Sebastian Montoya

Sebastian Montoya

In this week’s Teaser Energy Europe, we analyze reports from organizations such as the IEA and Eurelectric to identify the hottest asset classes in Europe’s renewable energy landscape.

BESS, hybrid projects and onshore wind all make the list, reflecting the sector’s strategies to balance ambition, security and renewable energy targets.

And don’t miss this week’s latest deals either:

- TotalEnergies agreed to sell a 50% stake in a 789 MW German battery storage portfolio to AllianzGI as part of a €500m investment programme covering 11 BESS projects under construction, while retaining operatorship and deepening its capital-recycling strategy in European flexibility assets.

- EBRD committed €85m in equity to Virya Renewables Poland to support the development and acquisition of a large-scale solar pipeline, anchored by the 722 MWp Sidłowo project, one of the country’s most significant PV developments currently advancing through permitting and construction stages.

- CriteriaCaixa agreed to invest €611m to raise its holding in Spanish utility Naturgy to 28.5%, buying out Global Infrastructure Partners’ remaining stake through an accelerated bookbuild and reinforcing its role as the company’s core long-term shareholder.

Want more insight?

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

Renewable assets to watch in Europe in 2026

An interesting way to describe renewable energy dealmaking is to call it the post-scale era. On one side, projects are moving fast. On the other, valuation anchors are changing.

- According to the Power Barometer 2025 report, low carbon sources accounted for 72% of European power generation in 2024.

- In 2025, wind and solar reached 30% of EU electricity, above fossil fuels.

This is a market that signals both ambition to expand and environmental commitment. But this success seems to have changed the hierarchy of value.

The report also suggests that the more Europe installs solar and wind, the more the premium moves away from pure megawatts and towards the ability to bring shape, firmness and predictability to revenues. In a previous edition of Teaser Energy Europe, we explored some of the factors behind this equation.

Today, we are talking about how this shows up in the hottest assets in the sector for 2026, and what signals matter if you want to adjust your strategy.

1. Batteries and hybrid systems

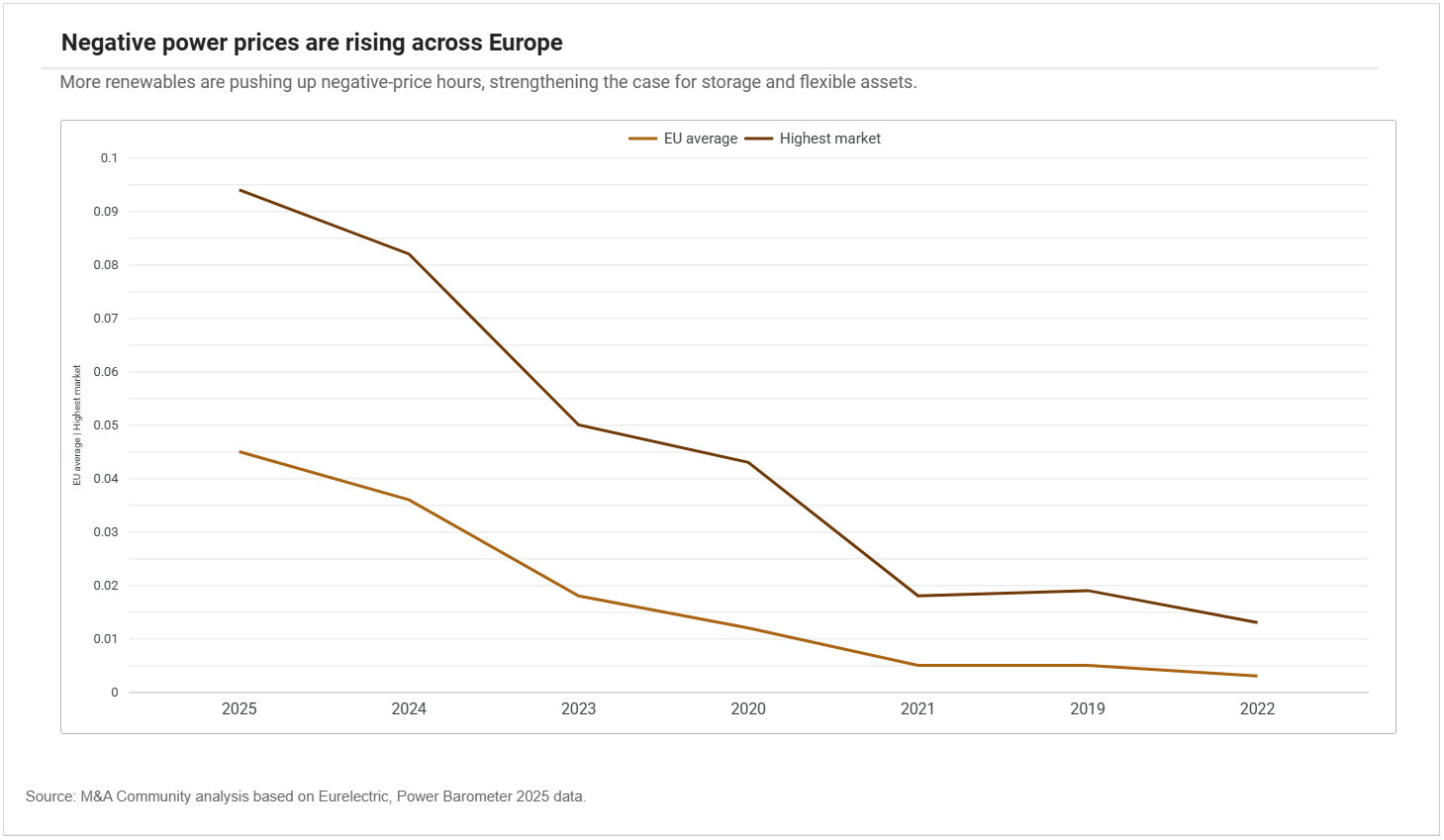

Price volatility is a challenge, and it is hard to find a dealmaker who has not run into it at some point in a negotiation. Negative prices were recorded in 4.5% of hours in 2025, compared with just 0.5% in 2019. The erosion of capture prices has started to penalise solar assets that are too exposed to the spot market.

That is why utility scale batteries and hybrid solar+BESS or wind+BESS projects move to the top of the list. According to Pexapart’s “Solar takes top spot in the EU for the first month ever” report, by the end of 2024, the EU had 5.4 GW of utility scale BESS installed.

Estimates pointed to more than 13 GW operational by the end of 2025 and 30.5 GW planned for the coming years.

More important than the scale is the economic role. Eurelectric itself estimates that co-located storage could add at least 15 percentage points to solar capture prices in Central and South Eastern Europe. Batteries are no longer an accessory to a renewable project. They have become a monetization tool, a hedge against volatility and a defence for valuation.

2. Onshore wind repowering

The second class of hot assets is repowered onshore wind.

Here, we are talking about onshore platforms that are already derisked.

- In 2025, Europe added more than 19.1 GW of new onshore wind. That represented 90% of all new wind capacity installed, and 2 GW came from repowering. That helps explain why assets that come with a known resource, a mapped connection, an operating history and lower development risk tend to command a premium in 2026.

In a more selective market, repowering is not only about efficiency. It is an elegant way to reduce risk without giving up growth.

3. Utility scale solar

Utility scale solar remains relevant, but only when it comes dressed for the new market: with a PPA, with storage or with a valuable connection.

The IEA revised upwards its European outlook especially for utility scale solar in Germany, Spain, Italy and Poland, driven by corporate PPAs. At the same time, the agency highlights the expansion of market based mechanisms and bilateral contracts in new renewable capacity, while Eurelectric points to growth in multi technology PPAs and deterioration in capture rates.

The takeaway? In 2026, the solar assets that stay hot are contracted and combined. Pure merchant solar, in a congested node, cools down quickly.

4. Offshore wind

Offshore wind enters this conversation with an asterisk.

The fragile side is well known. WindEurope warned at the end of 2025 about failed auctions in Germany, France, the Netherlands, Denmark and Lithuania, and about a business case that is clearly more pressured than it was a few years ago. But the positive side is also clear. When there is revenue visibility, capital responds.

Another example is the UK award in January of 8.4 GW of offshore wind in AR7. It was the largest offshore auction in Europe. The European Commission also approved a French scheme worth $11 billion to support offshore wind.

Offshore seems to remain attractive, but only when it arrives much more derisked, with a CfD or equivalent structure and a supply chain that is properly lined up.

5. Pumped storage and hydro flexibility

For many readers, seeing pumped storage and hydro flexibility on this list may come as a surprise. But an IHA agreement already suggests that this asset may be undervalued.

The reason is that its value can look old fashioned compared with the transition narrative, even though the system increasingly needs long duration flexibility.

That may be exactly why it deserves more attention.

How to choose the best strategy?

You already know the answer: it depends.

It depends on your objectives, the business, the synergies, the financing structures available, the incentives and the regulatory setting.

Rather than repeat the obvious, I will share the signal you should take into your strategy. It is this: do not think only about how much this asset generates. Think about how much system risk it removes.

The truly hot asset is the one that brings shape to the curve, firmness to the contract, flexibility to the grid and speed to the connection. That alone already points to much of this list.

Batteries, hybrids, repowering, pumped storage and offshore with a clear revenue floor fit that definition. Pure merchant solar, in saturated markets and without commercial protection, less and less.

In a Europe that already has renewables at scale, the premium is no longer in abstract green. It is in practical utility.

Battery storage

- Europe | PPC Group and METLEN Energy & Metals form 50:50 JV to develop up to 1,500 MW / 3,000 MWh battery storage portfolio across Romania, Bulgaria and Italy

- Germany | Flower acquires 63 MW/257 MWh ready-to-build battery storage project in Saxony-Anhalt from CCE, marking entry into the German market with utility-scale BESS

- Germany | TotalEnergies sells 50% stake in 789 MW/1628 MWh battery storage portfolio to AllianzGI, partnering on €500 m investment in 11 BESS projects under construction

- Spain | Return acquires 80 MW/318 MWh shovel-ready battery storage portfolio from Aquila Clean Energy, marking one of Spain’s first utility-scale standalone BESS portfolio transactions

- United Kingdom | S4 Energy agrees to acquire 30 MW battery storage project in Northwest England from Electric Land, expanding UK footprint and advancing pan-European BESS platform

Multiple

- Romania | Omnia Capital agrees to acquire Premier Energy’s majority stake in Alive Capital, restoring full founder ownership and positioning platform for renewable and storage expansion across Southeast Europe

- Spain | CriteriaCaixa increases stake in Naturgy to 28.5% for €611 m as GIP fully exits Spanish power and gas utility through accelerated bookbuild

Retail/Grid Network

Solar

- Germany | Quadoro and EB-SIM add 10 MWp Bodenrode solar park in Thuringia to QEEE fund portfolio, advancing construction-ready photovoltaic project

- Italy | A2A and Keynesia Energy partner to develop 100 MW portfolio of photovoltaic plants for business energy communities under KeyCER initiative

- Italy | BayWa r.e. sells 14.2 MWp C&I solar portfolio to NetOn Power, strengthening distributed energy solutions platform for industrial clients

- Poland | Virya Energy secures $99 m equity investment from EBRD to acquire and scale solar PV portfolio from Optima Wind, advancing large-scale project development in Poland

- United Kingdom | Downing acquires 42.5 MW Higher Witheven solar project in Cornwall, expanding ready-to-build solar portfolio ahead of planned 2027 grid connection

Wind

- Finland | DWS acquires 41.3 MW Maaselänkangas onshore wind farm in Oulainen from wpd Group, expanding European infrastructure portfolio with operational renewable asset

- France | Velto Renewables acquires 26.2 MW Haut Chemin 2 onshore wind farm from Q ENERGY in Haute-Marne, marking its first fully owned wind asset and expansion in the French market