Sebastian Montoya

Sebastian Montoya

The EU’s competitiveness in the energy transition is under pressure.

This week, we look at the Antwerp Declaration Monitoring Report 2026 to extract key insights on the region’s industrial challenges on the path to a greener future and how these dynamics are impacting dealmaking.

And, of course, we bring you this week’s clean energy M&A deals. Among them, the highlights are:

- TotalEnergies will take a 50% stake in EPH’s flexible generation platform in a EUR 5.1bn all-stock deal, creating a pan-European JV with more than 14 GW of assets and pipeline across gas, biomass and battery storage.

- TINC committed EUR 23m alongside partners to two Belgian BESS projects led by Storm, with total project value reaching EUR 330m for 300 MW/1.2 GWh, pointing to premium storage valuations in core European markets.

- Airengy agreed to acquire a 33.3 MW solar portfolio in Poland from INVL for EUR 23.7m, structuring the deal as a phased transfer and reinforcing its solar-plus-storage expansion strategy in Central Europe.

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Energy M&A in Iberia: Cocktails and connections

The Iberian energy market continues to lead the way in the European transition, driven by significant investment in renewables and a robust pipeline of infrastructure projects.

Join the M&A Community and Ideals for an exclusive networking evening at Casa Suecia. We’ll gather to discuss the evolving landscape of the Spanish energy sector at this stylish venue in the centre of Madrid.

Deals breakdown

Why Europe’s Clean Industrial Deal now depends on competitiveness

Clean energy M&A is shaped by a complex range of factors. Deal activity hinges on power prices, grid access, permitting timelines, public funding, industrial policy and, ultimately, Europe’s credibility as a place to build and invest.

That is precisely why the Antwerp Declaration Monitoring Report 2026, commissioned by Cefic and prepared by Deloitte, is so relevant. It provides a structured lens on the underlying conditions driving dealmaking.

The Antwerp Declaration itself is an industry-led initiative launched in February 2024 by more than 70 European industrial leaders, calling on the EU to restore competitiveness while advancing the green transition.

It was shaped by rising concerns over high energy costs, industrial slowdown and weakening investment, and pushes for a better alignment between climate ambition and the real conditions required to invest, build and scale in Europe.

One figure captures the report’s tone with clarity: 83% of the EU’s key competitiveness indicators are either stagnant or deteriorating. This does not reflect a lack of ambition, but rather a gap in execution.

Europe still struggles to convert policy intent into investable conditions, scalable infrastructure and industrial advantage. In that sense, the energy transition is no longer just a policy agenda. It has become a full-scale stress test of Europe’s ability to deliver.

To understand where that pressure is coming from, the report breaks the challenge down into pillars, each addressing a critical constraint shaping Europe’s clean energy investment and M&A landscape.

Policy, funding and execution risk

The report first points to a shift in political direction. The Clean Industrial Deal is now embedded in the EU’s strategic agenda, signalling that competitiveness has returned to the centre of policymaking.

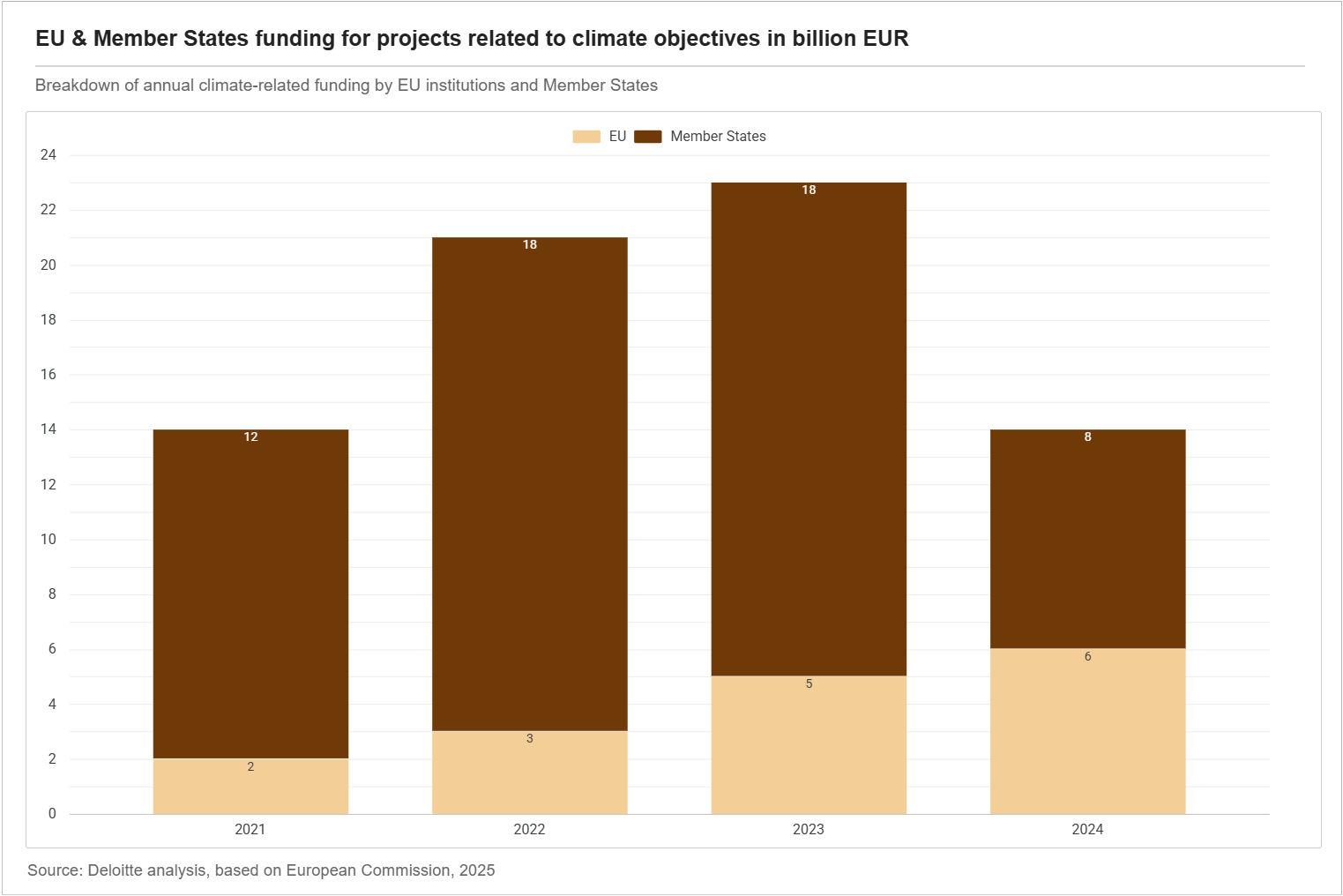

Yet the funding picture remains fragmented, resulting in uneven visibility on timelines, incentives and policy stability.

While public funding has increased (around €72bn mobilised between 2021 and 2024) Europe still faces an annual investment gap of roughly €406bn to meet its 2030 targets.

The Innovation Fund, for instance, was oversubscribed by more than 500% in 2024, highlighting strong demand but limited capacity to deploy capital at scale.

Energy costs remain the core constraint

Energy costs are a core driver of valuation, risk pricing and capital allocation for dealmakers. But it is also one of Europe’s most persistent structural weaknesses. Industrial electricity prices remain around 2.4x higher than in the US, China and India, while gas prices are close to 5x higher than in the US.

Clean capacity is expanding, but not fast enough to close the gap, with China installing new capacity at a significantly faster pace. Even corporate PPAs reflect this pressure, with volumes falling to 7.64 GW in 2025.

Infrastructure and scale are still misaligned

Progress in infrastructure investment is visible, but not yet sufficient. The EU increased grid and storage investment to around 0.46% of GDP, but bottlenecks persist, with connection queues stretching from 7 to 10 years in several markets.

At the same time, only 14 out of 27 Member States met interconnection targets. Beyond grids, gaps remain in CO₂ storage, digital infrastructure and industrial scaling capabilities. The result is a system where ambition continues to outpace delivery, increasing execution risk and delaying project timelines for investors.

Supply chains remain structurally exposed

Exposure to inputs is increasingly a pricing and strategy factor. Despite progress in circularity, Europe remains heavily dependent on external sources for critical raw materials, with none of the 34 materials assessed fully covered by domestic production.

At the same time, domestic gas production has fallen by around 66% since 2015, reinforcing structural dependencies. Circularity provides a relative advantage, with a material use rate of 12.2% versus a global average of 6.9%, but it is not sufficient to offset supply risks.

Market fragmentation and regulatory burden continue to weigh on deals

Finally, the report highlights persistent inefficiencies in how Europe operates as a market, generating higher transaction complexity, slower execution and reduced scalability across borders.

Intra-EU trade already represents around 33% of GDP, yet 61% of exporters still face fragmented rules across Member States. The cost of these internal barriers is significant, with estimates suggesting they are equivalent to tariffs of up to 65% for goods and 100% for services.

At the same time, 34% of firms identify regulation as a major barrier to investment.

The key takeaway?

All the pillars brought by the report converge into a single conclusion: Europe’s challenge is not a lack of ambition, capital or industrial capability. It is the lack of alignment between these elements.

For clean energy M&A, this is the underlying equation shaping where deals accelerate, where they stall and how assets are priced. The transition is no longer just a policy story. It is an operational one.

Battery storage

Bio-fuels

- EU | Glencore acquires majority stake in low-carbon fuels firm FincoEnergies, expanding into transportation fuels and carbon credit solutions

- Ireland | Universities Superannuation Scheme acquires 50% stake in Dublin Waste to Energy facility, enhancing long-term infrastructure investment strategy

- Spain | AGR Biogas and TURN2X partner to develop integrated renewable gas projects, combining biomethane production with e-methane generation to enhance industrial decarbonization

- United Kingdom | BioticNRG acquires Somerset anaerobic digestion plant, expanding UK bioenergy portfolio to nine AD sites and strengthening food waste management capabilities

Multiple

- Europe | Brookfield and La Caisse to acquire Boralex for $9.0 billion, positioning the renewable energy leader for accelerated growth and increased capital deployment

- Europe | EPH and TotalEnergies form joint venture to operate gigawatt-scale flexible power generation portfolio, with TotalEnergies acquiring 50% stake in EFG Holding

Retail/Grid Network

Solar

- Germany | Green FOX Energy hands over 3.5 MWp Beckum solar park to Energieversorgung Beckum, powering over 1,000 households with green electricity

- Germany | RP Global acquires 15 MWp solar projects from Vattenfall subsidiary, expanding its footprint in Baden-Wuerttemberg with plans for 2026 construction start

- Italy | European Energy divests 151 MW Mineo solar project to Sosteneo, completing capital rotation strategy with CfD-backed asset at ready-to-build stage

- Italy | Sonnedix acquires 194 MW Akira solar portfolio, surpassing 1 GW operational capacity in Italy and reinforcing leadership in the market

- Italy | Zenith Energy acquires 10 MWp agrivoltaic project in Lazio, expanding solar development pipeline to 173.5 MWp and supporting strategic growth targets

- Poland | INVL Renewable Energy Fund I sells 33.3 MW solar portfolio to Airengy for €23.7 million, advancing capital rotation strategy with proceeds directed to Romanian projects

Wind

- France | Axium Infrastructure acquires 49.9% equity in 174 MW operational wind portfolio from Banque des Territoires, marking first renewable energy investment in Europe

- France | Velto Renewables acquires 11 MW L’Escur Wind Farm from Q ENERGY, expanding its French wind portfolio and reinforcing IPP presence

- Poland | PNE Group sells 72 MW wind farm project to global energy transition player, reinforcing market position and expanding Polish renewable energy footprint