Sebastian Montoya

Sebastian Montoya

The European Commission’s new Clean Energy Investment Strategy does far more than simply recognise the infrastructure and regulatory challenges facing the region’s energy sector, it also sets out actionable insights: the capital is there, but it needs public sector support to start flowing.

In this edition of Teaser Energy Europe, we break down the four actions proposed by the Commission to unlock investment in renewables across Europe. And, of course, we also bring you the week’s key deals, including:

- Cloudberry Clean Energy agreed to acquire a 50% stake in a 132 MW onshore wind farm in Finland for an enterprise value of EUR 75m, marking a meaningful entry into the Finnish market through an operating asset at a valuation below replacement cost.

- Airengy signed the acquisition of a 33.3 MW solar portfolio in Poland from I Fund Energy Renewable INVL for EUR 23.7m, buying its entry into the operation of power generation assets in Europe.

- Aquila European Renewables completed the sale of the 40 MW Desfina wind farm in Greece to funds advised by Aquila Capital itself for EUR 26m, as part of the company’s wind-down process.

Want more insight?

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

European Commission proposes new clean energy investment strategy; here is how it could affect your deals

Private capital is available and must be mobilised.

According to the European Commission, around EUR 33.7 trillion is under private management in Europe, with more than EUR 12 trillion held by institutional investors such as insurers and pension funds. That is capital theoretically available for the energy transition.

In practice, however, much of it remains blocked by a mix of market and regulatory frictions: long permitting timelines, slow grid connections, fragmented national rules and risk profiles that still keep too many projects from reaching financial close.That is one of the key takeaways from the Commission’s new Clean Energy Investment Strategy. It also lands close to the point we made in our last Teaser: the will to invest in renewables is strong, but the act of investing is not quite so simple.

The document’s core proposition is to use public money more strategically: not to replace private capital, but to unlock it across grids, storage, energy efficiency and higher-risk technologies.

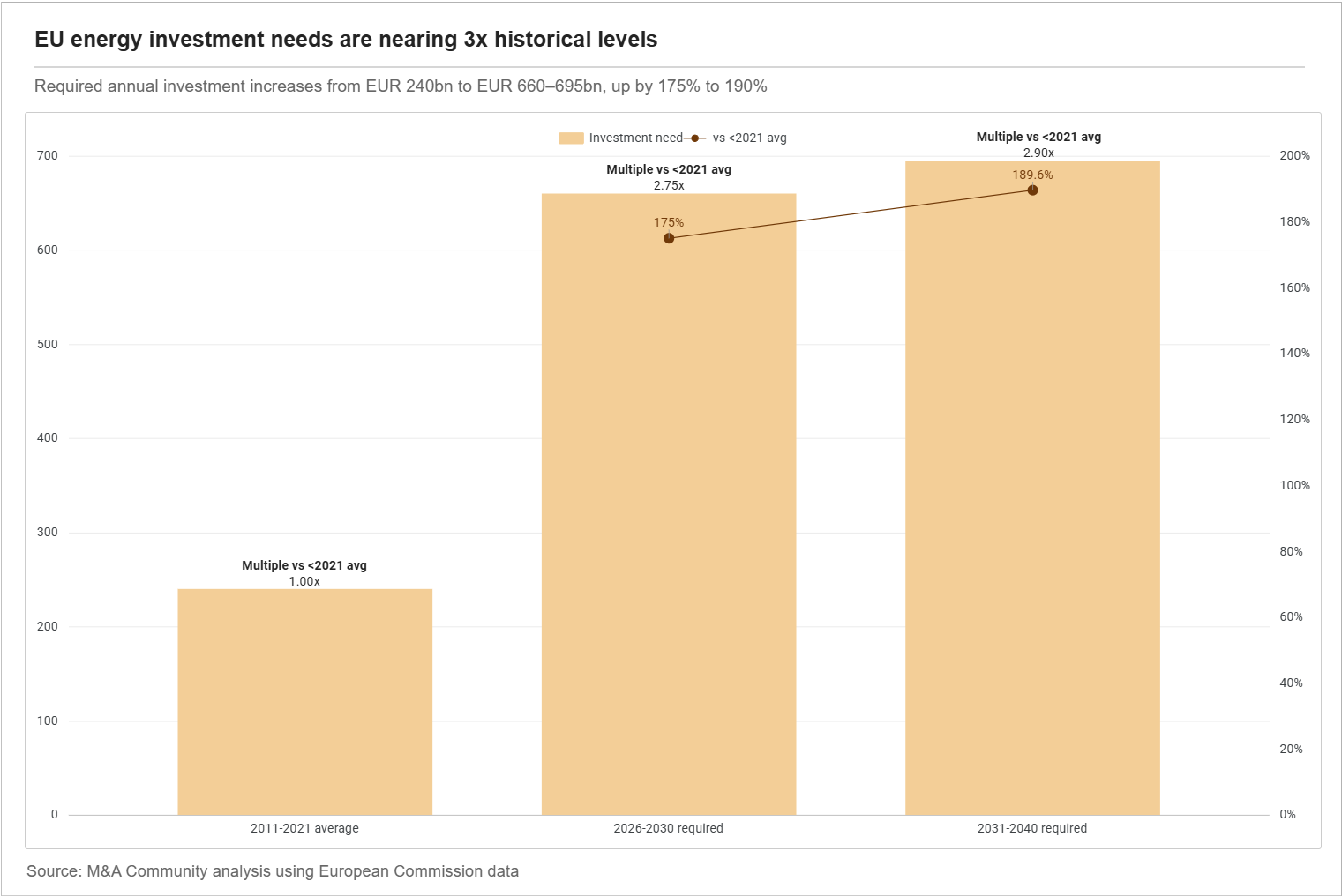

The timing is not incidental. Alongside the strategy, the Commission updated the scale of capital required to hit the region’s energy transition targets. It estimates that annual investment in the energy sector must reach roughly EUR 660 billion between 2026 and 2030, rising to EUR 695 billion a year between 2031 and 2040. That is a sharp step up from the EUR 240 billion annual average recorded between 2011 and 2021.

As the numbers rise, so does the urgency. The Commission is not proposing that public authorities fully finance the next wave of projects. Rather, it wants the public sector to absorb risk, structure financial instruments and attract private capital at scale. The operative logic is: less subsidy, more mobilisation of private capital.

The EIB Group, the EU’s financing arm for long-term investment, is a key actor in delivering the strategy. It intends to provide more than EUR 75 billion of financing over the next three years in support of the strategy and the wider energy transition. InvestEU is meant to amplify that firepower, particularly in higher-risk segments.

What the strategy actually does

In practical terms, the strategy is organised around four actions.

1. Strengthening grid operator balance sheets

Grids sit at the centre of the strategy.

The Commission and the EIB Group want to ensure that transmission and distribution operators can fund major infrastructure upgrades without overstretching their balance sheets. To do that, they propose three main tools:

- A Strategic Infrastructure Investment Fund (SII Fund), with an indicative EIB commitment of up to EUR 500 million to co-invest alongside private infrastructure funds.

- An Operator Securitisation Facility, designed to turn future regulated revenue streams into immediate liquidity without transferring physical ownership of the assets.

- Wider use of hybrid bonds, which are treated partly as equity and may help regulated operators raise capital while preserving credit quality.

2. Expanding credit for smaller operators and freeing up bank capacity

In the second action, the Commission wants to explore loan securitisation and intermediated lending structures that would allow commercial banks to free up balance sheet capacity and extend fresh loans to grid operators, including smaller local players.

It also sees a role for regional and local banks in aggregating projects and financing smaller operators in a still highly fragmented EU distribution landscape.

The point is to unlock more lending without relying directly on additional fiscal subsidy.

3. De-risking newer technologies and widening the investable universe

The third one is the broadest action in the strategy. The Commission and the EIB Group want to step up support for next-generation clean-energy technologies that still struggle to attract conventional capital on acceptable terms. That includes long-duration energy storage, floating wind, floating solar, ocean energy, agrivoltaics, advanced bio-based renewable solutions, CCS/CCUS and geothermal projects facing specific development risks.

It also introduces a more explicit cybersecurity lens for financed technologies where the EU depends on higher risk third-country providers.

The scope extends to small modular reactors and advanced modular reactors, where the Commission sees a need to de-risk early commercialisation and associated fuel-cycle and supply-chain assets.

- Beyond project finance, the strategy reaches scale-up capital too: the Commission wants to use tools such as venture debt, equity operations and investments funds, including InvestEU-backed institutions, as well as the Scaleup Europe Fund, to support the commercialisation of innovative energy companies.

Energy efficiency also sits squarely within this action.

The Commission and the EIB Group plan to strengthen financing for SME decarbonisation and launch, in 2026, a pilot aimed at leveraging EUR 500 million for “energy efficiency as a service” models. It also wants to support project aggregation so smaller efficiency investments can access capital markets more easily.

In parallel, Member States are being pushed to use national schemes more coherently so public money is not duplicated or deployed inefficiently across the bloc.

4. Creating a permanent investor dialogue

The fourth action is institutional. The Commission will establish an Energy Transition Investment Council bringing together investors, financial institutions, Member States and senior Commission officials, with a sub-group that also includes the EIB Group, other international financial institutions and national promotional banks.

The idea is to create a standing forum where policy design, funding frameworks and market reality can meet more directly.

The first meeting is scheduled for Q2 2026.

What this means for your next deal

If it works as intended, it should make the market more receptive to structures that sit between classic project finance and direct public support: co-investment platforms, securitisation, hybrid capital, guarantees, aggregation vehicles and other de-risking tools.

For sponsors, lenders and investors, the message is straightforward. Europe is trying to make clean-energy projects more bankable, not merely more subsidised. That has direct implications for grid assets, storage, technology platforms, utilities with large capex pipelines and managers able to structure blended finance efficiently. In the next phase of the transition, the projects most likely to move first will be those combining regulatory visibility, credible risk allocation, grid readiness and financing structures that private capital can efficiently absorb.

Battery storage

- Finland | Prime Capital acquires 125 MW Tuovila BESS project from Aurinkokarhu, expanding Finnish energy storage portfolio with third acquisition in rapid succession

- Finland | Usva Energia sells 100 MW ready-to-build BESS project in Teuva to Prime Capital, recycling capital to accelerate Nordic energy storage pipeline

- Romania | Nuvve expands OMNIA Global partnership with 60 MW/120 MWh BESS project in Brașov, scaling European battery portfolio beyond 150 MW across three countries

Solar

- Finland | Skarta Energy sells Pyhäsalmi solar park to Solarigo Systems, completing divestment as part of strategy to focus on larger-scale solar developments

- Germany | Pacifico Energy fund acquires 24.4 MWp operational solar park in Schleswig-Holstein, expanding portfolio under Energy Invest Mittelhessen 1 vehicle

- Poland | Airengy agrees to acquire 33.3 MW solar portfolio from INVL for ~€24 m, marking entry into European generation and underpinning solar-plus-storage platform strategy

- Poland | Virya Energy acquires 63 MW solar project portfolio from Eneoz, expanding newly established Polish platform and advancing development pipeline

- United Kingdom | Capital Dynamics acquires 63 MWp Fleet solar project in Hampshire from BayWa r.e., expanding UK solar portfolio and supporting energy security and decarbonisation targets

Solar + BESS

- Europe | Atrato Onsite Energy merges with Finlight to form ~700 MW distributed solar and battery platform backed by Brookfield, creating a leading C&I generation company across key European markets

- Ireland | GridBeyond raises €12 m equity round with Samsung Ventures participation, supporting global expansion of AI-driven optimisation platform for distributed energy assets

- United Kingdom | Good Energy acquires solar and battery installer Low Energy Services, expanding C&I installation capabilities and regional presence in Scotland and North East England

Wind

- Denmark | Eurowind Energy agrees to acquire Connected Wind Services Denmark from EnBW, strengthening wind operations and maintenance capabilities across Northern Europe

- Finland | Cloudberry Clean Energy acquires 50% stake in 132 MW onshore wind farm from Sampi Renewables, marking entry into Finnish market and strengthening Nordic generation portfolio

- France | Q ENERGY acquires stake in Pennavel floating offshore wind project, strengthening consortium to advance development of Brittany offshore wind farm

- Germany | Trianel and BMR form partnership to develop and operate 100 MW onshore wind portfolio in North Rhine-Westphalia, combining development and operational expertise

- Germany | Triodos Energy Transition Europe Fund sells remaining 50% stake in 34.5 MW Midlum wind farm to Enova Value, enabling full ownership and portfolio integration

- Greece | Aquila European Renewables completes €26 m sale of 40 MW Desfina wind farm to Aquila Capital funds, advancing managed wind-down and returning capital to shareholders

- United Kingdom | Boralex acquires 58 MW Upper Ogmore and Tom na Clach Extension onshore wind projects from RES, Marubeni and Infinergy, expanding UK development pipeline