Sebastian Montoya

Sebastian Montoya

In this week’s Teaser Energy Europe, we break down the list of 235 projects just published by the European Commission, the ones with the highest probability of reaching FID in the next 24 to 36 months. And what the list reveals might have a pretty relevant impact on your deal-making.

And of course, we also bring you all the deals of the week. The big highlights are:

- Galp agreed to acquire a 351 MW portfolio of operational onshore wind assets in Spain from Helia Funds for an equity value of €320m, in a move that broadens its Iberian renewables mix and gives it an immediate foothold in wind through 17 operating farms.

- ENGIE España acquired 278 MW / 1,112 MWh of battery storage projects in Andalusia from Rolwind Renovables, adding one of the largest standalone BESS portfolios currently under development in Spain as it doubles down on flexibility and grid-support infrastructure.

- Equitix bought a majority stake in Capital Energy‘s 120 MW Canales Sur wind project in Spain, extending a partnership that is increasingly centred on hybridisation, with a second phase expected to add up to 120 MW of solar and 120 MW of battery storage.

Want more insight? Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Energy M&A in Iberia: Cocktails and connections

The Iberian energy market continues to lead the way in the European transition, driven by significant investment in renewables and a robust pipeline of infrastructure projects.

Join the M&A Community and Ideals for an exclusive networking evening at Casa Suecia. We’ll gather to discuss the evolving landscape of the Spanish energy sector at this stylish venue in the centre of Madrid.

Deals breakdown

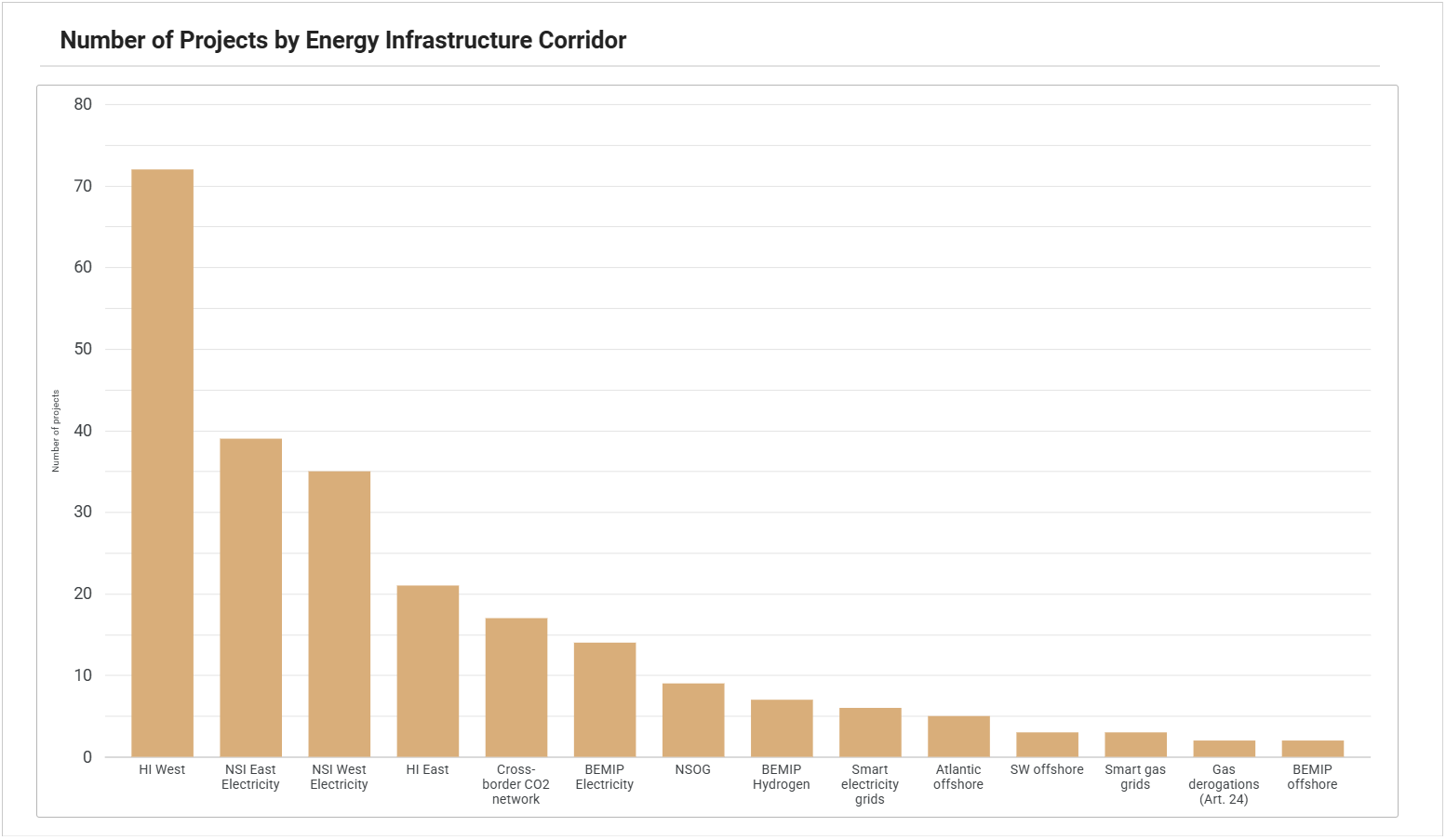

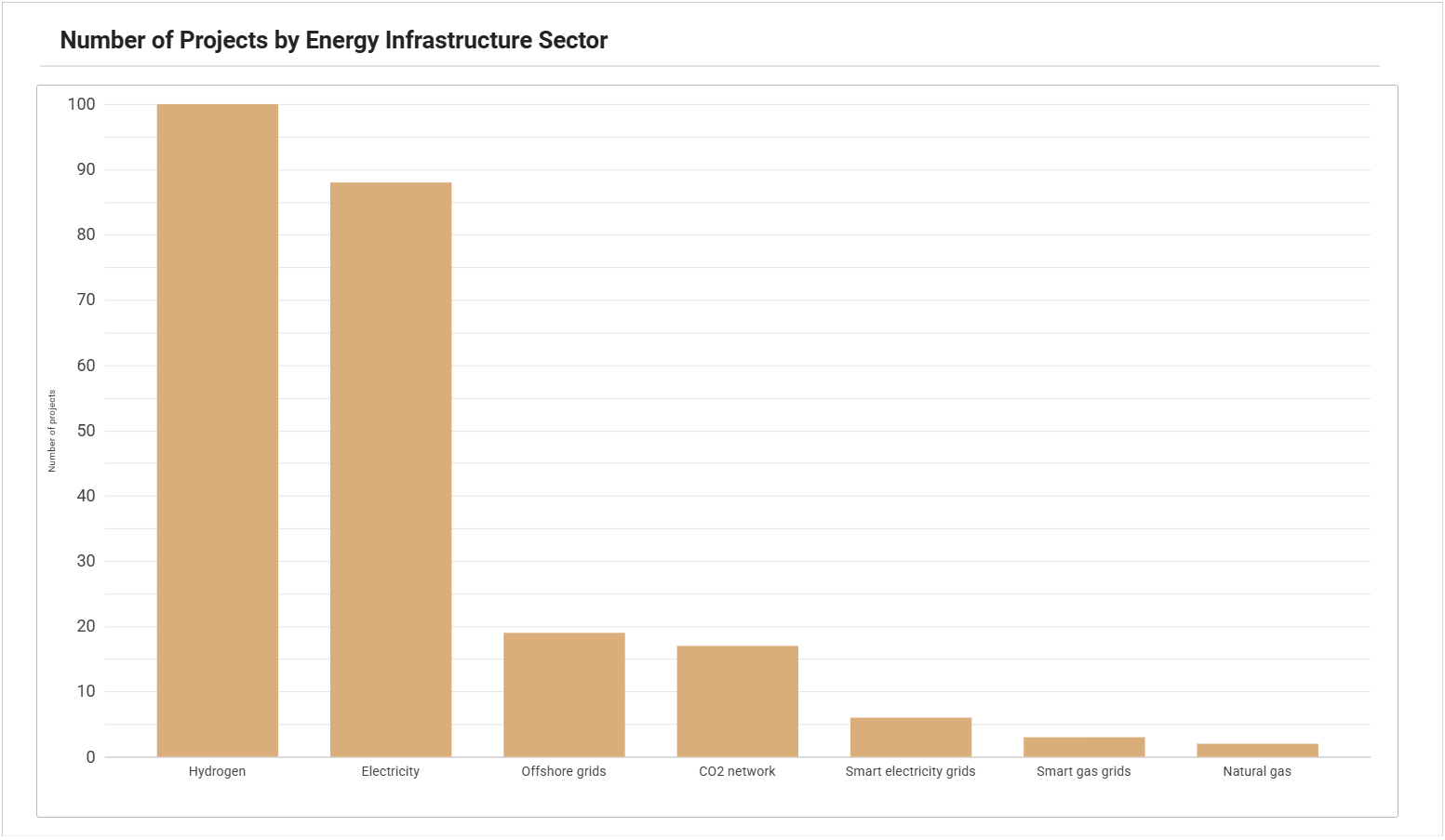

The new PCI and PMI list: 235 projects on the capital radar

The flow of notices from the European Commission has been especially interesting at the end of Q1 and start of Q2.

We have already covered important reports and projects here at Teaser Energy Europe, such as the Clean Energy Investment Strategy, published last month. Now, this week, the Commission published in its Official Journal the Delegated Regulation 2026/764, which establishes the second Union List of Projects of Common Interest (PCIs) and Projects of Mutual Interest (PMIs).

The first list came out in 2024, it is updated every two years and works, in practice, as the stamp that separates Brussels’ priority projects from the rest.

PCIs are infrastructures that connect two or more Member States, or that, even when internal, are essential to unlock cross-border flows. They are strategic projects to complete the EU’s internal energy market and push the bloc’s climate targets forward. PMIs follow the same logic, but involve countries outside the bloc (United Kingdom, Norway, Switzerland, Ukraine, Tunisia, Egypt, Israel, among others).

The second edition covers 235 cross-border energy infrastructure projects that will get accelerated permitting, regulatory support and eligibility for European funding. All of this comes into force at the end of April.

Looking at the list through an M&A lens makes it even more interesting. We can draw some readings from it, especially the fact that the listed projects give us, basically, a map of the assets with the highest probability of reaching FID in the next 24 to 36 months.

So if you have a project that fits, it is worth paying attention.

The M&A impact, in numbers

A report divulgated by Ember has already shown it: the EU needs 151 GW of new interconnection capacity by 2040, at an estimated cost of at least €150 billion. That is roughly €1 million per MW. The biggest projects on the list already show this order of magnitude:

- the Celtic Interconnector (France-Ireland, 700 MW) costs €1.6 billion

- the Great Sea Interconnector (Greece-Cyprus, 1,000 MW) is budgeted at €1.9 billion just for the Greece-Cyprus stretch

- the ELMED (Italy-Tunisia, 600 MW) was recently revised to €1.01 billion by the Tunisian authorities.

At the top of the range, the Triton Link (Belgium-Denmark, 2 GW, connecting two energy islands) is likely to move in the single-digit billions. Even projects considered mid-sized on the list, such as Fenno-Skan 3 (Finland-Sweden, 800 MW), should land between €500 and €800 million, using Fenno-Skan 2 as a reference, which was completed in 2011 at around €320 million.

Harmony Link itself is a reminder of the inflation in the segment: originally budgeted at €680 million, it received bids close to €1.6 billion and had to be re-tendered.

This fits into a pattern that goes beyond the EU borders. Historically, markets like the Brazilian one already see more equity attraction after construction for this kind of asset. But there is an important distinction here. Interconnectors held directly by TSOs through joint ventures are treated as core infrastructure and rarely change hands. The M&A activity tends to concentrate on merchant interconnectors or those under cap-and-floor regimes.

A recent example, from back when we were still publishing Teaser on Substack, is Greenlink (504 MW), developed by Partners Group at a cost above €500 million and in operation since 2024. It was sold in March 2025 to Baltic Cable (a Statkraft subsidiary) and Equitix at an enterprise value above €1 billion.

That was almost double the value between development and operation.

What do we see in the hydrogen example?

One sector that is interesting to look at more closely is hydrogen, where the picture seems more embryonic (but also more fragmented).

Among the projects on the list itself, there is already concrete movement:

- RWE started commissioning GET H2 Nukleus in Lingen in December 2024, currently the largest operational electrolyser in Europe. It was backed by €619 million in German public funding and a 15-year offtake contract with TotalEnergies for 30,000 tonnes per year from 2030.

- OMV took FID in 2025 on a 140 MW plant in Bruck an der Leitha, Austria, with investment in the hundreds of millions of euros.

- Thyssenkrupp Nucera closed in September 2025 the acquisition of key assets from Danish company Green Hydrogen Systems, which was going through insolvency. A sign that the consolidation wave in the electrolyser manufacturing chain has already started.

Even so, the bottleneck remains: the EY European Hydrogen Index 2025 estimates that 98% of the European pipeline of 142 GW in hydrogen is still at concept or feasibility stage.

The capital variable

The equation has another side: public money.

The main subsidy channel for the projects on the list is the Connecting Europe Facility, the EU fund dedicated to co-financing studies and works on cross-border energy infrastructure.

Since 2014, it has already disbursed €8.7 billion. The contribution is not marginal: Ember estimates that the CEF covers, on average, around 31.5% of the total CAPEX of an interconnector. In the big projects, this translates into contributions like the €537.5 million the Celtic Interconnector received, the €657 million of the Great Sea Interconnector or the €307.6 million of ELMED.

The single biggest beneficiary of the instrument, however, was the Baltic synchronisation, which received more than €1.2 billion over the years. The CEF 2026 call should open by the end of April, with the deadline at the end of September.

For the 2028-2034 Multiannual Financial Framework, the Commission has proposed to increase the instrument’s budget five-fold, from €5.84 billion to €29.91 billion. If the number survives the negotiation with the Council and the Parliament, it will materially change the viability math of several of the listed corridors (and, by extension, the appetite of strategic and financial buyers for positions in these assets before the final investment decision).

The list also does not come isolated. It adds to the European Grids Package, the regulatory package launched by the Commission to speed up the planning and financing of electricity grids, to the Energy Highways Initiative, which deals specifically with the large high-capacity transmission corridors between regions with surplus and deficit of renewables, and to the Energy Union Task Force, a political coordination group between the Commission and Member States created to unlock implementation bottlenecks.

Together, we see the framework in which the PCI and PMI list operates.

For the market, the message is that out of the candidate projects submitted in the last cycle, these are the ones Brussels considered mature, necessary and aligned with the bloc’s decarbonisation and energy security strategy.

It is worth following closely which of them start to change hands. And for that, keep following Teaser Energy Europe and don’t miss a thing.

Battery storage

- Germany | KGAL ESPF 5 invests in 17.3 MW / 48.8 MWh BESS project in Grevesmühlen from FENECON, expanding storage portfolio and securing near-term operational asset

- Spain | ENGIE acquires 278 MW battery storage portfolio from Rolwind Renewables, investing over €240m to strengthen grid stability and energy transition

Multiple

- Europe | Blackstone invests in Sunotec through structured equity partnership to scale solar, BESS and grid infrastructure platform, supporting international expansion across Europe

- Switzerland | Amundi invests in Youdera to scale distributed energy platform targeting C&I sector, backing €150m rollout of multi-technology infrastructure across Europe

- United Kingdom | Modutec acquires majority stake in EOS Europe to expand turnkey electrical services offering across energy and marine sectors

Solar

- Germany | Novar acquires 100 MWp Untermünkheim solar project from Stromernte, marking entry into southern Germany and advancing development pipeline with potential BESS integration

- Poland | Qualitas Energy acquires 376 MWp operational solar PV portfolio from Better Energy and Industriens Pension, marking first investment under Fund VI and expanding Polish footprint

Solar + BESS

- Romania | ALFI Green Energy Fund acquires 65% stake in 126 MWp solar and 200 MWh BESS project from Kraftfeld Energy, securing €90m financing to advance flagship hybrid development

- Romania | Renalfa Power Clusters acquires 365 MWp solar and 400 MW BESS projects to develop large-scale hybrid cluster, targeting over 1 GW storage and 568 MWp solar capacity

Wind

- Spain | Capital Energy sells majority stake in 120 MW Canales Sur wind project to Equitix, advancing partnership while retaining co-ownership and enabling future hybrid expansion

- Spain | Galp agrees to acquire 351 MW operational wind portfolio from Helia funds for ~€320m, diversifying renewable mix and strengthening Iberian wind exposure

- United Kingdom | Hexicon completes divestment of TwinHub floating offshore wind project to strategic buyer for nominal consideration, exiting UK development asset