Sebastian Montoya

Sebastian Montoya

Europe’s electricity prices are bouncing between the floor and the ceiling, again emphasising the critical need for flexibility in power generation.

Explore our analysis this week for the underlying drivers, and take a look at the week’s key deals.

- VARO Energy has acquired Preem, now rebranded as VAROPreem, in a transaction that positions the group as Europe’s second-largest producer of renewable fuels.

- EnBW has sold its stake in the 1.5 GW Mona offshore wind project to JERA Nex bp following the UK CfD setback, underlining tighter capital discipline and a broader repositioning among offshore wind players.

- Alpiq has acquired the Cheviré battery storage facility (100 MW / 200 MWh) from Harmony Energy, securing France’s largest operating storage asset and expanding its exposure to flexibility assets in key markets.

Connect with me on LinkedIn to stay on top of Europe’s latest moves.

Deals breakdown

Europe’s power prices are sending a clearer signal: Flexibility is the new premium

Europe has just hit a milestone that would have sounded fanciful not long ago: wind and solar generated more electricity in the EU in 2025 than fossil fuels, with wind and solar at 30% of generation versus 29% for fossil fuels.

Now, the more instructive news is what happens next: the system is increasingly shaped by when renewables produce, not only how much they produce.

And this is where price behaviour becomes the real story: dispersion across markets, sharper swings, and more frequent ultra‑low (and sometimes negative) price periods.

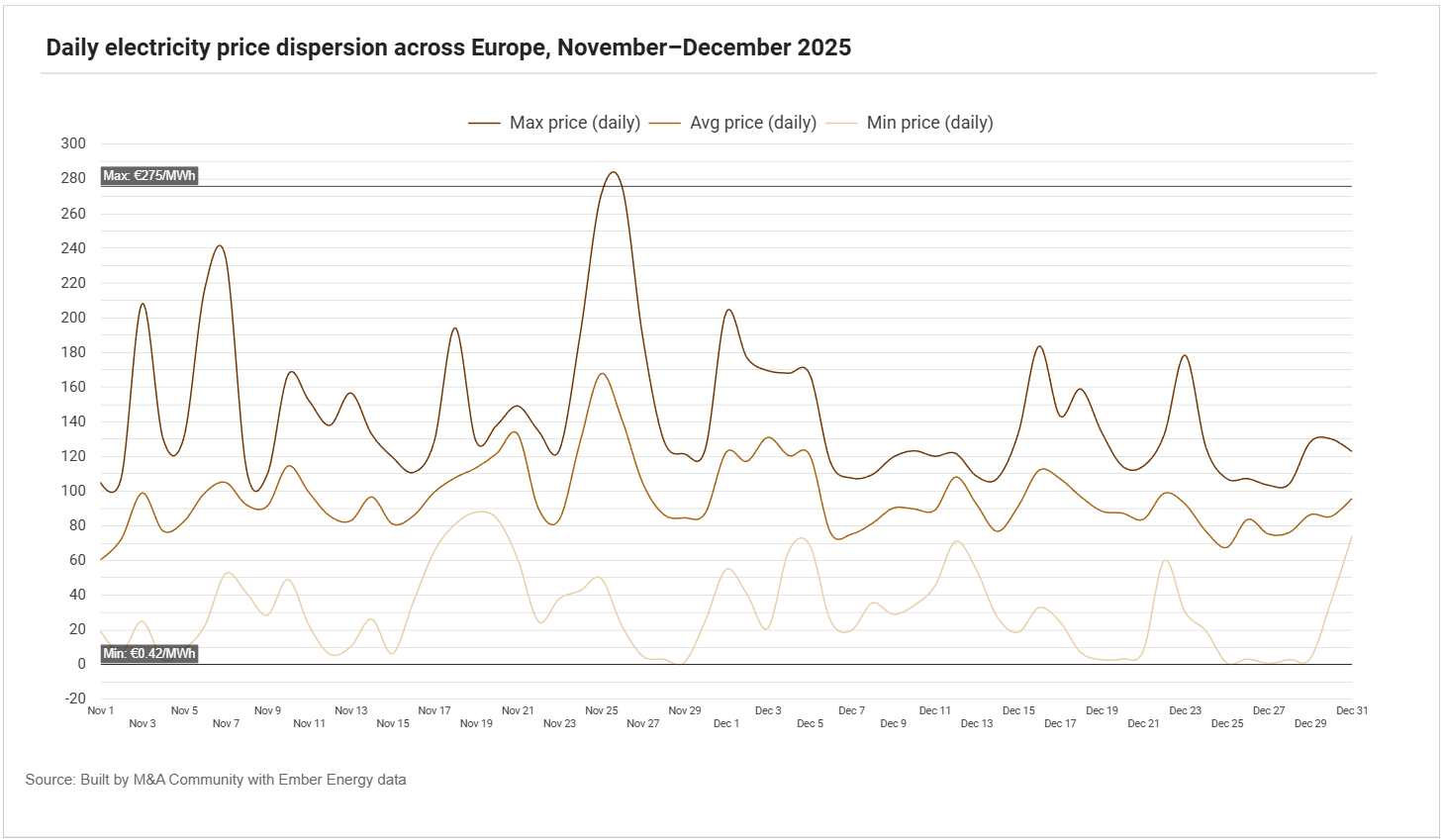

A new report from Ember Energy, European Wholesale Electricity Price, shows that between November/December 2025, the headline was not a single “Europe price” but how far apart markets can be on the same day.

- In this two‑month window, the average daily spread between the cheapest and most expensive market was roughly €110/MWh, and the extremes were striking: from €0.42/MWh (Sweden, 27 Dec) to €275.76/MWh (Ireland, 26 Nov).

That widening gap is consistent with what Eurelectric flags at the structural level: Europe is entering a “second stage” transition where the challenge is less about building clean generation, and more about absorbing it, with electrification still relatively stagnant and flexibility still insufficient.

- Eurelectric notes that negative price hours have surged in recent years, and ties the phenomenon to a combination of high renewable output, low/rigid demand, and limited flexibility (including storage and demand response).

What is driving the volatility (and why it matters for dealmaking)?

A useful way to frame it is: the system is learning to price “shape”.

- When supply is abundant and demand is not (especially during high solar or high wind periods) the market pushes prices towards ultra‑low levels.

- When the marginal unit is still fossil‑linked (often gas), prices can swing back quickly, and the system can revert to expensive hours. Reuters points to exactly this dynamic: gas generation rose due to lower hydro, lifting costs, and wholesale prices were higher during gas‑heavy hours.

Spain is a live case study of the renewables‑heavy version of this problem. Reuters reports that Spain recorded hundreds of hours of zero or negative prices over the year (UNEF’s warning), with the industry stressing that low and unstable capture prices can threaten the economics of the transition if flexibility does not scale with generation.

Europe is not one market, and that fragmentation is investable

This is where the story crosses even more with M&A: location and market design details increasingly drive value.

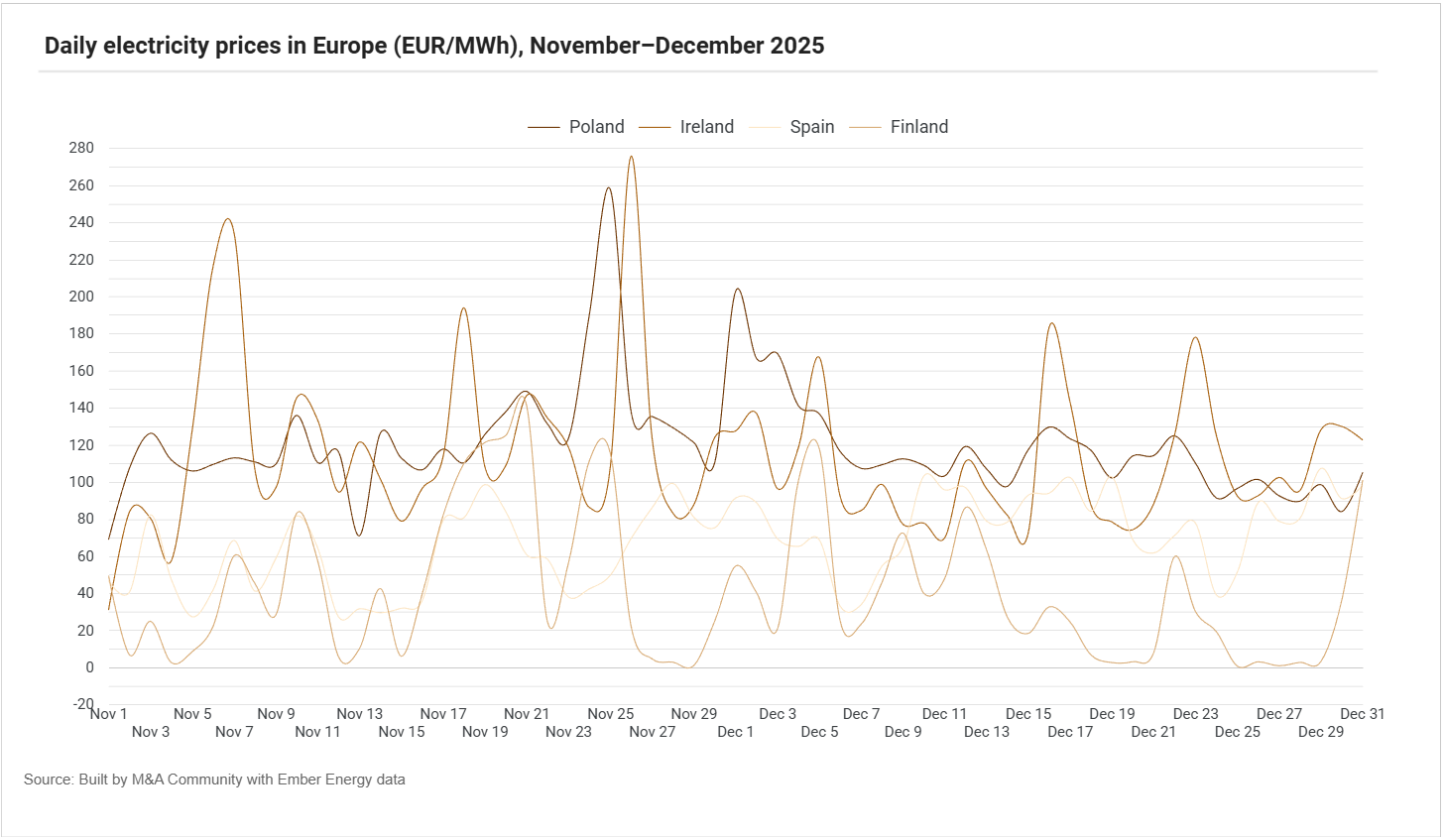

In the same November/December 2025 window, some markets were structurally lower (Nordics, Iberia), while others showed higher levels and sharper spikes (parts of Central/Eastern Europe and more constrained systems). That matters because it changes underwriting assumptions:

- Merchant risk is no longer a generic input. It is market‑specific and increasingly shape‑dependent.

- Capture prices and curtailment exposure become central, particularly for solar‑heavy portfolios.

- Route‑to‑market strategy (PPAs, CfDs, hedging structures, negative‑price provisions) becomes a valuation driver.

Eurelectric’s point is worth taking seriously here: ultra‑low and negative prices are not “a surprise bug”. They are a market signal that the system needs more flexibility and more electrification, not less renewables.

The near‑term implication for investors is more practical than philosophical: the winners will be the platforms that can monetise volatility rather than be penalised by it.

Where BESS enters the picture: From “nice to have” to system infrastructure

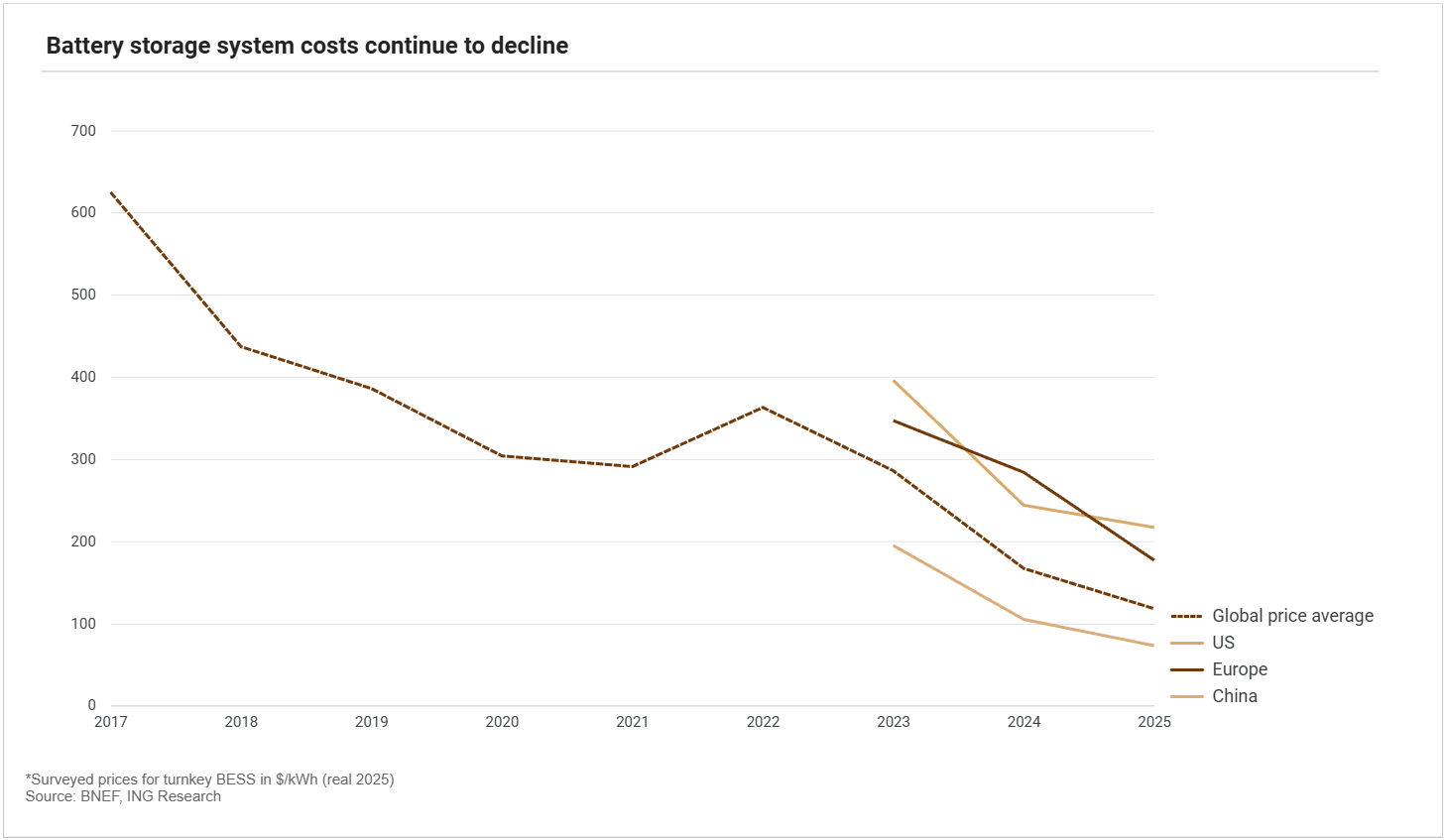

ING Research highlights that battery system costs declined materially over 2020–2025, and frames this as a key enabler for rapid capacity growth in the years ahead.

Lower capex does not eliminate risk, but it does change the dynamics: more projects can clear investment hurdles, and more grids can procure flexibility at scale.

Now combine that with the price reality: in a system with frequent low‑price periods and pronounced evening peaks, BESS is economically positioned to do three things at once:

- Arbitrage (shift low‑price energy into peak hours);

- Provide balancing and ancillary services, and;

- Reduce curtailment and stabilise capture prices for solar and wind (especially in hybrids).

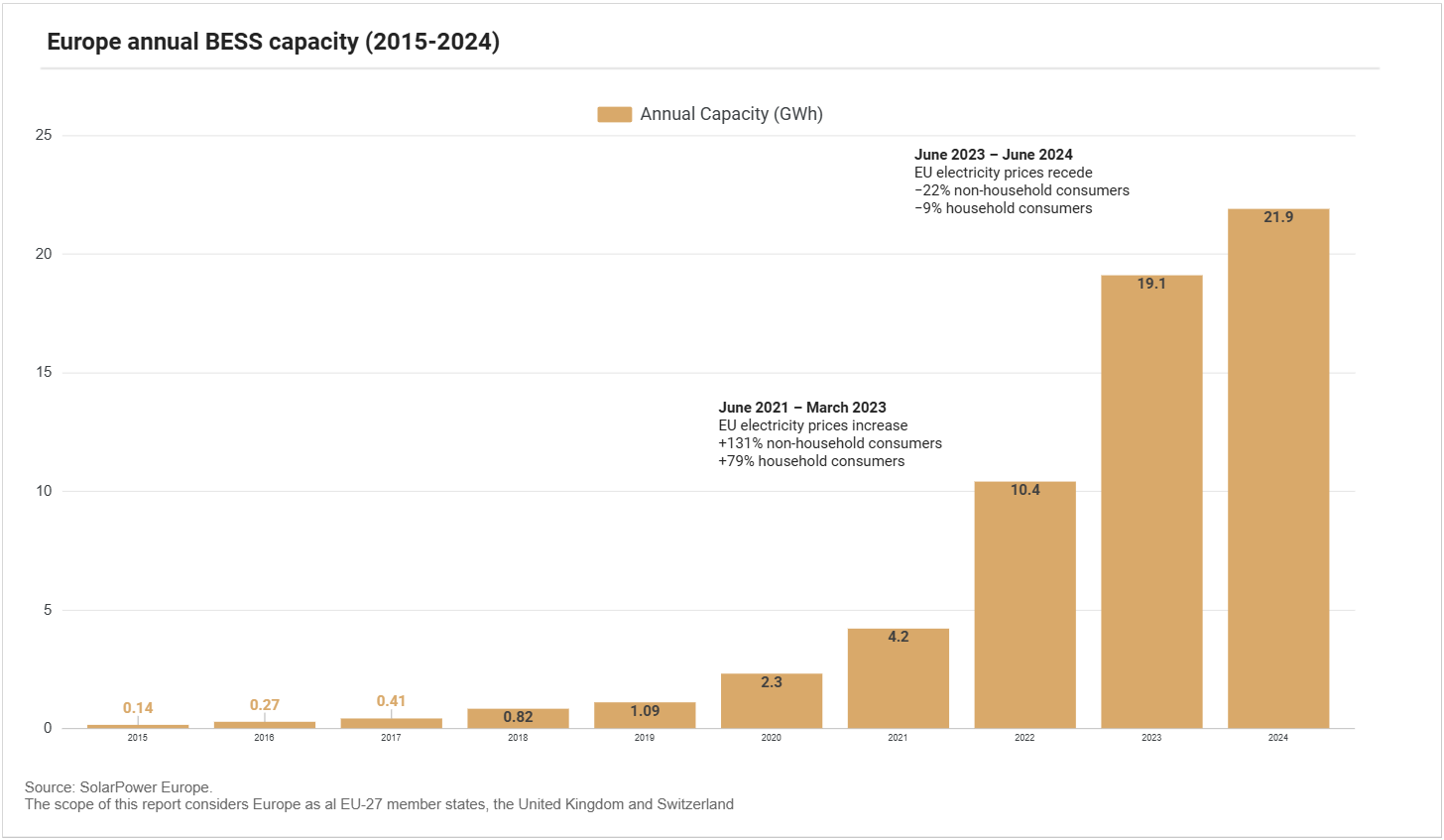

SolarPower Europe reports that Europe installed 21.9 GWh of BESS in 2024 (another record) although growth slowed to 15% as the market transitioned away from a residential‑led surge and towards a more grid‑scale‑driven phase.

Crucially, the same outlook expects growth to reaccelerate: under the Medium Scenario, annual deployments rise to 118 GWh by 2029, with grid‑scale BESS expanding its share of annual additions (SolarPower Europe).

That is a meaningful shift for M&A: The centre of gravity moves from fragmented behind‑the‑meter volumes to build‑to‑own grid‑scale assets, where revenue stacking, connection rights, permitting, and dispatch strategy become core diligence topics.

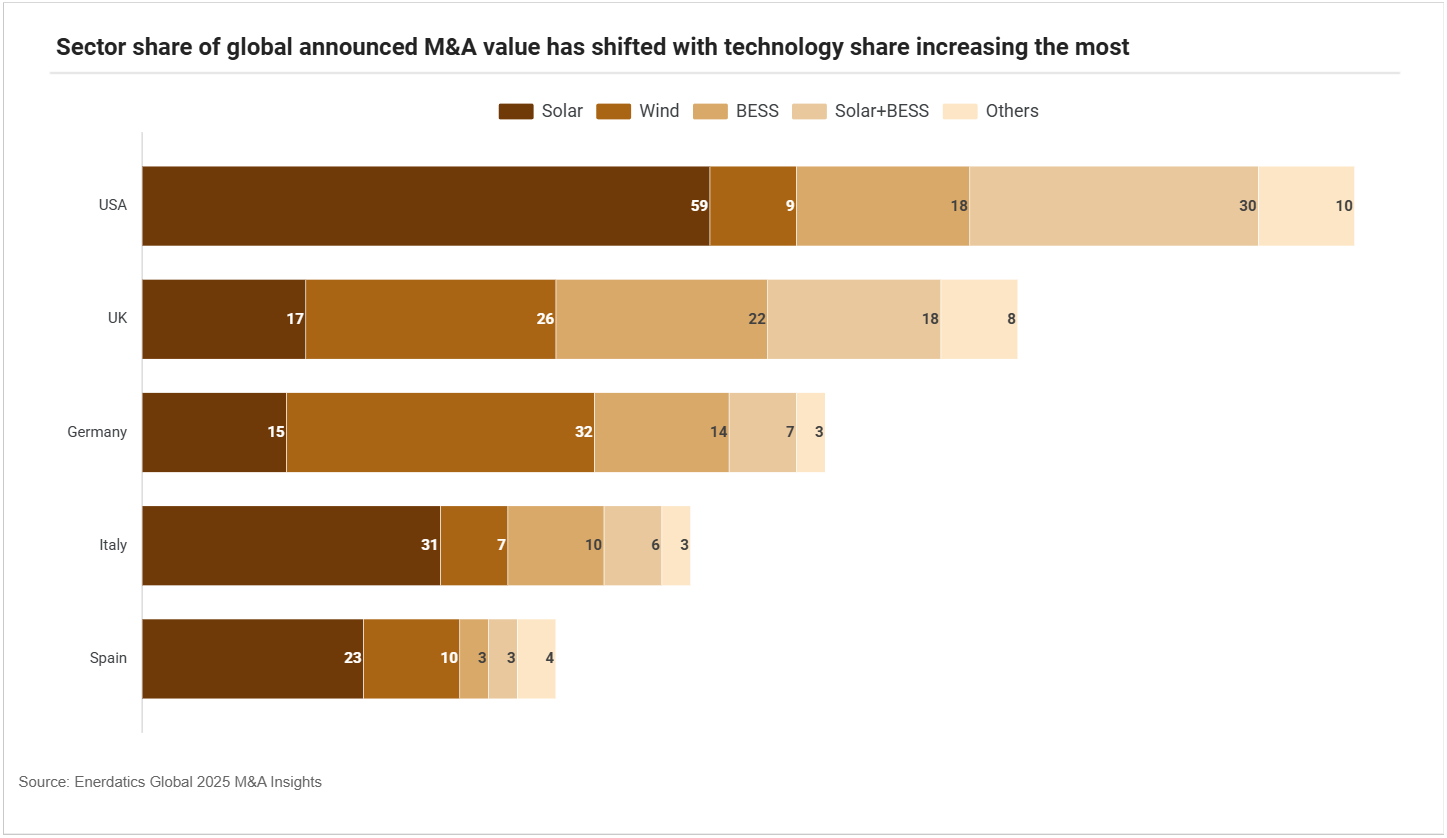

According to Enerdatics, across key geographies, deal activity clusters around solar and wind, but the presence of BESS and solar+storage is increasingly visible.

The investment takeaway?

Europe’s clean power build‑out is not slowing: it is moving into a more operationally complex phase. The premium is shifting from “can you build renewables?” to:

- Can you secure grid access and dispatch optionality?

- Can you manage capture price risk?

- Can you monetise volatility through storage, hybrids, and sophisticated route‑to‑market structures?

What’s your answer?

Battery storage

- Finland | Lehto Group acquires rights from HPF Kalajoki to develop 30 MW electricity storage facility in Kalajoki, securing grid connection with expansion option up to 100 MW

- Finland | SENS and Dovre Group agree sale of 85 MW / 170 MWh Pyhäsalmi BESS project to Frankfurt-based infrastructure investor, marking milestone asset-rotation transaction

- France | Alpiq acquires 100 MW / 200 MWh Cheviré battery storage facility from Harmony Energy, securing France’s largest operational BESS and expanding flexible assets portfolio

- Germany | Battery storage platform terralayr raises €192m equity round led by Eurazeo to scale grid-scale BESS portfolio and digital flexibility platform

- Germany | Milvio Energy completes sale of fully developed 50 MW stand-alone BESS project, highlighting strong investor appetite for utility-scale battery storage assets

- Lithuania | Aquila Clean Energy sells ready-to-build 50 MW / 100 MWh BESS project to Energy Gates, advancing portfolio rotation strategy in the Baltic energy storage market

- United Kingdom | Drax signs £36m acquisition of flexible energy asset optimisation platform Flexitricity from Quinbrook, supporting GW-scale battery storage growth strategy

Hydrogen

- Germany | BKW aims to acquire 40% stake in hydrogen-ready gas power plant project in Hamm with Trianel, supporting coal-to-hydrogen transition strategy

- United Kingdom | Hygen Energy acquires HyBont low-carbon hydrogen production and refuelling project in Wales from Marubeni, adding HAR1-backed asset and expanding UK hydrogen footprint

Multiple

- Europe | Caely Renewables acquires Nordic sustainability solutions provider Ecohz, combining complementary platforms to accelerate growth in renewable energy and decarbonisation services

- Europe | Gresham House completes acquisition of SUSI Partners, creating a £2.7bn energy transition infrastructure platform and expanding pan-European and Asian investment capabilities

- United Kingdom | Masdar and Octopus Energy sign MOUs to partner on clean energy initiatives in the UK and Africa, combining solar, storage and smart grid solutions

Solar

- Italy | Korkia completes sale of two ready-to-build solar PV projects totalling 6.5 MW in Friuli-Venezia Giulia, marking first exits from its Italian development platform

- Poland | PNE sells ~40 MW behind-the-meter solar project near Płock to ORLEN, supporting refinery decarbonisation and reinforcing PNE’s asset-rotation strategy in the Polish market

- Romania | CCE sells Horia 2 photovoltaic project SPV to Renalfa Solarpro Group, transferring 293 MWp large-scale PV development in Arad County

Solar + BESS

- Germany | Aream secures ~200 MWp solar PV pipeline with co-located battery storage through acquisition of development platform, expanding hybrid renewables footprint

- Greece | METLEN and Tsakos Group form JV to develop 251.9 MW solar PV and 375 MWh storage hybrid power project in Central Greece, advancing large-scale RES integration

Wind

- Finland | OX2 hands over 455.4 MW Lestijärvi onshore wind farm to consortium of Kymppivoima, Oulun Energia and Kuopion Energia, completing country’s largest wind project

- France | Allianz Global Investors acquires 20.25% minority stake in 500 MW îles d’Yeu et Noirmoutier offshore wind farm from Ocean Winds, marking first offshore wind investment in France

- Germany | Energiekontor sells two onshore wind park projects totalling ~93 MW to illwerke vkw, expanding the Völkersen site and extending long-standing partnership

- Germany | Iver acquires ENO Energy’s wind turbine service and maintenance activities, gaining established Rostock hub and expanding national service network

- Hungary | Iberdrola completes €171m sale of its Hungarian renewables business to Premier Energy-led consortium, exiting market and divesting 158 MW onshore wind portfolio

- Sweden | Ardian Clean Energy Evergreen Fund acquires 62 MW Furukraft wind farm from ERG via Enordic Evergreen, expanding Nordic wind portfolio and platform scale

- Ukraine | Horizon Capital backs Notus Energy with Catalyst Fund investment to launch 124 MW onshore wind project in Odesa region, marking fund’s first deal and supporting Ukraine’s energy recovery

- United Kingdom | EnBW sells stake in 1.5 GW Mona offshore wind project to partner JERA Nex bp, exiting project after UK CfD setback while refocusing offshore wind strategy

- United Kingdom | ERG acquires 73 MW onshore wind portfolio in Northern England from OnPath Energy and exits Sweden via sale of 62 MW Furuby wind farm, executing geographic refocus

- United Kingdom | Innagreen Investments enters UK market with acquisition of 38.7 MW Dunbeg South onshore wind farm in Northern Ireland from RES, marking first UK renewables investment