors, including Dwelly investor Anton Buzdalin

- Meticulous has raised $15 million in a Series A round led by Chemistry, with participation from Menlo Ventures and several AI industry leaders