Sebastian Montoya

Sebastian Montoya

INVITATION | Join M&A Community at Black Lacquer, Hyatt Regency London Blackfriars, for an exclusive evening of high-level networking and sharp market insight. Secure your place here.

—

Capital concentration is once again defining the European energy landscape.

This week’s flow of transactions shows investors doubling down on scale, contracted cash flows and grid-critical assets, even as development risk remains selective.

Alongside these transactions, this edition’s editorial takes a closer look at wind energy dealmaking across Europe and what it signals for capital allocation in 2026.

- Ardian just secured EU clearance for its €2.5bn acquisition of Energia, opening the door to the Irish electricity and gas markets and marking one of the most significant utility transactions in Europe this year.

- Nofar Energy is moving decisively into operating assets, agreeing to acquire a 45.9% controlling stake in Ellomay Capital at a USD 323m valuation, gaining exposure to solar portfolios in Spain and Italy.

- RES Operations divested a 230 MW / 920 MWh ready-to-build BESS project in Poland to an international investment firm, marking its first in-house large-scale storage exit.

Want more insight?

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

Battery Storage

- Denmark | Niteos and Twig Energy acquire 24.9 MW standalone BESS project in northern Jutland from E&B Renewables, expanding Nordic storage footprint

- Finland | Fu-Gen closes sale of 125 MW ready-to-build Vuolijoki BESS project to Nala Renewables, strengthening Nordic storage collaboration under 2025 framework agreement

- Germany | ESS acquires VoltStorage intellectual property and assets, expanding iron-salt battery platform for long-duration energy storage

- Germany | terralayr acquires remaining stake in BBD joint venture from Averdung Group, securing full control of 1 GW German BESS development pipeline

- Poland | RES Operations sells 230 MW/920 MWh ready-to-build BESS project to international investment firm, marking first in-house large-scale storage divestment

Hydrogen

- France | Vallourec and Baker Hughes sign MOU to integrate Delphy underground hydrogen storage with compression solutions, advancing green hydrogen infrastructure

- Greece | Hellenic Hydrogen reportedly seeks minority investors for 50 MW Amyntaio renewable hydrogen project, advancing Balkans’ first off-grid site

- Spain | MASPV partners with Shanghai Shaanyao to acquire and develop €1bn renewable hydrogen portfolio in Andalusia, targeting 2026 deployment

Retail/Grid Network

Solar

- Europe | Lexham Power (EOS IM) acquires 51% of Innovo Agri to form integrated agrivoltaic platform NT Innovo Agri, targeting 0.5 GW solar pipeline

- France | TotalEnergies launches sale of 17 MWp rooftop and carport solar portfolio in overseas territories, refocusing strategy on larger-scale projects

- Germany | Intertek acquires Aerial PV Inspection to expand solar inspection and digital assurance capabilities in European market

- Italy | Green Utility acquires 2.321 MWp Brindisi ground-mounted solar project, expanding domestic renewable portfolio

- Poland | EBRD invests up to €85m in Virya Energy’s Polish renewables platform to fund project rights acquisition and develop 722 MW utility-scale solar pipeline

- Romania | AJ Brand acquires 6.4 MW operational solar farm from Eximprod, marking shift from EPC contractor to power producer under €25m investment plan

- Europe | Nofar Energy seals deal to acquire a controlling stake in Ellomay Capital (45.9% at USD 323m valuation), gaining exposure to operating solar portfolios in Spain and Italy

- Spain | Greening’s takeover offer for EIDF reaches 74.51% acceptance, clearing the minimum threshold and paving the way for control/combination plan

- United Kingdom | Ampyr Solar Europe acquires a >530 MWp solar project in East Yorkshire from Boom Power, expanding its UK solar (and PV/BESS) pipeline

Solar + BESS

- Germany | ABO Energy seeks investors for 100 MWp solar and 80 MW battery storage portfolio, advancing divestment of subsidy-backed projects

- Romania | GEK TERNA acquires 100 MW solar park with 99 MW storage in Satu Mare from Renovatio Group, marking strategic expansion into Romanian market

- United Kingdom | Uniper partners with Innova on 100 MWp UK solar portfolio including co-located 30 MW BESS, advancing sole ownership of three CfD-backed projects

Wind

- Germany | greenwind acquires 22.4 MW Freudenberg Nord2 wind project in Brandenburg, advancing in-house construction and expanding local footprint

- Germany | KGAL acquires 14 MW Rekum repowering wind project near Bremen from Energiequelle for institutional fund, securing 20-year EEG tariff

- Spain | Recursos de Galicia acquires 49.5 MW Mondigo wind farm in Lugo from Sinia Renovables (Banco Sabadell) for €75m, marking its first wind asset and advancing regional energy strategy

- United Kingdom | Thrive’s JV Burgar Hill Energy acquires two 2.5 MW turbines from RWE for 30 MW repowering project at Orkney wind farm

Bioenergy

European wind power investment: the 2030 gap, the bankability reset, and what it means for investors

Europe is already a wind powerhouse, but the 2030 targets will not hit themselves. Installed capacity is large, the pipeline is real, and wind is now a structural part of the continent’s power mix, yet the gap to policy ambition remains uncomfortable.

What is changing in 2026 is not the wind resource, it is the economic engineering behind it (contracts, pricing mechanisms, grid, and risk allocation). That is where public policy and private capital are now meeting, and where M&A is starting to look less like “consolidation” and more like execution.

Europe is already huge in wind, but still behind on 2030

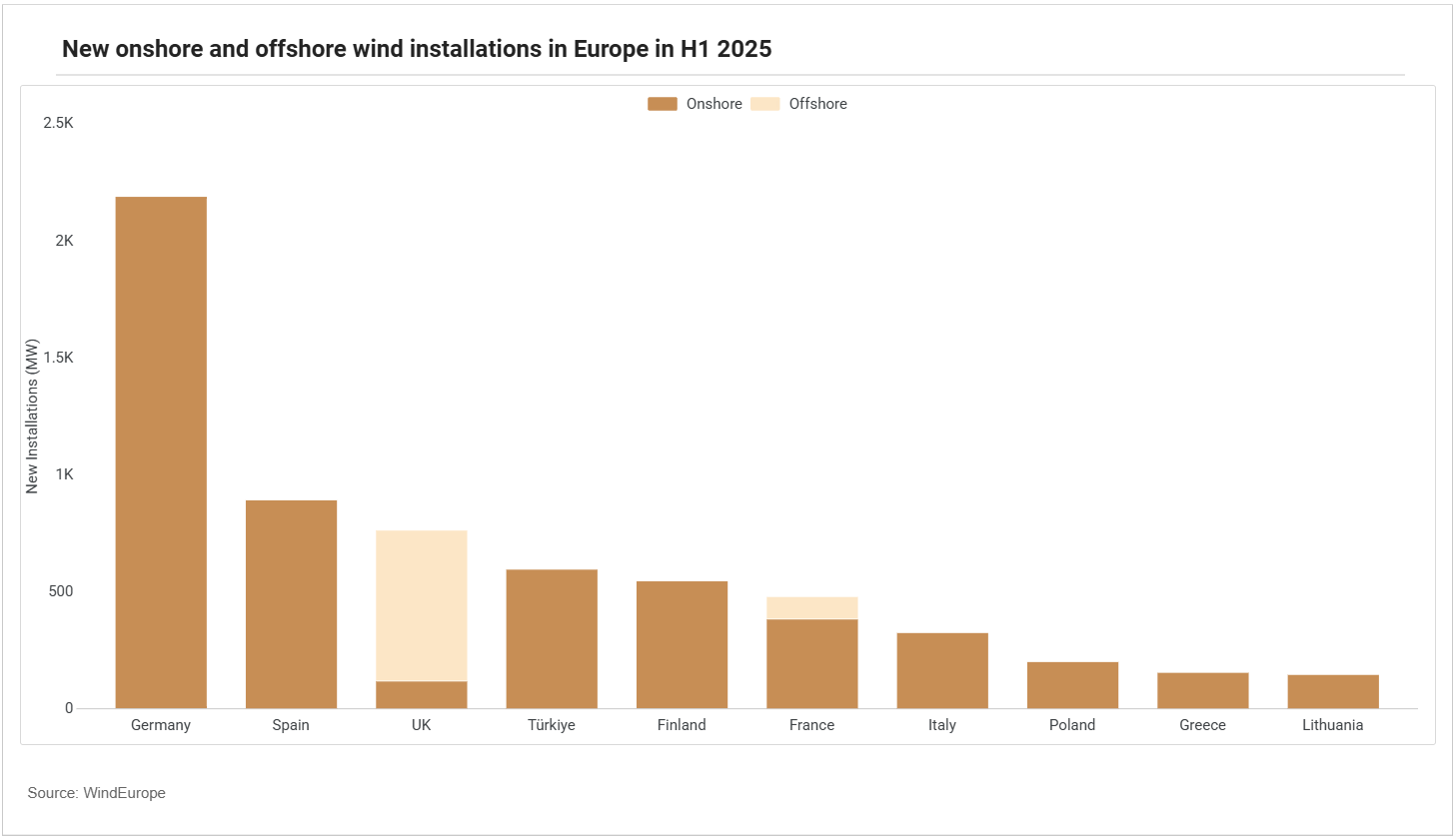

Europe is already gigantic in installed wind generation capacity, but we are still far from meeting our 2030 goals. To put the challenge in context: in Q1 2025, the region reached 291 GW of wind capacity (254 GW onshore, 37 GW offshore). Other sources even point to lower numbers, such as 236 GW in January 2026.

Either way, these are impressive figures for a technology that already accounts for 19% of electricity generation across the continent. Still, it is nowhere near what is required to reach the European Green Deal target of 425 GW. Investing in wind today means viewing expansion not only as a market necessity, but also as an ESG imperative.

At the same time, it sits on a paradoxical economic backdrop.

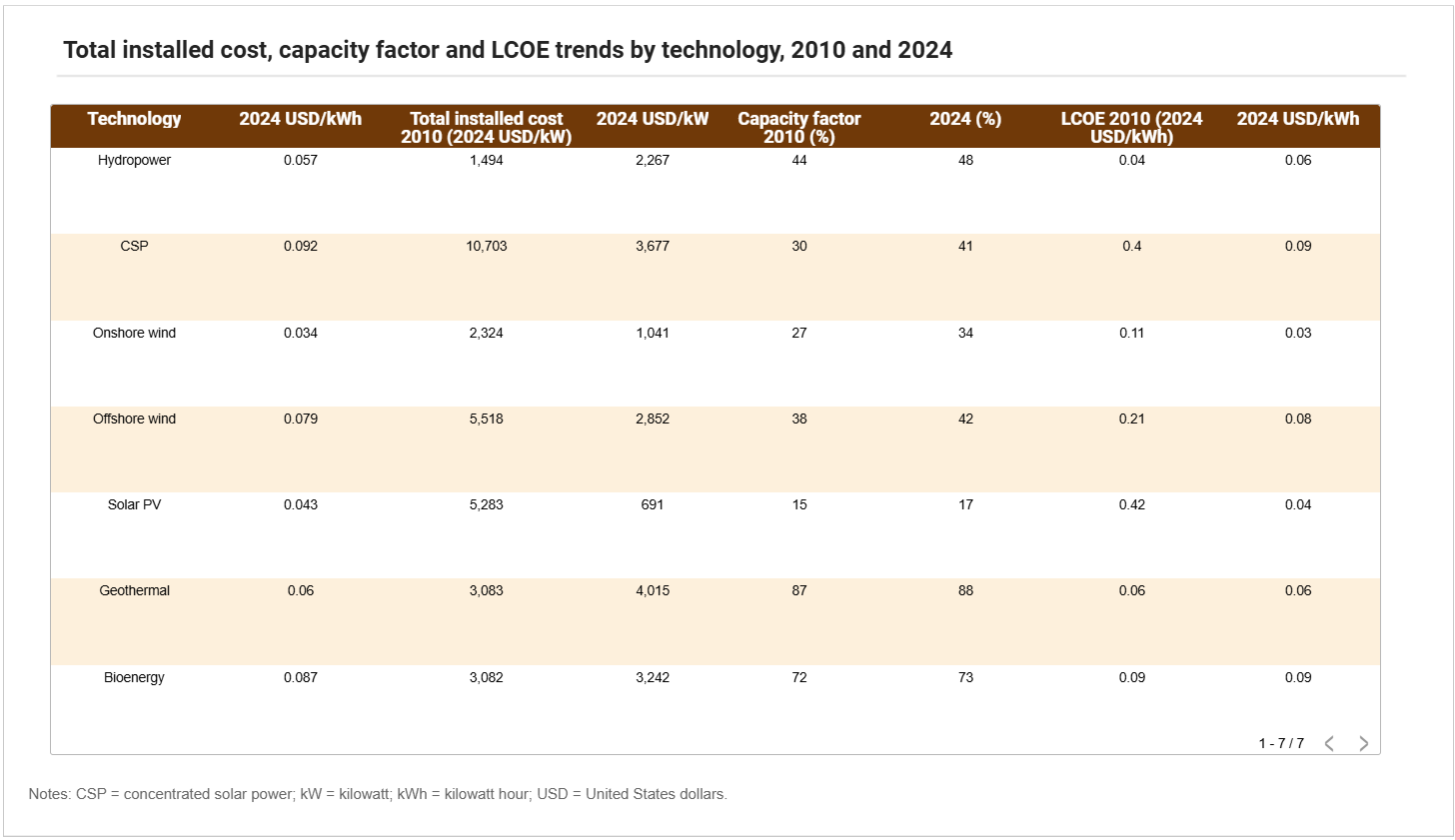

Data published late last year by the International Renewable Energy Agency (IRENA) indicated that, in 2024, onshore wind remained the renewable technology with the lowest total costs.

- In that period, the global weighted-average Levelised Cost of Energy (LCOE) was US$0.034/kWh, with offshore wind at US$0.079/kWh. Global average capacity factors were 34% (onshore) and 42% (offshore), and Europe’s regional average offshore LCOE was around US$0.080/kWh.

Winning the “lowest renewable LCOE” trophy in the region is an achievement, but it does not remove the counterpoint.

In the same period, IRENA’s data point to cost increases of 3% offshore and 4% onshore (second only to bioenergy, at 13%). LCOE is also high compared with other markets.

- In onshore wind, for example, China (US$0.029/kWh) and Brazil (US$0.030/kWh) show materially more competitive costs, which signals there is still room for further development in the EU. According to market sources from WindEurope, reducing CAPEX in the sector is one of the goals of the newly announced Offshore Wind Investment Pact.

The challenges created by price volatility and grid constraints close this circle. You can read more on this here. You have probably noticed that the wind narrative is starting to look very similar to the challenges other sectors (especially solar) are facing in the EU, often for the same reasons, which will only be solved if, one day, humanity learns how to control nature.

The market is growing, but contracts (PPAs and CfDs) are back at the centre

Today, we have a global wind market that keeps growing, with clear demand drivers and pipeline. Mordor estimates global wind at 1.27 TW (2025) and projects 2.31 TW by 2031, with a 10.52% CAGR (2026–2031).

- The consultancy attributes this growth to multi‑GW corporate Power Purchase Agreements (PPAs), offshore pipeline, and policy incentives that reduce the cost of capital.

- Mordor also highlights a shift in contracting dynamics, with technology companies acting as demand anchors, signing long-term PPAs to secure revenue and clean electricity for AI workloads. Global data from BloombergNEF, released last week, corroborate the growing weight of tech: Big Tech accounted for 49% of corporate clean energy deals in 2025.

Demand exists, and technology keeps improving. But the investor equation has flipped along with the market: it is no longer enough to have wind, you need contract certainty, predictability, and grid.

The 2026 Orrick Offshore Wind report brings two examples that show why revenue design is back at the centre.

- In Denmark, the report describes how the previous two tender rounds failed due to escalating costs and low, unpredictable returns in the electricity market. The response was a more developer‑friendly model, with a state‑backed two‑sided Contract for Difference (CfD) (cap €7.4bn) guaranteeing a minimum price for 20 years, without the previous requirement of 20% state co‑ownership, and with the State taking on preliminary study and mitigation costs (reducing upfront burden).

- In Belgium, the mechanism also evolved into an LCOE‑based two‑sided CfD, with an explicit logic to avoid windfall profits. There is a support cap and even a PPA carve‑out (up to 50% of production, under conditions), which shows an attempt to reconcile CfDs with private contracting.

- The UK awarded CfDs for 8.4 GW (fixed and floating), a record above 7.0 GW in the prior round.

- Germany had its first “zero-bid auction” due to higher costs, and is moving towards a CfD regime to re‑ignite investment.

Markets are already reacting, and the impact is now reaching public policy and contract design. Different states are redesigning mechanisms to restore bankability.

- In these examples, we see a lens where auction logic becomes less attractive, compared with focusing efforts on revenue engineering.

- We also see alternative approaches, where support models are reconfigured around indexation, caps on state exposure, and payback obligations when power prices rise.

Energy transition M&A in wind: capital recycling, co‑investment, and discipline

The Energy Transition M&A Outlook 2025 report, by DLA Piper, reinforces the shift in how dealmakers are operating: players are focusing more on strategic acquisitions, and there is a move from already-operational assets towards co‑development, early‑stage projects, and platforms/portfolios.

With ambitious targets, but still uncertain execution, the pieces are aligning around a broader risk‑mitigation mood. In private markets, this becomes more visible through capital recycling and co‑investment strategies.

There are notable project-level examples, such as when:

- Macquarie cancelled the sale process for Corio Generation due to a lack of investor interest. That is capital discipline, in ink.

- Masdar partnered with Iberdrola to acquire 50% of East Anglia Three. Both committed €5.2bn of co‑investment into construction.

It also shows up in floating, where technology risk is higher, and structures tend to incorporate more optionality, for example:

- Ørsted sold control of Salamander to Odfjell Oceanwind.

- Great British Energy, the National Wealth Fund, and the Scottish National Investment Bank acquired minority stakes in Pentland, up to £50m each.

The picture is a European wind sector where both public and private actors are redesigning the industry to regain bankability. The ambition and potential are still there, but to capture the full upside we need to look harder at economic engineering.Stability mechanisms are gaining weight in board meetings, so explore them strategically when shaping your investment strategy. I still want to talk about YOUR deal here, in our Teasers.