Daniel Black

Daniel Black

Hello,

It’s been quite a week in geopolitics, causing a few jitters in global markets. However, European stocks saw gains on Thursday after Trump rolled back on threats of tariffs and invasions.

And the M&A rumour mill kept on turning, with headlines including:

- Beazley turned down a £7.7bn Zurich takeover

- EQT is to buy Coller Capital for up to $3.7bn

- Multiple bidders are circling Aegon’s UK business unit

Thanks for reading, and connect with me on LinkedIn if you want to discuss how I can help with your next M&A deal.

Read the Ideals AI in M&A 2026 report

Artificial intelligence has become a true deal accelerator. According to a new report from Ideals, 59% of dealmakers say increased speed and efficiency is AI’s leading benefit.

The research combines survey insights from more than 100 M&A professionals with profiles of leading dealmakers, revealing how AI has moved from promise to practical impact in M&A.

You can download it here.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- EQT to buy UK’s Coller Capital for up to $3.7bn

- EQT CEO targets real estate expansion after deal to buy Coller

- Phoenix, Scottish Widows and Royal London circle insurer Aegon’s UK business

- UK’s NCC Group to sell Escode for $369.4m

- GSK makes $2.2bn swoop for RAPT Therapeutics’ food allergy drug

- Plan to overhaul CMA’s merger process sparks ‘cronyism’ fears

- GSK to buy US biotech behind food allergy drug for $2.2bn

- Three Ireland owner in talks over sale to Liberty Global

- French government seeks €95m in damages from Greybull over steel plant collapse

- UK government to take £25m stake in Octopus Energy’s tech arm Kraken

- Beazley rejects Zurich Insurance’s £7.7bn takeover bid

- Zurich confirms plans to launch Lloyd’s syndicate amid Beazley bid

- FitzWalter Capital sweetens buyout bid for Auction Technology to $658 million

- Literacy Capital sells Tyrefix to Norvestor-backed Citira

- Epiris to sell minority stake in Pure Cremation to Centerbridge

- Drax to buy optimisation platform Flexitricity in £36m deal

- TDR Capital to buy NCC’s Escode business in £275m deal

- UK minister met Paramount CEO Ellison in London on Thursday, source says

Industry news

- London stocks advance as Trump drops Greenland tariff threat

- Sterling edges up as focus shifts to data, BoE rate outlook

- UK bond yields rise after report of route back to parliament for Starmer rival Burnham

- London retains top spot in own global financial centre survey for sixth year

- Barclays to move ahead with relocation of European base to Paris

Salaries and bonuses

Job moves

- BGF promotes Ben Barker to chief investment officer

- Citi hires new London MD from team mandating more time in the office

- Hedge fund Two Sigma hired a top Goldman Sachs AI technologist in London

- Paul Weiss poaches Simpson Thacher partner to head european infrastructure M&A

Market trends

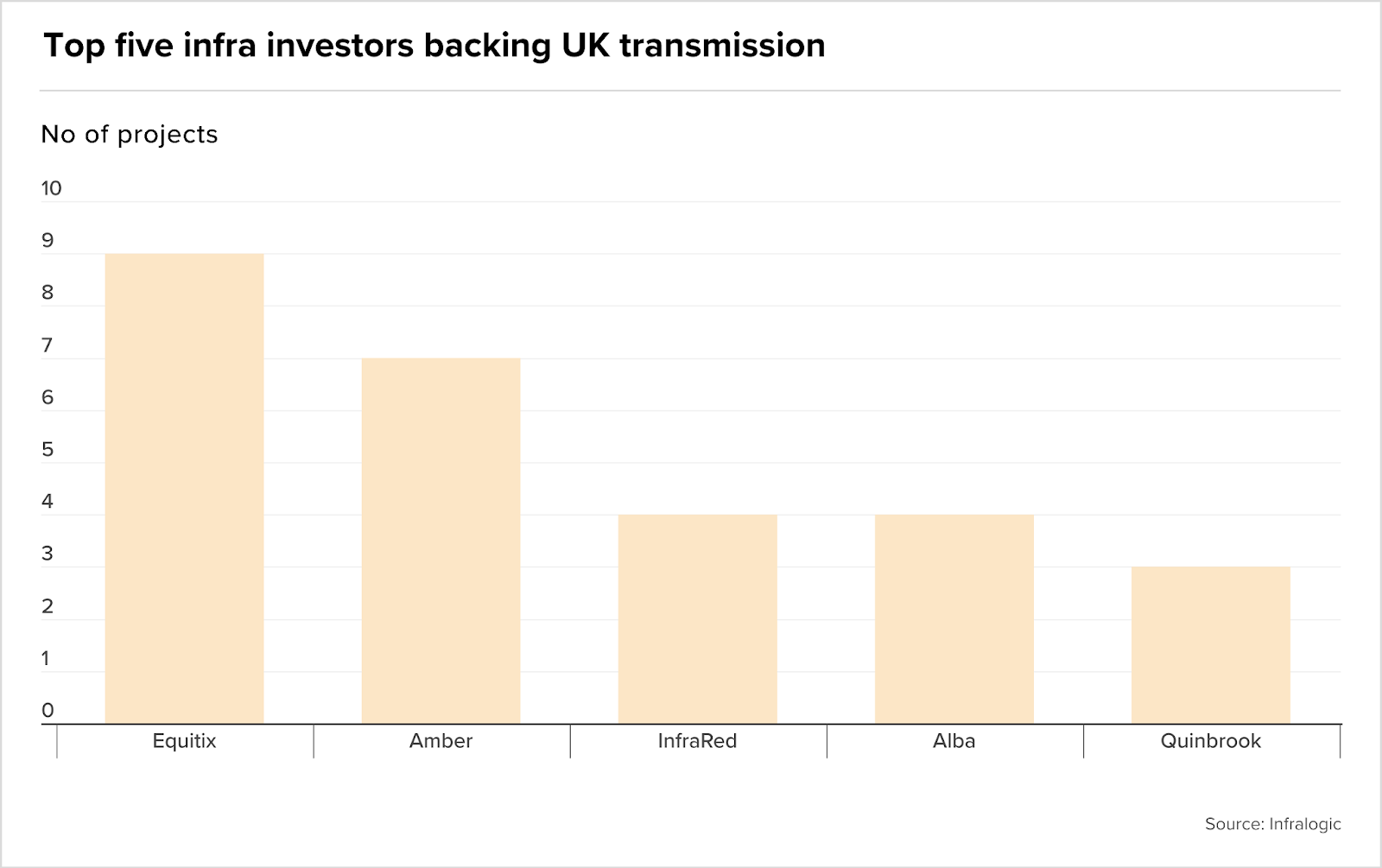

Energy transition shows no signs of slowing

New data from Infralogic shows that energy investment in EMEA reached an all-time high of $373bn last year, with power generation increasing 60% to $200bn while oil and gas remained unchanged at $86bn. Grid infrastructure deals nearly doubled to $19bn, battery storage nearly tripled to $9bn, and greenfield renewables investment in wind and solar increased by 63% to $67.6bn.

The UK dominated deal flow with the £38bn Sizewell C nuclear financing (the largest infrastructure transaction ever recorded globally) and $22bn in offshore wind project debt.

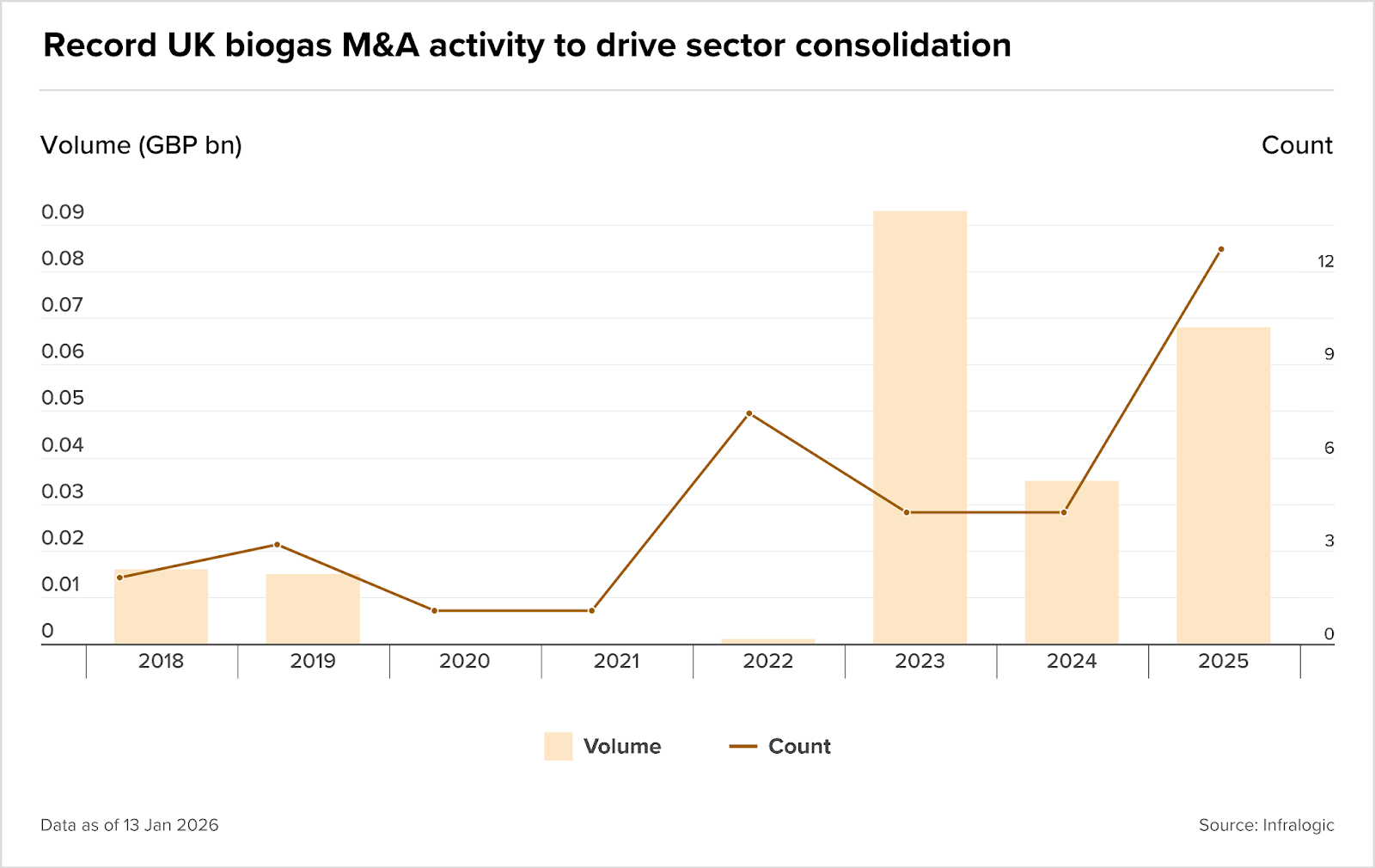

The report also shows that UK biogas entered a consolidation phase in late 2025.

An upsurge of year-end transactions was driven by buyers such as BioticNRG, the UK bioenergy fund of Palisade Real Assets, Australian power company EDL Energy, and Copenhagen Infrastructure Partners, as larger funds and utilities aimed to increase market scale through portfolio acquisitions.

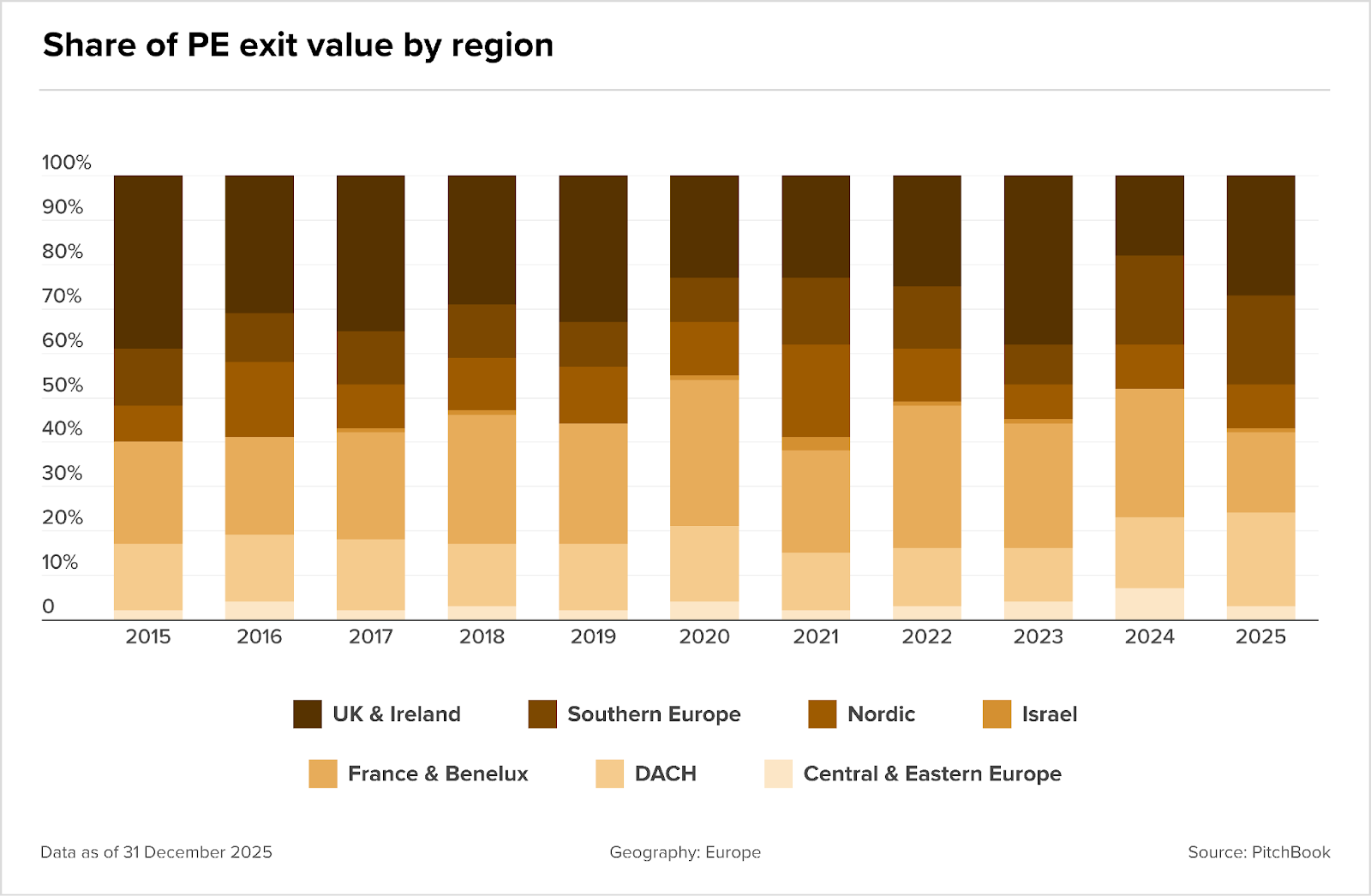

PE gets its mojo back

According to PitchBook’s PE Breakdown, UK & Ireland PE exit activity improved in 2025 as markets gradually reopened in the second half of the year. The region benefited from increased interest from inbound investors and a higher percentage of sponsor-to-sponsor transactions. Secondary buyouts became the primary exit strategy for funds looking for liquidity, supporting deal flow while traditional public market exits remained scarce.

Although the UK’s share of European exit value is still below its historical range from 2015–2020, the increase represents a recovery from muted 2023–2024 levels.

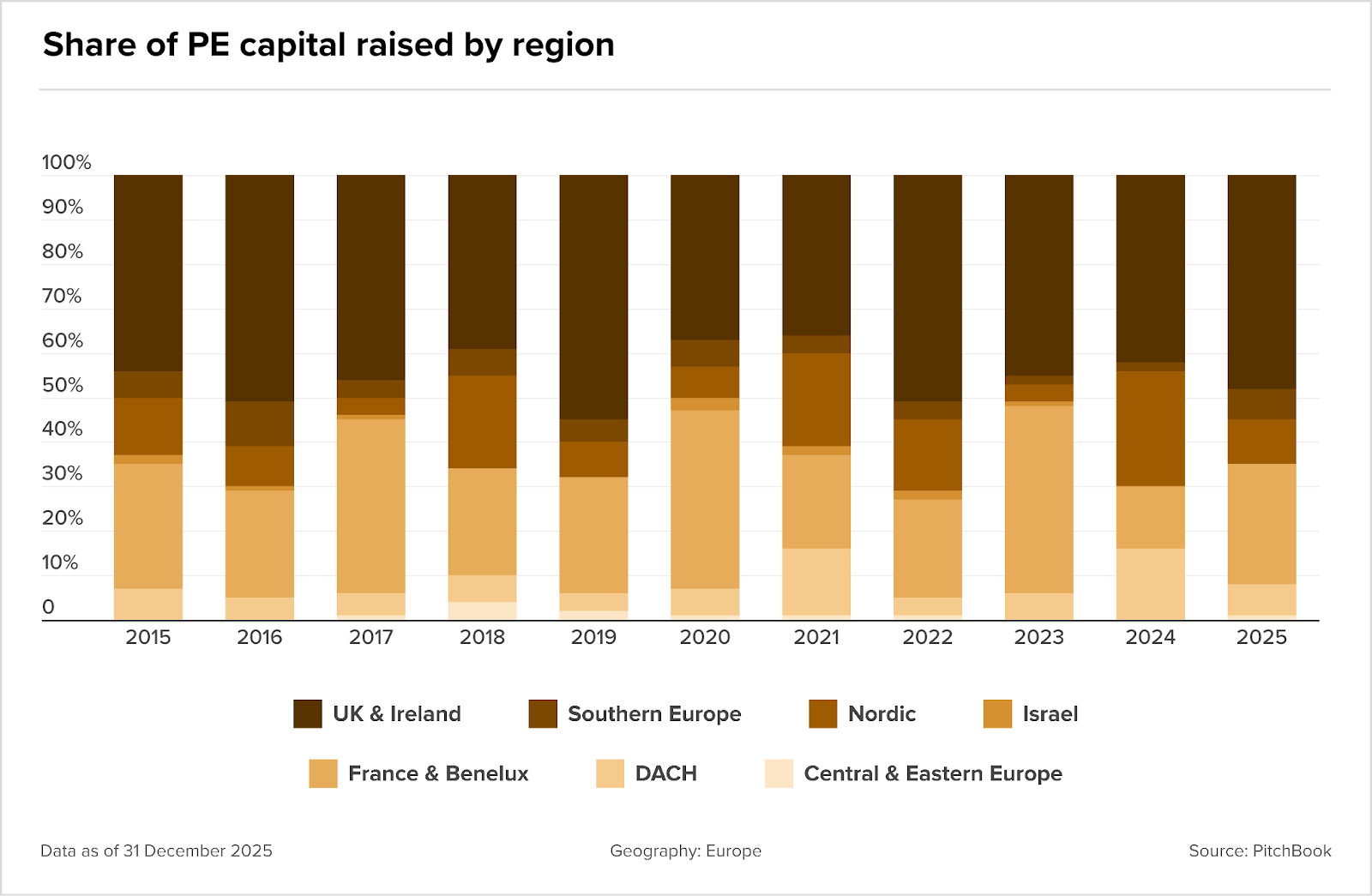

However, the UK’s dominance in European PE was most noticeable when it came to fundraising, accounting for nearly half of all capital raised in 2025 and roughly one-third of all funds.

Fundraising