Sebastian Montoya

Sebastian Montoya

This week, we look at data released by DLA Piper to examine how renewables dealmakers are thinking and where their priorities lie in 2026.

Also, this week’s latest M&A deals suggest that more measured planning and long-term positioning were central considerations for those closing transactions during the period.

Key highlights include:

- NextEnergy Solar Fund sold a 100 MW operational solar portfolio in the United Kingdom to Atrato Onsite Energy. The transaction was valued at EUR 46.2m and marks the completion of NESF’s Capital Recycling Programme. The value will primarily be used to reduce short-term debt and strengthen the fund’s balance sheet.

- Prime Capital acquired the Pyhäsalmi BESS project in Finland. With a storage capacity of 85 MW / 170 MWh, the project was valued at EUR 5.5m. The asset will be used for frequency regulation and energy arbitrage, serving as flexibility infrastructure for the Finnish grid.

- Zenith Energy acquired a portfolio of agrivoltaic solar projects in Italy with a combined capacity of 28 MWp for EUR 2m. The relatively low valuation per MW reflects the fact that these are early-stage pipeline assets rather than operational projects. Through the transaction, Zenith aims to expand its pipeline as part of its strategy to reach 200 MWp of installed solar capacity.

Want more insight?

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Energy M&A in the UK Cocktails & Conversations

The UK energy and infrastructure market is attracting global attention.

Join us at Black Lacquer at Hyde London City, a subterranean cocktail bar with signature drinks and smoky jazz, to discuss its implications during an exclusive networking evening.

Deals breakdown

Far beyond the green agenda, energy transition M&A makes business sense

What are renewable energy dealmakers prioritizing?

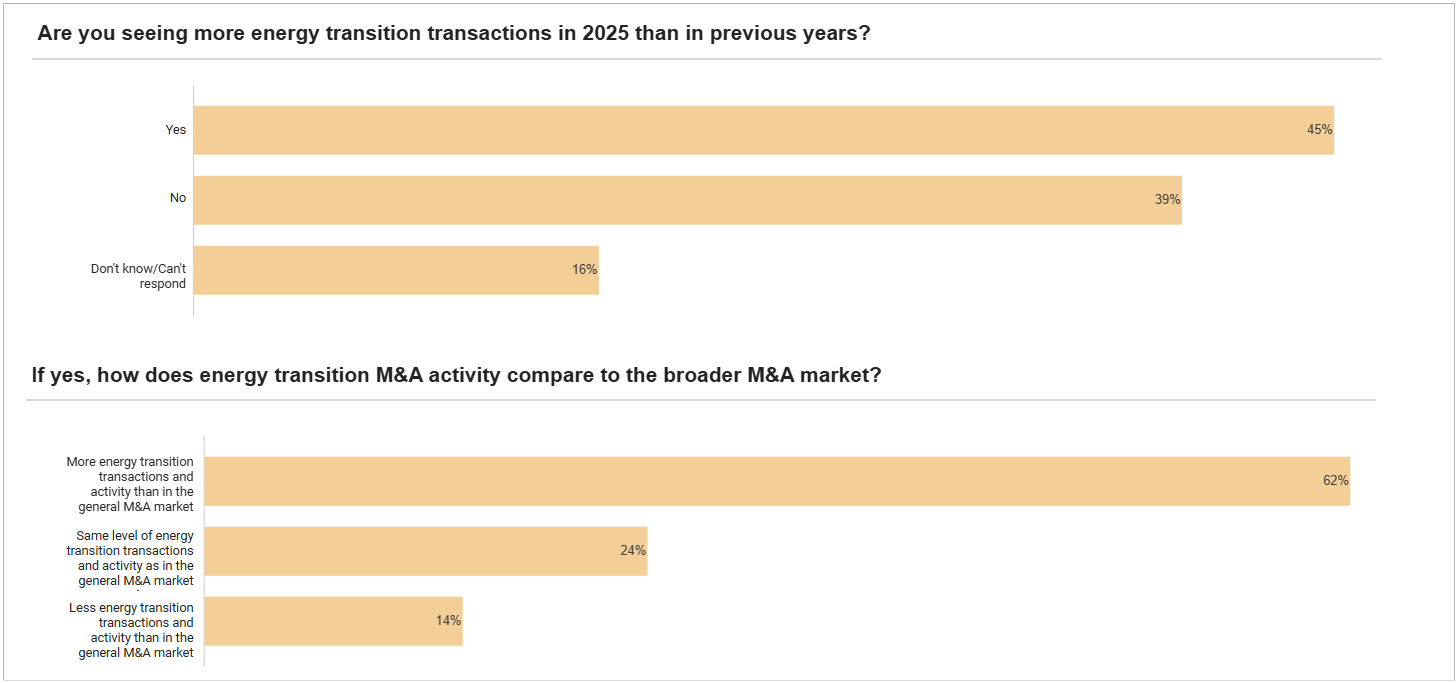

Data from DLA Piper’s Energy Transition M&A Report 2026, released in the second week of February, suggests that industry professionals are navigating a mix of optimism and uncertainty. Above all, however, they see the sector as one of the busiest corners of M&A.

That impression remains even after overall energy transition deal volume fell 15% in 2025. Renewable generation, in particular, saw volume fall 27%.

At the same time that deal count may have eased, the largest group of respondents (45%) still felt 2025 was busier than previous years. Among those already seeing more activity, 62% said energy transition was moving faster than the wider M&A market.

Clean energy M&A is commercially driven

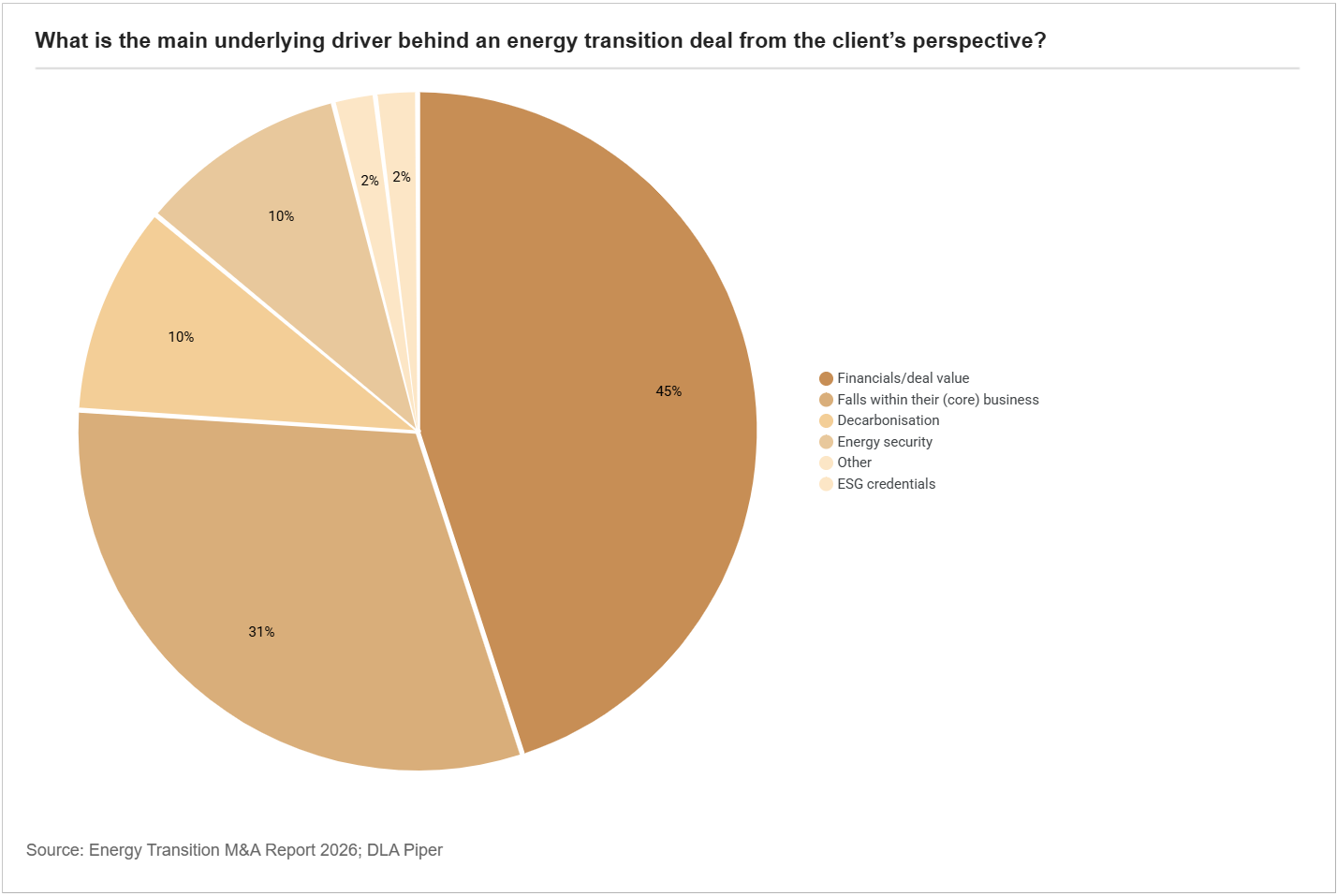

That sense of momentum has clear commercial roots. For 45% of respondents, the main driver behind deals was financials and valuation. Another 31% pointed to alignment with the buyer’s core business. Energy security and decarbonization accounted for 10% each.

That leaves little room for the old idea that the energy transition is mainly an environmental agenda carried by weak economics. Sustainability remains the obvious benefit of clean energy, but dealmakers increasingly treat the sector as an economic imperative.

Beyond the numbers, the sector is also a useful lever for companies looking to strengthen their business models. There are several examples, but one of the clearest in Europe in 2025 came from outside the energy sector itself.

- The investment arm of Ingka Group, IKEA’s largest retailer, acquired an operating portfolio of three solar parks in the Netherlands, with 76.3 MWp of capacity and estimated annual output of 67 GWh.

- The detail that best captures the logic behind that move is that these were mature, profitable assets, with more than five years of operating history. It was a global company treating renewable energy as a strategic asset, one able to combine returns, predictability and operational resilience.

- That is no coincidence. Ingka says it has committed EUR 7.5 billion by 2030 to renewable generation assets and technologies that support the transition.

Two factors, one serious bottleneck

Two factors stand out.

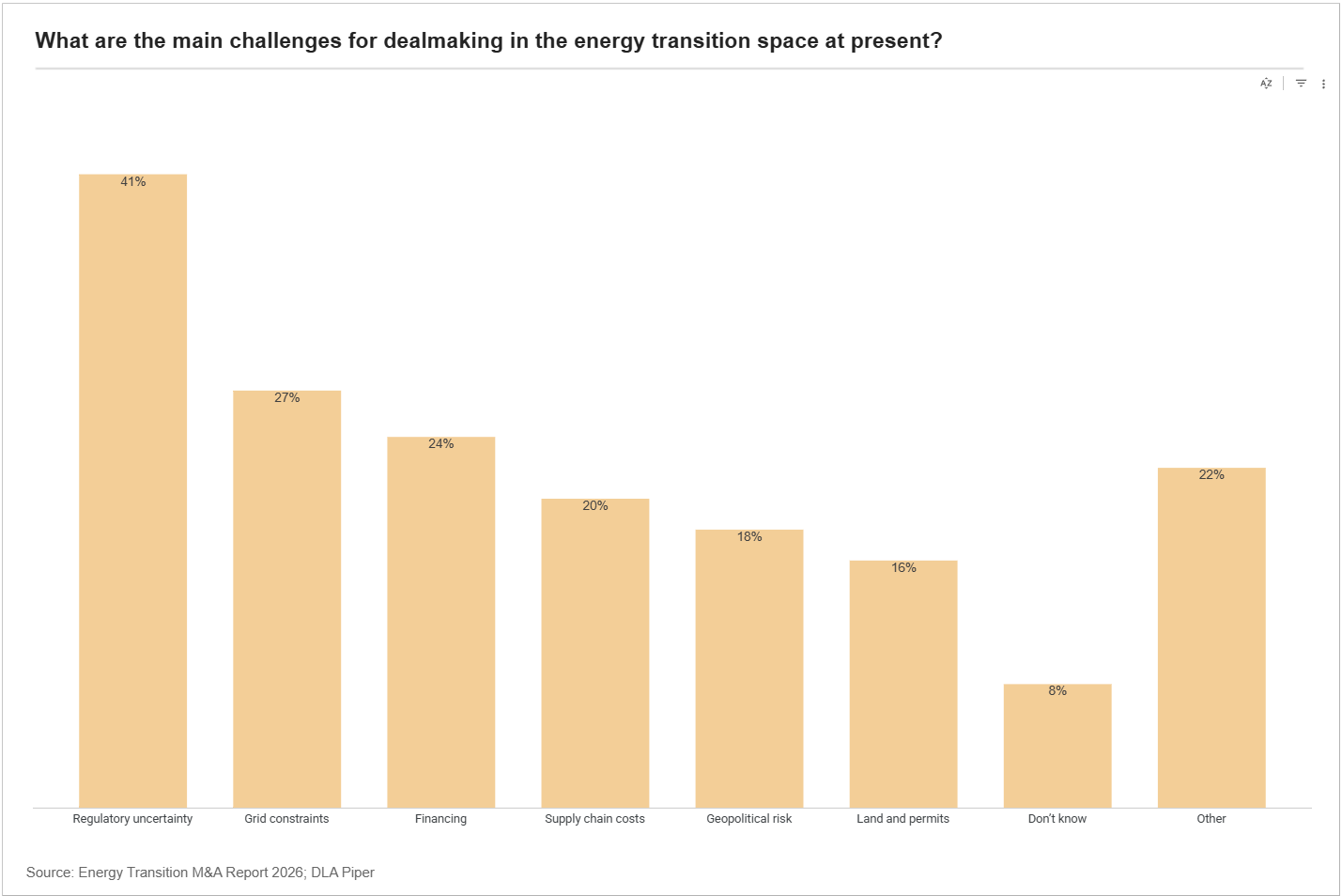

First, regulatory and policy uncertainty remain the main obstacle. The report says 41% of respondents see it as the biggest challenge. We have covered some of these points in earlier editions of Teaser Energy Europe.

So in practice, the market can generate interest and capital, but regulation and policy uncertainty turns the job of delivering supply and properly operating assets harder than it should be.

Some regional examples include:

- In the UK, the long review of electricity market design only ended in July, when the government dropped zonal pricing to restore predictability before the next CfD round.

- In the Netherlands, the government delayed 2 GW of offshore wind tenders after admitting that the zero subsidy model no longer worked for developers, then softened tender criteria and began studying support mechanisms to rebuild the business case.

- In Germany, a 2.5 GW auction received no bids for the first time, with the ministry itself pointing to auction design, site risk and volatility in prices and PPAs.

- In France, the political crisis delayed PPE3 and fresh tenders. A 1 GW round received no bids in part because of uncertainty around state support, while RWE said it intended to leave a winning 1.5 GW consortium because the relative value of the project had deteriorated.

In a market that is increasingly commercially driven, when investors cannot see the pricing regime, the timeline or planning certainty with enough clarity, capital asks for a discount.

The fall in deal volume reinforces that mood. It points to greater selectivity and slower closing timelines. DLA Piper says 86% of respondents have already seen these types of constraints slow projects.

That is enough to push the issue ahead of more familiar obstacles such as capital availability, inflation and geopolitical risk. In many cases, money and enthusiasm are not the problem.

Regulatory uncertainty is matched by infrastructure limits. Grid and interconnection constraints are the second biggest complaint, cited by 27% of respondents.

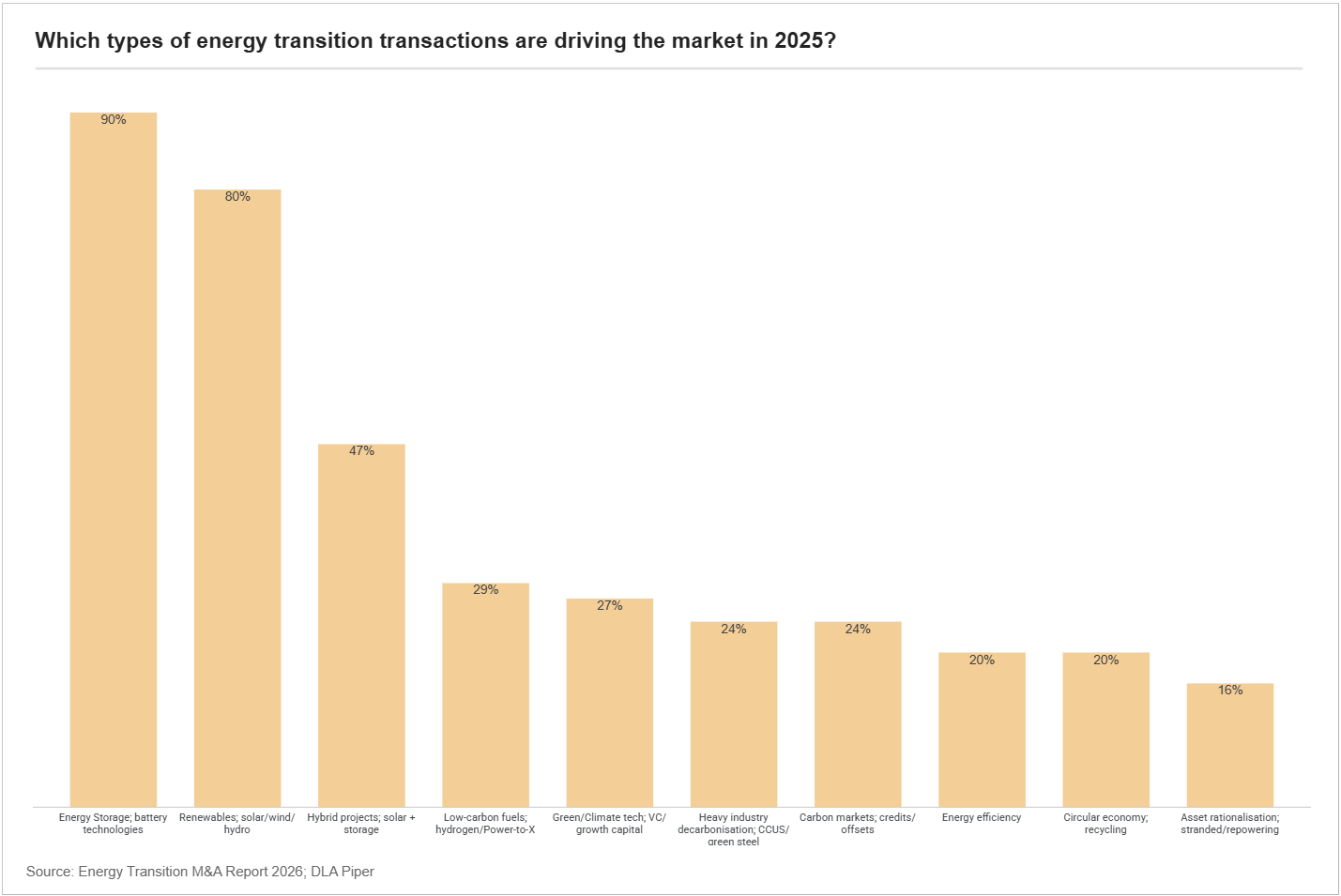

In that environment, storage solutions and hybrid projects naturally attract attention. They help over the medium and long term, especially where curtailment is a recurring problem, but they also raise a harder question about balance. After all, there is a thin line between investing more to improve project viability and actually expanding generation.

Operating in this sector is becoming a precision exercise. Grid availability, regulation and financing all increase the risk of higher CAPEX and demand a stricter view on project viability.

For anyone following the market, there is no shortage of deals that show how sharp the clean energy dealmaker has become. The challenge is considerable, dealmaker, but the upside is larger still.

Battery storage

- Finland | Fu-Gen agrees to sell 15 MW ready-to-build battery storage portfolio to Icecreek Energy, marking the buyer’s entry into the Finnish BESS market

- Finland | Prime Capital acquires 85 MW/170 MWh Pyhäsalmi battery storage project from SENS and Dovre Group for ~€5.5 m, enabling capital recycling for further BESS development

- Romania | Alive Energy acquires 82.8 MW/181 MWh Green Storage Farm BESS project, advancing ready-to-build battery development to support grid flexibility

Retail/Grid Network

- France | BKW enters talks to acquire 65% stake in green electricity supplier Volterres from Sun’R, expanding presence in French renewable power supply market

- Spain | OSW invests in Spanish solar distributor Soleme, marking entry into Spain and strengthening supply chain for distributed solar and storage solutions

Solar

- Germany | Nuveen’s NECRI fund acquires 70.4 MWp solar park in Brandenburg from Trianel, expanding European core renewables portfolio with operational German PV asset

- Italy | Zenith Energy acquires 10 MWp solar development project in Puglia, expanding renewable energy portfolio in southern Italy

- Italy | Zenith Energy buys 28 MWp agrivoltaic solar development projects in Piedmont for ~€2.0 m, expanding pipeline toward 200 MWp solar target

- United Kingdom | NextEnergy Solar Fund sells 100 MW UK solar portfolio to Atrato Onsite Energy for £46.2 m, completing capital recycling programme and reducing short-term debt

Wind

- Australia | Iberdrola completes acquisition of 242 MW Ararat onshore wind farm in Victoria from Partners Group and OPTrust, expanding Australian renewables portfolio and securing contracted generation capacity

- France | Nadara acquires wind turbine maintenance specialist Talveg, strengthening in-house O&M capabilities across its European wind portfolio

- Poland | RWE completes sale of 350 MW F.E.W. Baltic II offshore wind development project to PGE, transferring full ownership and related environmental decision for adjacent Baltic site