Daniel Black

Daniel Black

Central banks on both sides of the pond voted to keep interest rates steady this week, citing renewed inflationary pressures from the US-Israel war with Iran. The Bank of England even hinted that it might consider a rate rise this year if the situation worsens.

Elsewhere in our rumour mill:

- Banks are to net £83m in fees from the Schroders sale

- The UK might be losing its crown as the centre of European dealmaking

- Deutsche Bank MD bonuses are up 60% in two years

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Mastercard embraces digital future with $1.8bn bet on stablecoin infrastructure firm BVNK

- Embecta to buy Owen Mumford for up to £150m

- WisdomTree to buy Atlantic House for £150m

- ‘Centre of gravity’ of European M&A market shifting out of UK

- Schroders sale nets Wells Fargo, other banks £83m in fees

- BNP Cardif is said to near deal for Warburg Pincus stake in IndiaFirst Life Insurance

- Unilever and Kraft Heinz held talks over food merger uniting ketchup and mayo

- SpaceX Investor Baillie Gifford hails pre-IPO takeover of xAI

- Nordic Capital to buy majority stake in trade surveillance biz TradingHub

Industry news

Salaries and bonuses

- Jefferies cut its London pay after profits rose 40%

- Deutsche Bank MD bonuses are up 60% in two years, but there’s a catch

Job moves

- HSBC considers up to 20,000 job cuts through AI overhaul

- Close Brothers to cut 600 jobs as it faces down motor finance compensation bill

- Citigroup UK M&A head Evans joins Takeover Panel

- Standard Chartered hires Low to lead oil and gas M&A

- LSEG shakes up European equities trading leadership

- Dozens of candidates vie to lead UK’s new foreign investment office

- Top Flow Traders UK executive departs market-maker

- Senior Bank of England staff among departures in resignation scheme

Market trends

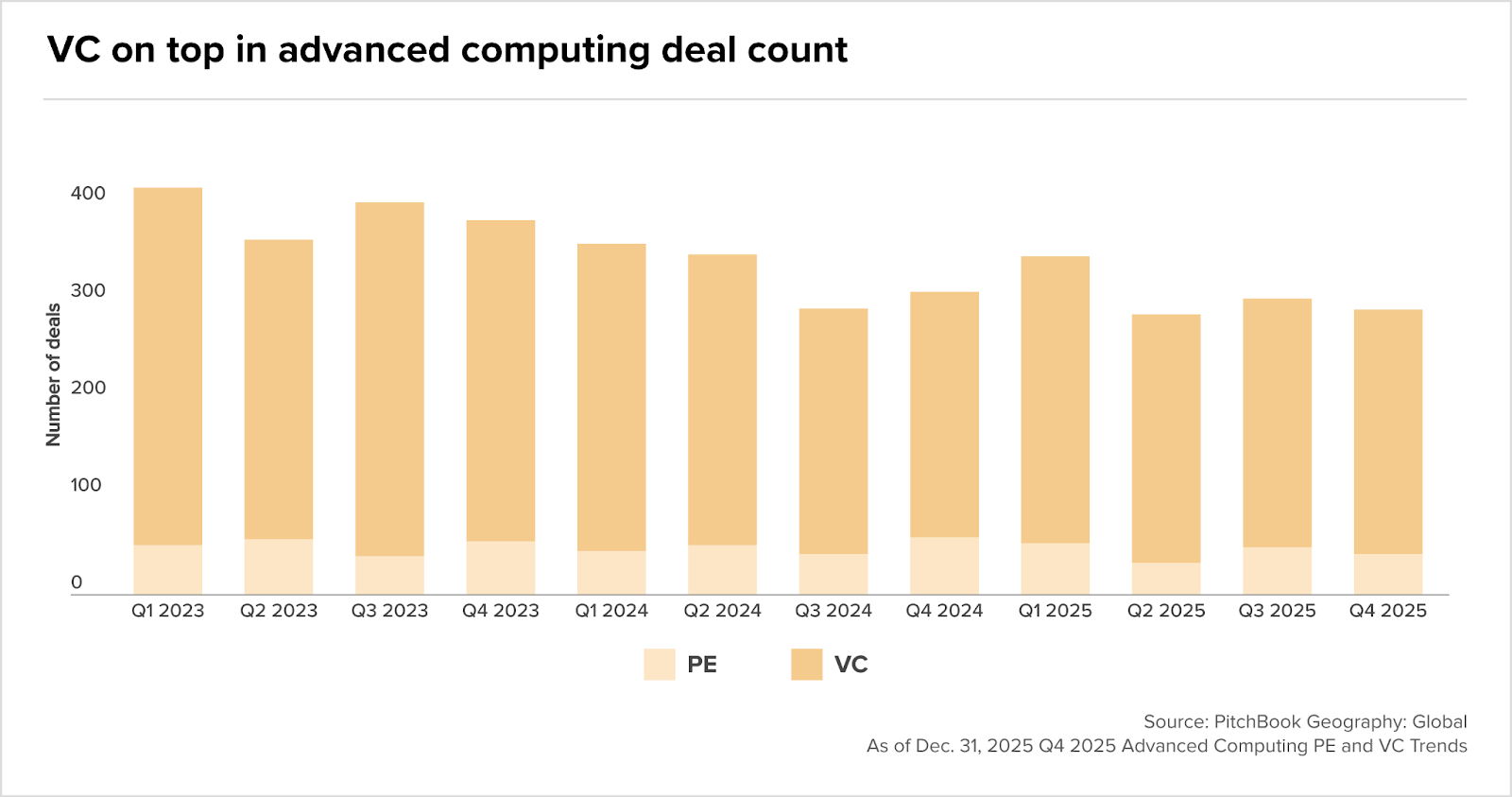

Behind every AI model is a data centre, and behind every data centre is a PE firm

According to PitchBook’s recent data, venture capital dominated advanced computing dealmaking in Q4 2025, accounting for 86% of transactions, yet captured just 16% of total deal value, a figure well below its five-year historical average of 29%. Private equity, with just 42 transactions, deployed $44.9bn of the sector’s $53.5bn total.

Data centre investment hit $48.1bn in the quarter, up from $13.2bn the period prior, driven by the kind of cheques that only a handful of institutions can write. BlackRock and Abu Dhabi’s MGX anchored a $40bn acquisition of Aligned Data Centers; Blackstone put $1.2bn into a power plant built specifically to keep AI workloads running.

What we’re seeing is an emergence of a two-tier market, with VC backing the software layer and PE quietly becoming the landlord of the infrastructure underneath it.

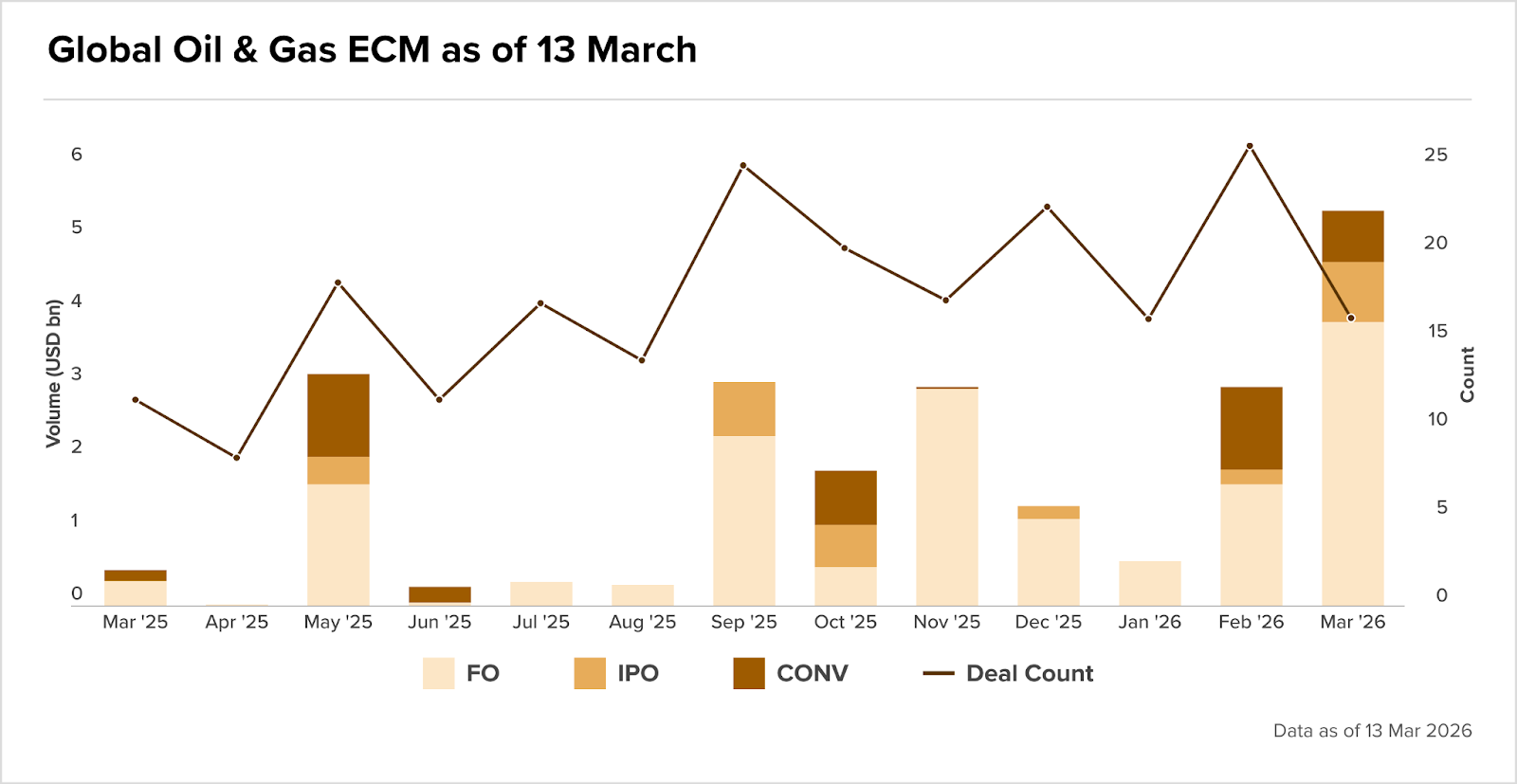

Crude at $114 – good for equity issuance, not so for dealmaking

That appetite for physical AI infrastructure runs headlong into a commodity market in upheaval.

Data centres rank among the heaviest consumers of fossil fuel-derived electricity, and with Brent crude, the global oil benchmark, having climbed from $101/bbl on 13 March to $114.91/bbl today, input cost assumptions across the sector are being repriced faster than most models can absorb.

Most dealmakers are in a holding pattern as a result, with valuation gaps between buyers and sellers widening.

For oil and gas investors, however, the volatility has created a different kind of opportunity. According to Dealogic data cited by Mergermarket, March 2026 had already produced $3.86bn in follow-on equity volume by mid-month, more than any complete month in the past year.

Lyndal Stephens Greth’s $1.9bn sale of a 3.91% stake in Diamondback Energy led the charge, with Encap, Oaktree and Diamondback itself engineering a $798m sell-down in Viper Energy days earlier.

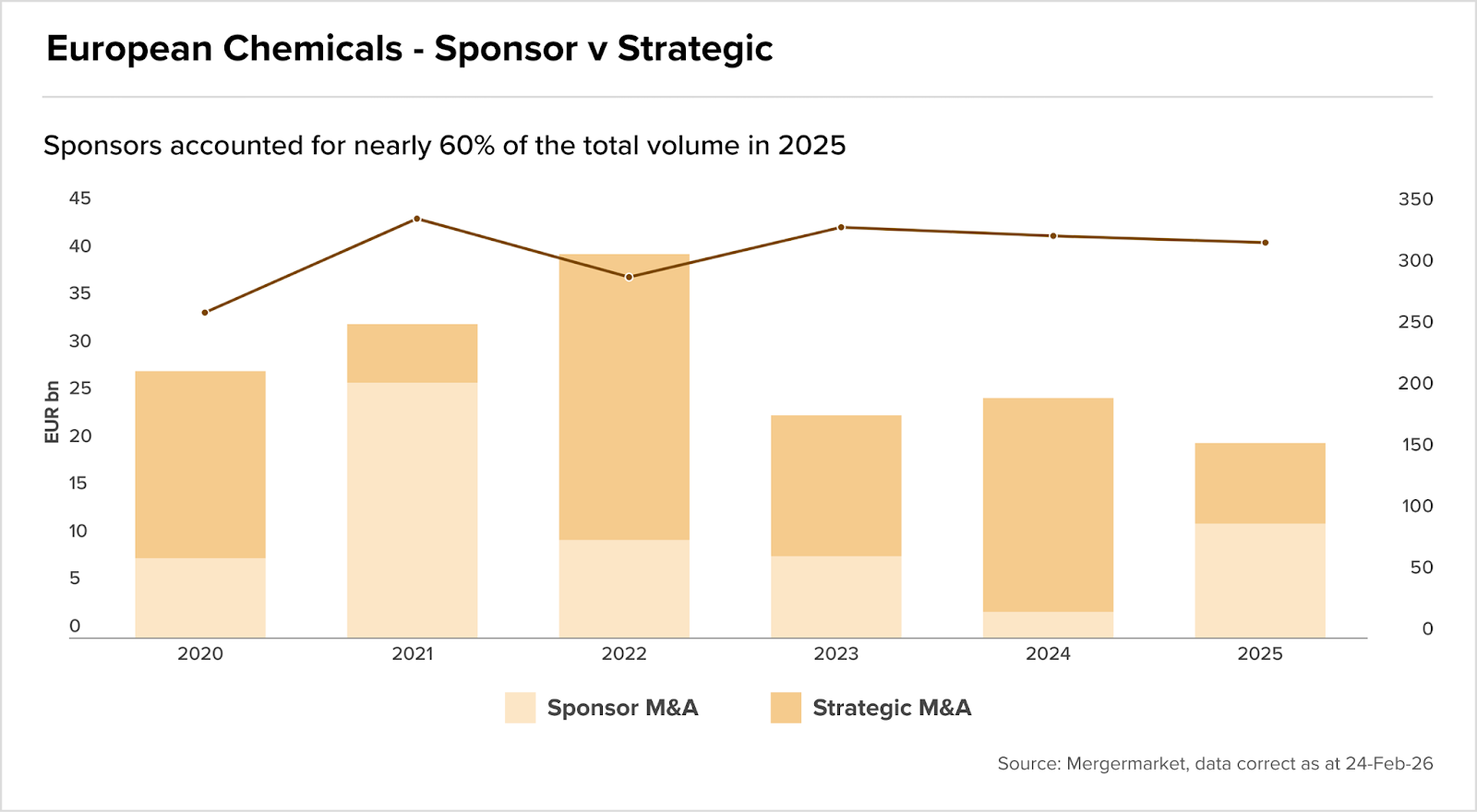

Sponsors are buying what strategics find too toxic to hold

The same crude price shock rattling oil and gas dealmakers is adding a new layer of risk to an already fraught corner of European M&A.

Europe’s chemicals sector has been under sustained pressure from energy costs, overcapacity and low-cost Asian competition, and PE has been moving in precisely because of it. PE buyouts of European chemicals assets surged to €12bn in 2025 from €2.6bn the year prior, the highest volume since 2021, based on Mergermarket data.

Sponsors accounted for nearly 60% of total deal volume, as strategic activity collapsed from €22.7bn in 2024 to €8.5bn, with incumbents focused on divesting non-core assets rather than acquiring them.

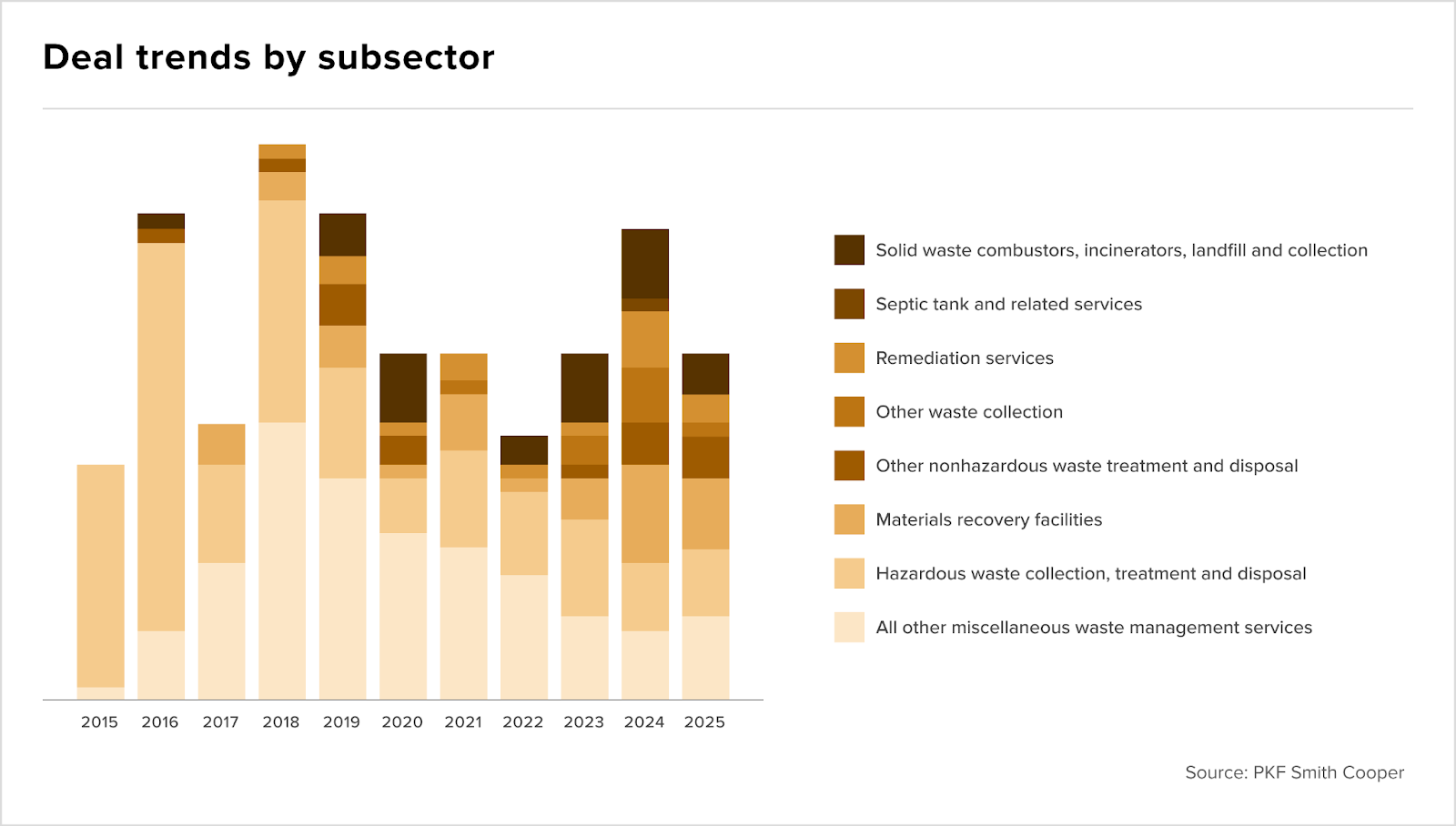

Diversification in UK waste market

UK waste sector deal volumes fell from 33 to 25 between 2024 and 2025, though PKF Smith Cooper’s read is that investor focus has shifted rather than retreated. Battery recycling, WEEE processing and materials recovery were near-absent from the subsector mix before 2018, but they now account for a meaningful and growing proportion of transactions.

Fundraising

IPOs