Daniel Black

Daniel Black

Hello,

The week starts with a mega-tailwind. Intertek has acquired Aerial PV Inspection: a move the company says responds to the solar market’s rapid growth, citing a forecast of 9.2% CAGR through 2029.

Other standout transactions this week:

- Wrisk has acquired Atto, a financial intelligence platform, to strengthen its embedded insurance and finance capabilities.

- ECI Partners has acquired Paragin Group (exam and assessment software) from Main Capital Partners, backing its next phase of growth.

- Thrive Renewable Energy’s JV, Burgar Hill Energy, is progressing a UK wind farm repowering, acquiring two 2.5 MW turbines as part of a project of up to c. 30 MW.

Thanks for reading.

If you’d like to take your M&A deals to the next level, connect with me on LinkedIn and let’s discuss how Ideals VDR can help elevate your strategy.

Deal Tracker

Our weekly roundup of all the confirmed M&A deals in the UK.

The rumour mill

- Elliott pushes for divestments, £5bn Buyback at LSE Group

- CVC Is working with Goldman Sachs on €1bn Marina Business sale

- CFC owners said to tap banks for sale, IPO of £5bn insurer

- Chesnara to buy Lloyds’ Scottish Widows Europe for €110m

- Nexfibre buys £2bn Alt-Net as UK consolidation starts

- London private equity firm Hollyport hires Evercore to explore Sale

- Ardian gets EU nod to acquire Irish utility Energia

- SME-focused Zempler Bank set to be acquired by The Access Bank UK

- Virgin Media O2 owners to buy British fibre firm Substantial for $2.7bn

- Nuveen to buy UK asset manager Schroders in $13.5bn deal

- Schroders boss told Treasury £9.9bn sale was ‘good deal’ for UK

- BDO UK and Ireland partners approve £1.1bn merger

- Elliott pushes LSE Group for £5bn buyback

- Zurich secures more time to finalise Beazley takeover

- Liberty Global agrees to buy out Vodafone in Dutch joint venture for €1bn

- Rosebank Industries vows to keep London listing as it explores $3bn in US deals

- Software group Pinewood plummets after AI sell-off scuppers £575mn deal

- UK’s Brewdog picks AlixPartners to run sale process

- Macquarie Asset Management to buy IHS Holding’s South American tower assets

- M&G and CVC agree $1.1bn private equity transaction

- NatWest looks to Technology to Cut Costs After Earnings Beat

- Maven Securities mulls UAE office as trading talent flocks to Middle East

Industry news

- UK inflation falls sharply to 3% in January

- BOE Is Considering Outside Help for Private Markets Stress Data

- Sterling steady, inflation figures reinforce near-term BoE cut bets

- UK’s FTSE 100 hits record as cooling inflation fuels rate‑cut bets; miners shine

Salaries and bonuses

- Lloyds Banking Group hikes bonuses for top investment bank staff by 24%

- NatWest ups bonuses for top staff by 13% as trading unit jumps

Market trends

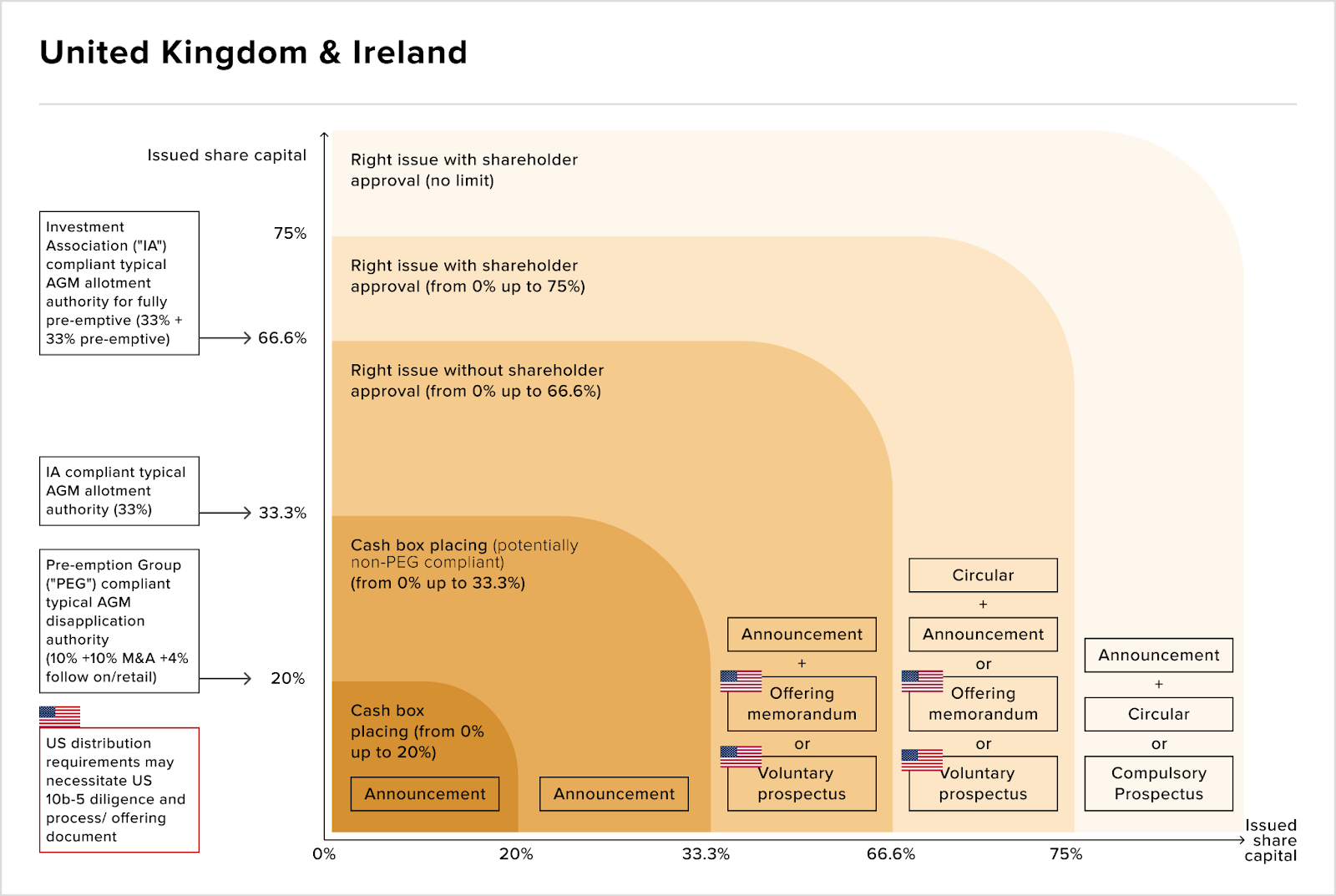

Prospectus reform: a procedural tailwind for listed acquirers

Quietly, the structural change that might have the biggest impact on UK M&A in 2026 is procedural.

Under the new prospectus regime, listed companies can issue shares up to 66.6% of their existing capital without shareholder approval and up to 75% without a full prospectus.

For dealmakers, this removes a long-standing disadvantage for London-listed acquirers, who previously faced circular requirements and approval timelines that continental and US rivals did not.

The direction of travel matters:

- Mega deals above £1bn rose to 34 in 2025, up from 31 in 2024, even as overall deal volume fell 13%;

- PE bidders featured in 44% of public M&A versus 31% the prior year, and US buyers alone accounted for aggregate deal value exceeding the entirety of domestic UK M&A.

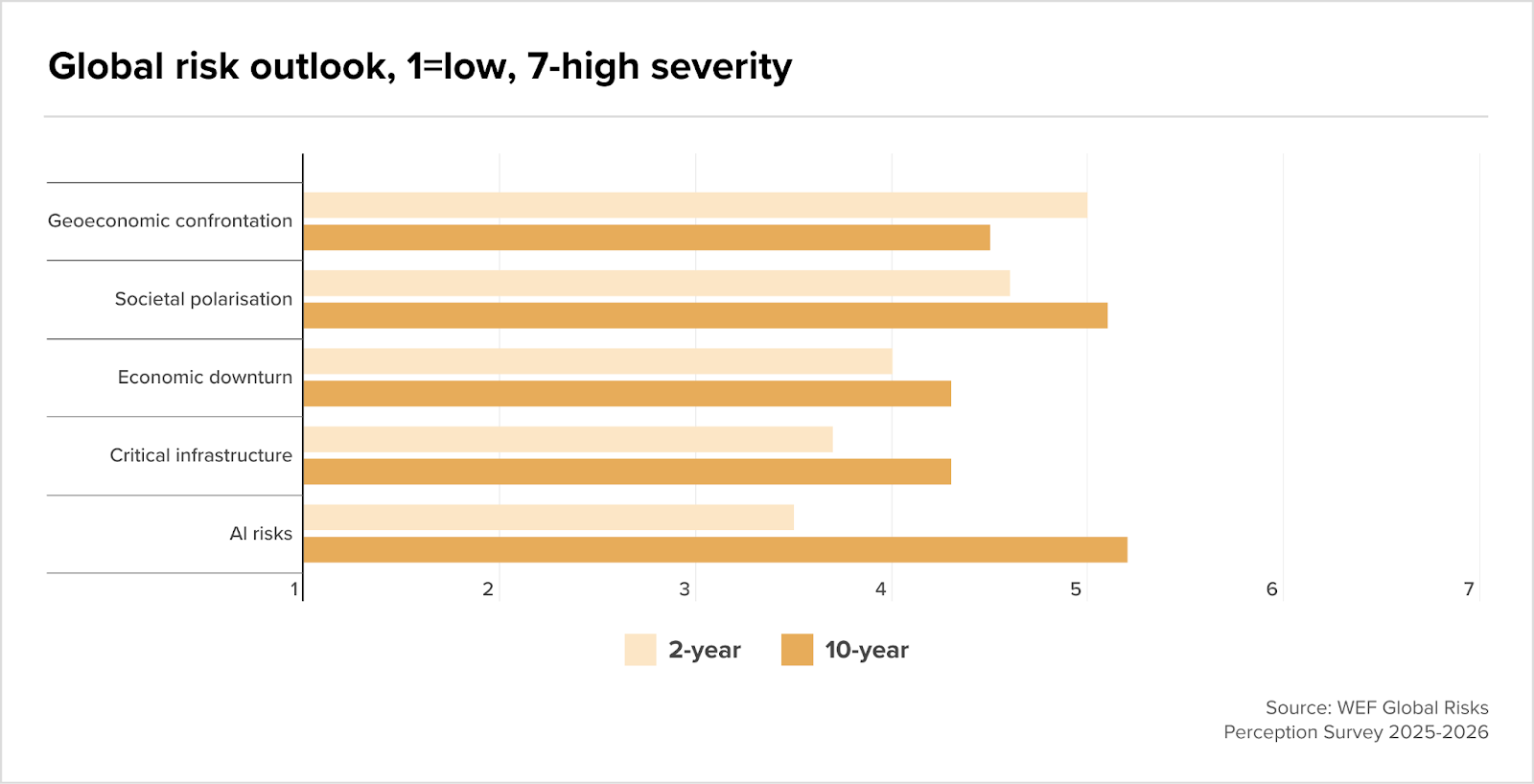

According to UK Finance data, geoeconomic confrontation now sits at the top of the near-term risk rankings, rated close to 5 out of 7 in severity and having jumped from ninth place the prior year.

- The WEF frames the risk as broader than tariffs: it encompasses institutional erosion, the use of sanctions to protect strategic capabilities, and fewer constraints on unilateral action by major powers.

The ten-year picture shifts materially on AI. Near-term severity sits below 3.5, placing it 30th in the immediate rankings.

Over a decade, that figure climbs above 5, the sharpest horizon gap of any risk category. The problems that arise are rooted in gaps in governance, unequal benefit distribution, and labour displacement.

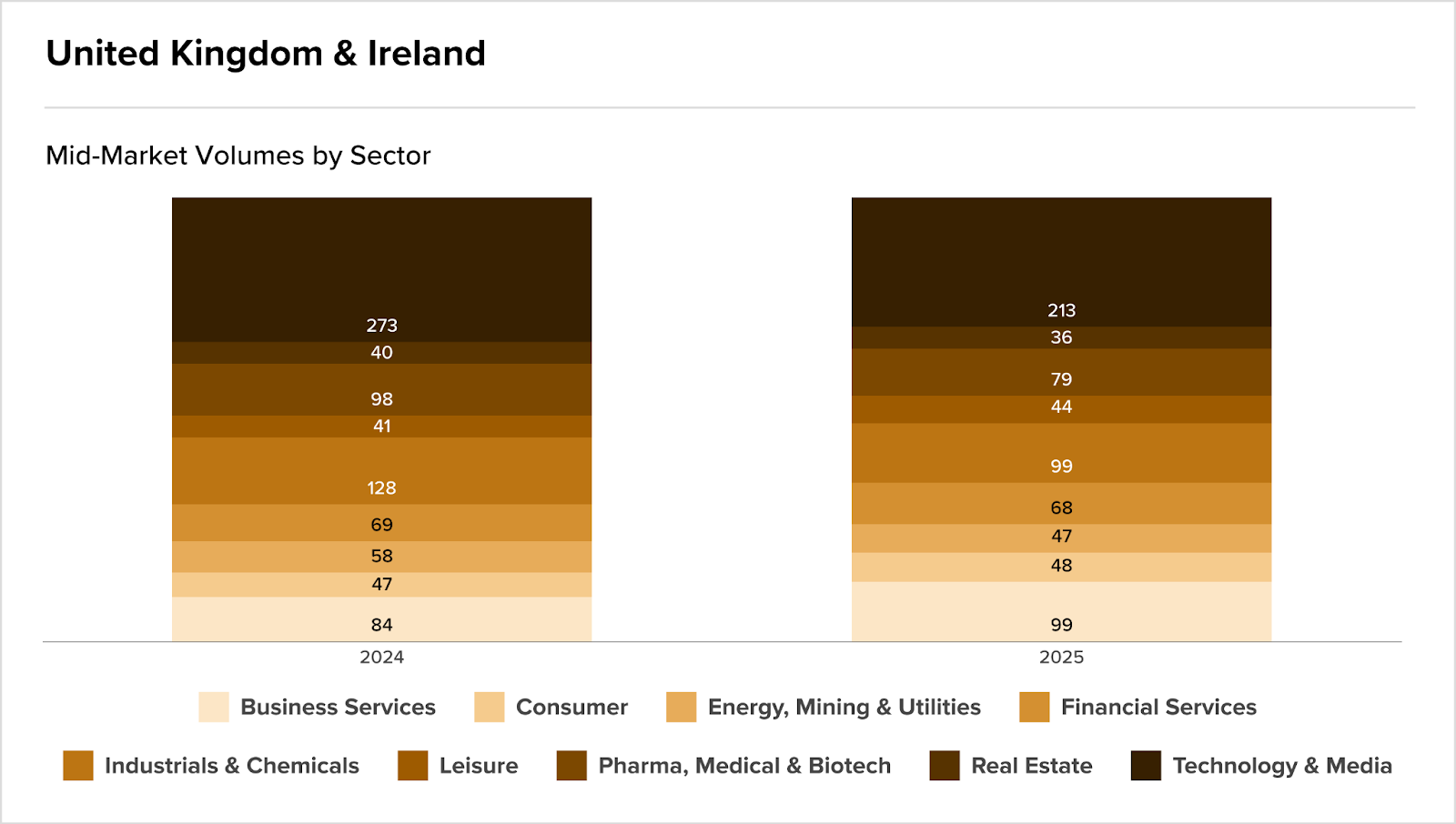

UK & Ireland mid-market: fewer transactions, higher aggregate value

UK and Ireland mid-market M&A closed 2025 with 739 transactions, down 12% on the prior year, yet aggregate deal value climbed 7% to $68bn.

The post-COVID boom of $72bn in 2022 came on the back of a crowded market; last year’s figure arrived through discipline, with bidders cutting noise and targeting fit.

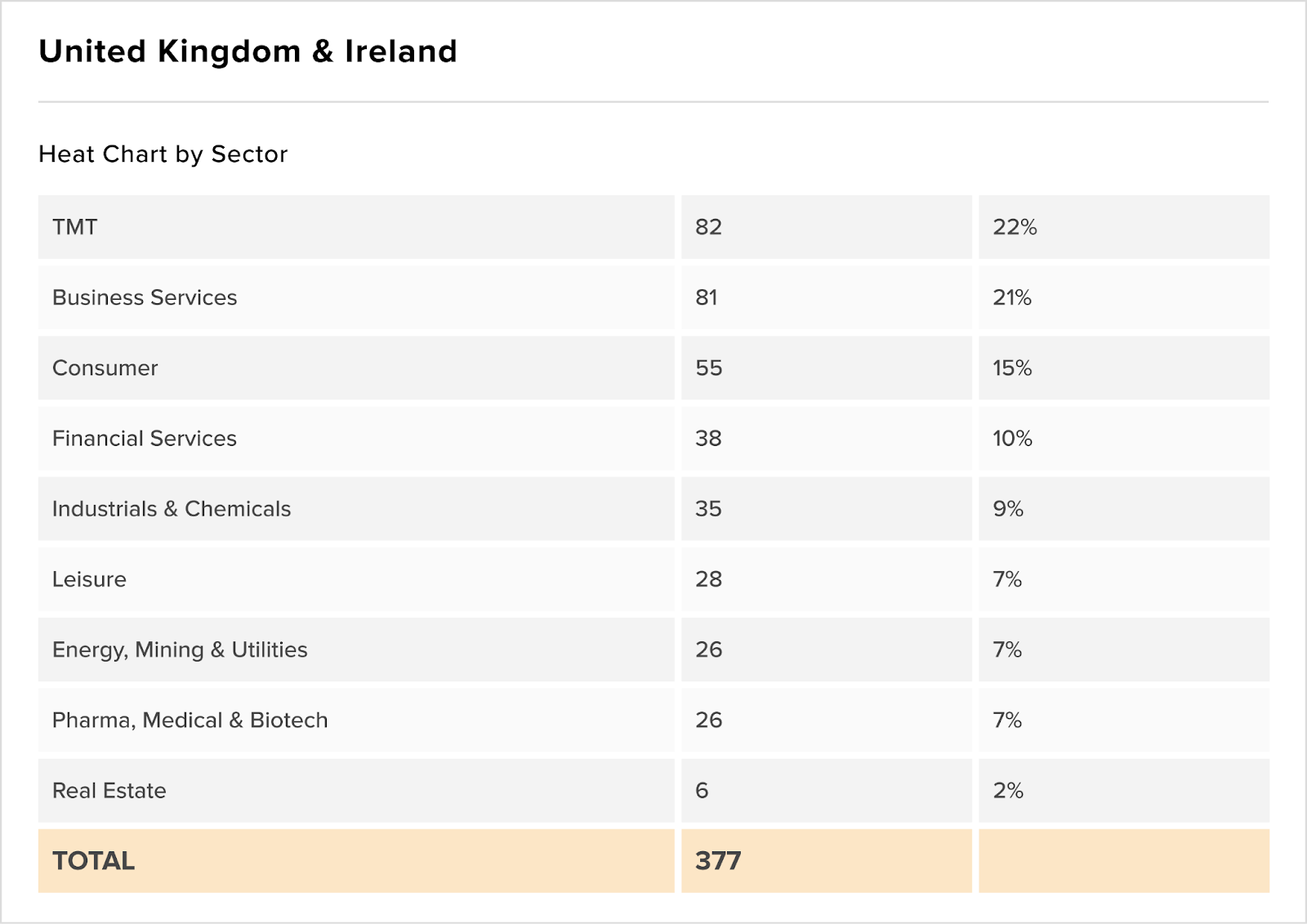

- TMT held the top position at 213 deals

- But TMTs 22% forward pipeline share is now being stalked by Business Services at 21%, up from 84 to 99 transactions across the year.

The assets drawing the sharpest competition sit at the intersection of both: SaaS platforms, cybersecurity, AI infrastructure. In that context, some deals stood out:

- NVIDIA paid $500m for autonomous vehicle software developer Wayve Technologies.

- Wolters Kluwer paid the same for Irish legal-tech firm Brightflag.