Daniel Black

Daniel Black

With all eyes on the Middle East, it’s been a relatively quiet week for the UK’s M&A rumour mill.

Bloomberg reports that the US-Iran war has caused dealmakers to pause activity while they assess the long-term impact and risks, though there’s no evidence of deals being taken off the table completely.

And in other news this week:

- CVC sports empire signed a €3.5bn debt deal after stake sale falters

- Axel Springer is to buy the Telegraph in a £575m deal

- Savills agreed to buy Eastdil Secured in a $1.1bn deal

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Dealmakers see Iran War stymieing M&A with delays, diligence

- CVC sports empire signs €3.5bn debt deal after stake sale falters

- Virgin Media O2 owner eyes broadband deals to take on BT Openreach

- Axel Springer buys Telegraph in £575m deal

- MFS Creditors facing £1.3bn shortfall allege improper loans

- Savills agrees to buy Eastdil Secured in $1.1bn deal

- Haleon CEO Targets China, India growth with new plant, M&A push

- UK’s Hill & Smith to acquire Freeberg Industrial Fabrication

- CVC reportedly considering buying minority stake in Belgian bank Belfius

- Shell to offload Jiffy Lube to Monomoy Capital for $1.3bn

Industry news

- Bank of England to hold rates in March, cut twice this year but timing unclear: Reuters poll

- Sterling sinks for third day as oil crisis burnishes dollar

- UK’s FTSE indexes rebound on Middle East de-escalation hopes

Salaries and bonuses

Market trends

Europe’s restructuring advisers closed 2025 on high note

Debtwire’s Restructuring Advisory Mandates Report has tracked advisory roles awarded to restructuring professionals across distressed situations in Europe. In 4Q25, 76 new mandates were awarded across 30 situations involving EUR 43.5bn of debt, a 49% increase on the prior quarter.

However the full year picture is less encouraging. 2025 recorded 274 mandates across 94 situations against 449 in 2024, a 39% decline, and the EUR 130.5bn of advised debt is heavily skewed by the Altice complex.

The UK was the standout country by mandate count, generating 99 new mandates from 32 situations involving EUR 22.4bn of debt across 2025, reflecting both sponsor-backed deal density and a well-established advisory bench. Two 4Q25 situations capture the nature of the stress: Lowell Group returning to restructuring within months of completing a prior process, and Gigaclear heading towards a lender-led takeover after a failed sale.

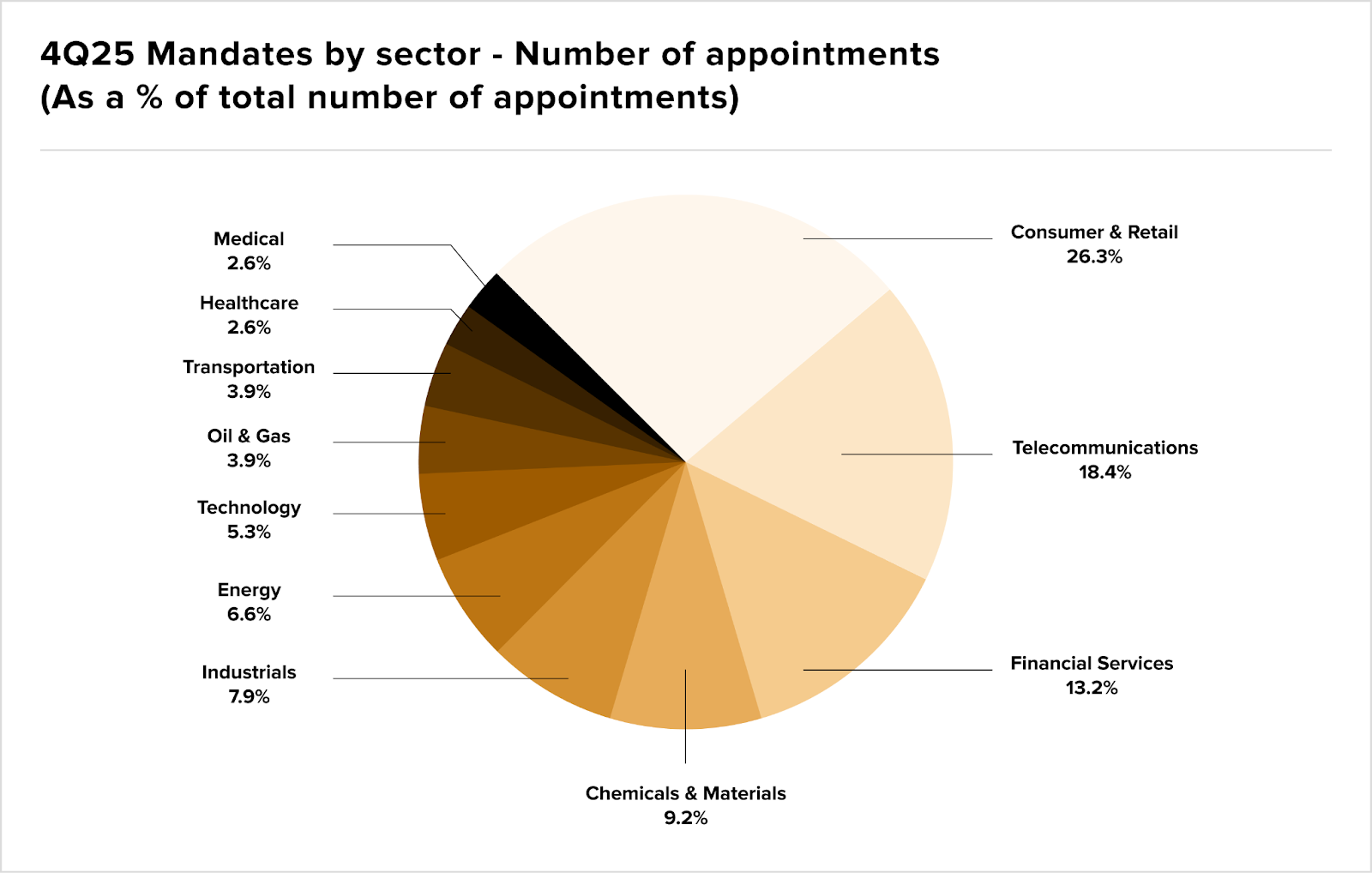

Consumer & retail dominated 4Q25 appointments at 26.3%, followed by telecoms at 18.4% (driven largely by the Altice International and Altice France restructurings). Together with financial services and chemicals & materials, these four sectors accounted for roughly two-thirds of all mandates in the quarter.

Financial services lead again

Speaking of sectoral breakdowns, Herbert Smith Freehills’ February M&A Update shows financial services accounting for two of the three firm offers announced in the month: Nuveen’s £9.9bn recommended cash offer for Schroders and Verdane’s £185.7m bid for Augmentum Fintech are both targeting the sector.

Firm offers in financial services rose from seven in 2024 to 16 in 2025, making it one of the most consistently active sectors in the UK public M&A market.

PE exits in the pipeline

MarshBerry’s data adds further texture to the February picture. Six transactions concentrated in asset and wealth management, headlined by Nuveen’s acquisition of Schroders and NatWest’s £2.7bn acquisition of Evelyn Partners, pushed aggregate deal values to a single-month record.

At 14 transactions year-to-date however, volume remains modest against prior years, and two of the six deals were private equity exits from 2021-2022 vintage funds. More of those are coming as holding periods mature.

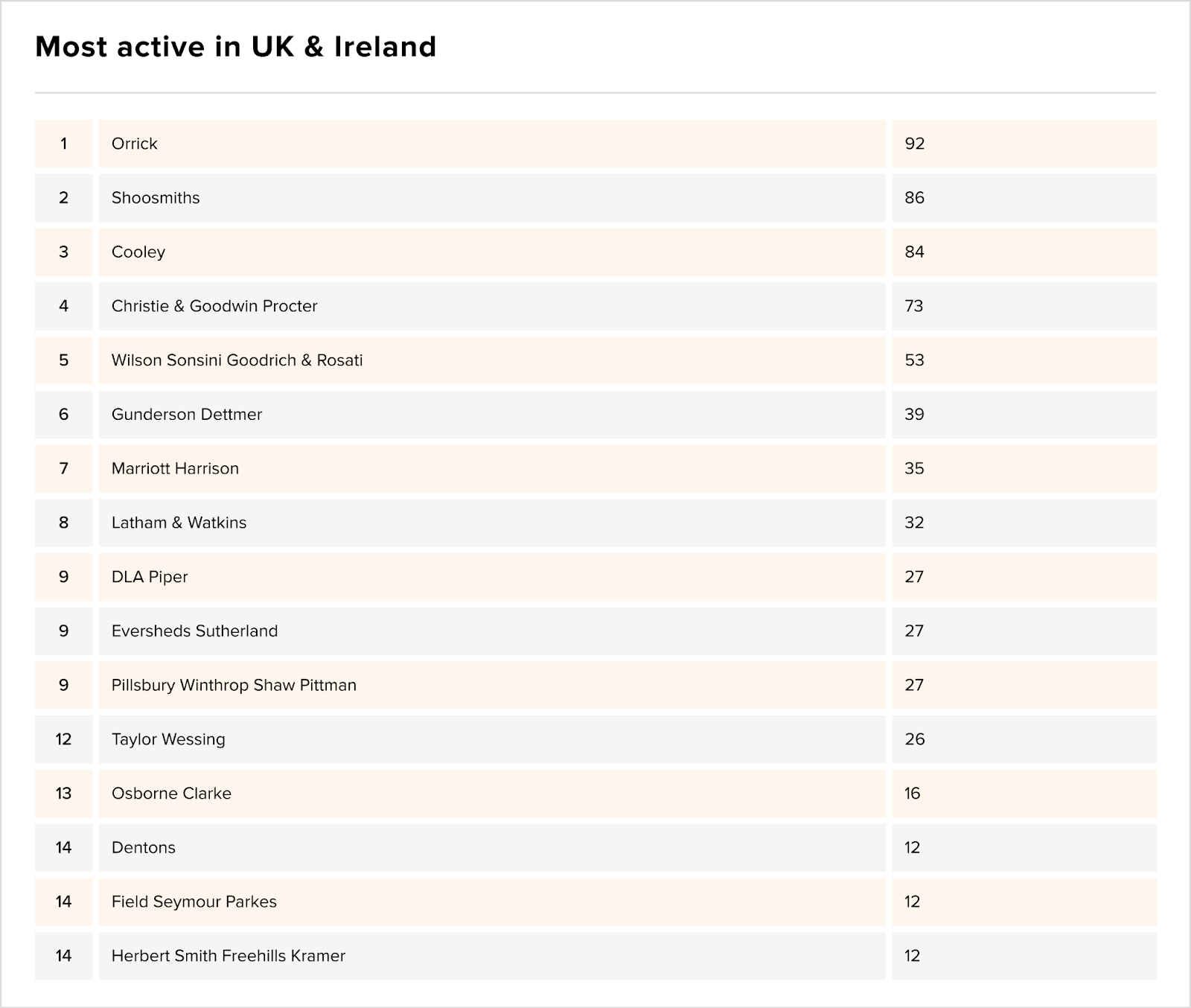

Who led the legal ranking for UK and Ireland VC deals in 2025?

On the legal side, Orrick topped PitchBook’s 2025 rankings with 92 deals, narrowly ahead of Shoosmiths on 86 and Cooley on 84. The top three are notably US-heavy, reflecting the continued dominance of transatlantic firms in the UK venture market. Congratulations to all firms that featured.